MNI US MARKETS ANALYSIS - Tsys, USD Gear for Weak NFP Revision

Highlights:

- Treasuries, dollar gearing for more signs of labour market weakness in today's benchmark payrolls revisions

- Benchmark revisions could open BLS up to more criticism from the White House

- JPY rallies as BoJ sources report suggests more aggressive tightening schedule

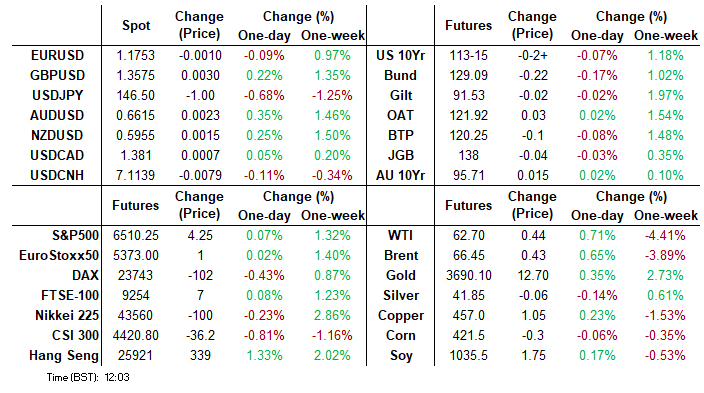

US TSYS: Off Yesterday’s Highs With Payroll Revisions and 3Y Supply Ahead

- Treasuries are mildly cheaper overnight, gently pushing back against yesterday’s bull flattening but comfortably within yesterday’s ranges.

- Today is highlighted by preliminary benchmark payrolls revisions at 1000ET (MNI Preview link), added attention on Trump administration BLS criticism, 3Y supply and then broader Trump comments. The docket will be seen in light of PPI and CPI coming on Wed and Thu respectively.

- Cash yields are 1.2-1.9bp higher on the day, with increases marginally led by 30s.

- Curves are marginally steeper but broadly consolidate yesterday's second day of flattening, including 5s30s at 113.9bp vs a briefly seen post-NFP high of 126.9bp (multi-year steeps).

- TYZ5 trades at 113-15+ (-02) off earlier lows of 113-11, on limited overnight volumes of 250k.

- Friday’s post-payrolls high of 113-21+ still carries weight having hit another fresh short-term cycle high. It marks the next resistance level after which lies 113-26+ (2.764 proj of Jul 15-22-28 price swing) whilst support is seen at 112-28+ (Sep 5 low).

- Data: Preliminary benchmark payrolls revision (1000ET).

- Coupon issuance: US Tsy $58B 3Y Note auction - 91282CNY3 (1300ET). Last month’s 3Y saw another small tail of 0.7bp although the bid-to-cover firmed a touch from 2.51 to 2.53.

- Bill issuance: US Tsy $85B 6W bill auction

- Politics: Press briefing with WH Press Sec Leavitt (1300ET), Trump participates in swearing-in ceremony for US Ambassador to Portugal (1600ET), Trump signs proclamation (1630ET)

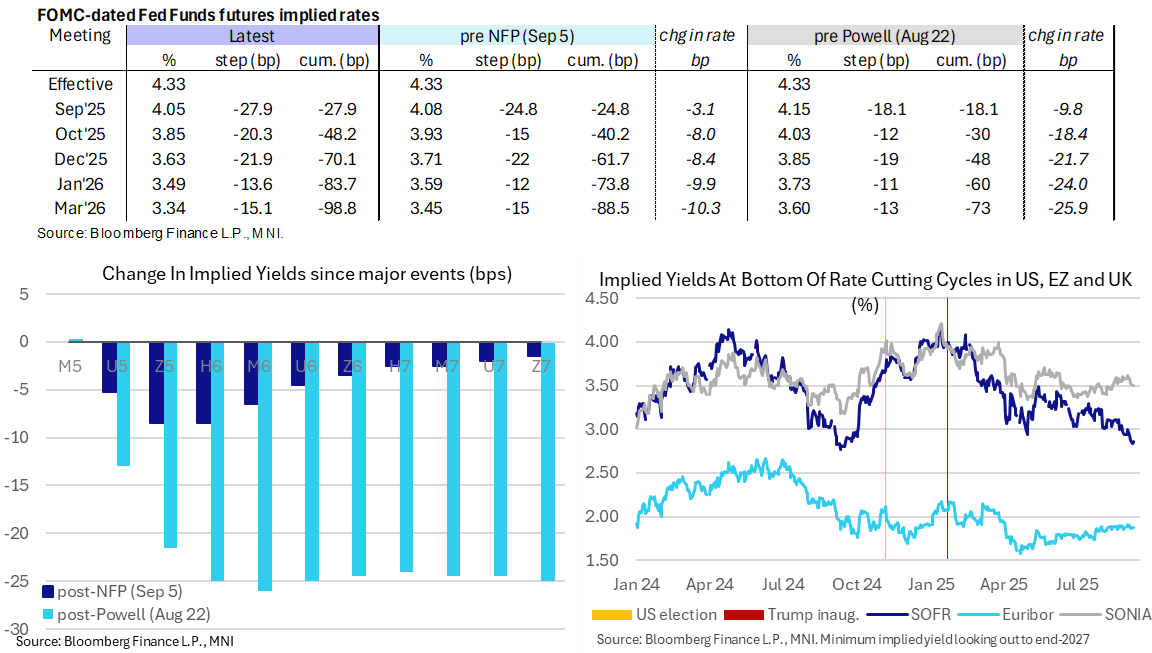

STIR: 70bp Of Fed Cuts Seen To Year-End With Payroll Revision Estimate Eyed

- Fed Funds implied rates are 1.5bp higher on the day for end-2025 rates, pulling a little further away from fully pricing three consecutive rate cuts, but remain within post-NFP ranges ahead of payrolls benchmark revisions at 3pm.

- Cumulative cuts from 4.33% effective: 28bp Sep 17, 48bp Oct, 70bp Dec, 83.5bp Jan and 99bp Mar.

- The SOFR implied terminal yield of 2.86% (SFRH7) is 2bp higher on the day after yesterday saw a fresh lowest close since Sept 2024 (when it saw cycle lows in the high 2.7s), hovering just shy of 150bp of cuts ahead from current levels.

- Today’s US macro docket is headlined by the preliminary estimate for payrolls benchmark revisions at 1000ET. There’s a wide range of estimates here but we judge the median expectation to be circa -750k. MNI Preview: https://media.marketnews.com/US_Prelim_Benchmark2025_Preview_f1d718139b.pdf

- On a related note, the WSJ reports that advisers to President Trump are preparing a report laying out alleged shortcomings of the BLS’s jobs data including revisions.

- Tomorrow (Sep 10), the Senate banking committee will vote to approve CEA's Miran for the Fed Board of Governors at 1000ET. He would still have to be approved by the full Senate to be fully confirmed but this is moving quickly enough to assume that he will be at the FOMC table at the Sept 16-17 meeting.

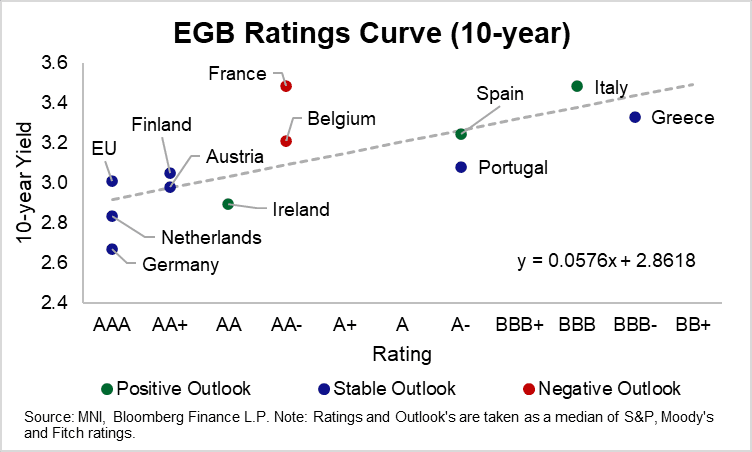

EGBS: A Fitch Downgrade Is Probably In The Price For OATs

- Fitch may downgrade France’s sovereign rating to A+ on Friday after hours, following Bayrou’s unsurprising ousting as Prime Minister after yesterday’s no confidence vote. However, given the political risk premium that has built up in OATs in recent weeks, we suspect markets have mostly priced in this outcome.

- President Macron’s office has said a new PM will be appointed in the coming days. See colour on the current front runners here .

- On March 14, Fitch affirmed France’s rating at AA- (Outlook Negative). In its report, Fitch noted that a downgrade would be possible if there is a “failure to implement a credible medium-term fiscal consolidation plan, for example, due to political opposition or social pressures” and/or if there is “materially lower economic growth prospects and weakened competitiveness.”

- Given recent political (and economic) developments, it seems the conditions for a downgrade have been met. If realised, Fitch would be the first major issuer to downgrade France from an “AA- equivalent” rating.

- S&P also maintains a Negative Outlook on France (rating AA-), but a review isn’t due until November 28. Moody’s holds France on a Stable Outlook (rating Aa3), with a review due on October 24.

- Other ratings action of interest on Friday include Fitch on Portugal (current rating: A-, Outlook Positive) and S&P on Spain (current rating A, Outlook Stable).

- Portugal was upgraded by S&P on Aug 29, so a similar outcome from Fitch is possible on Friday. OTs already screen a little rich on a simple ratings vs 10-year yield curve, so this may also (at least partially) be in the price.

EUROPE ISSUANCE UPDATE:

EU dual tranche syndication: Final terms

- E5bln of the new Oct-30 EU-bond. Spread set at MS + 22bp (guidance was MS + 24bps area), Books in excess of E70bln.

- E6bln (increased from E5bln, MNI had noted the potential to increase) of the new 30-year Oct-55 EU-bond. Spread set at MS + 119bp (guidance was MS + 121bps area), Books in excess of E98bln.

Netherlands auction results

- E1.74bln of the 4.00% Jan-37 DSL. Avg yield 2.949%.

UK auction results

- A strong 20-year auction there with the lowest accepted price of 93.708 higher than the gilt had traded (prior to the bidding window closing) and the average price another 0.027 higher than that (resulting in a tight 0.2bp tail).

- Gilt futures also move to their highs of the day post-auction.

- GBP1.75bln of the 4.75% Oct-43 Gilt. Avg yield 5.291% (bid-to-cover 3.50x, tail 0.2bp).

Austria auction results

- E1.15bln (E1bln allotted) of the 2.95% Feb-35 RAGB. Avg yield 2.937% (bid-to-cover 2.21x; bid-to-issue 1.92x).

German auction results

- E500mln (E491mln allotted) of the 0% Aug-31 Green Bund. Avg yield 2.25% (bid-to-offer 2.27x; bid-to-cover 2.31x).

- E1bln (E851mln allotted) of the 2.50% Feb-35 Green Bund. Avg yield 2.61% (bid-to-offer 1.62x; bid-to-cover 1.91x).

GBP: Sustainability of GBP Strength Rests on Fiscal Policy Mix

- Outside of JPY strength, GBP's gains today standout despite a lack of local drivers. The Gilt curve and, in particular, the longer-end has regained a sense of stability after being marked sharply higher into the end of August. How valid and long-lasting this market sustainability proves to be should determine GBP/USD's ability to correct back above 1.3595 and make meaningful headway toward the bull trigger of the July 1st high at 1.3789.

- While the initial cabinet reshuffle last week did little to shore up confidence headed into the Autumn Budget, there are some signs that - at least - the government are recognizing and looking to act on the economic challenges facing the UK. The appointment of economic advisers (including former BoE Deputy Governor Shafik) to No 10 suggests a renewed urgency on invigorating growth, and FT reports today that Chancellor Reeves is to tell ministers they must fight inflation, scrap the regulatory burden, resist public sector pay demands and back fiscal rules further bolster this view.

- Whether this economic focus changes to the outcomes of the UK Budget remains to be seen - but recognition that economic issues need addressing support the argument for conviction on November 26th. A fiscal policy mix that meets this requirement and placates back bencher preferences will, however, be a difficult task. As such, efforts to increase the efficiency of the state are likely to fall on cuts to the civil service, more restricted departmental budgets and regulatory reform - leaving welfare state spending a material issue in the medium-term.

FOREX: JPY Rallies as BoJ Report Suggests More Aggressive Tightening Schedule

- JPY started the session strong, carrying the theme through late Asia and early European trade. The stronger JPY helped aide USD weakness, prompting raising the importance of nearby USD Index support at 97.109, and into the bear trigger of 96.377. It's notable that today's USD weakness has not been triggered by a renewed pull lower in US yields (US 10y yield closed lower by over 5bps yesterday, but has steadied so far this morning).

- Instead, USDJPY selling looks the primary driver. JPY futures volumes are well ahead of average, with volumes supported by a sources report suggesting the BoJ see a strong chance of a further rate hike this year, despite the recent political upheaval in the ruling LDP. The piece reported some BoJ sources seeing the October meeting as a potential opportunity for tightening - a much more aggressive schedule than currently priced in.

- USD/JPY traded through the September lows in response, narrowing the gap with both the 100-dma of Y145.93 as well as decent-sized expiries into Y145.85-00 ($1.4bln).

- Focus for the duration of Tuesday trade rests on the annual benchmark payrolls revisions - which are expected to be marked notably lower for the 12 months into March - helping bolster the Oval Office's case for a more aggressive approach to monetary easing from the Fed. This morning's USD weakness is helping prop the major pairs through to new September highs headed into this week's economic and inflation data (today benchmark payrolls revisions, Wednesday PPI, Thursday CPI).

OPTIONS: USDJPY Slippage Puts Sizeable Strikes into Play

With light newsflow, sizeable option expiries helped exert influence over Monday range - helping contain the EUR/USD rally into the 10am NY cut. Today's expiry slate looks less effectual for EUR/USD, however GBP/USD's rally off yesterday's 1.3483 low brings today's $1.3595-00 strike into play. Meanwhile, USD/JPY's BoJ triggered slip today puts spot nearer decent-sized expiries at Y145.85-00 ($1.4bln)

- EUR/USD: $1.1650-70(E1.0bln), $1.1685-05(E2.3bln), $1.1750(E835mln), $1.1790-00(E1.2bln)

- USD/JPY: Y145.85-00($1.4bln), Y150.00($1.1bln)

- GBP/USD: $1.3595-20(Gbp1.0bln)

EQUITIES: Bull Cycle in E-Mini S&P Intact, Contract Close to Recent Highs

- A corrective bear cycle in Eurostoxx 50 futures remains in play. Recent weakness resulted in a breach of 5368.87, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5377.49, the 20-day EMA. A clear break of it would be a bullish development.

- A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6456.35, the 20-day EMA.

COMMODITIES: Gold Remains in a Clear Bull Cycle, Monday's Gains Reinforce Theme

- The trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from last Tuesday’s high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Gold remains in a clear bull cycle and last week’s gains plus Monday’s bullish start to the week, reinforce current conditions. The yellow metal has traded to a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a Fibonacci projection. Initial firm support lies at $3458.7, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 09/09/2025 | 1150/1350 | SNB's Schlegel at BIS fireside chat | ||

| 09/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 09/09/2025 | 1400/1000 | *** | Preliminary Benchmark Revision | |

| 09/09/2025 | 1515/1615 | BOE Breeden Moderates BIS Fireside Chat | ||

| 09/09/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 10/09/2025 | 0130/0930 | *** | CPI | |

| 10/09/2025 | 0130/0930 | *** | Producer Price Index | |

| 10/09/2025 | 0600/0800 | *** | CPI Norway | |

| 10/09/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/09/2025 | 0700/0900 | ** | Industrial Production | |

| 10/09/2025 | 0800/1000 | * | Industrial Production | |

| 10/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 10/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 10/09/2025 | 1145/1345 | SNB's Schlegel on Central Bank Communication in Vezia | ||

| 10/09/2025 | - | *** | Money Supply | |

| 10/09/2025 | - | *** | New Loans | |

| 10/09/2025 | - | *** | Social Financing | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 10/09/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result |