MNI US MARKETS ANALYSIS - Trump Searches for "Real End"

Highlights:

- Trump drops G7 meeting to deal with escalating Israel-Iran crisis; wants a "real end" to the nuclear programme

- Markets muted into retail sales / import, export price indices as tomorrow sees Fed meeting

- USD/JPY shrugs off BoJ tweak to bond-buys

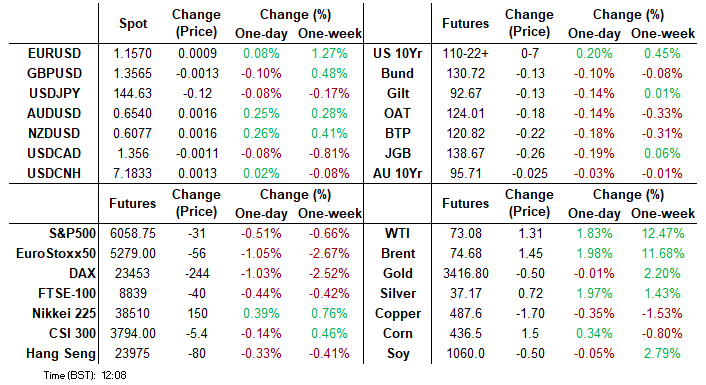

US TSYS: Narrow Ranges As Treasuries Outperform Europe Amidst Geopol Risks

- Treasuries have kept to narrow ranges overnight ever since opening firmer.

- They outperform European counterparts (e.g. 10Y Tsys -2.4bps vs +1.9bp Bunds & +2.9bp BTPs) in signs of some haven demand for US assets with Trump promising “bigger” and “better” than an Israel-Iran ceasefire on Truth Social and speaking to reporters on Air Force One.

- Geopolitics remains in focus as markets await more actionable headlines whilst there are some notable data updates today on day one of the two-day FOMC meeting.

- Cash yields are 2-2.5bp lower on the day, with declines slightly led by the belly.

- Curves consolidate yesterday’s steepening but remain comfortably off previous ytd highs, with 2s10s at 47.7bp (-0.7bp) and 5s30s at 93.0bp (+0.3bp).

- TYU5 has recently touched 110-23 (+ 07+) for joint overnight highs, although has remained within yesterday’s range throughout and cumulative volumes are modest at 275k.

- Resistance continues to be monitored, seen at 111-13 (Jun 13 high) and 111-14+ (Jun 5 high and 61.8% retrace of May 1-22 downleg), whilst support is seen at 109-28 (Jun 6/11 lows).

- Data: Retail sales May (0830ET), Import prices May (0830ET), NY Fed Services Jun (0830ET), IP/cap util May (0915ET), Business inventories Apr (1000ET), NAHB housing market index Jun (1000ET)

- Coupon issuance: US Tsy $23B 5Y TIPS re-open auction - 91282CNB3 (1300ET)

- Bill issuance: US Tsy $55B 6W bill auction (1130ET)

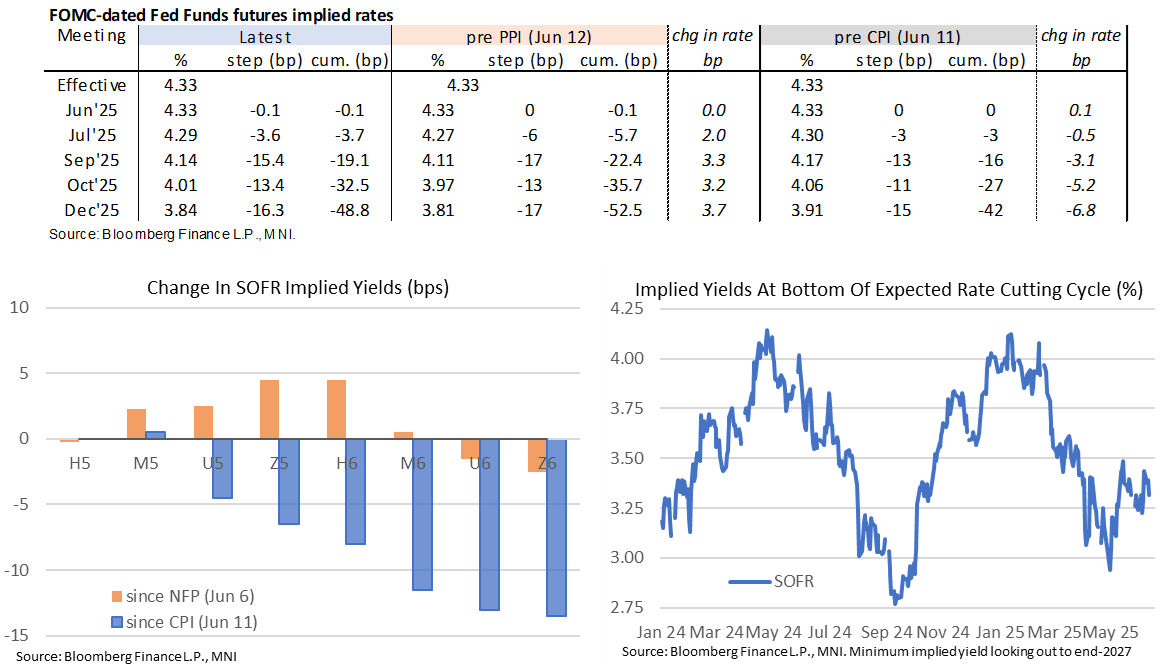

STIR: May Hard Data Update Due As FOMC Meeting Gets Underway

- Fed Funds implied rates are up to 2bp lower on the day for 2025 meetings but continue to hold little odds of a near-term Fed cut, with a next cut fully priced for October.

- US rates outperform European counterparts (e.g. SFRZ6 +2.5 ticks vs ERZ6 -2 ticks) in signs of some haven demand for US assets with Trump promising “bigger” and “better” than an Israel-Iran ceasefire on Truth Social and speaking to reporters on Air Force One.

- Cumulative cuts from 4.33% effective: 0bp for tomorrow, 3.5bp for Jul, 19bp Sep, 32bp Oct and 48.5bp Dec.

- The SOFR implied terminal yield of 3.295% (SFRZ6, -2.5bp) last closer lower on Thursday (Jun 12).

- Today sees data including retail sales and import prices for May (0830ET) before industrial production for May (0915ET). They provide important hard data updates for May heading into the two-day FOMC meeting starting today.

- MNI Fed Preview: https://media.marketnews.com/Fed_Prev_Jun2025_With_Analysts_a9c8a317ff.pdf

UK DATA: MNI UK CPI Preview: May 2025

- Ahead of the publication of the MPC policy decision on Thursday, May CPI data will be published tomorrow morning at 7:00BST (although the MPC will already have advance access to the data as of yesterday morning).

- The ONS' VED (road tax) component error in the April dataset which boosted headline CPI by around 0.13ppt (on our calculations core by 0.16ppt and services CPI by 0.25ppt) will be reversed in the May data.

- Headline CPI was also boosted in April by Easter effects: air fares contributed 0.11ppt to the increase, package holidays 0.07ppt and sea transport 0.04ppt. These combined are therefore over 0.2ppt and along with the VED a fully reversal would see headline CPI drop by almost 0.4ppt and services CPI by almost 0.8ppt.

- The MNI median looks for a smaller fall to 3.3%Y/Y for headline (from 3.53%, 3.40% adjusted for VED) and for services to 4.8%Y/Y (from 5.42%, 5.17% adjusted). The BOE forecasts are 3.36% and 4.73% respectively. We see risks skewed more to the downside for services.

- However, there are upside risks to core goods (albeit resulting in a smaller downside surprise to the BOE) and food prices.

US TSY FUTURES: Limited Positioning Swings On Monday Owing To Geopolitics

OI data points to fairly non-committal trade for a second consecutive session, with net OI and DV01 equivalent swings fairly limited as geopolitical risk centred on the Middle East remained heightened on Monday.

- There was a mix of net short setting (FV, TY, UXY & WN) and long cover (TU & US) as contracts settled lower.

- The apparent net short setting in TY futures provided the only 7 figure DV01 equivalent net positioning move on the curve.

| 16-Jun-25 | 13-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,979,676 | 3,983,489 | -3,813 | -149,319 |

FV | 6,897,741 | 6,880,210 | +17,531 | +763,300 |

TY | 4,830,693 | 4,809,088 | +21,605 | +1,430,258 |

UXY | 2,347,111 | 2,346,995 | +116 | +10,112 |

US | 1,733,338 | 1,735,439 | -2,101 | -288,557 |

WN | 1,893,897 | 1,893,809 | +88 | +15,663 |

|

| Total | +33,426 | +1,781,456 |

EUROPE ISSUANCE UPDATE:

EU syndication: Priced

- E5bln WNG tap (the bottom of the E5-9bln range MNI expected) of the 3.375% Oct-39 EU-bond. Reoffer 99.209 to yield 3.445%. Spread set at MS+73bps (guidance was MS+75bps area), final books above E93bln.

German auction results

- E1bln (E989mln allotted) of the 2.10% Apr-29 Green Bobl. Avg yield 2.02% (bid-to-offer 3.18x; bid-to-cover 3.22x).

- E500mln (E495mln allotted) of the 2.30% Feb-33 Green Bund. Avg yield 2.37% (bid-to-offer 3.49x; bid-to-cover 3.53x).

US: Trump-'Not In Mood To Negotiate' w/Iran, Wants 'Complete Give-Up' On Nukes

Speaking to reporters aboard Air Force One, President Donald Trump says on the situation in the Middle East, says he is looking for "better than a ceasefire" in Iran. Says he is "not too much in the mood to negotiate" with Iran on its nuclear programme and wants a "complete give-up" on its enrichment efforts.

- On trade and tariffs, Trump says that the EU is "not yet offering a fair deal on trade". Says that pharmaceutical tariffs are coming "very soon".

- Says he may offer Canada a separate deal to become part of Trump's touted 'golden dome' project. Adds that Canada will have to pay to participate.

POLITICAL RISK: Trump Wants 'Real End' To Iran's Nuclear Programme

Jennifer Jacobs at CBS puts two lengthy posts on X after US President Donald Trump left the G7 early. Some of the main points noted below:

- Trump says he needs to be in the White House Situation Room where he can be "well versed" on the state of play in the Middle East. Calls for a "real end" to Iran's nuclear programme with Iran "giving up entirely" on nuclear weapons.

- Says Israel is not slowing its barrage on Iran. Says he may end VP JD Vance or Middle East envoy Steve Witkoff to talk to Iran.

- Says US would "come down so hard if they do anything to our people," re: threats to US bases in Middle East.

- Says he hope Iran's nuclear programme "is wiped out long before [US involvement]."

- Confirms that Treasury Secretary Scott Bessent 'and a couple of others' have stayed behind to meet with G7 leaders.

- Says he has not seen the G7 statement, but has "authoized them go say certain things." Earlier, Trump reversed course and signed a G7 resolution calling for “a broader de-escalation of hostilities in the Middle East, including a ceasefire in Gaza", after initially refusing to back the wording.

At present, neither Israel nor Iran have actively shown any sign of ramping down their missile attacks on one another. A flurry of whipsawing headlines on 16 June, at one moment suggesting de-escalation and then minutes later further escalation, has not changed the calculus at present. Attacks continue apace and Israel maintains its need to eliminate Iran's nuclear programme.

FOREX: JPY Looks Through Slowing of Cuts to Bond Buys, GBP Sold on Rallies

- The Bank of Japan rate decision came in broadly as expected, and while signals were given over a slower pace of cuts to their bond-buying program, this meant little to the JPY currency, which remains inside the recent range. Spot remains below last week’s high. Recent weakness suggests the correction between Jun 3 - 11, is over. The trend direction is down - moving average studies are in a clear bear-mode position, highlighting a dominant downtrend.

- GBP trades poorly, and is fading against all others in G10. As a result, GBP/USD has again struggled to hold gains above 1.36 and is on the backfoot. As such, the sell-on-rallies theme remains dominant. The outlook will deteriorate on any break and close below 1.3456, which would signal the first phase of a corrective pullback. 1.3371, the 50-dma, and 1.3270 are the first downside targets here. UK CPI prints early Wednesday ahead of the BoE rate decision on Thursday.

- In the crosses, NZDJPY is threatening to break above 87.95, which would be the highest close since January, placing the focus on the year’s highs at 89.71. For AUDNZD, spot has been consolidating in a 1.0750/1.0800 range, however MA studies do highlight bearish momentum. A sustained break above 1.0825 would be required to alter this trend.

- The US retail sales print for May is next up, with markets on watch for a slowdown in the advance retail sales headline to -0.6% from +0.1% prior. Import and export price indices will be released alongside. ECB's Villeroy and Centeno are set to speak, while the Fed remain inside their pre-rate decision media blackout period.

OPTIONS: Expiries for Jun17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1625(E1.3bln)

COMMODITIES: Bullish Theme in Gold Remains Intact, Recent Gains Bolster Trend

- WTI futures traded sharply higher last week and Friday’s early rally marked an acceleration of the current bull phase. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is currently in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted $68.49, the Jun 13 low. A breach of this level would signal scope for a deeper retracement.

- A bullish theme in Gold remains intact and last week’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3267.0, the 50-day EMA.

EQUITIES: Eurostoxx 50 Futures Breach 50-Day EMA Following Latest Pullback

- The latest pullback in the Eurostoxx 50 futures contract has resulted in a breach of the 50-day EMA at 5299.04. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would signal a short-term top and highlight scope for a deeper retracement. This would open 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5363.03, the 20-day EMA.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 6000.18, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5890.99. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

| Date | GMT/Local | Impact | Country | Event |

| 17/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 17/06/2025 | 1730/1330 | Bank of Canada Summary of Deliberations | ||

| 18/06/2025 | 2350/0850 | * | Machinery orders | |

| 18/06/2025 | 0600/0700 | *** | Consumer inflation report | |

| 18/06/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 18/06/2025 | 0730/0930 | ECB Elderson At SRB Legal Conference 2025 | ||

| 18/06/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/06/2025 | 0900/1100 | *** | HICP (f) | |

| 18/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 18/06/2025 | 1500/1700 | ECB Lane At Macroprudential Conference | ||

| 18/06/2025 | 1515/1115 | BOC Governor speaks in Newfoundland. | ||

| 18/06/2025 | 1600/1200 | ** | Natural Gas Stocks | |

| 18/06/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/06/2025 | 1800/2000 | ECB de Guindos at Osservatorio Permanente Giovani-Editori | ||

| 18/06/2025 | 2000/1600 | ** | TICS | |

| 19/06/2025 | 2245/1045 | *** | GDP |