MNI US MARKETS ANALYSIS - USD Index Narrows In On Bear Trigger

Highlights:

- Risk more fragile as Trump looks to defend US aluminium & steel

- USD Index within range of bear trigger; next drivers?

- ISM Manufacturing employment watched carefully after Friday's weak MNI Chicago PMI

US TSYS: Off Lows But Still Bear Steeper, Mfg Surveys Headline Docket

- Treasuries are off lows although still sit bear steeper from Friday’s close in a “sell the US” theme following Trump’s doubling of steel and aluminum tariffs to 50% late Friday.

- It’s with a backdrop of the Trump administration’s higher growth rather than spending cuts approach to debt stabilization.

- Bloomberg earlier today on some major investment firms’ policies linked to long end woes: “For DoubleLine Capital, there are two approaches to consider when it comes to 30-year US Treasuries: either avoid them, to the degree they can, or outright short them.”

- Today sees manufacturing surveys in focus, with heightened sensitivity as markets assess the sector's ongoing handling of tariff policy changes and heightened uncertainty.

- Cash yields are 1.5-3.5bp higher on the day, with increases led by 10s through to 30s.

- 2s10s sits at 52.4bp (+1.5bp) whilst 5s30s at 98.0bps (+1.0bp) earlier touched a high of 100.23bps (ask price) to return close to ytd highs of 101.4bp on May 22.

- TYU5 trades at 110-21+ (-02+) off a low of 110-18 that equalled Friday’s low, on moderate volumes of 315k.

- Whilst a bear cycle remains in play, with support at 109-26 (May 29 low), last week saw a piercing of key resistance at 110-23 (May 16 high). Friday’s high of 110-30 now marks initial resistance before 111-05+ (May 9 high).

- Data: S&P Global US PMI mfg May final (0945ET), ISM mfg May (1000ET), Construction spending (1000ET)

- Fedspeak: Logan Q&A (1015ET), Goolsbee Q&A (1245ET), Powell opening remarks (1300ET, text only)

- Bill issuance: US Tsy to sell $76bn 13-W, $68bn 26-W bills

STIR: Fed Rates A Little Off Last Week’s Dovish Ending Point

- Fed Funds implied rates are nearly 2bp higher from Friday’s close for the Dec’25 FOMC.

- It’s on a return to some inflationary rather than growth negative concerns from US policies (following Trump’s doubling of steel and aluminum tariffs to 50%) plus spillover from higher oil on weekend OPEC deliberations and Ukraine-Russia strikes.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 6.5bp Jul, 21.5bp Sep, 35.5bp Oct and 53bp Dec.

- SOFR implied yields are seen bottoming at 3.255% (SFRZ6, +1.5bp) as they continue to test what had been a rough range of 100 +/-5bp of cuts from current effective rates seen over the past three weeks.

- Fed Gov. Waller (permanent voter) at a Bank of Korea conference said overnight that he sees the economy on the path to his “good news” rate cut scenario for later this year, rather than the larger/faster cuts under the alternative bad news/high tariff scenario previously laid out. He doesn’t expect tariff-driven inflation to persist (echoing his previous sentiment although with no sign of a discussion on the matter in last week’s FOMC minutes) and expects job cuts to remain modest.

- Ahead, Powell is unlikely to materially touch on mon pol but will be watched just in case whilst both Logan and Goolsbee have spoken recently, on May 30 and May 29.

- Logan (’26 voter) in moderated Q&A (no text)

- Goolsbee (’25 voter) in moderated Q&A (text tbd)

- Powell (permanent voter) in opening remarks at Board of Governors International Finance 75th anniversary (text only). The conference is to recognize the division’s history.

US TSY FUTURES: CFTC Points To Funds & Asset Managers Cutting Positions

The latest weekly CFTC CoT report points to an aggressive unwind of positions on the part of both asset managers and leveraged funds, although this may be skewed by roll activity.

- The report suggested that asset managers trimmed their net longs by ~$47mln DV01 equivalent, although the cohort remains net long across the curve.

- The report suggested that leveraged funds trimmed their net shorts by ~$30mln DV01 equivalent, although the cohort remains net short across the curve.

- Non-commercial net positioning (detailed in the table below) pointed to net shorts bring trimmed in most contracts. The exception was the addition to net shorts in FV futures. Note that the cohort remains net short across the curve.

Source: MNI - Market News/CFTC/Bloomberg

STIR: Mix Of Long Setting & Short Cover Seen In SOFR Futures On Friday

OI data points to net short cover in 6 of the front 7 SOFR futures on Friday, as most contracts finished higher come settlement.

- A mix of net long and short cover then became evident further out the strip.

| 30-May-25 | 29-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,066,650 | 1,065,881 | +769 | Whites | -22,995 |

SFRM5 | 1,468,871 | 1,480,333 | -11,462 | Reds | -14,158 |

SFRU5 | 1,112,569 | 1,124,355 | -11,786 | Greens | +4,269 |

SFRZ5 | 1,068,365 | 1,068,881 | -516 | Blues | -4,334 |

SFRH6 | 766,815 | 772,877 | -6,062 |

|

|

SFRM6 | 751,370 | 754,985 | -3,615 |

|

|

SFRU6 | 700,853 | 706,891 | -6,038 |

|

|

SFRZ6 | 843,880 | 842,323 | +1,557 |

|

|

SFRH7 | 661,068 | 662,922 | -1,854 |

|

|

SFRM7 | 594,033 | 591,868 | +2,165 |

|

|

SFRU7 | 421,009 | 419,137 | +1,872 |

|

|

SFRZ7 | 420,285 | 418,199 | +2,086 |

|

|

SFRH8 | 287,494 | 286,665 | +829 |

|

|

SFRM8 | 211,083 | 212,592 | -1,509 |

|

|

SFRU8 | 164,162 | 162,800 | +1,362 |

|

|

SFRZ8 | 173,635 | 178,651 | -5,016 |

|

|

FOREX: USD Index Bear Trigger Within Range; Next Drivers?

- Broad dollar weakness Monday has shifted market focus back to the post-election cycle lows for the USD Index at 97.921. A close at today's lows would mark a resumption of the S/T downcycle, narrowing the gap with the bear trigger to just 0.75%. The formation of a bearish engulfing daily candle on Thursday last week adds to the S/T downside focus.

- Today's moves may not only be being driven by the repricing of structurally higher inflation (as covered earlier this morning), but the street consensus for USD is also shifting. This weekend's Morgan Stanley note is garnering plenty of attention - seeing a 9% decline in the USD Index to 91.00 in the next 12 months. This is considerably more bearish than consensus (street looks for ~96.00 at end-Q2'26), but the growing USD net short position suggests these expectations are coming under pressure.

- Derivatives markets often move with a higher beta to spot - so it's a surprise to see a synthetic USD Index risk reversal proving more resilient to the recent sell-off relative to today's price (see below). Should the sell-the-US narrative return in earnest (likely via US equities breaking through the mid-May lows), options positioning could extend lower and provide the needed impetus for the next leg lower in the greenback, compensating for the already-stretched CFTC net position.

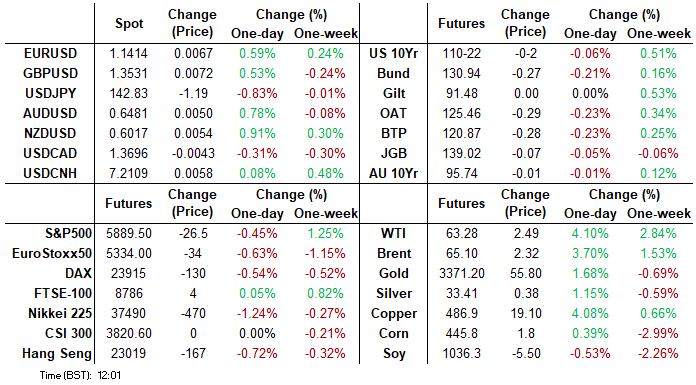

FOREX: USDJPY Sub-143.00 Amid Broad Based Dollar Weakness

- Risk sentiment has been dented to start the week, as markets assess the latest geopolitical concerns regarding the Russia/Ukraine conflict and tariff related developments between the US and China.

- The prevailing trend of greenback weakness has resumed, prompting USDJPY to extend its pullback from last Thursday’s 146.28 high. This leaves spot trading below 143.00 once more and a continuation lower would expose 142.12, the May 27 low. Clearance of this level would resume the bear leg and signal scope for a move towards a key medium-term pivot around the 140.00 mark.

- The Yen is notably outperforming the Swiss Franc, prompting a 0.35% move lower for CHFJPY. While this cross remains in the middle of the May range, spot continues to find good resistance around the 176.00 handle. Further weakness would raise attention on the key 50-day EMA support, intersecting at 173.35, an average we have not closed below since mid-March.

- Goldman Sachs say JPY is still one of their favourite medium-term dollar shorts, stating it continues to be an attractive hedge in a backdrop of elevated recession risk, despite odds of a downturn falling in recent weeks.

- GS believe the price action over recent weeks (and in prior periods of fiscal shocks) supports their view that safe haven demand should still dominate. Recently, GS also noted they prefer funding in CHF rather than JPY, believing that the Swiss Franc is not particularly misaligned in either direction from either a cyclical or structural standpoint.

FOREX: Downside in Focus for DXY, USD/JPY Support in Sight

- The greenback is slipping against all others early Monday, turning focus back to the recent lows and bear trigger for the USD Index at 97.921. A close at today's lows would mark a resumption of the S/T downcycle, narrowing the gap with the bear trigger to just 0.75%. The formation of a bearish engulfing daily candle on Thursday last week adds to the S/T downside focus.

- Trump's doubling of aluminum & steel tariffs on Friday have countered any building hopes that tariffs could be fading as a primary policy tool, even as the likes of the EU are granted reprieves and delays to the onset of major levies. Risk sentiment has been dented as a result, as markets assess the latest geopolitical concerns regarding the Russia/Ukraine conflict and tariff related developments between the US and China.

- The prevailing trend of greenback weakness has resumed, prompting USDJPY to extend its pullback from last Thursday’s 146.28 high. This leaves spot trading below 143.00 once more and a continuation lower would expose 142.12, the May 27 low. Clearance of this level would resume the bear leg and signal scope for a move towards a key medium-term pivot around the 140.00 mark.

- The Yen is notably outperforming the Swiss Franc, prompting a 0.35% move lower for CHFJPY. While this cross remains in the middle of the May range, spot continues to find good resistance around the 176.00 handle. Further weakness would raise attention on the key 50-day EMA support, intersecting at 173.35, an average we have not closed below since mid-March.

- Focus for the remainder of the session rests on May ISM Manufacturing data, with the employment subcomponent in particular focus ahead of Friday's nonfarm payrolls print. Markets are on watch to see whether today's print mirrors that of the MNI Chicago PMI on Friday, which came in well below expectations. Speakers due today include Fed's Logan, Goolsbee & Powell as well as BoE's Greene & Mann.

OPTIONS: Expiries for Jun02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1250($1.4bln), $1.1300-05(E1.9bln), $1.1345-50(E1.9bln)

- EUR/JPY: Y159.50(E500mln)

- AUD/USD: $0.6400(A$856mln), $0.6425-45(A$789mln)

EQUITIES: Recent Weakness for Eurostoxx 50 Futures Considered Corrective

- The trend cycle in Eurostoxx 50 futures is unchanged, it remains bullish and recent weakness appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5254.09, the 50-day EMA. A clear break of this average would signal a possible reversal.

- The trend condition in S&P E-Minis remains bullish. Last Thursday’s initial gains delivered a print above 5993.50, the May 20 high and a bull trigger. The break highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5742.22, the 50-day EMA. A clear break of this average is required to highlight a reversal.

GOLD: Cleaner Positioning Backdrop For Those Looking To Re-engage Longs

Gold non-commercial net long contracts rose by 10.2k to 174.2k in the week to May 27, with first Comex Gold future consolidating its recovery from the May 15 lows during this period. Net longs are now broadly in line with the long-term term average, indicating a much less-stretched positioning backdrop than in Q1 2025. This is supportive of those looking to re-engage in gold longs, which may still be attractive given the macro/geopolitical outlook and bullish technical conditions.

- In the week to May 27, short covering appeared dominant, with non-commercial shorts falling 14.2k to 59.9k. Total longs fell 4.0k to 234.1k.

- Intraday, spot prices are off session highs but remain up 1.80% at $3,348/oz. Familiar drivers are at play:

- (i) Heightened policy uncertainty and trade tensions (which is also dragging the USD lower), following US President Trump’s latest threat of 50% tariffs on steel/aluminium imports from June 4 and ongoing hostility between the US and China.

- (ii) Geopolitical unease following Ukrainian drone strikes on Russia this weekend.

- (iii) Risks of structurally higher global inflation in the medium-term, a function of less open trade/global supply chains.

- A bullish theme in spot gold remains intact and recent gains signal the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Next resistance levels to watch:

- RES 1: $3365.9 - High May 23

- RES 2: $3435.6/3500.1 - High May 7 / High Apr 22 and bull trigger

COMMODITIES: Bullish Gold Narrows Gap to Next Resistance at $3435

- WTI futures are in consolidation mode. The contract traded to a fresh short-term cycle high on May 21 before finding resistance. A bear threat remains intact and the recovery since Apr 9, appears corrective. Key resistance is $62.47, the 50-day EMA. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger.

- A bullish theme in Gold remains intact and recent gains signal the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would open $3435.6 next, the May 7 high. Key support and the bear trigger to watch, has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 02/06/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/06/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 02/06/2025 | 1400/1000 | * | Construction Spending | |

| 02/06/2025 | 1400/1000 | * | Construction Spending | |

| 02/06/2025 | 1400/1000 | Dallas Fed's Lorie Logan | ||

| 02/06/2025 | 1400/1500 | BOE's Mann fireside chat at Fed's IF 75th anniversary conference | ||

| 02/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/06/2025 | 1630/1830 | ECB Lagarde Video Message at Women In Finance Event | ||

| 02/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 02/06/2025 | 1700/1300 | Fed Chair Jerome Powell | ||

| 02/06/2025 | 1700/1800 | BOE Greene Fireside Chat | ||

| 03/06/2025 | 0130/1130 | Business Indicators | ||

| 03/06/2025 | 0130/1130 | Balance of Payments: Current Account | ||

| 03/06/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 03/06/2025 | 0630/0830 | *** | CPI | |

| 03/06/2025 | 0700/0300 | * | Turkey CPI | |

| 03/06/2025 | 0900/1100 | *** | HICP (p) | |

| 03/06/2025 | 0900/1100 | ** | Unemployment | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0915/1015 | BOE Bailey, Breeden, Dhingra, Mann At TSC | ||

| 03/06/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/06/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 03/06/2025 | 1700/1300 | Fed Governor Lisa Cook | ||

| 03/06/2025 | 1930/1530 | Dallas Fed's Lorie Logan |