MNI US MARKETS ANALYSIS - USD Lower for 4th Day on Shutdown

Highlights:

- Shutdown begins in earnest, helps usher in 4th day of USD losses

- Further meetings and votes expected, but progress very unlikely with little pressure on dealmaking

- BoJ's Tankan survey endorses BoJ tightening

US TSYS: Closed Until Further Notice

- US Government closed until further notice. First closure since Pres Trump's first term from Dec 22, 2018 to Jan 25, 2019. An estimated 750,000 federal employees expected to be furloughed according to Congressional Budget Office (CBO) based on federal agencies' contingency plans.

- Most of today's data will be released as scheduled as most provided by private sector. Exception: US Census Bureau's Construction Spending delayed until government reopens. Friday's employment report will be suspended as well, according to the BLS.

- The BLS plans to "suspend all operations. Economic data that are scheduled to be released during the lapse will not be released. All active data collection activities for BLS surveys will cease. The BLS website will not be updated with new content or restored in the event of a technical failure during a lapse." LINK

- Treasuries are trading steady to modestly mixed w/ Bonds lagging 5s-10s: Tsy Dec'25 10Y contract (TYZ5) currently trades at 112-17 (+1) on average cumulative volumes of 275k. 10Y yield at 4.1503% (+.0000). Curves twist steeper: 2s10s +.807 at 54.798, 5s30s +2.462 at 101.31.

- A short-term bear cycle in Treasury futures remains in play. Recent weakness has resulted in a print below the 50-day EMA, currently at 112-10+. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is unchanged, at 113-00, the Sep 24 high.

- Economic Data: MBA Mortgage Applications (0700ET), ADP Employment Change (0815ET), S&P Global US Manufacturing PMI (0945ET) and ISMs (1000ET).

- Treasury Auctions: $67B 17W bills at 1130ET.

- Fedspeak: Richmond Fed Barkin moderated discussion on economy (text) (1215ET), Chicago Fed Goolsbee radio interview Marketplace (1700ET).

- Politics: WH Press Sec Leavitt briefing (1300ET). President Trump to sign executive orders (1630ET) - closed to press. Expect to see social media posts from President Trump, however.

[US GOVERNMENT SHUTDOWN]: This morning, the US government shut down for the first time since 2018-19, after the Senate rejected a House-passed Continuing Resolution to extend FY25 government funding through November. The Senate also rejected a competing Democratic funding bill that would extend expiring Obamacare subsidies, among a raft of healthcare measures.

- There are no ongoing negotiations or meetings planned today, but Senate Majority Leader John Thune (R-SD) is expected to hold a third vote on both bills at 11:00 ET 16:00 BST. They are expected to fail again.

- Our most up-to-date coverage on the shutdown here: https://media.marketnews.com/MNIPOLRISK_Govt_Shutdown_Underway_b47a8b77c4.pdf

SOFR: Net Long Setting Most Prominent On Tuesday

OI data suggests that net long setting dominated through the blue pack of the SOFR futures strip as contracts rallied on Tuesday, with only fairly limited rounds of net short cover seen.

| 30-Sep-25 | 29-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,434,715 | 1,436,478 | -1,763 | Whites | +24,410 |

SFRZ5 | 1,486,770 | 1,481,845 | +4,925 | Reds | +19,326 |

SFRH6 | 1,184,903 | 1,178,018 | +6,885 | Greens | +12,007 |

SFRM6 | 1,030,118 | 1,015,755 | +14,363 | Blues | +510 |

SFRU6 | 941,016 | 924,107 | +16,909 |

|

|

SFRZ6 | 1,023,265 | 1,034,952 | -11,687 |

|

|

SFRH7 | 777,640 | 767,774 | +9,866 |

|

|

SFRM7 | 781,775 | 777,537 | +4,238 |

|

|

SFRU7 | 679,305 | 672,566 | +6,739 |

|

|

SFRZ7 | 734,732 | 723,765 | +10,967 |

|

|

SFRH8 | 414,198 | 416,385 | -2,187 |

|

|

SFRM8 | 355,013 | 358,525 | -3,512 |

|

|

SFRU8 | 284,370 | 278,252 | +6,118 |

|

|

SFRZ8 | 299,666 | 300,676 | -1,010 |

|

|

SFRH9 | 189,417 | 189,408 | +9 |

|

|

SFRM9 | 172,129 | 176,736 | -4,607 |

|

|

US TSY FUTURES: Short Setting Further Out The Curve Dominated On Tuesday

OI data points to a mix of long setting (TU), short cover (FV) & short setting (TY through WN) as the Tsy curve twist steepened on Tuesday, with the latter dominating, accounting for an $11.3mln DV01 equivalent shift in net positioning.

| 30-Sep-25 | 29-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,568,610 | 4,545,811 | +22,799 | +772,151 |

FV | 6,641,928 | 6,683,876 | -41,948 | -1,839,602 |

TY | 5,458,585 | 5,436,020 | +22,565 | +1,469,908 |

UXY | 2,450,087 | 2,429,244 | +20,843 | +1,821,149 |

US | 1,837,844 | 1,818,108 | +19,736 | +2,788,969 |

WN | 2,054,194 | 2,026,201 | +27,993 | +5,194,247 |

|

| Total | +71,988 | +10,206,822 |

EUROPE ISSUANCE UPDATE:

Ireland To Hold 1 Bond Auction In Q4

- NTMA has confirmed that it will hold one auction in Q4-25, on Thursday 9 October. Details will be confirmed on Monday 6 October.

- We had pencilled in 0-1 auctions, but think that the market was looking for no more auctions this year given that the NTMA did not hold any auctions in Q4 in each of 2022, 2023 and 2024 after reaching the bottom of the funding target range.

UK auction results

- GBP1.6bln of the 1.125% Sep-35 Linker. Avg yield 1.673% (bid-to-cover 3.09x).

German auction results

- E5bln (E3.807bln allotted) of the 2.60% Aug-35 Bund. Avg yield 2.72% (bid-to-offer 0.94x; bid-to-cover 1.23x).

EGB FUNDING UPDATE: DFA Sees E500bln+ Funding Requirements

DFA (German DMO) sees "federal government's financing requirements will amount to E500bln annually in the coming years and are set to rise even further" according to an interview in newspaper FAZ. For comparison, German 2024 gross issuance for the federal core budget (excl. special funds) stood at E381.8bln. The figure does not come as a surprise given the ongoing fiscal easing in the country.

Some key highlights from the interview below:

Q: Are there already [funding] plans for 2026?

A: We are currently working on that. We will publish our issuance plans for 2026 in December. We had the highest financing volume in 2023, when the federal government sold bonds worth €500 billion. That is the order of magnitude we expect to see in borrowing over the next few years.

Q :So you expect new federal securities worth €500 billion annually over the next five years?

A: Diemer: Yes, and this figure may even increase slightly. We definitely expect financing requirements to grow over the next few years.

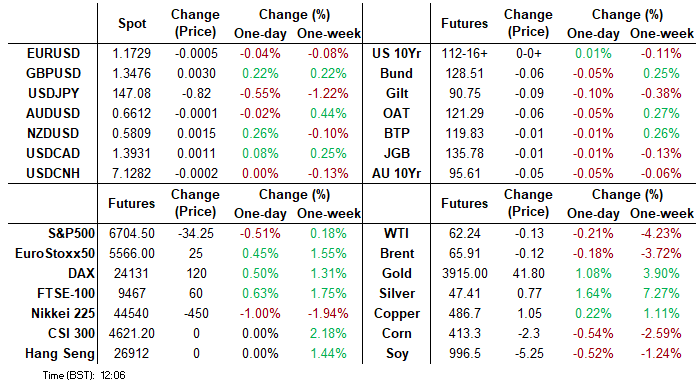

FOREX: Government Shutdown Tips USD Lower for 4th Session, JPY Main Beneficiary

- The initial impact of the US government shutdown have proved negative for the USD: the USD Index is lower for a fourth consecutive session, pressing prices toward the late September lows of 97.221, but still has someway to go before any test of the cycle and pullback low into 96.218.

- How the government shutdown impacts markets more broadly may be defined by availability of data and the longevity of such a shutdown. Given the higher-than-expected current run rate for growth in the US, a prolonged shutdown will almost certainly have a slowing effect on the economy in early Q4. While this Friday's NFP data will almost certainly be delayed (and possibly the US CPI print on October 15th), the scarcity of data is unlikely to steer the FOMC away from a further 25bps rate cut in October, currently priced at ~24bps.

- The JPY is the strongest currency in G10, gaining amid the uncertainty stemming from the US government shutdown as well as the drift off highs for global equities. A stronger-than-expected Tankan manufacturing sentiment index overnight adds a further tailwind, endorsing BoJ tightening in the medium-term. The e-mini S&P is off just over 0.5% at pixel time, putting futures over 50 points off the alltime high. CAD/JPY is through several key levels as a result, clearing clustered horizontal support layered between 105.95 - 106.01.

- Focus for the session ahead rests on any confirmation from the Federal Government that incoming data releases will be delayed - a very likely outcome - but also any clues on the longevity of the current shutdown

EUR: Phase of EUR Weakness Stands Out, EUR/USD Within Range of Sizeable Strike

EUR selling pressure helps tip EUR/USD, EUR/JPY and EUR/GBP through to new daily lows. Little headline flow or news to trigger the phase of EUR weakness here, although it does coincide with Bund futures creeping back to flat on the day, as mentioned above. Gov shutdown risks and the BoJ Tankan survey have been the primary drivers so far today, but the latest phase of EUR weakness stands out somewhat - but looks largely flow driven at this stage.

- Futures markets show a decent pick-up in interest in EUR selling 1118BST, which marked some of the best activity of the session so far, even including the price action across the PMI and HICP releases. Over 3k EUR Z5 futures contracts traded into the session low for a cash equivalent of just below E500mln.

- The fade in price tips spot toward some of the more sizeable options interest rolling off at today's cut, with E2.4bln expiring between $1.1700-10 today.

OPTIONS: Expiries for Oct01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-10(E3.3bln), $1.1700-10(E2.2bln), $1.1750-60(E2.1bln), $1.1775(E709mln), $1.1791-05(E1.9bln), $1.1900(E1.3bln), Y147.50($651mln), Y148.65-75($1.0bln)

- USD/JPY: Y146.15($864mln), Y146.40-50($1.7bln)

- EUR/JPY: Y175.00(E802mln)

- EUR/GBP: Gbp0.8780(E599mln)

- AUD/USD: $0.6600-10(A$1.1bln), $0.6700(A$1.6bln)

- USD/CAD: C$1.3900-10($655mln)

- USD/CNY: Cny7.1900($599mln)

EQUITIES: EuroStoxx 50 Futures Strike New Highs on Closing Basis

- Eurostoxx 50 futures maintain a bullish theme. This week’s gains have resulted in a breach of key resistance and the bull trigger at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend and paves the way for a climb towards 5564.82, a Fibonacci projection. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Initial firm support lies at 5452.19, the 20-day EMA.

- A bull cycle in S&P E-Minis remains intact. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, initial support to watch lies at the 20-day EMA, at 6656.22. It has been pierced, a clear break of it would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6541.51.

COMMODITIES: Gold at Fresh Record High, Fibonacci Resistance at $3909.4

- WTI futures have pulled back from their recent gains. The contract has recently breached $65.43, the Sep 2 high and this has potentially improved the S/T condition for bulls. However, the next key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. For bears, a clear reversal lower would refocus attention on key support at $60.85, the Aug 13 low. A break of this level would reinstate the downtrend.

- The trend condition in Gold is unchanged and a bull cycle remains in play. The yellow metal has traded to a fresh cycle high this week, confirming a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3909.4, a Fibonacci projection. On the downside, support to watch lies at $3646.3, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 01/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 01/10/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/10/2025 | 1215/0815 | *** | ADP Employment Report | |

| 01/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/10/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 01/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 01/10/2025 | 1730/1330 | BOC Summary of Deliberations | ||

| 01/10/2025 | 1805/1405 | BOC Sr Deputy Rogers speaks at competition panel | ||

| 02/10/2025 | 0130/1130 | ** | Trade Balance | |

| 02/10/2025 | 0630/0830 | *** | CPI | |

| 02/10/2025 | 0830/0930 | Decision Maker Panel data | ||

| 02/10/2025 | 0900/1100 | ** | EZ Unemployment | |

| 02/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 02/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 02/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 02/10/2025 | 1430/1030 | Dallas Fed's Lorie Logan | ||

| 02/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 02/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 02/10/2025 | 1700/1900 | ECB de Guindos Fireside Chat at ESADE Madrid | ||

| 02/10/2025 | 1725/1325 | BOC Deputy Mendes speaks at Western University |