MNI US MARKETS ANALYSIS - USD Remains Inside S/T Downtrend

Highlights:

- Treasuries await 5y supply after smooth short-end sale

- China's Shein switch IPO venue, could have broader market implications

- Light calendar keeps focus on simmering trade, geopolitical tensions

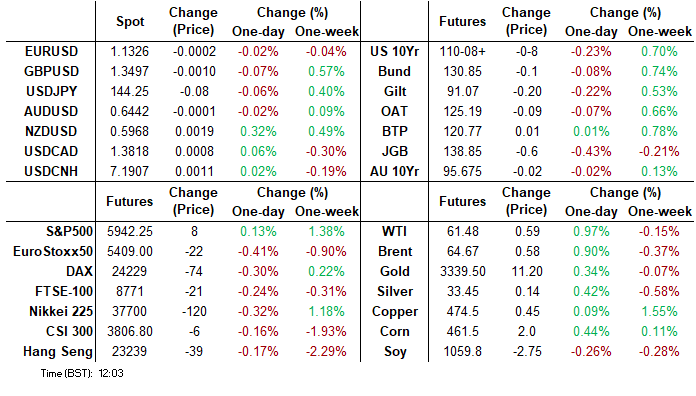

US TSYS: Bear Steeper, Softer Impulse Following Weak JGB Auction

- Treasuries are bear steeper, with the long end seeing some downward pressure following a weak 40Y JGB auction that pared some of yesterday’s gains on Reuters reporting around potential issuance plan tweaks.

- Today sees some attention on 5Y supply at 1400ET after yesterday’s 2Y was solid, trading through by 1bp. Last month’s 5Y traded through by 1bp and the bid-to-cover ticked up after what had previously been the lowest in nine auctions.

- Cash yields are 0.4-2.6bp lower on the day.

- Some steepening is mechanically boosted by the new 2Y benchmark after yesterday’s auction.

- 2s10s for instance is 4.3bp higher on the day at 51bps vs 5s30s just 0.8bp higher at 92.8bp as it continues to hold off last week’s multi-year highs of 101bps.

- TYU5 trades at 110-10 (-08), taking the front contract but with volumes of only 195k despite the ongoing roll.

- Resistance is seen at 110-21+ (50-day EMA) before a key 110-23 (May 16 high) but the bear cycle remains in play with support at 109-12+ (May 22 low).

- Data: MBA mortgage applications (0700ET), Richmond Fed mfg May (1000ET), Dallas Fed services May (1030ET)

- Fedspeak: FOMC minutes (1400ET)

- Coupon issuance: US to sell $28bn 2Y FRN re-open (1130ET), US to sell $70bn 5Y notes - 91282CNG2 (1300ET)

- Bill issuance: US to sell $60bn 17W bills (1130ET)

- WH Economic Council Chair Miran late yesterday stated that whilst it is uncertain where final tariff rates will end up, a 10% rate isn't large enough to have adverse effects on the economy. He compared the tariff move to a 10% shift in the exchange rate (although noted that they aren't the exactly the same), while stating that revenue inflow from the tariffs will help alleviate fiscal deficit concerns (per BBG).

STIR: Fed Rates Unchanged, FOMC Minutes Made Stale By Trade Developments

- Fed Funds implied rates are essentially unchanged on the day, still close to the most hawkish levels seen since February.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 6.5bp Jul, 18bp Sep, 31.5bp Oct and 48bp Dec.

- The SOFR implied terminal yield is 3bp higher on the day at 3.29% after yesterday’s 3.26% was the lowest close since May 9.

- NY Fed’s Williams (permanent voter) in a fireside chat yesterday: can’t take well-anchored inflation expectations for granted and wants the whole curve of inflation expectations “well behaved”. We’re still in a low neutral rate globally but there is a lot of uncertainty around neutral rate estimates.

- Today sees the FOMC minutes at 1400ET from the May 6-7 FOMC meeting. They are likely to be perceived as stale after the US-China trade de-escalation on May 12 before last week’s threat of 50% tariffs on the EU and subsequent one-month delay in when they might start.

STIR: OI Points To Long Setting Bias In Most SOFR Futures Early This Week

OI data indicates a general bias towards net long setting in SOFR futures between Friday & Tuesday settlements, although there was a pocket of net short cover across the reds.

| 27-May-25 | 25-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,069,748 | 1,070,469 | -721 | Whites | +48,701 |

SFRM5 | 1,394,695 | 1,364,253 | +30,442 | Reds | -32,944 |

SFRU5 | 1,102,147 | 1,097,821 | +4,326 | Greens | +29,523 |

SFRZ5 | 1,064,203 | 1,049,549 | +14,654 | Blues | +14,867 |

SFRH6 | 763,368 | 764,236 | -868 |

|

|

SFRM6 | 722,043 | 730,060 | -8,017 |

|

|

SFRU6 | 723,409 | 736,714 | -13,305 |

|

|

SFRZ6 | 837,016 | 847,770 | -10,754 |

|

|

SFRH7 | 686,622 | 683,982 | +2,640 |

|

|

SFRM7 | 592,974 | 584,225 | +8,749 |

|

|

SFRU7 | 421,404 | 412,221 | +9,183 |

|

|

SFRZ7 | 418,615 | 409,664 | +8,951 |

|

|

SFRH8 | 279,927 | 288,725 | -8,798 |

|

|

SFRM8 | 197,659 | 201,997 | -4,338 |

|

|

SFRU8 | 161,649 | 152,216 | +9,433 |

|

|

SFRZ8 | 193,593 | 175,023 | +18,570 |

|

|

HONG KONG STOCKS: Shein IPO Venue Switch Could Have Broader Market Implications

Chinese eCommerce firm Shein is said to be switching focus for their IPO listing from London and to Hong Kong after the company failed to gain the approval of Chinese regulators, and in particular the CSRC, according to Reuters sources.

- The newsflow is notable for several reasons: Firstly, a Shein IPO in London would have been the largest since Glencore in 2011 and the most significant listing since Deliveroo's volatile IPO in 2021 (who are now destined to leave the market this year after DoorDash announced their plans to buy the company). As such, Shein's switch in focus is detrimental to London's standing as a global financial hub and means the city misses out on another sizeable float.

- Secondly, this redirects focus to the HK market. A Shein IPO here of similar size would equate to a $5-9bln raise on a $50-90bln valuation and could almost double the already-strong YTD fundraising on the exchange (running at just under $10bln).

- With a placement seen as likely later this year (although subject to regulatory approval), focus may shift to potential distortions in HKD cash demand: Sizeable demand for securities can help narrow the HKD forward discount, which has proved sensitive in recent years to a pick-up in capital markets activity, as the uptick in cash demand in turns adds upward pressure to HIBOR. This could relieve pressure on USD/HKD spot, which is pressing toward the weak-side of the trading band after recent HKMA intervention.

- Lastly, the valuation of a Shein IPO is seen as highly sensitive to global 'de minimis' rules. Their business model relies on duty exemptions given their high volume, low price strategy - keeping focus on EU and US rulings over parcel levies and trade tension sensitivities.

RUSSIA: Lavrov-New Round Of Ukraine Talks To Be Announced "In Very Near Future"

State-run Tass reports Foreign Minister Sergey Lavrov saying that Russia will confirm the dates of the next round of direct talks with Ukraine on reaching a ceasefire "in the very near future," Speaking in Moscow, Lavrov says "At these negotiations on May 16 in Istanbul, when they resumed, we insisted on the abolition of all these discriminatory laws and will continue to do so in the next round of direct negotiations," Lavrov also confirmed that "A neutral and nuclear-free status for Ukraine is one of Russia's key demands.”

- Both Ukraine and the United States are awaiting a formal memorandum outlining Russia's demands for enacting any ceasefire. While both Kyiv and Washington, D.C., wait, Russia continues to make advances in the Sumy region of northeastern Ukraine. This sits across the border from the Kursk oblast of Russia, which was for some time occupied by Ukrainian forces.

- On 27 May, Ukrainian President Volodymyr Zelenskyy warned that some 50k Russian troops were massing along the border with the Sumy region. Last week, Russian President Vladimir Putin spoke of establishing "buffer zones" along the border. Zelenskyy claimed that the Russian troops were some of Moscow's "largest, strongest forces".

- Russia launching a summer offensive and forgoing ceasefire talks could draw a robust response from the US. While isolationists within the Trump administration have sought to pull back from any further commitments to Ukraine's defence, the president's recent comments regarding Russian attacks could suggest secondary/banking sanctions on Russia are not unfeasible.

EUROPE ISSUANCE UPDATE:

Spain syndication: Final terms

- E13bln of the new Oct-35 Obli. Books above EU120b, spread: MS+7 (guidance was SPGB+9 area)

UK auction results

- Green supply saw solid demand, which allowed gilts to stabilise this morning.

- GBP2.75bln of the 0.875% Jul-33 Green Gilt. Avg yield 4.511% (bid-to-cover 3.56x, tail 0.3bp).

German auction results

- E1.5bln (E1.398bln allotted) of the 1.00% May-38 Bund. Avg yield 2.8% (bid-to-offer 2.20x; bid-to-cover 2.36x).

- E500mln (E490mln allotted) of the 4.75% Jul-40 Bund. Avg yield 2.85% (bid-to-offer 5.68x; bid-to-cover 5.80x).

FOREX: USD Index Fades Off High, Keeps Price Inside S/T Downtrend

- The USD Index has faded back just below the 100.00 handle to erase overnight gains and keep the price inside the downtrend drawn off the failed test of the 50-dma back in mid-May. Headlines and newsflow have been few and far between for markets, with a semblance of stability for the Japanese yield curve helping contain markets, as well as reduced newsflow on the flow of trade deals with the US.

- NZD is outperforming following the RBNZ rate decision. While the bank cut rates - as expected - by 25bps to 3.25%, the board suggested that the base rate is near the 'neutral' zone, which may limit the space for further rate cuts ahead. NZD/USD bounced well off the overnight low of 0.5924 in response, but is yet to make a test on yesterday's 0.6007 highs.

- CAD is among the poorest performers in G10, slipping despite a more favourable backdrop for oil prices. Brent crude prices are more stable above the week's lows, however slippage across core equity benchmarks is undermining the recent pick-up in short-term downward momentum for USD/CAD (evident in the 50-dma showing below the 200-dma last week).

- Month-end flows should pick up through US hours, particularly as today marks month-end value date. We see a series of sizeable option strikes set to expire at today's cut that could keep a lid on spot markets in a quiet news backdrop: EUR/USD sees $1.1300(E1.4bln), $1.1390-00(E1.4bln), while USD/JPY trades in close proximity to Y143.90-00($1.9bln).

- The Fed minutes is unlikely to garner too much market focus later today, with the release covering the most recent, relatively uneventful, rate decision. The data slate is similarly quiet, as is the speaker schedule - with only BoE's hawk Pill set to speak at 1600BST/1100ET, however he is likely to repeat comments made in recent weeks.

EURGBP: Stretched GBP Valuation as BoE-ECB Pricing Spread Meeting Resistance

- EUR/GBP remains well within range of recent lows as the cross holds close the entirety of the tick lower off the late May high at 0.8459. This keeps short-term momentum measures pointed lower, despite the price finding support into the 0.8383 200-dma.

- We wrote a few weeks ago that a UK-US trade deal is unlikely so shift the near-term narrative for GBP, meaning any post-deal announcement strength could prove short-lived. Since then, GBP has proved more resilient than expected - so much so that the currency remains the most stretched in developed markets on a REER basis, still ahead of EUR.

- It's BoE pricing that's backing up this stretched valuation, with the Dec-25 SONIA-EURIBOR spread still in focus. However this pricing may also suggest the room for EUR/GBP to fall further here may be limited. We see that the spread may struggle to meaningfully push through resistance at 213.5bps (Jan 14 close) without a fresh re-escalation of trade tensions - which has prevented EUR/GBP from further follow-through sales, keeping EUR/GBP above this week's lows for now.

OPTIONS: Expiries for May28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1300(E1.4bln), $1.1390-00(E1.4bln), $1.1445-55(E1.0bln), $1.1500-20(E1.4bln)

- USD/JPY: Y141.00($1.3bln), Y141.75-80($990mln), Y143.00($2.0bln), Y143.90-00($1.9bln), Y145.00($1.8bln)

- AUD/USD: $0.6325-30(A$500mln)

- NZD/USD: $0.5725(N$1.1bln)

EQUITIES: MA Studies for Eurostoxx 50 Futures Remain in a Bull-Mode Position

- The trend cycle in Eurostoxx 50 futures remains bullish and the recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear uptrend and recent gains maintain the sequence of higher highs and higher lows. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Key support to watch lies at 5238.48, the 50-day EMA. Clearance of this average would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and the latest pullback appears to have been a correction. Last Friday’s sell-off resulted in a print below the 20-day EMA, at 5794.26. A key support lies at 5728.00, the 50-day EMA. A clear break of this average is required to highlight a stronger reversal and signal scope for a deeper retracement. Sights are on the bull trigger at 5993.50, the May 20 high.

COMMODITIES: Recovery for WTI Futures Since Apr 9 Still Appears Corrective

- WTI futures traded to a fresh S/T cycle high last Wednesday before finding resistance. The recovery since Apr 9, appears corrective. Key resistance to watch is $62.63, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal and open $65.82, Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. The price pattern on May 21 is a shooting star - a bearish signal.

- Recent gains in Gold signals the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are unchanged, they remain bullish. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. A continuation higher would open $3435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/05/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/05/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/05/2025 | 1500/1600 | BOE's Pill on monetary policy panel at Austria National Bank / SUERF | ||

| 28/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 28/05/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/05/2025 | 1800/1400 | FOMC Minutes | ||

| 28/05/2025 | 1800/1400 | *** | FOMC Minutes | |

| 28/05/2025 | 0000/2000 | New York Fed's John Williams | ||

| 29/05/2025 | 0130/1130 | * | Private New Capex and Expected Expenditure | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 29/05/2025 | 0900/1000 | BOE's Breeden opening remarks at conference on non-bank financial sector and financial stability | ||

| 29/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 29/05/2025 | 1230/0830 | * | Current account | |

| 29/05/2025 | 1230/0830 | * | Payroll employment | |

| 29/05/2025 | 1230/0830 | *** | GDP | |

| 29/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 29/05/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 29/05/2025 | 1445/1545 | BOE's Saporta panellist on hedge funds' role in recent crises | ||

| 29/05/2025 | 1500/1100 | ** | DOE Weekly Crude Oil Stocks | |

| 29/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 29/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 29/05/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/05/2025 | 1800/1400 | Fed Governor Adriana Kugler | ||

| 29/05/2025 | 1900/2000 | BOE's Bailey speech and fireside chat at Irish IAIM Dinner | ||

| 29/05/2025 | 2000/1600 | San Francisco Fed's Mary Daly |