MNI US MARKETS ANALYSIS: USD & Oil Bid On Russia Headlines

Highlights:

- USD & oil firmer as market looks to hawkish elements of latest U.S. & Russia comments surrounding Ukraine.

- Bonds back from highs after git futures pierce resistance.

- U.S. new home sales is the main data point later today, before Thursday’s SNB decision and US jobless claims data. Comments from Fed's Daly & BoE's Greene are also due today.

US TSYS: Tsys Inside Ranges Ahead New Home Sales, US$ Climbing

Treasuries are running steady to mixed, inside a narrow overnight range after 10s revisited last Thursday's closing levels. US$ climbing, Bbg index +4.48 at 1200.15 - early Monday levels.

- TYZ5 currently trades at 112-28 (+0.0) on cumulative volumes of 220k. 10Y yield +.0077 at 4.1138%.

- Moving average studies remain in a bull mode position, highlighting a dominant uptrend. The bull trigger has been defined at 113-29, the Sep 11 high. Otherwise, the pullback in Treasury futures appears corrective after TYZ5 moved through the 20-day EMA, at 112-28. The break signals scope for a deeper retracement and attention turns to the 50-day EMA, at 112.10 and the next key support.

- Lighter data on tap ahead a much busier Thursday: MBA Mortgage Applications (0700ET), New Home Sales (1000ET) along with Building Permits at some point today. Main focus is on Thursday's heavy data drop: Personal Consumption, GDP, Durables/Cap Goods, and weekly claims.

- Treasury supply: $28B 2Y FRN re-open (91282CNQ0) & $65B 17W bill auctions (1130ET), $70B 5Y Note Auction (91282CPA3) at 1300ET.

- Fedspeak: At 1610ET, SF Fed President Daly's economic outlook at the annual Spencer Fox Eccles Convocation at the University of Utah’s School of Business, moderated Q&A follows.

- Politics: President Trump's schedule is muted today after speaking at the at the United Nations yesterday, largely closed press items. Unscheduled social media posts always a potential market mover, however.

US TSY FUTURES: Net Long Setting In TY Futures Noted On Tuesday

OI data points to a mix of net long setting (FV, TY, UXY and WN) and short cover (TU & US) as Tsy futures settled higher on Tuesday, with the only meaningful positioning swing coming via the net long setting in TY futures (~$2.3mln DV01).

| 23-Sep-25 | 22-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,531,832 | 4,560,564 | -28,732 | -984,506 |

FV | 6,750,221 | 6,733,778 | +16,443 | +725,919 |

TY | 5,477,985 | 5,442,415 | +35,570 | +2,331,635 |

UXY | 2,373,993 | 2,370,888 | +3,105 | +272,902 |

US | 1,834,358 | 1,834,493 | -135 | -19,167 |

WN | 2,019,868 | 2,018,623 | +1,245 | +232,128 |

|

| Total | +27,496 | +2,558,912 |

SOFR: Long Setting Most Prominent In Futures On Tuesday, Pockets Of Cover Seen

OI data points to net long setting dominating as SOFR futures ticked higher on Tuesday, with the only short cover of any real note coming in the reds.

| 23-Sep-25 | 22-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,469,770 | 1,461,381 | +8,389 | Whites | +39,767 |

SFRZ5 | 1,559,007 | 1,550,994 | +8,013 | Reds | +7,684 |

SFRH6 | 1,180,726 | 1,163,177 | +17,549 | Greens | +11,130 |

SFRM6 | 1,053,819 | 1,048,003 | +5,816 | Blues | +8,905 |

SFRU6 | 930,052 | 938,440 | -8,388 |

|

|

SFRZ6 | 1,074,520 | 1,042,996 | +31,524 |

|

|

SFRH7 | 744,495 | 745,722 | -1,227 |

|

|

SFRM7 | 802,467 | 816,692 | -14,225 |

|

|

SFRU7 | 665,961 | 661,401 | +4,560 |

|

|

SFRZ7 | 717,820 | 709,544 | +8,276 |

|

|

SFRH8 | 431,095 | 436,204 | -5,109 |

|

|

SFRM8 | 368,415 | 365,012 | +3,403 |

|

|

SFRU8 | 276,589 | 270,876 | +5,713 |

|

|

SFRZ8 | 301,116 | 299,920 | +1,196 |

|

|

SFRH9 | 190,007 | 188,377 | +1,630 |

|

|

SFRM9 | 176,432 | 176,066 | +366 |

|

|

EUROPEAN & UK ISSUANCE UPDATE

Germany auction results

- E4bln (E3.045bln allotted) of the 2.50% Nov-32 Bund. Avg yield 2.52% (bid-to-offer 1.13x; bid-to-cover 1.48x).

Italy auction results

- E2.5bln of the 2.10% Aug-27 BTP Short Term. Avg yield 2.23% (bid-to-cover 1.57x).

- E1.25bln of the 1.10% Aug-31 BTPei. Avg yield 1.17% (bid-to-cover 1.67x).

- E1.25bln of the 2.40% May-39 BTPei. Avg yield 2.13% (bid-to-cover 1.67x).

Latvia syndication: Mandate

- Latvia has mandated Deutsche Bank, Erste Group and Goldman Sachs Bank Europe SE for a potential benchmark syndicated transaction of a Euro-denominated 10-year line, subject to market conditions, according to Bloomberg.

Gilt auction results

- Slightly weaker 4.375% Mar-30 Gilt sale than recent re-openings. The 0.4bp tail was a little wider than the 0.1-0.2bps seen between June and August, but in line with May’s re-opening.

- The 2.80x bid-to-cover ratio was the lowest on record for this line, and below the 3.19x average for the prior four re-openings.

- The lowest accepted price was 101.109, a shade above the 101.100 pre-auction mid.

- GBP4.75bln of the 4.375% Mar-30 Gilt. Avg yield 4.095% (bid-to-cover 2.80x, tail 0.4bp).

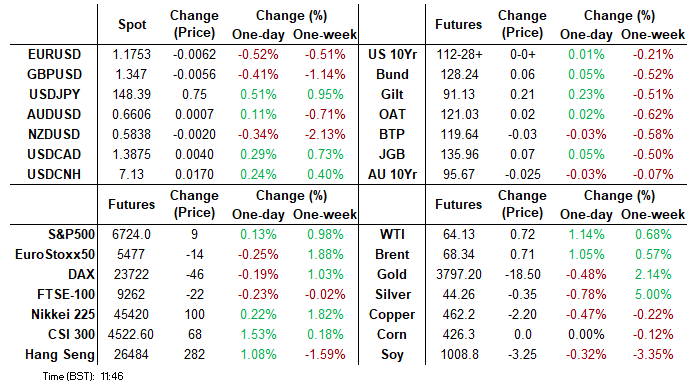

FOREX: USD Outperforms, AUDNZD Surges to Fresh Cycle High Above 1.13

Over the course of the European morning, the US Dollar has been trading with a supportive tone. Despite remaining within the post-Fed ranges, the likes of EUR and GBP have extended session declines to around 0.5% as we approach the NY crossover. For EURUSD, the solid amount of option expiries between 1.1750/1.18 appears to have capped the overnight price action, with the pair slowly edging back below 1.1760 at typing.

- GBPUSD has traded through the 50-day EMA and this leaves support at 1.3458 exposed, a trendline drawn from the Aug 1 low. Clearance of this line would strengthen a bearish threat.

- Firmer-than-expected monthly CPI data in Australia is prompting some Aussie outperformance, with AUDUSD currently up 0.15% and bucking the stronger dollar theme. Market participants have been more focussed on AUDNZD, which has extended its impressive rally on Wednesday to trade to a fresh cycle high of 1.1317. Resistance remains scant on the chart until 1.1491, the 2022 high. It is also worth noting that the NZ government has appointed Riksbank First Deputy Governor Anna Breman to be the new RBNZ governor.

- The low yielders have been under pressure this morning, with USDJPY notably rising above the post Fed highs of 148.38. Uncertainty regarding Japanese politics and the upcoming LDP leadership election may be playing its part here, while moving average studies continue to highlight a dominant uptrend. A resumption of gains would open 149.14, the Sep 3 high. Furthermore, the impressive grind higher for the likes of EURJPY and CHFJPY may be bolstering the bearish yen theme.

- US new home sales is the main data point later today, before Thursday’s SNB decision and US jobless claims data.

FOREX OPTIONS: Expiries For Sep24 NY Cut 1000ET (Source: DTCC)

- EURUSD: 1.1730 (628mln), 1.1750 (978mln), 1.1760 (324mln), 1.1800 (1.39bn), 1.1811 (355mln)

- GBPUSD: 1.3500 (1.31bn)

- USDJPY: 147.90 (241mln), 148.00 (296mln), 148.40 (350mln), 148.50 (729mln)

- USDCAD: 1.3850 (540mln)

- AUDUSD: 0.6600 (904mln), 0.6625 (575mln)

- NZDUSD: 0.5890 (351mln), 0.5900 (372mln)

- EURNOK: 11.7500 (405mln)

CENTRAL BANKS: Riksbank Breman Appointed New RBNZ Governor – Things To Note

The NZ government has appointed Riksbank First Deputy Governor Anna Breman to be the new RBNZ governor. Breman will start the position on December 1 of this year on a 5-year term. She will leave the Riksbank on October 10.

- Breman is an experienced economist, previously Chief Economist and Global Head of Macro Research at Swedbank before her time at the Riksbank (alongside roles in the Swedish Ministry of Finance and the World Bank). She joined the Riksbank in 2019, becoming the Board’s number 2 in 2022. Three points to consider around Breman’s transition into her new role:

- Mandates: The Riksbank and RBNZ have similar mandates. The RBNZ aims to keep inflation “between 1% and 3% on average over the medium term, with a focus on keeping future average inflation near the 2% target midpoint.”. Meanwhile, the Riksbank targets a 2% inflation rate, with a “variation band” of 1-3% (note: “Without neglecting the inflation target, the Riksbank shall moreover contribute to a balanced development of output and employment”).

- Note that in recent monetary policy deliberations, Breman has been one of the more dovish members of the Executive Board. She has advocated for additional rate cuts to support economic activity given inflation is considered to be consistent with the 2% target in the medium term (that rate cut was delivered at yesterday’s decision).

- Rate Path Projections: Both central banks publish a rate path once a quarter to supplement monetary policy communications. During her time at the Riksbank, Breman actively highlighted the uncertainty surrounding rate path projections, particularly further out the forecast horizon. The Riksbank has formally communicated that the first three quarters of a new rate path projection is “owned” by the Executive Board (and is intended to be a policy rate signal), while the rest of the curve is a function of staff models, and should not be over-interpreted as a signal.

- Alternative Scenarios: In its quarterly MPR reports, the Riksbank usually provides at least two alternative scenarios for the policy rate, GDP and CPIF inflation. While not an explicit policy signal, these scenarios are meant to illustrate the most pressing risks currently facing the central bank’s mandate, and possible reaction functions. Breman has stressed the usefulness of these scenarios in internal and external communications, so could consider introducing a similar framework at the RBNZ.

- The Riksbank Executive Board will have four members until Breman’s replacement is appointed, with Governor Thedéen holding the deciding vote in the case of a tie. With the Riksbank now widely expected to be at the end of its easing cycle, this shouldn’t have a major impact on market expectations for the policy rate.

EQUITIES: Bull Cycle In EUROSTOXX50 Futures Intact

A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high on Monday. Price has recently breached the 6700.00 handle and this signals scope for an extension towards 6787.63, a 1.382 projection of the Aug 1 - 15 - 20 price swing. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6625.74, the 20-day EMA.

- EUROSTOXX 50 futures are trading closer to their recent highs. The contract recently cleared resistance around the 20-day EMA - a bullish development - and the subsequent rally reinforces a bullish theme. The move signals potential for a climb towards 5525.00, the Aug 22 high and a bull trigger. On the downside, key support to monitor is 5302.00, the Sep 2 low. First support lies at 5417.44, the 20-day EMA.

COMMODITIES: Gold Bulls Remain In The Driver's Seat

Gold is in a clear bull cycle and shallow short-term pullbacks remain corrective. A fresh all-time high once again, yesterday, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is the $3800.0 handle. Initial firm support lies at $3610.2, the 20-day EMA.

- The trend condition in WTI is unchanged - a bear cycle remains intact and short-term gains are considered corrective. The pullback from the Sep 2 high highlights a possible reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $65.43, the Sep 2 high. A stronger resumption of weakness would open $57.50, the May 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 24/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 24/09/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/09/2025 | 1400/1000 | *** | New Home Sales | |

| 24/09/2025 | 1400/1000 | *** | New Home Sales | |

| 24/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 24/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 24/09/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 24/09/2025 | 1630/1730 | BOE Greene On Supply Shocks and MonPol | ||

| 24/09/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 24/09/2025 | 2010/1610 | San Francisco Fed's Mary Daly | ||

| 25/09/2025 | - | Swiss National Bank Meeting | ||

| 25/09/2025 | 0600/0800 | ** | PPI | |

| 25/09/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 25/09/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/09/2025 | 0730/0930 | *** | SNB Interest Rate Decision | |

| 25/09/2025 | 0800/1000 | ** | M3 | |

| 25/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/09/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 25/09/2025 | 1220/0820 | Chicago Fed's Austan Goolsbee | ||

| 25/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 25/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 25/09/2025 | 1230/0830 | * | Payroll employment | |

| 25/09/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/09/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 25/09/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 25/09/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/09/2025 | 1300/0900 | New York Fed's John Williams | ||

| 25/09/2025 | 1300/0900 | KC Fed's Jeff Schmid | ||

| 25/09/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 25/09/2025 | 1400/1000 | *** | NAR existing home sales | |

| 25/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 25/09/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 25/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 25/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 25/09/2025 | 1700/1300 | Fed Governor Michael Barr | ||

| 25/09/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 25/09/2025 | 1740/1340 | Dallas Fed's Lorie Logan | ||

| 25/09/2025 | 1900/1500 | *** | Mexico Interest Rate | |

| 25/09/2025 | 1930/1530 | San Francisco Fed's Mary Daly |