MNI US MARKETS ANALYSIS - USD Softer Ahead of NFP Tomorrow

Highlights:

- Approaching the busy central bank slate and US data calendar this week, the dollar is starting the week on the back foot once again.

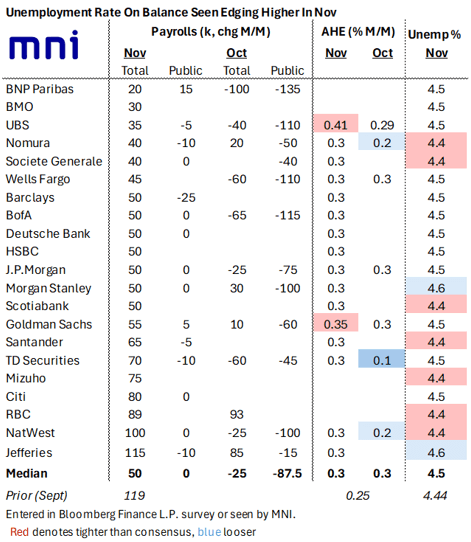

- Our latest survey of primary dealer analyst expectations shows a median estimate of 50k nonfarm payroll gains in November after -25k in October (following +119k in September).

- Fed's Miran and Williams are scheduled to appear later today, while US empire manufacturing and the NAHB housing market index are on the calendar in terms of data.

US TSYS: Modestly Firmer But TY Bear Threat Remains Present

Treasuries are modestly firmer as they pare Friday’s gains by differing amounts, helped by some outperformance of EGBs plus softer crude oil futures. Today sees remarks from NY Fed’s Williams in focus but with NFP/retail sales tomorrow and CPI on Thursday looming large.

- Cash yields are 1-2.2.1bp lower on the day, with the front-end lagging declines.

- Curves remain close to recent steeps, with 5s30s at 110.3bps off Friday’s circa three-month high of 111.8bp.

- TYH6 trades at 112-11+ (+06+) as it holds steady gains seen ahead of London hours, on thin cumulative volumes of 210k.

- A bear threat remains present, with Friday’s 112-03+ coming close to a bear trigger at 111-29 (Dec 10 low). Resistance meanwhile is seen at 112-21 (20-day EMA and 112-23 (Dec 11 high).

- Data: Empire Mfg Dec (0830ET), NAHB housing market index Dec (1000ET)

- Fedspeak: Miran on inflation outlook (0930ET), Williams keynote remarks (1030ET), Miran on CNBC (1100ET)

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump in Mexican Boarder Defense Medal Presentation (1500ET), Trump in Christmas receptions (1615ET & 2015ET)

US OUTLOOK: NFP Growth Eyed at 50k in Nov After -25k in Oct

- Our latest survey of primary dealer analyst expectations shows a median estimate of 50k nonfarm payroll gains in November after -25k in October (following +119k in September).

- Public sector payrolls are seen contracting heavily in October, largely reflecting deferred DOGE layoffs rather than the federal government shutdown, before a relatively flat figure in November. The October public sector range is wide, from -135k (BNP Paribas) to -15k (Jefferies) with a median of -87.5k that lands between -75k and -100k estimates.

- The unemployment rate is on balance seen ticking up to 4.5% in November from an unrounded 4.44% in September (reminder, no Household Survey and therefore no unemployment rate will be published for October).

- Two look for a further upward surprise at 4.6% (MS and Jefferies, the latter despite being the strongest for estimated NFP growth) but risk is generally skewed lower with seven analysts eyeing an unchanged 4.4%.

- Average hourly earning growth is seen relatively steady at 0.3% M/M in both months (vs 0.25% in September) but with risk skewed a little lower for October.

- The full MNI US Payrolls Preview will follow later today.

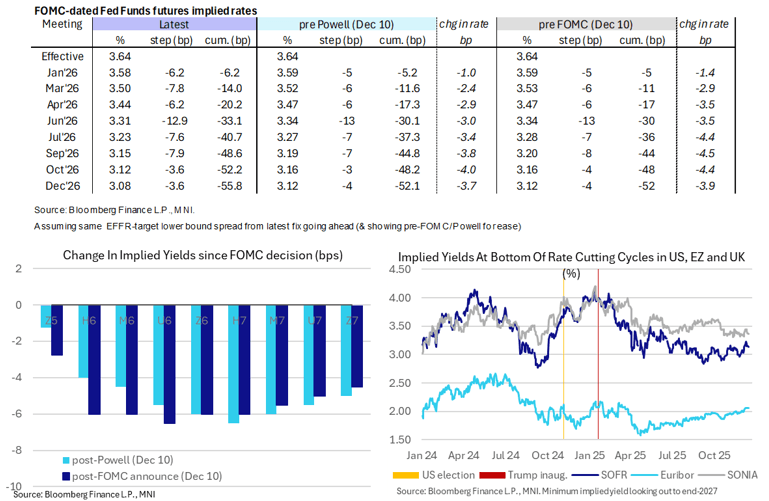

STIR: Williams Watched for Latest Guidance But Key Data Looms Large This Week

- Fed Funds implied rates are broadly unchanged since Friday for 2026 meetings ahead of a session headlined by NY Fed’s Williams but with NFP/retail sales tomorrow and CPI on Thursday looming large.

- Cumulative cuts from 3.64% effective: 6bp Jan, 14bp Mar, 20bp Apr, 33bp Jun, 38.5bp Sep and 56bp Dec.

- SOFR futures are up to 2 ticks firmer looking out to 2027 contracts, with he terminal implied yield of 3.14% (Z6) holding within recent ranges.

- The next Fed Chair race is now seen as a much closer call between Kevin Hassett and Warsh now (53% vs 41% on Polymarket) after Trump told the WSJ in an interview on Friday that he’s leaning toward the two Kevins compared to prior expectations that Hassett held a commanding lead.

- Today sees Fedspeak from Gov. Miran x 2 (outright dove) in his first comments since another dovish dissent last week and NY Fed’s Williams (permanent voter) after his uncharacteristic guidance in November set up last week’s cut.

- 0930ET - Miran on inflation outlook (text tbd, Q&A) – he again dissented for a 50bp cut last week – not a surprise – but more surprisingly was almost certainly behind the marked push lower in the 2026 dot to 2-2.25% from one of two at 2.5-2.75% with the Sept SEP.

- 1030ET – Williams keynote remarks (text + Q&A). The most influential of Fed speakers outside of FOMC commentary in the last inter-meeting period, he said Nov 21: "I view monetary policy as being modestly restrictive, although somewhat less so than before our recent actions. Therefore, I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral, thereby maintaining the balance between the achievement of our two goals.”

- 1100ET – Miran on CNBC

STIR: Focus on How the ECB Responds to Recent Hawkish Repricing on Thursday

- The main intrigue heading into Thursday's ECB decision is how the Governing Council responds to the recent wave of hawkish front-end repricing. ECB-dated OIS now price 6bps of hikes priced through December, with essentially no implied probability of another cut this cycle. Pricing likely hasn't strayed far enough from the ECB's base case to warrant explicit commentary/pushback from President Lagarde, but we think a re-iteration that policy is in a "good place" could temper hike expectations a little - in contrast to meetings earlier this year.

- The policy statement is expected to re-iterate a data-dependent and meeting-by-meeting approach, with primary focus on the updated macroeconomic projections and the balance of risks to inflation and growth. Relative to the September projection round, both growth and inflation outcomes have been higher than expected. As such, analysts expect upward revisions to both GDP and core HICP projections. Headline HICP projections are expected to be broadly steady due to weaker energy prices and the delay to the EU's ETS2 carbon pricing scheme. Projections for 2028 will be presented for the first time, but Governing Council speakers have played down their relevance, owing to still elevated uncertainty.

- Our Policy Team's latest sources piece noted that December meeting communication will seek to reinforce two-way risks around the 2.0% policy rate. Although the bar to another cut has clearly been raised, dovish members of the Governing Council remain cognizant of downside inflation risks, with under delivery of Germany's anticipated fiscal expansion still a risk to monitor.

- Note that December flash PMIs are also due on Tuesday. Focus will be on whether the solid momentum seen in October and November is sustained, setting the stage for another improved GDP reading in Q4.

STIR: Sell-Side Not Expecting Imminent Hawkish Extension in EUR Rates Around ECB

We have flagged some dovish risks around the ECB reiterating that monetary policy is “in a good place” alongside Thursday’s interest rate decision, with the Bank’s updated economic projections set to provide an extra layer of input for markets to trade off. Sell-side notes that we have read generally point to caution when it comes to the idea of a swift extension of last week’s hawkish repricing in EUR STIRs, with some looking to fade the move:

- Bank of America: We stay received Mar ‘26 ECB. Our economists still expect a 25bp cut in March ‘26 vs. market pricing of less than 1bp of cumulative cuts by then. Risks are stronger than expected growth or inflation.

- Goldman Sachs: We do not think EUR front-end steepness out to 2y1y is excessive given the shift in momentum in German activity and elevated long-dated forwards. But the repricing in nominal rates has been abrupt and has outrun signals from traded inflation. In that sense, the key determinant of returns in front-end longs relates to whether and how much the cyclical improvement in Germany - that we expect - is convincing enough to shift the distribution of risk in Euro area inflation. We do think that better cyclical data will floor the inflation distribution and will see EUR core yields drift higher - we remain short Bunds vs. Gilts - but presuming President Lagarde falls short of endorsing hike pricing, risks are tilted towards a consolidation in front-end pricing in the near term.

- Natixis: We continue to expect the ECB to maintain its “we are in a good place” stance, while the market believes that “stability” warrants a risk of a hike next year. We therefore prefer a Euribor Mar ‘26/Dec ‘26 flattener because we think that Lagarde will probably halt the trend, even if GDP growth projections are likely to be revised upward.

SOFR: Mix of Positioning Swings Seen in Futures on Friday

OI data points to short setting dominating in the greens and long cover dominating in the blues in SOFR futures on Friday, with a less coherent positioning picture in the whites and reds as contracts settled in different directions.

| 12-Dec-25 | 11-Dec-25 | Daily OI Change | Daily OI Change In Packs | ||

| SFRU5 | 1,297,497 | 1,287,922 | +9,575 | Whites | -14,844 |

| SFRZ5 | 1,686,273 | 1,705,375 | -19,102 | Reds | -22,971 |

| SFRH6 | 1,396,256 | 1,406,825 | -10,569 | Greens | +32,876 |

| SFRM6 | 1,118,319 | 1,113,067 | +5,252 | Blues | -34,672 |

| SFRU6 | 1,183,616 | 1,184,504 | -888 | ||

| SFRZ6 | 1,125,439 | 1,152,896 | -27,457 | ||

| SFRH7 | 870,470 | 864,323 | +6,147 | ||

| SFRM7 | 767,783 | 768,556 | -773 | ||

| SFRU7 | 824,140 | 804,752 | +19,388 | ||

| SFRZ7 | 831,994 | 828,932 | +3,062 | ||

| SFRH8 | 459,804 | 453,293 | +6,511 | ||

| SFRM8 | 411,534 | 407,619 | +3,915 | ||

| SFRU8 | 389,173 | 384,545 | +4,628 | ||

| SFRZ8 | 291,530 | 327,532 | -36,002 | ||

| SFRH9 | 190,702 | 200,280 | -9,578 | ||

| SFRM9 | 209,794 | 203,514 | +6,280 |

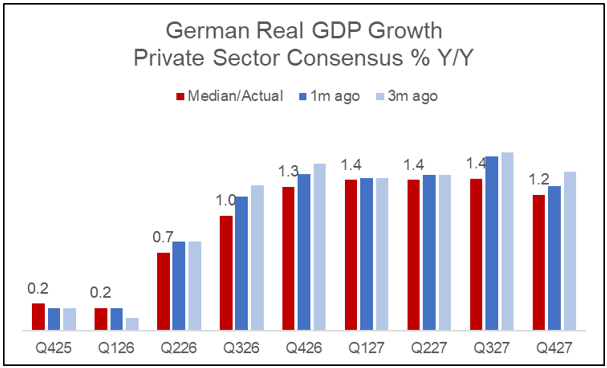

GERMANY: Downward Adjustment of German Growth Forecasts Continues

Private sector German medium-term GDP forecasts have again seen a deterioration with hard data continuing to lag improving sentiment and an apparent stagnation in terms of wider economic reform from the government. The downward revisions across 2026 provide an interesting contrast to the most recent hawkish ECB repricing, and should be weighed against analysts' expectations for upward revisions to the ECB's Eurozone GDP forecasts which are to be published Thursday.

- Updating a median estimate from seven sellside analysts that we track, Y/Y growth is expected to start accelerating in Q2 of next year before topping out at 1.4% Y/Y over the course of 2027. However, these medium-term forecasts have seen downward pressure in recent months, with broad downward revisions of ~0.3pp in most of 2027 comfortably outweighing a marginally higher median for 4Q25.

- This comes after IFO published on Friday a material downside growth revision - to 0.8% Y/Y for 2026 (from 1.3%). 0.8% is exactly where their 2026 view stood right before IFO started incorporating the government's fiscal easing announcement from last March, suggesting this has been crowded out to a large extent by underlying weakness in the private sector. "The German government's measures will help in the short term but are insufficient to expand the production capacities of the German economy in the long term", IFO commented.

- The government also shared their view this morning, concluding that "the German economy continues to face conflicting pressures: on the one hand, external factors are weighing on the economy in the form of weak foreign demand, declining competitiveness, and isolated bottlenecks for certain intermediate goods; on the other hand, there are signs of a gradual stabilization of the domestic economy, supported in part by the increasingly noticeable fiscal stimulus measures implemented recently".

FRANCE: Senate to Vote on 2026 PLF Today, But National Assembly Support Unlikely

French politics remains a focus, with the year-end deadline for passing a 2026 budget nearing. The 2026 State budget (PLF) is being voted on by the Senate today. Assuming the Senate’s amended version of the PLF is passed, a Joint Committee (formed of seven parliamentarians and seven senators) will be convened on Friday to try and reach an upper/lower house compromise. This seems unlikely - on November 21, the National Assembly voted 404 to 1 (with 84 abstentions) against adoption of the first draft of the PLF.

- We wrote last week that the government is likely to face difficulties passing the PLF, which is a more contentious bill than the Social Security budget (PLFSS). As such, PM Lecornu is likely to submit a ‘Special Law' on Friday, which would allow the government to roll over taxes and spending at 2025 levels until a new budget can be agreed upon in the new year (assuming a compromise is not reached in the National Assembly before year-end).

- Last week, Socialist First Secretary Faure struck a pessimistic tone with respect to the PLF: "it's different" because "voting for it would bring us into the majority."… "We are open to finding compromises to avoid paralyzing the country, but there will be no confusion: we are in the opposition," …."at this stage, [Faure] doesn't even see what would justify abstention." (see here)

- Meanwhile, Green Leader Marine Tondelier said yesterday that “There is no reason today to vote anything other than against because what is happening is unacceptable and is leading our country straight into the hands of the National Rally, describing the PLF as "unfair and incomprehensible." (see here)

- On Friday, the Senate rejected the 2026 Social Security Bill (PLFSS) on a second reading. However, this was fully expected, and the bill now passes back to the National Assembly for a final vote tomorrow. The Senate’s rejection can essentially be circumvented, with the National Assembly expected to narrowly adopt the PLFSS in line with the December 9 vote.

FOREX: Negative Dollar Bias Dominates, USDJPY Returns to 155.00

- Approaching the busy central bank slate and US data calendar this week, the dollar is starting the week on the back foot once again. Moves for the dollar index have been relatively contained, with the DXY just 0.1% lower on the session, although we remain within 20 pips of last week’s pullback lows. The softer dollar backdrop has allowed the likes of gold and silver to extend higher, rising 1% and 3% respectively, while the Japanese Yen outperforms across the G10.

- USDJPY has been pressured by lower core yields on Monday and the monthly Tankan survey / wage report reinforcing the expectations for a BOJ hike this week. USDJPY has exhibited a 105-pip range, with the latest dip below 155 now probing last week’s lows. Below here, the December 05 low at 154.35 and the 50-day EMA at 153.95 represent an important support area as we navigate both the US data releases and BOJ meeting.

- At the other end of the G10 leaderboard, NZD has notably declined amid comments from the newly appointed RBNZ Governor. Breman said the forward path for the OCR published in the November policy statement “indicates a slight probability of another rate cut in the near term”, pushing back against any expectations for a hike in 2026. NZDUSD is 0.35% lower on the session and back below 0.58, while AUDNZD briefly rose to a recovery high of 1.1520.

- Elsewhere, USDKRW has extended session losses to nearly 1% after South Korea’s National Pension Service said it will conduct its strategic FX hedging in a “flexible” manner. USDKRW gathered downside momentum through the overnight lows at 1470 and notably, we are now below 20-day EMA support – a close below this average would be the first since September.

- Fed's Miran and Williams are scheduled to appear later today, while US empire manufacturing and the NAHB housing market index are on the calendar in terms of data.

EQUITIES: Short-Term Cycle Highs for E-Mini S&P Last Week Strengthens Bull Theme

- A bull cycle in Eurostoxx 50 futures remains intact and the contract is trading closer to its recent highs. Price is also trading above the 20- and 50-day EMAs, and has cleared 5742.40, 76.4% of the Nov 13 - 21 bear leg. The breach of this price point paves the way for an extension towards 5825.00, the Nov 13 high and the bull trigger. First key support to watch lies at 5641.23, the 50-day EMA.

- A bull cycle in S&P E-Minis remains intact and a fresh short-term cycle high last week strengthens the bull theme. Sights are on 7014.00, the Oct 30 high and bull trigger. Clearance of this hurdle would confirm a resumption of the primary uptrend. This would open the 7044.82 area, a Bollinger band resistance. Initial firm support to watch lies at 6828.90, the 50-day EMA. Key support and a reversal trigger is at 6583.00, the Nov 21 low.

COMMODITIES: MA Studies for WTI Highlights a Dominant Medium-Term Downtrend

- A bearish theme in WTI futures remains intact and the move down last week reinforces this theme. Note that moving average studies are in a bear-mode position, highlighting a dominant medium-term downtrend. A continuation of the bear leg would open key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high.

- Gold traded higher last week, reinforcing a bullish theme. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4069.6. Clearance of this EMA would signal scope for a deeper retracement. Attention is on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 15/12/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 15/12/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 15/12/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 15/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 15/12/2025 | 1330/0830 | *** | CPI | |

| 15/12/2025 | 1430/0930 | Fed Governor Stephen Miran | ||

| 15/12/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 15/12/2025 | 1530/1030 | New York Fed's John Williams | ||

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/12/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 16/12/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | Italy Final HICP | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI (f) | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Services PMI (f) | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Composite PMI (f) | |

| 16/12/2025 | 1000/1100 | * | Trade Balance | |

| 16/12/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 16/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 16/12/2025 | 1000/1100 | Foreign Trade | ||

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (f) | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Services Index (f) | |

| 16/12/2025 | 1500/1000 | * | Business Inventories | |

| 16/12/2025 | 1730/1230 | BOC Gov Macklem speech in Montreal | ||

| 17/12/2025 | 2350/0850 | * | Machinery orders |