FOREX: Dollar Tilts Lower Ahead of Payrolls, JPY and GBP Outperforming

Dec-16 10:29

- The Dollar index is 0.1% in the red Tuesday, hovering just above the recent pullback lows as we approach the return of tier-one data from the US later today. GBP outperforms across the G10 following UK labour market data that showed higher-than-expected wage data, while risk-off sentiment overnight has moderately boosted the yen. Both French and German flash services PMIs were a touch weaker-than-expected but have done little to move the EUR needle this morning.

- GBP added to the morning's gains on the back of a firm UK PMI print, with GBPUSD comfortably clear through yesterday's highs above the 1.34 handle. Price action narrows the gap with major resistance into 1.3438 - the multi-month high. Meanwhile, EURGBP has slipped 0.2% in tandem, and with current spot levels of 0.8771, may have further to run towards last week’s lows at 0.8720.

- Weakness for major equity benchmarks across the APAC session, led by tech names, has boosted the Japanese yen, with USDJPY slipping to a new weekly low of 154.68. Despite the underlying bullish theme for USDJPY, support at 154.00, the 50-day EMA, remains exposed. A clear breach of this average would undermine the bull theme and signal scope for a deeper retracement.

- While the Euro has not been impacted by today’s flash PMI’s, EURUSD is consolidating close to recent highs around 1.1760. With multiple tier-one data releases from the US upcoming, as well as the ECB decision, market attention will be firmly on the pair. Recent gains have reinforced a bull theme highlighting potential for an extension higher. Sights are on 1.1779 next, the October 1 high.

- All focus on US data later today, with a double release of NFP included in the employment report, alongside retail sales data for October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

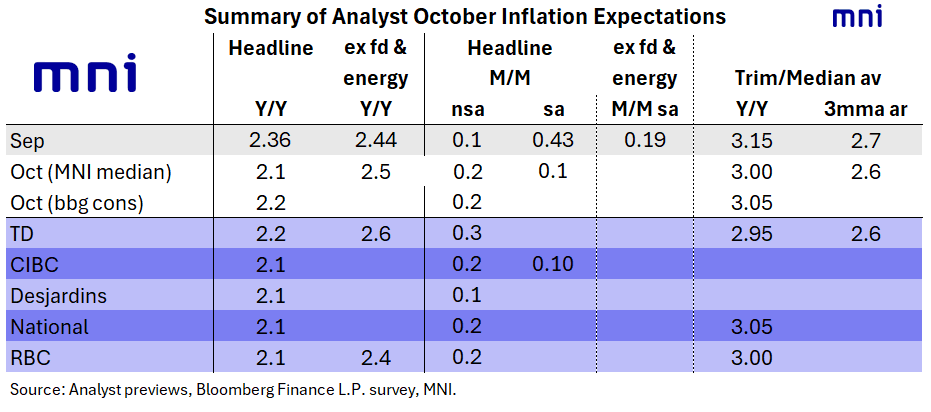

CANADA DATA: October CPI Preview: Analysts Eye Lower Gasoline Prices (2/2)

Nov-14 21:30

Canadian analysts' expectations for October inflation:

- CIBC: "Inflation should have eased slightly in October, mainly due to a drop in gasoline prices following an increase in the prior month that was atypical of usual seasonal patterns....Measures of core inflation may not decelerate as much, with rent inflation still stubbornly higher relative to market asking prices.... Inflationary pressures should have eased again relative to the prior month but, with various year-over-year core measures still averaging closer to 3% than 2%, the inflation data are likely to reaffirm that the Bank of Canada is on hold for the foreseeable future."

- Desjardins: "The removal of retaliatory tariffs last month continues to filter through to consumer prices, which should help temper headline inflation in the coming months. With goods inflation excluding food and energy already trending lower, the elimination of countertariffs is expected to further support this normalization. Services inflation, which remained sticky due to strong readings in late 2024, is likely to continue its downward trajectory, with additional progress anticipated through Q4. A similar trend is evident in the Bank of Canada’s core measures, which likely moderated slightly in October but remain near 3%."

- National: "Despite a drop in energy prices, headline prices may still have increased 0.2% in the month (not seasonally adjusted). If we’re right, the annual inflation rate could decline by three-tenths of a percentage point to 2.1% as a result of a highly negative base effect. Looking at the Bank of Canada's core measures, we expect the CPI-med to move from 3.2% to 3.1% on an annual basis, while the CPI-trim should ease from 3.1% to 3.0%.

- RBC: "moderation is expected to be primarily driven by lower gasoline prices, which fell 5% from September. We expect food price growth to hold close to September’s 3.8% annual rate in October. The October data will include the annual update on property tax prices in the CPI data. Significant property tax increases again took effect in some major population centers, but nationally we expect a smaller increase (4%) than the 6% increase in October a year ago. Headline CPI growth continues to be distorted on the downside by the removal of the carbon tax from energy products in most provinces in April. Broader measures of ‘core’ inflation are expected to remain above the Bank of Canada’s 2% target rate in October."

- TD: "A larger drag from energy and further disinflation in shelter should drive the headline print, while core measures edge lower to 2.95% y/y in a sign of thawing underlying price pressures. However, we don't expect material implications for the near-term rate outlook given hawkish BoC guidance last month."

CANADA DATA: October CPI Preview: Moderation Won't Sway BOC From Holding (1/2)

Nov-14 21:24

Canadian CPI is expected to have pulled back in October from September's 7-month high 2.4% Y/Y. Consensus (Bloomberg median) sees October CPI at 2.2% Y/Y (2.4% prior), with M/M at 0.2% (0.1% prior), while the average Median/Trim measure is seen at 3.05% (3.15% prior).

- MNI's analyst median skews a little softer than that. In the next note we include some sell-side expectations for Monday's release - several haven't yet published their forecasts but we will provide our usual roundup on Monday ahead of the print.

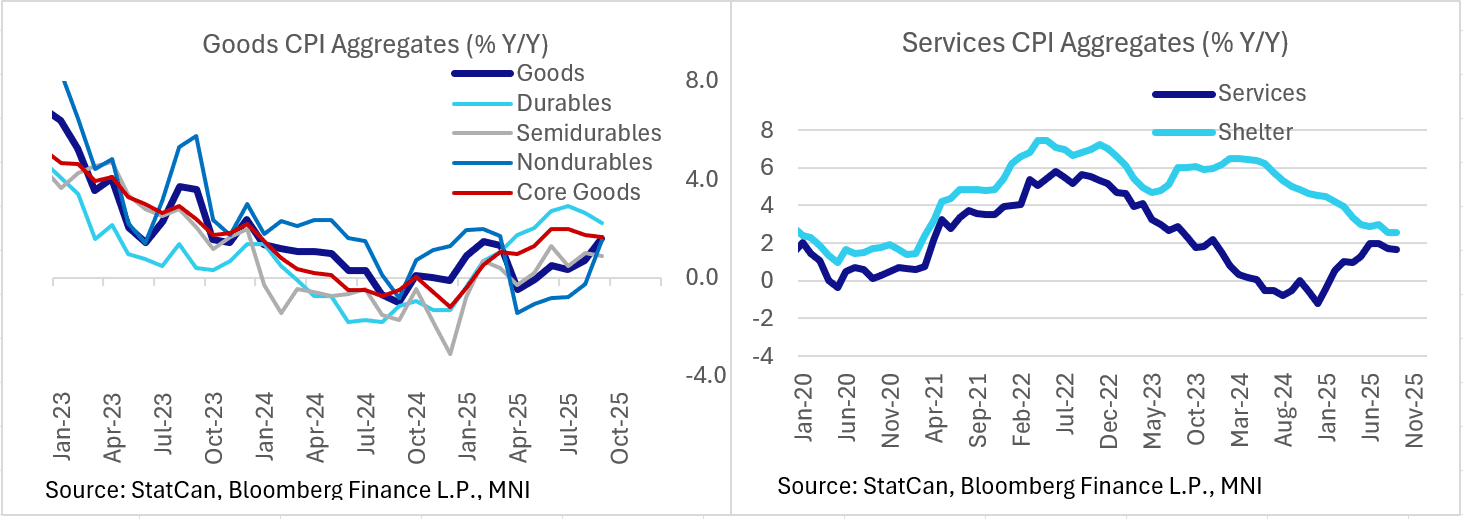

- A variety of factors are seen behind the moderation, including Ottawa's removal of retaliatory tariffs on the US in September, as well as softer gasoline prices. Overall, core goods inflation is moderating with core services merely a little stickier, and it was largely food/energy inflation and downstream effects thereof that spurred the latest tickup in overall CPI.

- The standout takeaway from the September CPI report was in the stubborn trim/median average failing to decelerate in the month as expected. Though that particular measure has been increasingly discounted by Bank of Canada policymakers, core metrics were also largely sequentially steady/higher. None appeared to be game-changers however in terms of the overall consensus narrative of gradual disinflation from the summer's highs but nonetheless ensured the report carried a slightly hawkish tone overall with continued evidence that prices may be a little sticker than hoped.

- October's data are unlikely to change the Bank of Canada's assessment at the October meeting that "Looking at the full range of inflation indicators, Governing Council concluded that underlying inflation was still around 2½%."

- In any case they "acknowledged that year-over-year inflation would be choppy in the coming months" so would be likely to maintain the bias to hold rates for the foreseeable future even in the event of a downside surprise.

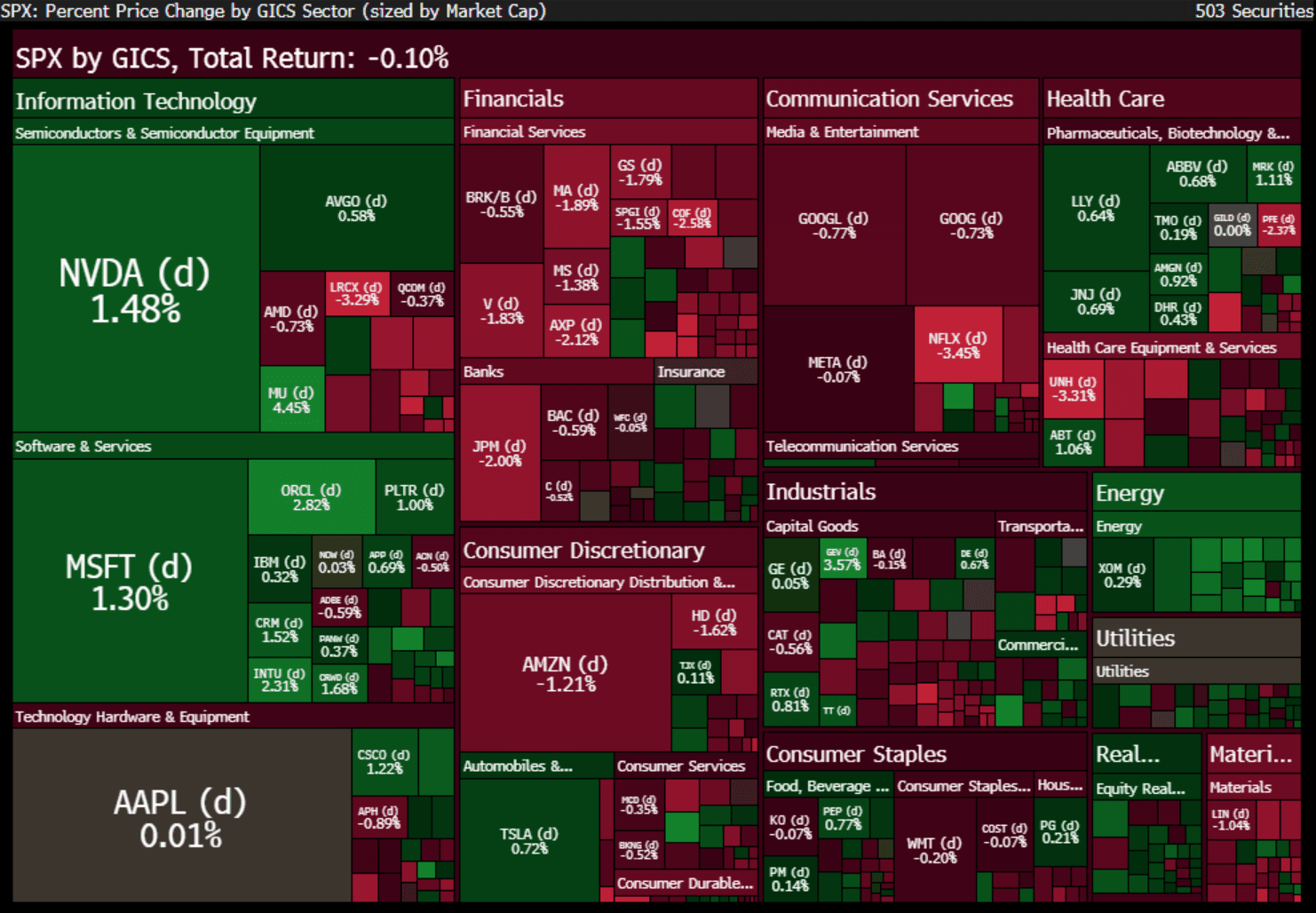

US STOCKS CLOSE: Equities Recover From Intraday Pullback

Nov-14 21:07

Equities recovered from a sharp intraday sell-off to close roughly flat Friday, with the Nasdaq and S&P 500 almost unchanged but the the Dow Jones retracing 0.7% after Thursday's outperformance.

- Reeling from concerns over AI-related valuations and waning prospects for a December Fed cut, the S&P fell as much as 1.3% (6,646.87) which would have marked the lowest close in a month, but bounced to trade roughly flat on the session.

- Energy (+1.4%) and tech (0.7%) outperformed on the S&P 500, with losses led by financials (-1.0%) and materials (-1.2%).

- Megacaps NVidia (+1.6%) and Microsoft (+1.3%) were the biggest upside contributors, offsetting downside for Google (-0.7%), Netflix (-3.4%) and Amazon (-1.1%) in the tech/communications space, while JPM (-1.8%), Visa (-1.7%) and Mastercard (-1.8%) pulled down financials.

- Latest futures levels: Dow Jones mini down 325 pts or -0.68% at 47253, S&P 500 mini down 6.25 pts or -0.09% at 6762.5, NASDAQ mini down 13.75 pts or -0.05% at 25125.25.