MNI US MARKETS ANALYSIS - USD, Fed Rates Undergo Relief Rally

Highlights:

- Fed implied rates edge lower, but USD benefits from minor relief rally

- Trade headlines remain the background threat, but JOLTS data will be watched for labour market clues

- AUD fades again as RBA minutes affirm board discussed sizeable easing

US TSYS: Modestly Firmer As Soft China PMI Weighs On Risk Sentiment

- Treasuries are modestly firmer across the curve, initially boosted by the softer than expected China Caixin mfg PMI weighing on risk sentiment before a further bid in London hours.

- 2s and 5s remain within yesterday’s range. 10s and 30s in particular pushed above yesterday’s range but are still lower than Friday’s close as the late Friday doubling of aluminum/steel tariffs still weighs on US assets on net.

- Cash yields are roughly 2bp lower across the curve.

- As such, curves consolidate yesterday’s intraday flattening after 5s30s hit 100.2bps to come closer to ytd highs of 101bps (currently 96.6bp).

- TYU5 trades at 110-22+ (+07+) having eased off session highs of 110-26, with volumes at a subdued 265k.

- Resistance is seen at 110-30 (May 30 and Jun 2 highs) having last week breached an important 110-23 (May 16 high). A clear break could open 111-05+ (May 9 high).

- Data: JOLTS Apr (1000ET), Factory orders Apr (1000ET)

- Fedspeak: Goolsbee (1245ET), Cook (1300ET), Logan (1530ET) – see STIR bullet

- Bill issuance: Tsy to sell $60bn 6-W bills (1130ET)

STIR: Dovish Tilt In Fed Rates - JOLTS, Factory Orders and Cook Ahead

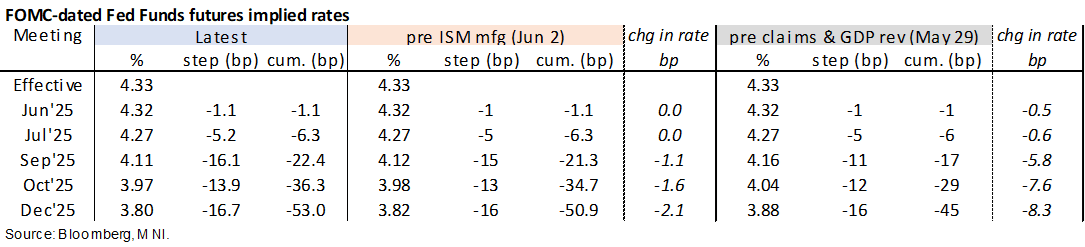

- Fed Funds implied rates are up to 2bp lower for 2025 meetings, with the move coming in London hours rather than a clearer initial reaction to a softer than expected China Caixin mfg PMI earlier overnight.

- Cumulative cuts from 4.33% effective: 1bp Jun, 6.5bp Jul, 22.5bp Sep, 36.5bp Oct and 53bp Dec.

- The 53bp of cuts for the year does however remain off the 54-56bp seen late Fri/early Mon.

- The SOFR terminal implied yield of 3.245% (SFRZ6, -4bp) has reversed yesterday’s increase for back close to its most dovish close since May 7.

- Today sees JOLTS and factory orders for April whilst Fedspeak focus should be on Governor Cook later on.

- 1245ET – Goolsbee (’25 voter) moderated Q&A (text tbd). He spoke yesterday, saying he’s hesitant to make the transitory argument for tariff-driven inflation and that whilst there has been surprisingly little impact on data to date, the April PCE data might have been the last round of pre-tariff data.

- 1300ET – Cook (voter) on econ outlook (text + Q&A). She offered financial stability focused remarks on May 23 (seeing signs of stress in sub-prime borrowers but only moderate vulnerabilities from overall household borrowing). Before that, she said May 10, a few days after the May 6-7 FOMC, that she would want higher rates for longer if productivity is lower whilst warning that protectionist polices may prop up less efficient firms. Against that, there could be a surge in potential output with wider AI use.

- 1530ET – Logan (’26 voter) Fed Listens opening remarks (text only). The nature of remarks suggests low likelihood of anything market moving.

STIR: Mix Of Net Short Setting & Long Cover Seen In SOFR Futs On Monday

OI data points to net short setting in SFRU5 & Z5 on Monday, while the unchanged price status of SFRH5 & M5 makes it hard to provide any real inference when it comes to the nature of the apparent net cover seem in those contracts.

- Net short setting then came to the fore in the reds, before a more balanced mix of net short setting and long cover was evident further out the strip.

| 02-Jun-25 | 30-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,068,953 | 1,066,311 | +2,642 | Whites | +2,226 |

SFRM5 | 1,452,883 | 1,469,931 | -17,048 | Reds | +36,874 |

SFRU5 | 1,119,211 | 1,112,571 | +6,640 | Greens | -6,422 |

SFRZ5 | 1,078,359 | 1,068,367 | +9,992 | Blues | -129 |

SFRH6 | 782,440 | 766,816 | +15,624 |

|

|

SFRM6 | 767,357 | 751,371 | +15,986 |

|

|

SFRU6 | 709,679 | 700,153 | +9,526 |

|

|

SFRZ6 | 839,118 | 843,380 | -4,262 |

|

|

SFRH7 | 669,181 | 661,066 | +8,115 |

|

|

SFRM7 | 586,744 | 594,032 | -7,288 |

|

|

SFRU7 | 415,716 | 421,009 | -5,293 |

|

|

SFRZ7 | 418,328 | 420,284 | -1,956 |

|

|

SFRH8 | 289,661 | 287,493 | +2,168 |

|

|

SFRM8 | 213,789 | 211,083 | +2,706 |

|

|

SFRU8 | 162,654 | 164,162 | -1,508 |

|

|

SFRZ8 | 170,139 | 173,634 | -3,495 |

|

|

EUROPE ISSUANCE UPDATE

UK auction results

- GBP1.25bln of the 4.00% Oct-63 Gilt. Avg yield 5.281% (bid-to-cover 3.51x, tail 0.3bp).

Austria auction results

- E863mln (E750mln allotted) of the 2.90% May-29 Green RAGB. Avg yield 2.116% (bid-to-cover 2.76x; bid-to-issue 2.40x).

- E575mln (E500mln allotted) of the 2.95% Feb-35 RAGB. Avg yield 2.857% (bid-to-cover 3.89x; bid-to-issue 3.38x).

Germany auction results

- E4.5bln (E3.678bln allotted) of the 1.70% Jun-27 Schatz. Avg yield 1.78% (bid-to-offer 2.39x; bid-to-cover 2.92x).

SWITZERLAND DATA: CPI Leaves SNB Pricing Split Between 25/50bps Cut in June

Highlights of the May Swiss CPI print, with plenty of moving parts:

- CPI excl. housing rentals remained unchanged at -0.7% Y/Y after the category saw its quarterly update (2.6% vs 3.2% prior)

- Airfares continued their downward trajectory, now contributing -0.14pp to headline (-13.9% Y/Y vs -9.5% prior), lowest rate since March 2021

- This, together with lower fuel inflation and rental cars, brought down the transport category to its lowest rate since July 2023

- Food inflation meanwhile ticked up by 0.59pp to -0.25% Y/Y, adding 0.06pp to headline vs April

- The acceleration in the recreation category appears to be a mix of package holidays and some goods subcategories in the sector.

What remains is that CPI left the SNB's target range for the first time since March 2021, leaving intact market pricing for around 1/3 odds of a 50bp cut to -0.25% at the upcoming June meeting. USCHF saw no material move on the release, with support sitting at 0.8040, the decade lows seen on April 21, while resistance would stand at the key 0.8333 level.

EUROPEAN FISCAL: French Fiscal Consolidation Intact; More Proposals Due In July

The 10-year OAT/Bund spread is currently ~67bps. That’s still well above the 40-50bps range seen before the snap Legislative Election announcement in May 2024, but below the 70bp handle that provided a floor for the spread through much of H2 2024 and Q1 2025.

- An unwind of immediate domestic political risks and post-Liberation Day tariff concerns has been supportive of spread narrowing, However, markets should still be cognizant that the Bayrou administration is held up by fragile cross-party agreements, which could unravel if future policy proposals ostracize one- (or both) end of political spectrum.

- The French budget deficit was E69.3bln in April, compared with E91.6bln in the same month last year. The improvement relative to 2024 was due to higher tax revenues (E99.6bln vs E69.7bln a year ago). The press release notes that “this difference is explained by the absence of recording of certain revenues collected at the end of April 2024, due to the temporary closure of the Chorus application” (Chorus is a government portal used for business-to-government transactions).

- Despite this caveat, current YTD tracking suggests budget consolidation continues to progress. However, more fiscal tightening is expected to be delivered for the administration to meet its 5.4% 2025 and 4.6% 2026 budget deficit targets.

- Speaking to BFM TV last week, Bayrou noted that the government will seek E40bln in spending cuts in the next budget, for which proposals will be presented in early July. It is unclear at present what measures might be included as part of the package. Bayrou did add he "could take up" the issue of "social VAT", which consists of compensating for reductions in contributions weighing on employment by increasing VAT."

BOC: MNI BoC Preview-June 2025: Not Enough Clarity To Cut

- Download Full Report Here

- The Bank of Canada is likely to maintain the overnight rate target steady at 2.75% for a second consecutive meeting on Wednesday, though analyst opinion and pricing eye a possible 25bp cut.

- April’s pause came after 225bp of cuts to arrive in the middle of the BoC’s currently estimated neutral range of 2.25-3.25% (unchanged in the April Monetary Policy report).

- With this having put the BOC in a position to see further developments in the US-Canada trade dispute before pulling the trigger on further moves, incoming economic data have tilted toward a further hold.

- In particular, better-than-expected GDP and a pickup in core inflation should tilt the balance toward a hold.

- Almost all analysts expect at least one further cut (markets are split between 1 and 2), with current expectations of the terminal overnight rate ranging from 1.75-2.75%.

FOREX: Mild Relief Rally for USD; EUR CPI Justifies ECB Rate Cut

- The USD is undergoing a mild corrective bounce early Tuesday, reversing a small part of the Monday underperformance as catalysts for a further phase of USD weakness dry up somewhat. The market bias remains wholly negative dollars, with the looming background threat of trade headlines still working in favour of the short side. That said, there remain short-term drivers of a potential relief rally for the USD; particularly this Friday's NFP print, at which the Fed will be watching carefully for further signs of a deterioration of the labour market. For now, the USD is the strongest currency in G10 on the day.

- Eurozone inflation data came in on the low side of expectations, with a particular step lower for services pricing prompting headline inflation to slip below the ECB's target and further justify an ECB rate cut at this Thursday's meeting. EUR/GBP edged lower in response, putting the cross to 0.8439, but still clear of the Monday lows. These remain the first downside level of note at 0.8424.

- AUD sold off on the most recent RBA rate decision, and the currency is weaker again today following the minutes of the meeting at which the bank discussed the option of a 50bps cut to the benchmark rate, with members increasingly concerned over the prospects for growth from Trump's trade tariff policies. AUD/USD found support just ahead of the 0.6450 level, but is once again pressuring that mark into early NY hours.

- JOLTS jobs data is the data highlight Tuesday, with markets expecting job openings to ebb again toward multi-year lows. Speakers set for Tuesday include Fed's Goolsbee, Cook & Logan as well as members of the BoE MPC testifying in front of UK lawmakers.

FOREX: Markets Consider Potential Drivers for S/T USD Relief Rally

With a clamour of recent sell-side calls for broader USD losses, some note bullish factors that could provide a reprieve for the dollar in the short-term:

- We wrote yesterday that derivatives markets often move with a higher beta to spot - so it's a surprise to see a synthetic USD Index risk reversal proving more resilient to the recent sell-off relative to today's price - which could be containing the next leg lower for the dollar.

- Deutsche Bank's latest World Outlook sees markets on a turbulent, but sustained, path toward de-escalation of tariff headlines, and while there's likely to be prolonged uncertainty and a notable slowdown in US growth over H2, the de-escalation will support growth earlier relative to prior expectations.

- MUFG write that the Fed need to see clearer evidence that the US labour market is loosening in order to have more confidence to resume rate cuts, and should NFP meet expectations of +130k on Friday, this may not be weak enough to significantly bring forward expectations for rate cuts from September.

- ING see trade developments as remaining crucial, and while China is gaining leverage over the US through control of chip supply, Trump and Xi are to speak this week, leaving room for a positive surprise that could help the dollar at some point this week.

OPTIONS: Expiries for Jun03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1348-50(E3.2bln), $1.1395-00(E1.2bln), $1.1450(E651mln)

- AUD/USD: $0.6415(A$672mln), $0.6500-05(A$1.2bln)

- USD/CAD: C$1.3700($885mln)

EQUITIES: E-Mini S&P Trend Unchanged Following Recent Breach of Bull Trigger

- The trend cycle in Eurostoxx 50 futures remains bullish and recent weakness appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5258.36, the 50-day EMA. A clear break of this average is required to signal a possible reversal.

- The trend condition in S&P E-Minis is unchanged and remains bullish. Recent gains delivered a print above 5993.50, the May 20 high and a bull trigger. The break highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5756.81, the 50-day EMA. A clear break of this average is required to highlight a reversal.

COMMODITIES: WTI Futures in Consolidation Mode and Close to Recent Highs

- WTI futures are in consolidation mode but remain closer to their recent highs. A bear threat remains present and the recovery since Apr 9, appears corrective. Key resistance to monitor is $62.47, the 50-day EMA. It has again been pierced. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger.

- A bullish theme in Gold remains intact and yesterday’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. A continuation higher would open $3435.6 next, the May 7 high. On the downside, key support and the bear trigger to watch, has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 03/06/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/06/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 03/06/2025 | 1700/1300 | Fed Governor Lisa Cook | ||

| 03/06/2025 | 1930/1530 | Dallas Fed's Lorie Logan | ||

| 04/06/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 04/06/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/06/2025 | 0130/1130 | *** | Quarterly GDP | |

| 04/06/2025 | 0700/0900 | ** | Industrial Production | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 04/06/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 04/06/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/06/2025 | 1230/0830 | Atlanta Fed's Raphael Bostic | ||

| 04/06/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 04/06/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/06/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/06/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/06/2025 | 1430/1030 | BOC press conference | ||

| 04/06/2025 | 1800/1400 | Fed Beige Book |