MNI US MARKETS ANALYSIS - Tsys Offered into Jobs Data

Highlights:

- Treasuries look vulnerable into run of jobs data, unemployment rate

- No post-payrolls Fedspeak on the schedule, but Waller will be watched carefully for the initial reaction pre-market tomorrow

- GBP gains on the back of punchy wage numbers, but rate cut this week still most likely outcome

US TSYS: A Bearish Outlook For TY Awaiting NFPs and Retail Sales

Treasuries have pared small further gains overnight over the past two hours as US desks start to filter in. Cumulative overnight volumes have been very thin ahead of an important docket that sees the November payrolls report and October retail sales as well as flash PMIs for December and the latest weekly ADP update to main a few other releases.

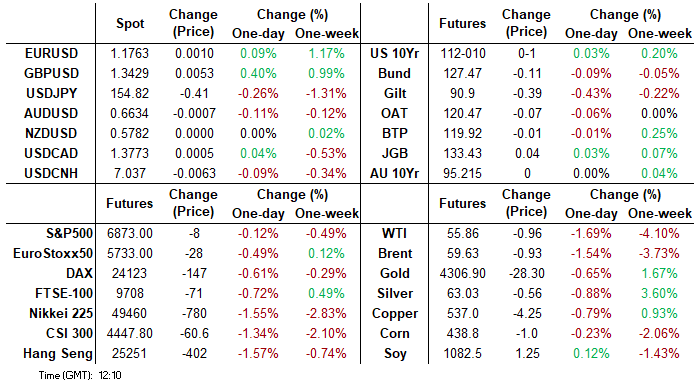

- Cash yields are 0-0.5bp higher on the day.

- 5s30s earlier hit 113.4bp for a fresh three-month high, currently at 112.4bp.

- TYH6 trades at 112-10 (+01) on very thin volumes of 190k, holding within yesterday’s range.

- The technical set-up points to a bearish outlook with support at the bear trigger of 111-29 (Dec 10 low) before 111-19 (Fibo projection). Resistance meanwhile is seen at 112-20 (20-day EMA) before 112-23 (Dec 11 high).

- Data: Weekly ADP (0815ET), NFP Nov (0830ET), Retail sales Oct (0830ET), NY Fed services (0830ET), Weekly Redbook retail sales (0855ET), S&P Global PMIs Dec prelim (0945ET), Business inventories Sep (1000ET)

- Bill issuance: US Tsy $75B 6W Bill auction (1130ET)

- Politics: Trump in ambassador credentialing ceremony (1400ET, closed press), Trump participates in Hanukkah reception (2015ET)

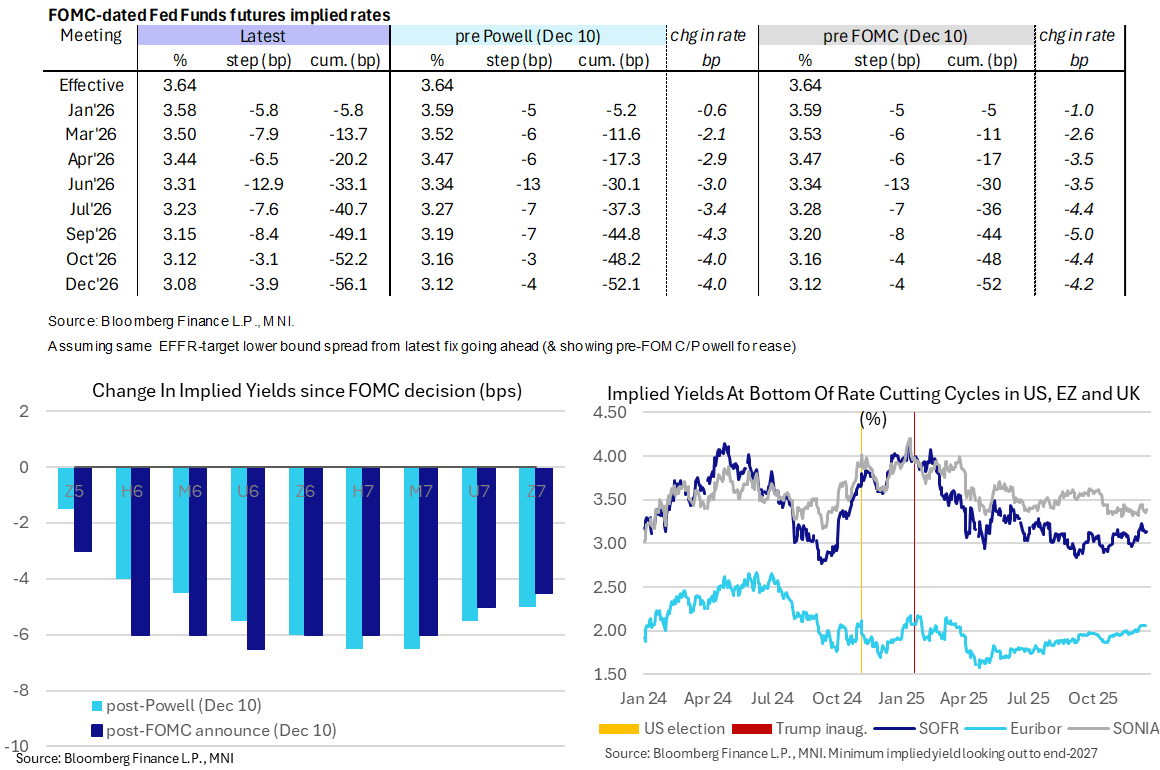

STIR: Next Fed Cut Fully Priced For June Ahead Of NFPs and Retail Sales

- Fed Funds implied rates are unchanged overnight for near-term meetings but up to 1.5bp higher for meetings in 2H26 despite crude oil futures slipping another 1%.

- It comes ahead of an important NFP release, with two months of payrolls data and a single month of unemployment data, with retail sales for October landing simultaneously and expected to show a generally solid start to Q4.

- MNI Payrolls Preview: https://media.marketnews.com/USNFP_Nov2025_Preview_postshutdown_392dffc2d3.pdf

- There is currently no Fedspeak scheduled today, with Fed Gov. Waller (voter, dove) first in line for a payrolls reaction tomorrow at 0815ET when he speaks on the economic outlook.

- Cumulative cuts from 3.64% effective: 7bp Jan, 14bp Mar, 20bp Apr, 34bp Jun, 49.5bp Sep and 57bp Dec.

- SOFR futures are up to 1 tick lower in 2H26/1H27 contracts, with the terminal implied yield of 3.14% (Z6) holding within recent ranges.

- A reminder that former Fed Governor Kevin Warsh is now a slight favorite for next Fed Chair after a further boost yesterday, at 44% on Polymarket vs 42% for NEC’s Kevin Hassett.

MNI PREVIEWS

MNI US PAYROLLS PREVIEW: Double NFPs and a Single Unemployment Update

It’s an unusual payrolls release this month, with two months of data for the establishment survey (payrolls, hours worked and wages) for October and November plus a single report for the household survey (unemployment and participation rates) in November. The BLS wasn’t able to conduct a household survey for October under the government shutdown and will have had to run the November survey shortly after the government re-opened. Nonfarm payrolls growth is seen at 50k in November after slipping circa -25k in October, with the latter coming from a wide range of expectations for the impact of DOGE deferred resignations.

MNI UK DATA PREVIEW: December 2025 Release

Both labour market data and CPI data will be critical for the expected MPC cut on Thursday (which at the time of writing all of the sellside previews that we had seen had pencilled in a 25bp cut while markets priced 22bp). In order to get a cut across the line it is likely that all four members who voted for a November cut repeat their votes and likely that we need Governor Bailey to join them. There is additional focus on Lombardelli potentially joining the doves, with some also not ruling out a potential 7-2 vote.

MNI NBH PREVIEW: Chance of a Dovish Shift

The final NBH meeting of the year could present the central bank with an opportunity to lay the groundwork for a rate cut in Q1/Q2 next year. While the overwhelming likelihood is that the base rate will remain unchanged at 6.50% until after the elections next year, the December Inflation Report may present the case for a dovish shift in language. Among sell-side, the base rate is unanimously expected to be unchanged, but the prospect of a communication tweak is considered.

MNI CHILE CB PREVIEW: Rate Cut Seen as CPI Fears Ease

The BCCh is widely expected to deliver a 25bp reference rate cut to 4.50% on Tuesday after benign CPI data over the last two months have eased policymakers concerns about persistent inflation pressures. Headline inflation has fallen back within the central bank’s 2-4% target range over the period, while the policy relevant ex-volatiles measure has also declined to below the central bank’s latest projections.

MNI BI PREVIEW: BI Holds, Rupiah Stability Key

Bank Indonesia announces its decision on Wednesday and like the last couple of meetings it is likely to be a balanced discussion. Currently 21 analysts on Bloomberg expect rates to remain unchanged at 4.75% and 11 are forecasting a 25bp cut. In Q3, BI's focus was on growth but this quarter it appears to have returned to FX stability. USDIDR is down 0.5% and the BIS IDR NEER is up 0.3% since the last meeting but the rupiah remains weaker than its mid-year levels and so BI may want to see further strengthening before easing again.

MNI BOT PREVIEW: Macro Conditions Warrant Easing

Bank of Thailand is likely to announce a 25bp rate cut on Wednesday, which would bring it to 1.25% and easing in 2025 to 100bp. With core inflation remaining below the bottom of BoT's target band, severe weather events, disappointing Q3 GDP, slowing export growth and continued baht strength, the central bank is likely to deem the timing this month as appropriate.

MNI ECB PREVIEW: Relative Resilience Confirms In A Good Place

We have published and e-mailed to subscribers the MNI ECB Preview, including MNI analysis plus analyst views on what to expect at this month's meeting.

MNI CNB PREVIEW: Repo Rate To End 2025 At 3.50%

The Czech National Bank (CNB) will almost certainly deliver a well-telegraphed unanimous decision to keep the two-week reference rate unchanged at 3.50% at the final meeting of this year as concerns about familiar inflationary risks continue to linger. Although headline inflation moderated to +2.1% Y/Y in November, the property market is running hot, wages are still growing at pace, and there is considerable uncertainty about the fiscal outlook under the new government. Meanwhile, the key interest rate already sits at the upper end of the range of neutral-rate estimates, keeping the room for further rate cuts limited.

SOFR: Net Long Setting Dominated In Futures On Monday

OI data points to net long setting dominating in SOFR futures on Monday, with only limited, isolated instances of net short cover seen as contracts ticked higher on the day.

| 15-Dec-25 | 12-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,299,510 | 1,296,569 | +2,941 | Whites | +4,277 |

SFRZ5 | 1,569,979 | 1,575,061 | -5,082 | Reds | +53,885 |

SFRH6 | 1,390,362 | 1,385,834 | +4,528 | Greens | +50,805 |

SFRM6 | 1,117,924 | 1,116,034 | +1,890 | Blues | +29,110 |

SFRU6 | 1,184,180 | 1,181,534 | +2,646 |

|

|

SFRZ6 | 1,146,221 | 1,126,261 | +19,960 |

|

|

SFRH7 | 887,420 | 854,900 | +32,520 |

|

|

SFRM7 | 766,542 | 767,783 | -1,241 |

|

|

SFRU7 | 832,506 | 816,721 | +15,785 |

|

|

SFRZ7 | 841,487 | 830,534 | +10,953 |

|

|

SFRH8 | 478,724 | 459,804 | +18,920 |

|

|

SFRM8 | 416,681 | 411,534 | +5,147 |

|

|

SFRU8 | 384,614 | 389,172 | -4,558 |

|

|

SFRZ8 | 323,557 | 293,990 | +29,567 |

|

|

SFRH9 | 196,101 | 190,702 | +5,399 |

|

|

SFRM9 | 207,932 | 209,230 | -1,298 |

|

|

US SWAPS: Front End Spread Outperformance Intact, Sell-Side Expect Extension

Front end U.S. swap spread outperformance remains a feature after last week’s frontloaded Reserve Manage Purchases (RMP) announcement from the Fed.

- TD Securities have joined the list of sell-side names looking for an extension of this move, issuing a recommendation to enter 3s10s spread curve flatteners late on Monday.

- They anticipate improved funding conditions on the back of the Fed’s RMP announcement (driving further outperformance in the front end of the curve), as well as flagging an attractive relative value proposition (10s rich in ASWs and vs. the Tsy curve) and a positive carry profile.

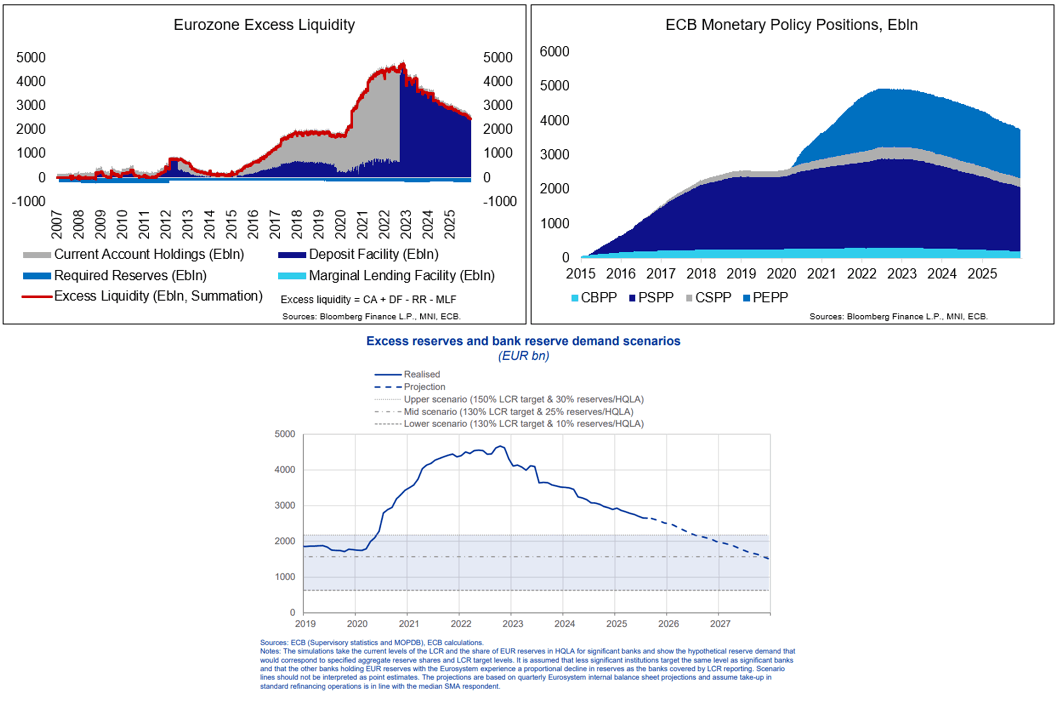

ECB: Balance Sheet Suggests Little Need For Liquidity Action in Eurozone

ECB balance sheet data ahead of Thursday's meeting confirms that excess reserves remain well above levels approaching scarcity across the Eurozone, leaving little pressure on the ECB to act on the structural bond portfolio for now.

- This is contrary to the Fed & BoE which both have provided fresh liquidity support/increased focus on bank liquidity provisions in recent months, after bank reserves in their respective jurisdictions moved towards / reached a less abundant state. Latest ECB projections see excess reserves hitting bank demand in mid-2026 in an "upper scenario" but not until late 2027 in a "mid scenario".

- Passive run-off of the ECB balance sheet can be bumpy in the short term but a longer-term downtrend remains intact. This led Eurozone excess liquidity to decrease by roughly €32bln/month YTD 2025, bringing the measure to around €2.465trl, down by 48% from the series' high of €4.748trl in November 2022.

- When liquidity ultimately becomes "scarce" (or close to it) that will show in money market tensions and increased takeup in the ECB's standard refinancing operations, neither of which are apparent at this stage.

The long-term liquidity decline since the peak was initially been driven by a roll-off of the ECB's TLTROs (with the TLTRO III programme starting in 2019 with three-year maturities and with the final maturity in Dec 2024) but mostly comes on the back of the declining ECB's monetary policy positions (PEPP + APP), which are standing at a current €3.753trl combined. Amongst the policy positions, the ECB envisages a further average monthly roll-off of around €13.4bln of the PEPP through Dec-26 and of around €28.6bln of the APP through Jul-26 (respective f'cast horizons).

- Latest ECBspeak on the balance sheet came from Schnabel in a speech titled "Towards a new Eurosystem balance sheet" (speech here, later slides here. Mirroring the above, Schnabel highlighted:

- "Quantitative normalisation is proceeding smoothly, with strong liquidity positions of banks and abundant excess liquidity"

- "Operational framework suggests a sequence for how to supply reserves in the future, with a persistent take-up of standard refinancing operations to precede the launch of structural operations, starting with longer-term refinancing operations and followed by a structural securities portfolio"

- "Considerations about stance neutrality, policy space and financial soundness suggest tilting the new structural securities portfolio towards shorter-term securities"

INR: USD/INR Rally Shows No Signs of Stalling, No Progress on US-India Deal

- USD/INR closed above 91.00 for the first time, with increased hedging activity and portfolio outflows reportedly a headwind for the rupee on an intraday basis. According to Reuters, the likely maturity of positions in the NDF market put pressure on the currency, though dollar sales by state-run banks – most likely on behalf of the RBI – slowed its decline.

- At the start of the month, it was reported that India's central bank would tolerate a weaker rupee, indicating that it will intervene mostly to curb sharp volatility or on any signs of a speculative build-up rather than to defend any specific level. Since then, the rupee has been the worst performing APAC currency by some margin. 1-month implied vols are up around 0.75ppts on the month, but below the November highs, and at the same time the 25 delta 1-month option vol skew has swung in favour of calls, implying that option markets are hedging against the risk of further rupee weakness ahead.

- The lack of any substantial progress on trade talks with the US has been a key headwind for the rupee. Trade Minister Agrawal said Monday that India is engaged with the US to see if they can close a deal "sooner than later" – but no specific timeline was provided.

FOREX: Dollar Tilts Lower Ahead of Payrolls, JPY and GBP Outperforming

- The Dollar index is 0.1% in the red Tuesday, hovering just above the recent pullback lows as we approach the return of tier-one data from the US later today. GBP outperforms across the G10 following UK labour market data that showed higher-than-expected wage data, while risk-off sentiment overnight has moderately boosted the yen. Both French and German flash services PMIs were a touch weaker-than-expected but have done little to move the EUR needle this morning.

- GBP added to the morning's gains on the back of a firm UK PMI print, with GBPUSD comfortably clear through yesterday's highs above the 1.34 handle. Price action narrows the gap with major resistance into 1.3438 - the multi-month high. Meanwhile, EURGBP has slipped 0.2% in tandem, and with current spot levels of 0.8771, may have further to run towards last week’s lows at 0.8720.

- Weakness for major equity benchmarks across the APAC session, led by tech names, has boosted the Japanese yen, with USDJPY slipping to a new weekly low of 154.68. Despite the underlying bullish theme for USDJPY, support at 154.00, the 50-day EMA, remains exposed. A clear breach of this average would undermine the bull theme and signal scope for a deeper retracement.

- While the Euro has not been impacted by today’s flash PMI’s, EURUSD is consolidating close to recent highs around 1.1760. With multiple tier-one data releases from the US upcoming, as well as the ECB decision, market attention will be firmly on the pair. Recent gains have reinforced a bull theme highlighting potential for an extension higher. Sights are on 1.1779 next, the October 1 high.

- All focus on US data later today, with a double release of NFP included in the employment report, alongside retail sales data for October.

OPTIONS: Expiries for Dec16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1750-55(E1.8bln)

- USD/JPY: Y156.00($1.1bln)

- GBP/USD: $1.3500(Gbp3.8bln)

- NZD/USD: $0.5845-50(N$540mln)

- USD/CAD: C$1.3750($885mln)

EQUITIES: Current Bull Cycle in Eurostoxx 50 Futures Remains Intact

- The current bull cycle in Eurostoxx 50 futures remains intact. Price is trading above the 20- and 50-day EMAs, and has cleared 5742.40, 76.4% of the Nov 13 - 21 bear leg. The breach of this latter price point paves the way for an extension towards 5825.00, the Nov 13 high and the bull trigger. First key support to watch lies at 5645.93, the 50-day EMA. A clear break of the EMA would highlight a potential short-term reversal.

- A bull cycle in S&P E-Minis remains intact and the latest pullback - for now - is considered corrective. Initial support to watch is 6830.94, the 50-day EMA. A clear break of this average would signal scope for a deeper retracement. Note that the key support and reversal trigger lies at 6583.00, the Nov 21 low. For bulls, a resumption of gains would refocus attention on the key resistance and bull trigger at 7014.00, the Oct 30 high.

COMMODITIES: WTI Futures Probing Key Support and Bear Trigger at $55.99

- A bearish theme in WTI futures remains intact and recent weakness reinforces this theme. MA studies are in a bear-mode position, highlighting a dominant downtrend. Sights are on key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend and open $54.72, the Apr 9 low. Key short-term resistance to watch is $61.84, the Oct 24 high. First resistance is at $59.43, the 50- day EMA.

- A bullish theme in Gold remains intact. The bear phase between Oct 20 - 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch is the 50-day EMA, at $4078.9. Clearance of this EMA would signal scope for a deeper retracement. Attention is on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 16/12/2025 | 1445/0945 | *** | S&P Global Services Index (flash) | |

| 16/12/2025 | 1500/1000 | * | Business Inventories | |

| 16/12/2025 | 1745/1245 | BOC Gov Macklem speech in Montreal | ||

| 17/12/2025 | 2350/0850 | * | Machinery orders | |

| 17/12/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 17/12/2025 | 0700/0700 | *** | Producer Prices | |

| 17/12/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 17/12/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 17/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 17/12/2025 | 1315/0815 | Fed Governor Christopher Waller | ||

| 17/12/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/12/2025 | 1405/0905 | New York Fed's John Williams | ||

| 17/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 17/12/2025 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 17/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/12/2025 | 2145/1045 | *** | GDP |