MNI US MARKETS ANALYSIS - Tsys, USD Hold Post-Fed Moves

Highlights:

- Treasuries, greenback hold post-Fed moves, yields comfortably north of 4.00%

- Xi and Trump strike interim deal including fentanyl tariff reduction, large scale purchases of US agricultural, energy products

- JPY weaker as BoJ fail to commit to December rate hike

US TSYS: Powell Sell-Off Consolidated, Claims And Bills Ahead

- Treasuries consolidate yesterday’s shift lower, which had started below the FOMC decision before accelerating on a hawkish Powell – see the MNI Fed Review here.

- As part of Trump’s “12 out of 10” meeting with China’s Xi, the U.S. has agreed to remove a 10% fentanyl tariff imposed on Chinese goods, while its 24% reciprocal tariff will continue to be suspended for one year.

- QT will end on Dec 1, with the date chosen to give market participants time to adjust. MBS reinvestments will be made into Treasury bills as opposed to across the Treasury curve - an area of uncertainty ahead of the meeting.

- Cash yields are between 0-0.5bp lower on the day.

- 2Y yields trade at 3.596% after yesterday’s high of 3.610%. It comfortably cleared the 50d moving average we highlighted yesterday but the near- and medium-term chart is still interesting with next resistance at 3.6676% before the 100d MA rounded up to 3.70%

- TYZ5 trades at 112-25+ (-03+), consolidating yesterday’s slide and with healthy volumes of 430k as Asia and European investors react to Powell.

- An overnight low of 112-22+ built on clearance of latest support at 112-27 (50-day EMA), opening 112-16+ (Oct 10 low). The pullback extending has highlighted potential for a deeper retracement near-term.

- Today’s local docket is headlined by state-level jobless claims data in the afternoon (as has been the case under this government shutdown). Powell yesterday: “The fact we are not seeing an uptick in claims or a downtick in openings suggests that you are seeing maybe continued gradual cooling, but nothing more than that, so that does give you some comfort.”

- Data: Dallas Fed weekly economic index (1130ET), State-level jobless claims released during the afternoon

- Fedspeak: Bowman (0955ET) and Logan (1315ET) are both speaking but won’t touch on monetary policy with the FOMC blackout in place until tonight.

- Bill issuance: US Tsy $110B 4-wk bills, $95B 8-wk bills (1130ET)

- Politics: Trump flying back from Korea, arrives at the White House 1505ET

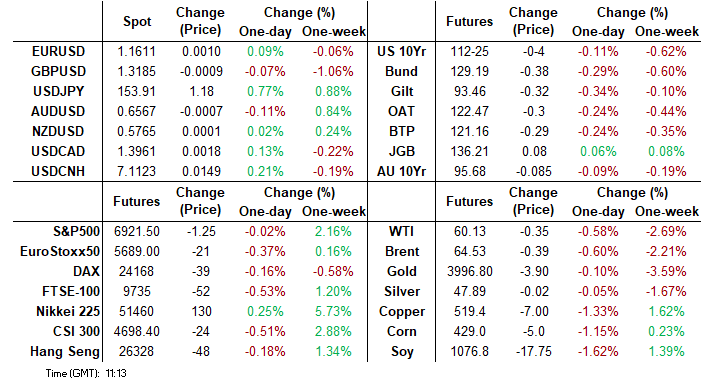

STIR: December Fed Cut Odds Hold Increased Uncertainty Post-Powell

- Fed Funds implied rates hold yesterday’s hawkish shift on Powell indicating a strongly divided FOMC on December cut prospects, whilst also digesting Trump’s “12 out of 10” meeting with China’s Xi.

- No spillover from the BoJ, with Ueda not providing a signal around the likely timing of the next rate hike. ECB Lagarde’s tone will be watched later on for potential spillover, with the rate decision itself likely a non-event.

- Cumulative cuts from an assumed 3.87% effective: 17bp Dec (vs 22-23bp pre-Powell), 26bp Jan, 35bp Mar, 42.5bp Apr and 57bp Jun (vs 65bp pre-Powell).

- There is however higher uncertainty here after the recent push higher in the EFFR.

- SOFR futures see modest further losses in the Z5 and H6 (-0.02) otherwise are little changed on the day.

- The SOFR terminal implied yield of 3.065% (SFRH7) is 0.5bp lower after yesterday’s highest close since Oct 9, i.e. prior to the initial re-escalation in US-China trade tensions on Oct 10 before subsequent improvements. It’s at some of its highest levels for the past month.

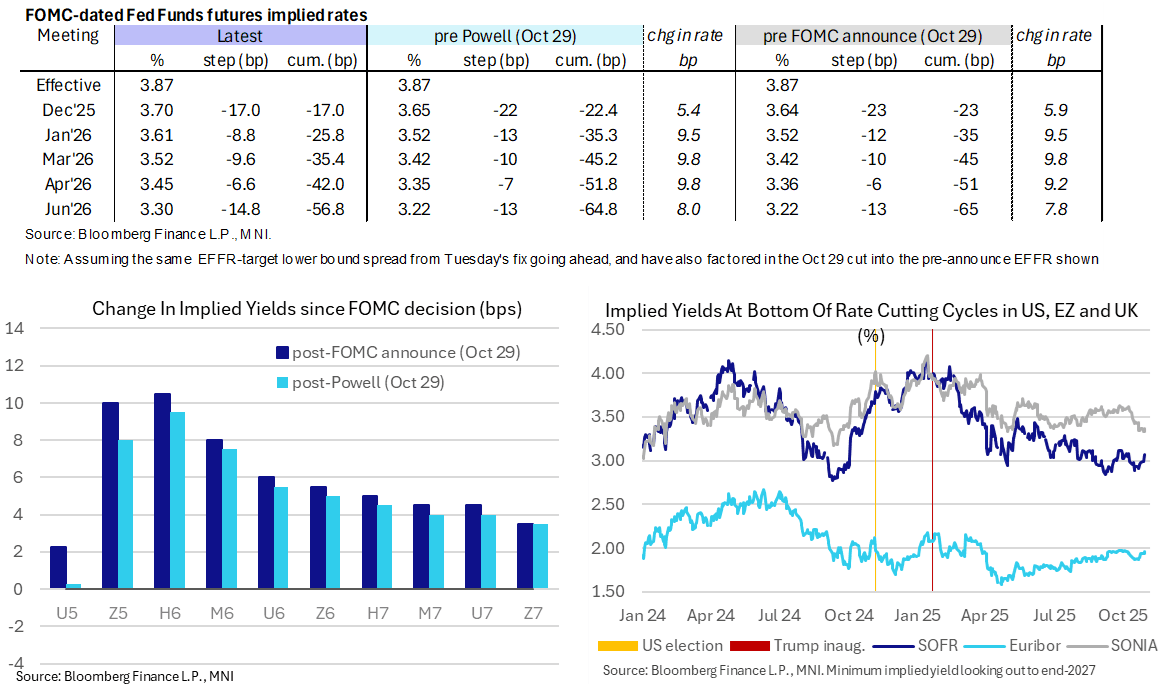

BOE: Huge increase in STR usage; repo operation usage up GBP21.4bln this week

- There has been a huge increase in STR usage today of GBP14.201bln. This is the largest increase on record eclipsing the previous GBP8.1bln record increase.

- This puts STR usage at GBP97.882bln and follows a large increase in ILTR usage to GBP54.321bln (the biggest weekly net increase since the first week of the COVID lockdown).

- Overall this puts BOE repo operation usage at GBP152.203bln - an increase of GBP21.359bln from a previous record high.

- This will have coincided with large TFSME repayments (there was still around GBP25bln due to be repaid by the end of October following the last weekly balance sheet update dated 22 October).

- This broadly shows that the balance sheet hasn't really fallen in size despite the reduction in TFSME lending.

- The next balance sheet update will be published today at 15:00.

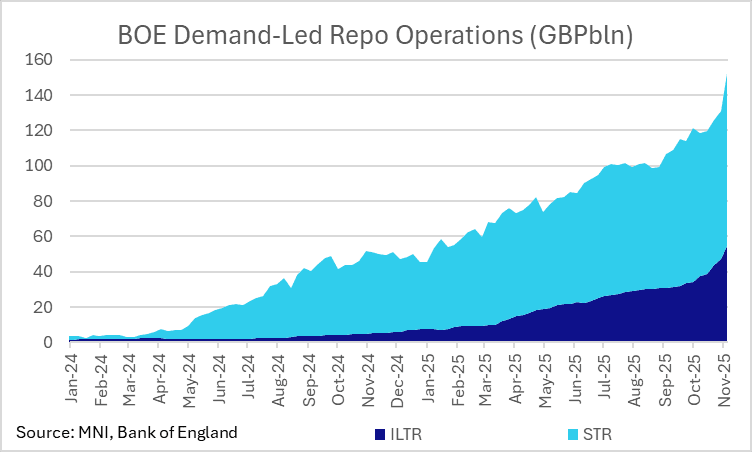

NETHERLANDS: Moderates Gain In Election As Parties Of Fmr. Gov't Lose Out (1/2)

The main 'winners' from the 29 October general elections were parties from the centre of the political spectrum, with the liberal pro-EU Democrats 66 (D66) and centre-right Christian Democratic Appeal (CDA) each making significant gains. The D66 saw a late surge in polling support, with Rob Jetten's party looking set to have won 26 seats in the 150-member House of Representatives, up from nine in 2023. The CDA, which at one point was leading nationwide polls, had to settle for 18 seats, up from five.

- With 99.7% of votes counted, Geert Wilders' far-right populist Party for Freedom (PVV) is neck-and-neck with D66 in terms of overall vote share and is set to win 26 seats (down from 37 in 2023). It would appear voters laid the failures of the Schoof gov't largely at the feet of the PVV (and the centrist New Social Contract, which lost all 20 of its seats). For Wilders, this will mean a return to the position of main opposition, attempting to steer public debate on issues of immigration and culture but without direct policy influence.

- The election has claimed the position of one major party leader, with centre-left/environmentalist GreenLeft-Labour (GL-PvdA) leader Frans Timmermans announcing his resignation after the party saw its seat total fall from 25 to 20.

- The 'easiest' route to a coalition gov't would be a broad centrist bloc containing D66, CDA, GL-PvdA, and the liberal conservative People's Party for Freedom and Democracy (VVD, 22 seats), encompassing 86 seats and comfortably crossing the 76-seat majority threshold. Jetten would be the frontrunner to become the Netherlands' youngest-ever PM as leader of the largest party and a centrist compromise for the GL-PvdA and VVD.

Chart 1. General Election Results, 2023 (LHS) and 2025 (RHS)

Source: NOS, Kiesraad, MNI. N.b. 2025 results based on 99.7% of votes counted.

NETHERLANDS: Moderates Gain In Election As Parties Of Fmr. Gov't Lose Out (2/2)

- There is the narrow prospect that the CDA and VVD push for a conservative coalition, substituting the GL-PvdA with the right-wing JA21 (nine seats). This coalition would hold 75 seats based on current vote share, one short of a majority. The inclusion of the pensioners' interest 50 Plus (two seats), or centre-left Christian socialist Christian Union (three seats) would allow the threshold to be crossed. It may also serve to offset D66 concerns about the inclusion of JA21. Nevertheless, this remains an unlikely scenario.

- As has been the case in recent elections, the gov't formation process is likely to take months rather than weeks. The fragmentation of Dutch politics in recent years has seen four party coalitions required to reach a majority. Up until the final gov'ts of erstwhile PM Mark Rutte, two or three-party coalitions were the norm. The more parties needed in a coalition, the lengthier the coalition talks, as more compromises are necessary to reach an agreeable coalition document.

- The demissionary gov't of PM Dick Schoof will remain in place until a new gov't is formed. It will have the powers to ensure the running of day-to-day gov't, but cannot enact major legislation or pass new budgets. As such, policy implications from the election are unlikely to be known for some time until coalition talks get underway in earnest.

- For all the gains of the D66 and CDA, the election should not necessarily be viewed as a repudiation of right-wing politics by the Dutch electorate. JA21 gained eight seats, while the far-right nativist Forum for Democracy (Fvd) expanded its seat total from three to seven, highlighting potential disillusionment with Wilders as a party leader rather than the issues his party has championed.

UK: Reeves Looks To Have Survived Rental Blunder, But Comes At Bad Time

Chancellor of the Exchequer Rachel Reeves looks likely to survive a media furore surrounding her not obtaining the proper permissions to rent out her family home after moving into the chancellor's dwelling at No.11 Downing St. after last year's general election. Initially reported in the Daily Mail, Reeves did not obtain a 'selective' rental licence, required by some English councils. Reeves outlined the issues in a letter to PM Sir Keir Starmer in which she "sincerely" apologised for her "inadvertent error". In reply, Starmer said that he was content that the "matter can be drawn to a close" after consulting the Independent Adviser on Ministers' Interests Laurie Magnus, who said he would not be launching an investigation.

- Leader of the main opposition centre-right Conservative Party, Kemi Badnoch, has called for Reeves to resign. At present, the pressure does not appear to be as intense as that faced by erstwhile Deputy PM Angela Rayner in September after revelations of her tax affairs came to light and she stepped down from the Labour frontbench.

- Nevertheless, the story comes at an inopportune time for Reeves and Starmer. With less than a month until the 26 November budget, there is significant focus on whether the gov't will break its manifesto pledges not to raise income tax, National Insurance, or VAT. Headlines regarding potential financial impropriety by the very individual presenting the budget could further sour public opinion towards the gov't.

FOREX: USDJPY Surges Through Key Resistance to Fresh 8-Month Highs

- USDJPY (+0.62%) has broken through key resistance Thursday, rallying to fresh 8-month highs of 153.89. Bank of Japan Governor Ueda did not provide a signal around the likely timing of the next rate hike, which combined with the hawkish Fed has underpinned the constructive USDJPY price action. Ueda noted that still-elevated trade policy uncertainty justified holding rates in October, while the BOJ wants to get an early read of next year's wage momentum before delivering another hike.

- The move strengthens bullish trend conditions in USDJPY, with focus now on 154.39, a Fibonacci retracement point. While press conference commentary on recent exchange rate moves was rather in line with previous rhetoric, further upward pressure in USDJPY could raise concern amongst BoJ officials - whose commentary subsequently remains key to watch for the pair.

- Elsewhere, markets view the outcome of the overnight Trump-Xi meeting rather favourably, with the key rare earths conflict appearing to be resolved for the time being. This may have underpinned some NZD outperformance on the margin, with NZDUSD standing at 0.5773, but feedthrough to wider G10 FX appears limited for now.

- Eurozone Q3 GDP is scheduled for release soon, ahead of German national-level CPI later today. Attention then turns to the ECB, firmly expected to hold its key interest rates, putting focus on Lagarde's press conference. EURUSD has recovered from the post fed lows of 1.1578, consolidating around the 1.1625 mark. Price needs to trade above 1.1728, the Oct 17 high, to reinstate a bull theme.

FOREX: EURUSD Support Remains Intact, New Cycle Highs for EURJPY

- EURUSD has recovered from the post fed lows of 1.1578, consolidating back above the 1.1600 mark as we approach the ECB decision and press conference later today. This meeting is likely seen as a stepping stone to December’s updated economic projections, which will include new forecasts for 2028. Any hints here will likely shape market reaction although we see Lagarde opting for a broadly neutral tone to maintain optionality.

- While EURUSD remains inside its current short-term range, importantly support at 1.1542 (Oct 09) has remained intact. The pair needs to trade above 1.1728, the Oct 17 high, to reinstate a bull theme. Of note ahead of the meeting and further Eurozone inflation releases to end the week, there are a number of EUR crosses that maintain a bullish tone:

- EURJPY: The Bank of Japan provided no guidance as to when it would next raise its policy interest rate, and EURJPY has surged to fresh cycle highs today as a result, marking a resumption of the primary uptrend. Spot has narrowed the gap significantly to 178.94, the 1.236 projection of the Jul 31 - Sep 29 - Oct 2 price swing. Initial support moves up to 176.23, the 20-day EMA.

- EURGBP: UK fiscal concerns continue to fuel renewed sterling pessimism, and EURGBP’s move above 0.8800 has placed the cross at its highest level since May 2023. Topside targets for the move include 0.8835 and 0.8875, the April 2023 high.

- EURCHF: It’s also worth highlighting that EURCHF held a significant medium-term support last week, now operating roughly 80 pips above the key 0.9206 level. A break back above 50-day EMA resistance at 0.9310 would be a bullish development, likely allowing the cross to re-establish the 0.93-0.94 range that was broadly in place between May/September.

OPTIONS: Expiries for Oct30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-05(E1.3bln), $1.1625(E668ln), $1.1650(E949mln), $1.1700(E558mln)

- USD/JPY: Y150.00($878mln), Y153.00($785mln)

- EUR/GBP: Gbp0.8750(E429mln)

- AUD/USD: $0.6515(A$865mln)

- USD/CAD: C$1.3675($1.1bln), C$1.3965($1.0bln), C$1.4015($1.7bln)

COMMODITIES: Gold Cycle Low Means Correction May Not Be Over

- A fresh cycle low this week in Gold highlights an extension of the bear cycle that started Oct 20. Note that the trend is overbought and the deeper retracement is allowing this condition to unwind. The 20-day EMA has been breached, signalling scope for a deeper retracement, towards the 50-day EMA, at $3846.3. Key resistance and the bull trigger has been defined at $4381.5, the Oct 20 high. Initial resistance is at $4161.4, the Oct 22 high.

- Recent gains in WTI futures appear corrective for now, however, note that price has recently traded through the 50-day EMA, currently at $60.09. The breach of this average signals scope for a stronger recovery. A resistance at $62.34, the Oct 8 high, has also been pierced. A clear break of it would expose key resistance at $65.77, the Sep 26 high. Key support and the bear trigger has been defined at $55.96, the Low Oct 20.

EQUITIES: Trend Condition in Stocks Remains Bullish

- The trend condition in S&P E-Minis remains bullish and price is trading higher this week. The fresh cycle high confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 6974.04 next, a Fibonacci projection point. Initial firm support to watch lies at 6748.48, the 20-day EMA. A pullback would be considered corrective.

- The trend structure in Eurostoxx 50 futures remains bullish. This week’s fresh cycle high’s reinforces a bull theme and the move higher maintains the rising price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 5777.41, a Fibonacci projection. First support lies at 6740.59, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 30/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 30/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/10/2025 | 1230/0830 | * | Payroll employment | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1300/1400 | *** | Germany CPI (p) | |

| 30/10/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 30/10/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 30/10/2025 | 1345/1445 | ECB Press Conference | ||

| 30/10/2025 | 1355/0955 | Fed's Michelle Bowman | ||

| 30/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 30/10/2025 | 1515/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 30/10/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 30/10/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 31/10/2025 | 2330/0830 | ** | Tokyo CPI | |

| 31/10/2025 | 2330/0830 | * | Labor Force Survey | |

| 31/10/2025 | 2350/0850 | * | Retail Sales (p) | |

| 31/10/2025 | 2350/0850 | ** | Industrial Production | |

| 31/10/2025 | 0030/1130 | * | Producer price index q/q | |

| 31/10/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/10/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 31/10/2025 | 0700/0800 | ** | Import/Export Prices | |

| 31/10/2025 | 0700/0800 | ** | Retail Sales | |

| 31/10/2025 | 0730/0830 | ** | Retail Sales | |

| 31/10/2025 | 0745/0845 | *** | HICP (p) | |

| 31/10/2025 | 0745/0845 | ** | PPI | |

| 31/10/2025 | 0930/0930 | Blue Book / Pink Book | ||

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | Italy Flash Inflation | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/10/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 31/10/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/10/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 31/10/2025 | 1600/1200 | Fed's Beth Hammack, Raphael Bostic | ||

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |