MNI US MARKETS ANALYSIS - USD Dip Accelerates

Highlights:

- USD dip accelerates, putting USD Index flat for Q4

- Last pre-Christmas data releases due, GDP expected at a healthy clip

- Dollar weakness continues to favour precious metals, putting spot gold on course for $4,500

US TSYS: Dragged Higher On Very Low Volumes, Data and Issuance Ahead

Treasuries have firmed throughout Asia and London trading, with assistance from JGBs paring previous losses and a dovish repricing in EUR STIR following Schnabel yesterday (despite her broadly clarifying pre-ECB meeting remarks). Year-end factors could also be at play. Today’s focus will be on a solid data docket before further issuance, the latter highlighted by the 5Y but with some added attention on bills after yesterday’s preference for longer-dated maturities.

- Cash yields are 0.5-2.5bp lower, bull steepening with curves pulling back a little further off recent highs.

- TYH6 trades at session highs of 112-16 (+05) on tiny cumulative volumes of 125k.

- It reverses yesterday’s further losses which saw a low of 112-09+ (not troubling support at 112-06, Dec 16 low) but is only back at the low end of Friday’s range and is still a way off resistance at 112-21+ (50-day EMA).

- Data: Weekly ADP (0815ET), GDP Q3 (0830ET), Durable goods Oct prelim (0830ET), Philly Fed non-mfg (0830ET), Weekly Redbook retail sales (0855ET), IP/cap util Nov & Oct (0915ET), Conf Board consumer survey Dec (1000ET), Richmond Fed mfg Dec (1000ET)

- Coupon issuance: $70B 5Y Note - 91282CPR6, US Tsy $28B 2Y FRN - 91282CPG0 (1300ET). Yesterday’s 2Y tailed by 0.2bp and bid-to-cover slipped from 2.68 to 2.58, whilst last month’s 5Y also tailed by 0.2bp but with the bid-to-cover nudging higher from 2.38 to 2.41.

- Bill issuance: US Tsy $75B 6W & $50B 52W bill auctions (1130ET). Yesterday’s six-month offering was preferred to the three-month with Fed rate expectations potentially at play.

- Politics: Trump doesn’t have any public events scheduled

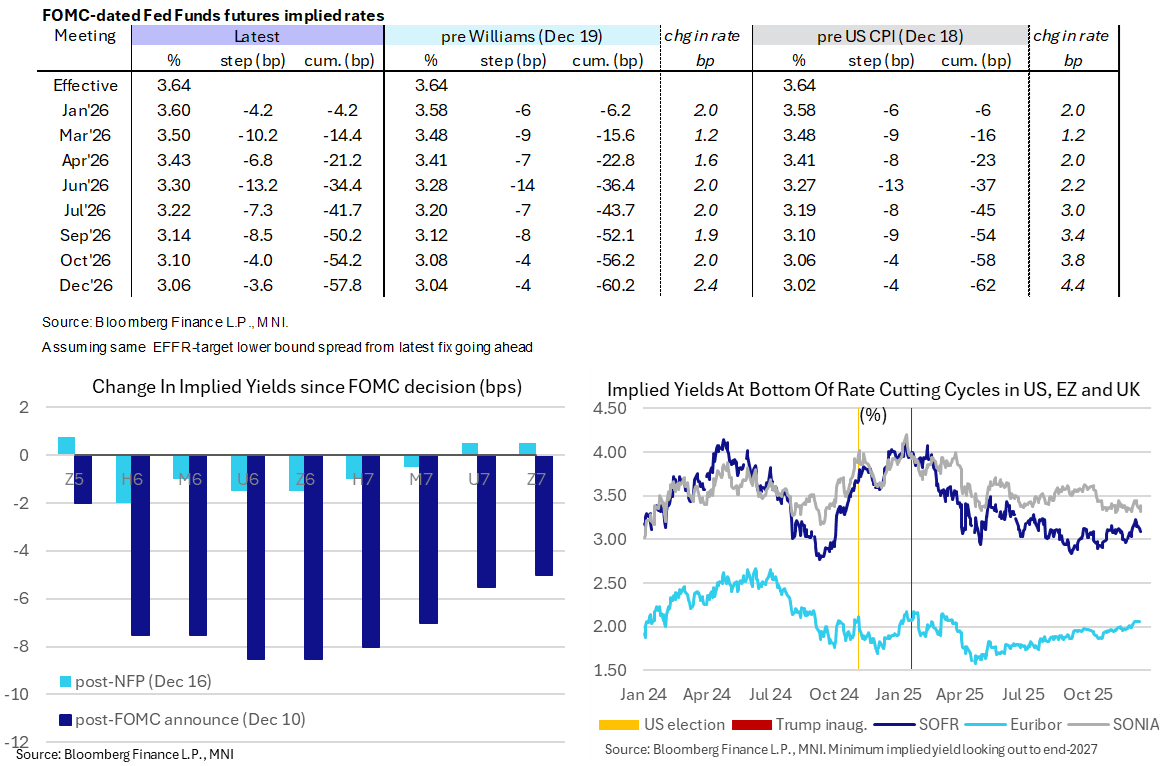

STIR: Awaiting Some Of The Last US Data Releases Before Christmas

- Fed Funds implied rates are essentially unchanged overnight for 2026 meetings ahead of busier day for data including weekly ADP, an eventual Q3 GDP release, delayed releases for durable goods & IP and the Conference Board’s consumer survey. Weekly jobless claims round out tomorrow's data calendar.

- There is just 4bp of cuts priced for the Jan FOMC whilst likelihood of a next cut in April has drifted a little lower over the past couple sessions with a cumulative 21bp priced.

- Cumulative cuts from 3.64% effective: 4bp Jan, 14.5bp Mar, 21bp Apr, 34.5bp Jun (new Fed chair), 50bp Sep and 58bp Dec.

- SOFR futures range from -0.005 to +0.015 looking out to end-2027, with the terminal implied yield of 3.115% (Z6, -0.5bp) remaining within ranges over the past month.

- There’s no Fedspeak scheduled today although there could still be the odd median appearance ahead of Christmas as was the case with Gov. Miran yesterday.

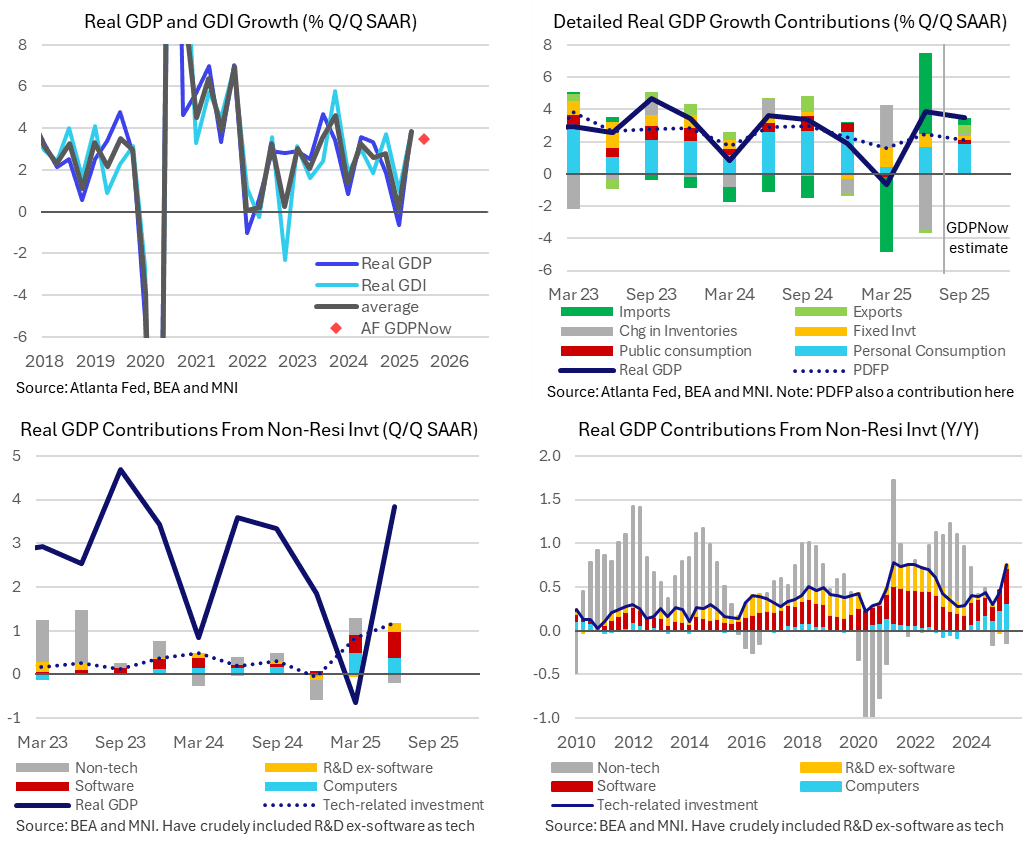

US DATA: Robust GDP Growth Expected For Q3 - 0830ET

Today sees long-awaited Q3 GDP data at 0830ET, in “initial” release form that replaces what would have been the second GDP and the preliminary corporate profits estimates (the advance release was cancelled). This will be the first GDP release since the third Q2 report on Sep 25.

- The extended tracking window of the Atlanta Fed’s GDPNow points to strong real GDP growth of 3.5% annualized after an average 1.6% in 1H25 (-0.65% in Q1 before 3.84% in Q2). Bloomberg consensus is a little softer at 3.3% annualized.

- Expect continued close attention on private demand, best seen by Powell’s preferred PDFP category, which is currently tracking at ~2.4% annualized to match the 2.4% averaged in 1H25 (1.9% Q1 before 2.9% in Q2).

- Consumption dynamics remain important, seen at a healthy 2.7% annualized by both GDPNow and Bloomberg consensus, but there’s less scope to surprise this time having received the September PCE data on Dec 5.

- Investment will continue to be watched closely, with further strong increases expected for IP products and equipment. It follows a very strong 1H25, including software alone adding 0.6pps in Q2 and 0.4pps in Q1 to quarterly GDP growth and computers & peripheral equipment adding 0.4pps in Q2 and 0.5pp in Q1.

- As for the more volatile GDP components, GDPNow eyes a net export boost of 1.0pps (after a huge +4.8pp in Q2 and -4.7pps in Q1) along with broadly neutral changes in inventories at 0.1pps (after -3.4pp in Q2 and +2.6pp in Q1) in some stabilization after major tariff distortions.

- The “third” Q3 GDP release has been confirmed for Jan 22 whilst there’s no current set date for the Q4 advance originally planned for Jan 29.

UK: Gov't Raises IHT Thresholds For Farms Following Rural Backlash

The Department for Environment, Farming and Rural Affairs published a statement confirming the inheritance tax relief threshold will rise to GBP2.5mn for farmers and businesses. DEFRA: "The reforms to agricultural property relief and business property relief mean that only a small number of estates with agricultural and business assets will pay additional inheritance tax." The change comes days after the publication of a report from Baroness Minette Batters, former president of the National Farmers' Union (NFU), regarding farming profitability, which stated many farmers were "bewildered and frightened" by the proposed changes.

- As the BBC reports, "The report did not look in detail at the government's proposed changes to inheritance tax, which are set to apply to farm businesses worth more than £1 million at a rate of 20% from April 2026. But Baroness Batters said it was raised as the single biggest concern by almost everyone in the farming sector she talked to as part of the review."

- The issue had become a significant political headache for PM Sir Keir Starmer's Labour gov't. Farmers have mounted high-profile protests around the Houses of Parliament with tractors, disrupting central London and gaining significant media attention.

- The very nature of Labour's large Commons majority will also have put pressure on Starmer. Historically, the centre-left Labour Party has represented seats in urban areas, while the centre-right Conservatives have represented rural seats. However, the massive gains Labour made in the 2024 general election mean that more than 100 of its MPs represent rural areas. With many of these MPs sitting on small majorities, the loss of support among farmers and the broader rural community would imperil their (already vulnerable) seats even more.

- Opinion polling in the new year will be closely watched to see if the increased threshold does anything to win back support for Labour in rural areas.

POLITICAL RISK: Greenland Issue Re-Emerges As Threat To US-EU Relations

Earlier on 23 Dec, French President Emmanuel Macron posted (in English) on X, "In Nuuk, I reaffirmed France’s unwavering support for the sovereignty and territorial integrity of Denmark and Greenland. Greenland belongs to its people. Denmark stands as its guarantor. I join my voice to that of Europeans in expressing our full solidarity." The French president's call for European solidarity comes amid a re-escalation in transatlantic tensions between the Trump administration and the gov't of Denmark over the future of Greenland.

- US President Donald Trump's appointment of Louisiana Gov. Jeff Landry (R) as 'special envoy to Greenland' earlier in the week has sparked a firm backlash in Nuuk and Copenhagen, as well as several other European capitals, where national leaders have sought to reiterate their support for Denmark.

- Even the European Commission, which has historically stayed quiet on issues where the US president's ire may be raised, criticised the move.

- In October, Politico speculated on the potential method the White House would use to gain effective control of Greenland: "...the Danish government doesn’t expect a military invasion — it expects an invasion of dollars. Either as an outright offer to pay a large sum to each Greenlander, or a campaign to buy influence and local politicians."

- The renewal of the Greenland issue remains a risk to cooperation between NATO states, as well as the future of the US-EU joint statement on trade, with Trump having proved willing to threaten economic ruin via tariffs to secure concessions in other areas.

FRANCE: Parl't To Pass Special Law To Maintain State Functions w/o '26 Budget

The gov't will look to pass a special law in parliament today (23 December) that will ensure the state can continue to levy taxes, borrow on financial markets, and pay public sector workers in the absence of a budget being passed for 2026. First, Minister of the Economy, Roland Lescure, and the Minister of Public Action and Accounts, Amélie de Montchalin, are in front of the Senate Finance Committee to answer their questions on the law. The National Assembly will then debate the bill from 1400CET (0800ET, 1300GMT), followed by a vote. It will then immediately move to the Senate in order to be passed before the midnight deadline set by the Constitution (23 Dec being 70 days after the first submission of the budget to parliament). Once passed by both chambers, President Emmanuel Macron can promulgate the law in the coming days before the new year.

- Committee work in parliament on the draft state budget (PLF) could resume as soon as the week of 5 January, according to Minister Delegate for Relations with Parliament Laurent Panifous, after he said that negotiations between the gov't and political groups will continue over the Christmas period.

- Speaking on France 2, Panifous also confirmed the National Assembly would reintroduce the large company profit surtax that was removed from the Senate's version of the PLF. Panifous: "Following the Senate's work, we have a text with a deficit of 5.3%, which is far too high. The shared objective on both the left and the right is 5%,"

UKRAINE: Massive Overnight Barrage On Ukraine As US VP Strikes Dour Note On Deal

President Volodymyr Zelenskyy has stated that Russia launched a "massive" barrage of more than 600 drones and 30 missiles overnight in 13 regions, killing three. Zelenskyy said the attacks, which targeted power substations and grid infra, "essentially the entire infrastructure of daily life", send "an extremely clear signal about Russia’s priorities." Zelenskyy: "[Russian President Vladimir] Putin still cannot accept that he must stop killing. And that means that the world is not putting enough pressure on Russia."

- Russia's state-run Interfax reports comments from Russian Deputy Foreign Minister Sergei Ryabkov, saying that Russia and the US held a new round of talks over the weekend on the situation in Ukraine (dismissively referring to Ukraine as "irritants"). Says that the "main issues remain unresolved", and a new round of contacts may take place in "early spring".

- On 22 Dec, US Vice President JD Vance spoke to UnHerd. In contrast to the rest of the Trump administration, which has sought to convey the idea that a peace deal may be reached soon, the VP played down the prospect of an agreement in the near future. Vance: "We’re gonna try to get this thing solved. We’re going to keep on trying to negotiate. And I think that we’ve made progress, but sitting here today, I wouldn’t stay with confidence that we’re going to get to a peaceful resolution. I think there’s a good chance we will, I think there’s a good chance we won’t."

FOREX: JPY Extends Advance. Katayama and Takaichi Provide Supportive Backdrop

- The US dollar is weaker again on Tuesday, continuing the theme that played out across Monday’s session. The USD index has extended the week’s decline to 0.7% in a broad greenback move, however, the advance for the Japanese yen has been most notable as we approach the holiday season.

- The yen received a significant boost from finance minister Katayama’s comments on Monday, who provided the most forceful warning of intervention in recent times, stating that the MoF have a ‘free hand’ to take bold action on the currency. This backdrop has kept pressure on USDJPY, which at its lowest level this morning has erased around 210 pips from last Friday’s close. Indeed, the latest acceleration lower was likely tied to the pair sinking through the BOJ press conference lows at 155.85, further pressuring short-term longs.

- Additionally, PM Takaichi may have exacerbated this morning’s price action, providing another angle of yen optimism through her communication that she will not implement irresponsible tax cuts or bond issuance, allaying fiscal concerns somewhat.

- Finally, the technical angle has also assisted the pullback, with last Friday’s rally falling just 10 pips shy of key resistance at 157.89, the Nov 20 high and a bull trigger. Given the volatile moves in recent sessions, the most notable support lies at 154.40, the 50-day EMA. A clear breach of it would undermine the bull theme and signal scope for a deeper corrective pullback.

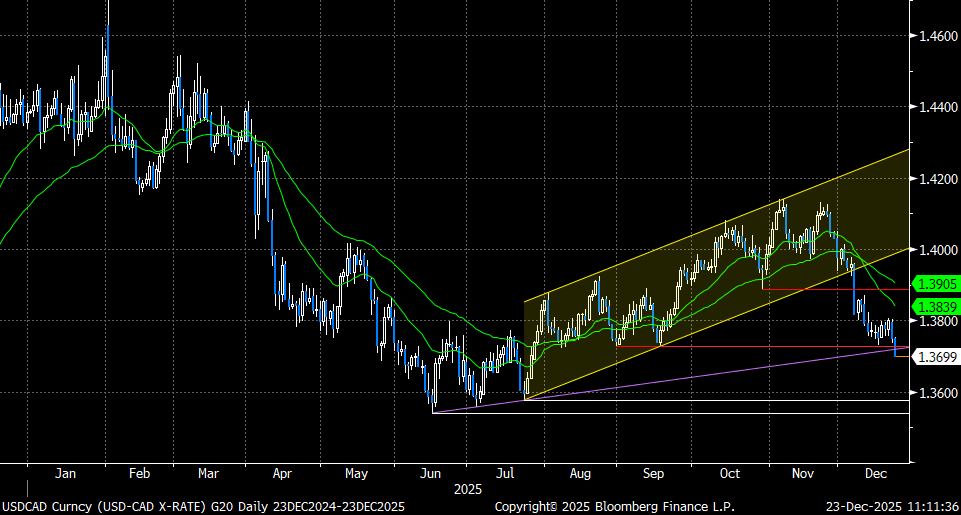

FOREX: USDCAD Slips to Lowest Level Since July, US & Canada GDP Due

- The softer dollar backdrop has been prevailing on Tuesday, prompting the DXY to extend this week’s decline to 0.7% and notably return to last week’s lows at 97.87. The likes of AUD and NZD continue to be well supported by positive equity sentiment, while USDCAD has also gathered downside momentum this morning.

- A break of multiple daily lows at 1.3727 is noteworthy, placing USDCAD at the lowest level since late July as we now press below 1.3700. Overall, USDCAD has now extended its 1-month selloff to around 3%, with the breach of the bull channel in early December exacerbating declines.

- Notably, spot is also testing below another trendline support this morning, drawn from the June 16 low. A daily close below this mark would further bolster the bearish conditions in place for the pair. A small retracement support is seen at 1.3682, however, more notable targets for the move are located at 1.3637 (July 25 low) and 1.3540 (June 16 low).

- GDP data from both the US and Canada should keep the focus on USDCAD later today. As a reminder, Canada's economy rebounded much faster than expected in Q3 led by a drop in imports. However, a contraction in October's flash GDP suggested weakness ahead – whether this manifests or not could be an important driver for CAD heading into year-end.

EQUITIES: Key Resistance for E-Mini S&P Marked at 7014.00, the Oct 30 High

- A bull cycle in Eurostoxx 50 futures remains intact and the latest pullback appears to have been a correction. The first key support to watch lies at 5685.07, the 50-day EMA. A clear break of the EMA would highlight a potential short-term reversal. This would open 5622.00, the Nov 26 low. For bulls, sights are on key resistance at 5847.00, the Nov 13 high. The price pattern on Dec 18 is a bullish engulfing candle - a reversal signal.

- The recent pullback in S&P E-Minis appears to have been a correction. A key short-term support has been defined at 6771.50, the Dec 18 low. A break of this level would signal scope for a deeper retracement of the recent bull phase between Nov 21 - Dec 11. This would open 6737.71, a Fibonacci retracement. For bulls a stronger resumption of gains would refocus attention on key resistance at 7014.00, the Oct 30 high.

COMMODITIES: Fresh Cycle Highs for Gold Reinforce Bullish Conditions

- The trend condition in WTI futures remains bearish and short-term gains are considered corrective. MA studies are in a bear-mode position, highlighting a dominant downtrend. A key support and the bear trigger at $56.11, the Oct 17 low, has been breached. Clearance of this level resumes the downtrend and opens $53.77, a Fibonacci projection. Key short-term resistance to watch is $61.25, the Oct 24 high. First resistance is at $58.71, the 50- day EMA.

- The trend structure in Gold is unchanged, it remains bullish and another fresh cycle high reinforces current conditions. The break higher confirms a resumption of the primary uptrend. The metal has traded through the psychological $4400.0 handle and this opens $4500.0 next, ahead of $4536.0, a Fibonacci projection. Initial firm support to watch lies at $4259.9, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 23/12/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 23/12/2025 | 1330/0830 | *** | Gross Domestic Product by Industry | |

| 23/12/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | *** | GDP / PCE Quarterly | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 23/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 23/12/2025 | 1415/0915 | *** | Industrial Production | |

| 23/12/2025 | 1500/1000 | ** | Richmond Fed Survey | |

| 23/12/2025 | 1500/1000 | *** | Conference Board Consumer Confidence | |

| 23/12/2025 | 1630/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 23/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 23/12/2025 | 1800/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 23/12/2025 | 1830/1330 | Bank of Canada meeting minutes | ||

| 24/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 24/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 24/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 24/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 24/12/2025 | 1630/1130 | ** | US Treasury Auction Result for 7 Year Note | |

| 24/12/2025 | 1700/1200 | ** | Natural Gas Stocks |