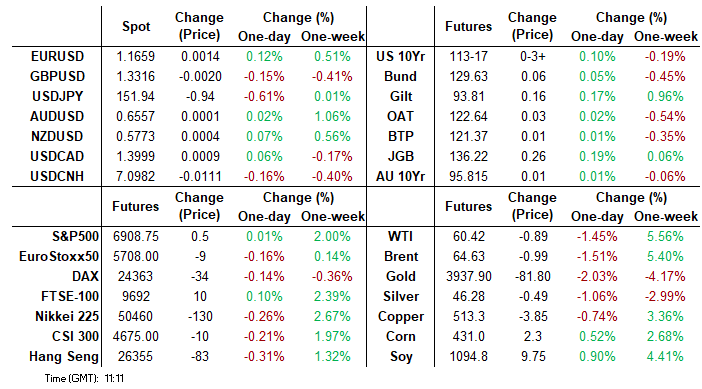

MNI US MARKETS ANALYSIS - Tsys Focus Shifts to 7y Supply

Highlights:

- US, Japan sign key mineral deal and formal investment pledge

- Treasuries little changed with focus on the upcoming 7yr supply

- GBP weaker, Gilts stronger as fiscal picture may trigger further tax rises

US TSYS: Little Changed; Consumer Confidence and 7Y Supply Lead Docket

- Treasuries are little changed on the day, with yields between +/- 0.5bps, consolidating yesterday’s twist flattening.

- Early attention could be on geopol headlines, including with President Trump at a dinner with business leaders in Tokyo.

- We suspect today’s data focus is on the Conference Board consumer survey for October, especially the labor differential which in recent months has continued to imply a steady drift higher in the unemployment rate.

- Today also sees further note issuance with 7Y supply after yesterday’s double 2Y and 5Y auctions of which both were near in-line.

- The FOMC tomorrow, Trump-Xi Thursday and big tech earnings loom large this week.

- Fed Funds implied rates are unchanged on the day, pointing to a 25bp cut tomorrow and a cumulative 49bp to year-end, before 73.5bp for March and 93bp for June.

- TYZ5 trades at 113-16 (+02+) on modest volumes of 245k, having kept to narrow ranges of 113-14+ to 113-18+.

- It consolidates yesterday’s lift off lows of 113-04, in a move that probed support at 113-06+ (20-day EMA) and opened 112-25+ (50-day EMA). Recent weakness appears to be corrective with a bullish structure still in place, with resistance at 113-24 (post-CPI high) before 114-02 (Oct 17 high).

- Data: FHFA/S&P Cotality House Prices Aug (0900ET), Conf Board consumer survey Oct (1000ET), Richmond Fed mfg Oct (1000ET), Dallas Fed Services Oct (1030ET)

- Coupon issuance: Tsy $44B 7Y Note auction - 91282CPF2 (1300ET)

- Bill issuance: US Tsy $95B 6W & $50B 52W bill auctions (1130ET)

- Politics: Trump in Reception and Dinner with Business Leaders in Tokyo (0605ET)

US-JAPAN: Trump & Takaichi Sign Mineral Deal And Formalise Investment Pledge 1/2

US President Donald Trump and Japanese Prime Minister Sanae Takaichi have signed a critical mineral framework and formalised the implementation of a USD$550 Japanese investment pledge from Tokyo to ease a Memorandum of Understanding on trade that would cap tariffs on Japanese exports at 15% - including on autos -, signed on September 4.

- According to the Japanese Ministry of Finance, the investment pledge taps private funding from major Japanese firms, including Westinghouse, GE Vernova Hitachi, Mitsubishi, Panasonic, and Soft Bank, to finance investment in energy and power primarily related to Artificial Intelligence.

- At 06:00 ET 10:00 GMT 19:00 JST, Trump will participate in a reception with Japanese business leaders, where Toyota is expected to announce a plan to manufacture cars in the US.

- The trade deal is also expected to increase Tokyo’s purchases of US LNG, reducing reliance on Russia’s Sakhalin-2 project, which makes up roughly 9% of Japanese imports.

- The US and Japan said in a joint statement, “The Agreement will help both countries to strengthen economic security, promote economic growth, and thereby continuously lead to global prosperity,” noting that relevant ministers will take further steps for a “NEW GOLDEN AGE” of the ever-growing US-Japan Alliance.

- The framework deal on rare earths and critical minerals notes that the two countries will take steps to accelerate permitting, mobilise capital to secure supply chains, and invest in mining and processing.

US-JAPAN: Trump & Takaichi Sign Mineral Deal And Formalise Investment Pledge 2/2

Bullet continued. Earlier today, at a bilateral meeting, Takaichi leveraged her association with former Prime Minister Shinzo Abe to bolster her relationship with Trump. Taikachi pledged to increase defence spending, saying Japan is “ready to contribute even more proactively to peace and stability of the region,” addressing a longstanding Trump grievance.

- Bloomberg notes, “Trump said the US and Japan were looking to boost their joint shipbuilding capacity as his Commerce Secretary, Howard Lutnick, signed a memorandum of understanding with Japanese officials.”

- The agreement on rare earths, which follows similar deals with Australia, Malaysia, and Thailand, come as the Trump administration seeks to formalise an alternative rare earth supply chain to reduce reliance on China ahead of a key meeting between Trump and Chinese President Xi Jinping on the margins on Thursday.

- Reuters notes, “While dominated by China, the U.S. and Myanmar control 12% and 8% of global rare earth extraction, according to Eurasia Group, and Malaysia and Vietnam cover another 4% and 1% of processing, respectively.”

- Earlier, Treasury Secretary Scott Bessent noted in a readout of a meeting with Finance Minister Satsuki Katayama that he was “glad to hear the Minister’s perspective on Japanese fiscal measures" and "expressed his eagerness to learn more as the full package is worked out so as to better understand the potential impact.”

- Katayama told reporters he had “no direct talks about direction of monetary policy,” and noted there has been “no change to US-Japan joint statement on forex,” per Reuters.

EUROPE ISSUANCE UPDATE:

Slovakia syndication: Revised Guidance

- EUR Benchmark (MNI expects E1.5-E2.5bln) of the new 12-year Nov-37 SlovGB. Revised guidance: MS+100 Area (guidance was MS+105 Area), books in excess of E3.1bln.

Finland USD syndication: Guidance

- Benchmark (MNI expects USD1.0-1.5bln) of the new 5-year Nov-30 USD line. Guidance is SOFR MS+38bps area (IPTs were SOFR MS (S/A, 30/360) +40bp area (~CT5+9.6bps / ~ WI+9.9bps ), IOIs in excess of $2.4bn.

Italy auction results

- E2bln of the 2.10% Aug-27 BTP Short Term. Avg yield 2.15% (bid-to-cover 1.71x).

- E1.5bln of the 1.80% May-36 BTPei. Avg yield 1.72% (bid-to-cover 1.68x).

UK auction results

- GBP1.5bln of the 1.125% Sep-35 Linker. Avg yield 1.571% (bid-to-cover 2.94x).

Germany auction results

- Another weak German auction today of the 2.20% Oct-30 Bobl. Amount of bids remained roughly unchanged vs October 7, when the line was last issued.

- Demand metrics remained very weak despite picking up marginally vs Oct 7: * The auction was technically uncovered with a 0.94x bid-to-offer. Bid-to-cover also low at 1.24x. The lowprice achieved at the auction was above the pre-auction secondary market midprice, however.

- No discernible market reaction following the results.

- E4bln (E3.02bln allotted) of the 2.20% Oct-30 Bobl. Avg yield 2.21% (bid-to-offer 0.94x; bid-to-cover 1.24x).

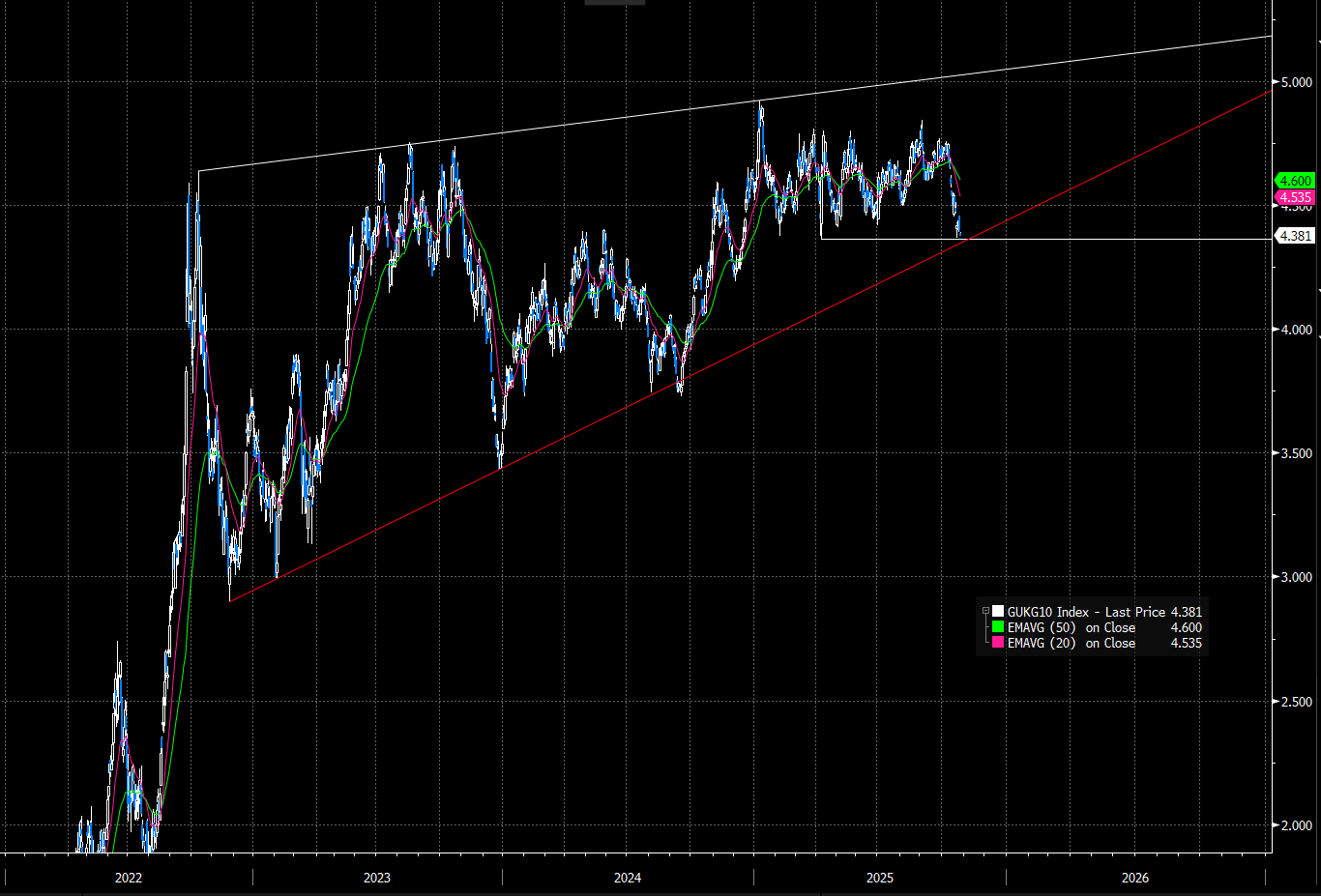

GILTS: Outperforming Bunds Across The Curve With More Fiscal Tightening Likely

Gilts outperform German peers across the curve, with the 10-year Gilt/Bund spread testing the March closing low of 177.5bps, down 1bp on the session. There are increasing signs that UK Chancellor Reeves will have to raise income tax at the November 26 budget to fill a widening fiscal hole, and potentially increase headroom above the ~GBP10bln seen at previous fiscal events.

- The FT reported yesterday evening that the OBR is expected to cut its trend productivity forecast by 0.3pp, larger than the 0.1-0.2pp that had been expected by most analysts/independent forecasters. The IFS’ Green Budget estimated that each 0.1pp downgrade to productivity would increase 2029-2030 PSNB by GBP7bln, so this downgrade implies a GBP21bln hit to public finances. A reminder that the YTD tracking error with existing OBR projections is also GBP7.23bln.

- 10-year Gilt yields are down 2bps to 4.38%, narrowing the gap to clustered support around 4.35% (April 7 low and trendline drawn from the November 2022 low). 30-year yields are down 1.5bps at typing, while 2- and 5-year yields have fallen almost 3bps.

- Gilt futures are +24 ticks at 93.89, just off opening highs of 93.91. A bull cycle remains intact, with moving average studies also highlighting a dominant uptrend. Initial resistance is the Oct 22 high at 93.93.

- The DMO will sell GBP1.5bln of the 1.125% Sep-35 linker at 1000GMT today.

- The BRC-NIQ Shop Price Monitor, released overnight, showed the first slowdown in the Y/Y pace of growth of the year, with overall shop price inflation falling to 1.0%Y/Y in October, from 1.4%Y/Y in September. And it helps to validate some of the food price falls seen in the official ONS CPI release - particularly on the ambient side. This seems to support that food price inflation may already have peaked, and may therefore give more confidence to MPC members ahead of the November policy decision.

- In GBP STIR markets, SONIA futures are +0.5 to +4.0 ticks through the blues. BOE-dated OIS price ~7bps of easing through November, and ~17bps of easing through year-end (the latter 1.5bps more dovish than yesterday's close)

Figure 1: 10-year Gilt Yields (Source: Bloomberg Finance L.P)

FOREX: Yen Snaps Losing Streak Following Sharp Rebound

- Japanese yen volatility has been the key feature for G10 FX markets on Tuesday, following details emanating surrounding the discussions between US and Japanese administrations. The US Treasury provided a read out of the Treasury Secretary and Japan FinMin meeting, with Bessent emphasizing the need for sound monetary policy to keep inflation expectations anchored and avoid FX volatility.

- USDJPY is currently down 0.65%, with the 151.76 session lows marking a 1% correction from yesterday’s highs of 153.26. First important support to watch lies at 151.09, the 20-day EMA.

- Weakness for GBP in early trade puts GBPUSD through yesterday’s lows of 1.3311 on decent volumes: GBP futures volumes suggest a flow-driven move rather than a headline or news trigger spell of weakness. The fiscal picture remains the key driver more broadly, particularly given the increasing signs that the Chancellor will have to raise income tax at this month’s budget to fill a widening fiscal hole. The GBPUSD bear trigger remains 1.3249, the October 14 low.

- NOK meanwhile also underperforms on pressured oil prices as fears around how much crude is actually coming off the market from earlier Russia sanctions have somewhat subsided. Expect global developments to continue dictating NOK price action in the near-term, with little in the way of market moving domestic data due ahead of Norges Bank's November decision. EURNOK stands at 11.67, with next resistance at 11.83, the Oct 17 high.

- Attention turns to central banks for the remainder of the week, with the Bank of Canada and FOMC both firmly seen to deliver cuts tomorrow, while the BoJ and ECB are expected to hold rates in their respective meetings on Thursday. Australian CPI and Spanish GDP are due Wednesday.

OPTIONS: Expiries for Oct28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E874mln), $1.1625-35(E1.9bln)

- USD/JPY: Y152.50($720mln), Y152.95-00($1.0bln), Y153.35-50($609mln)

- AUD/USD: $0.6475(A$573mln)

COMMODITIES: Gold Extends Bear Cycle

- The latest recovery in WTI futures appears corrective for now, however, note that price has traded through resistance at the 50-day EMA, at $61.14. The breach of this average signals scope for a stronger recovery. A resistance at $62.34, the Oct 8 high, has been pierced. A clear break of it would expose key resistance at $65.77, the Sep 26 high. Key support and the bear trigger has been defined at $55.96, the Low Oct 20.

- Gold is trading lower as it extends the bear cycle that started Oct 20. Note that the trend is overbought and a deeper retracement is allowing this condition to unwind. Support at the 20-day EMA, at $4045.9, has been breached, signalling scope for a deeper retracement, towards the 50-day EMA, at $3838.2. Key resistance and the bull trigger has been defined at $4381.5, the Oct 20 high. Initial resistance is at $4161.4, the Oct 22 high.

EQUITIES: Trend Condition for Equities Remains Bullish

- The trend condition in S&P E-Minis remains bullish and the contract traded higher Monday, as it started the week on a bullish note. The fresh cycle high confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. The 6900.00 handle has been cleared, opening 6953.25 next, a Fibonacci projection. Initial firm support to watch lies at 6748.48, the 20-day EMA.

- The trend structure in Eurostoxx 50 futures is bullish. Monday’s fresh cycle high reinforces a bull theme and maintains the rising price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 5727.18, a Fibonacci projection. First support lies at 5625.31, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 28/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/10/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 28/10/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/10/2025 | 1400/1000 | ** | housing vacancies | |

| 28/10/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 28/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/10/2025 | - | Bank of Japan Meeting | ||

| 29/10/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 29/10/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 29/10/2025 | 0030/1130 | *** | CPI inflation | |

| 29/10/2025 | 0700/0800 | Flash Quarterly GDP Indicator | ||

| 29/10/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 29/10/2025 | 0800/0900 | *** | GDP (p) | |

| 29/10/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 29/10/2025 | 0930/0930 | ** | BOE M4 | |

| 29/10/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 29/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 29/10/2025 | 1100/1200 | ** | PPI | |

| 29/10/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/10/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 29/10/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 29/10/2025 | 1430/1030 | BOC press conference | ||

| 29/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 29/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/10/2025 | 1800/1400 | *** | FOMC Statement |