MNI US MARKETS ANALYSIS - Trump, Cook Trade Barbs

Highlights:

- Treasury curve sits twist steeper as Trump, Cook trade barbs

- EUR/USD erases Jackson Hole rally, French political concerns weigh

- Prelim durable goods, open White House cabinet meeting and August consumer confidence the calendar highlights

US TSYS: Twist Steeper On Latest Fed Independence Concerns

- Treasuries sit twist steeper following the latest escalation in President Trump’s push against Fed independence, claiming to have fired Fed Governor Cook who has since said he doesn’t have the authority to do so.

- Ahead, data is headlined by durable goods and the Conf. Board consumer survey with its labor differential. Focus will then be on Trump’s remarks at 1100ET before the 2Y auction for an interesting test of front-end demand amidst Fed independence concerns.

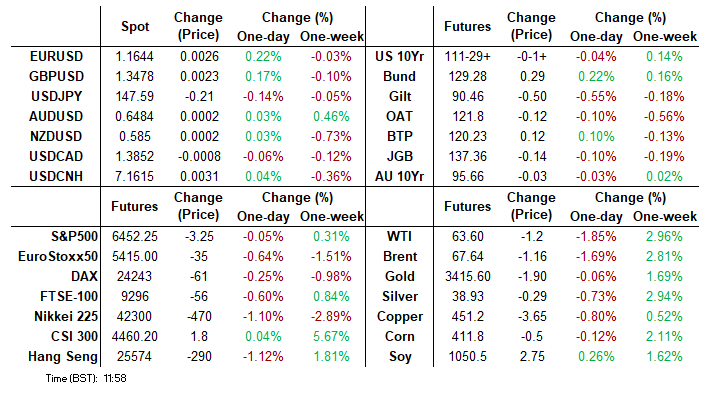

- Cash yields are 1.9bp lower (2s) to 3.9bp higher (30s).

- 5s30s sits at 114.9bp (+4.3bps) off an overnight high of 116bps, a fresh multi-year high.

- TYU5 trades at 111-29 (-02) on elevated cumulative volumes of 575k of which a little more than half is quarterly roll related. We estimate more than half the roll has been completed, with higher roll rates in other contracts.

- TYU5 continues to slowly pare Friday’s Powell-driven gains, which saw a high of 112-08 stop short of resistance at 112-15+ (Aug 5 high, bull trigger). Support is seen at 111-13 (50-da EMA).

- Data: Durable goods orders Jul prelim (0830ET), Philly Fed non-mfg Aug (0830ET), FHFA/S&P house prices Jun (0900ET), Conference Board consumer survey Aug (1000ET), Richmond Fed mfg Aug, Dallas Fed services Aug (1030ET)

- Fedspeak: Barkin repeats speech (0830ET)

- Coupon issuance: US Tsy $69B 2Y Note auction - 91882CNV9 (1300ET). Last month’s 2Y auction stopped through by 0.5bp and the bid-to-cover increased from 2.58 to 2.62 but indirect take-up retreated.

- Bill issuance: US Tsy $85B 6W bill auction (1130ET)

- Politics: Trump participates in cabinet meeting with White House press pool (1100ET)

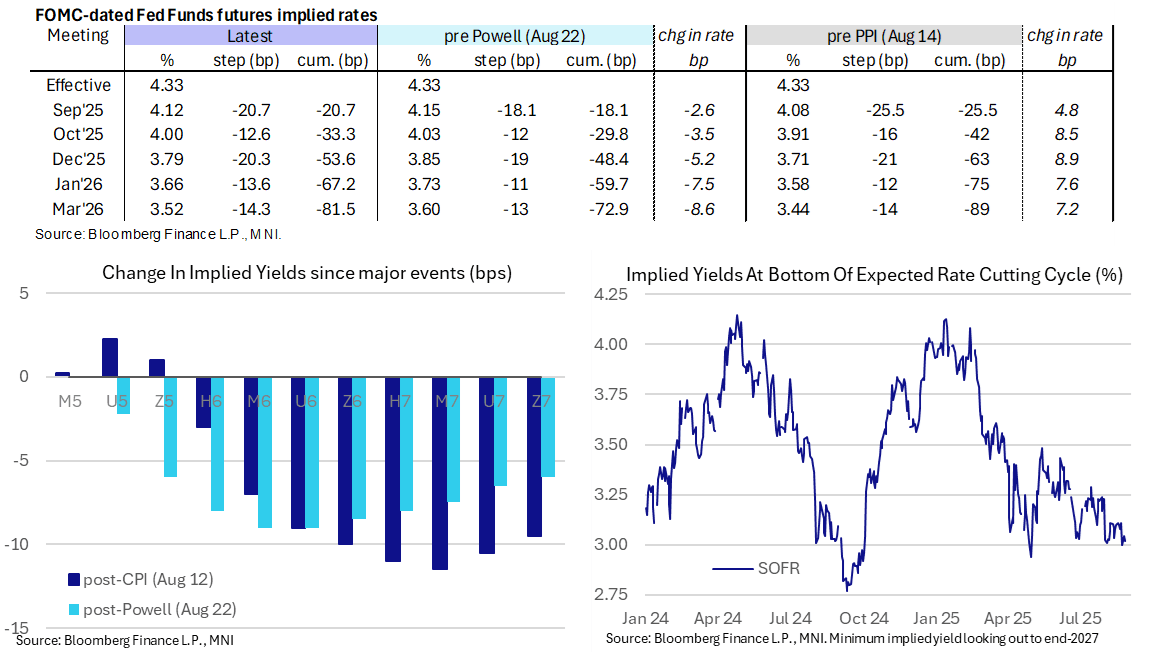

STIR: Holding Dovish Tilt Seen After Latest Trump-Cook Headlines

- Fed Funds implied rates have been held lower overnight by Trump saying he had removed Fed Governor Cook with immediate effect late yesterday.

- The dovish shift has been pared somewhat with help from Cook again since pushing back, saying he has no authority to fire her and she won’t quit.

- Cumulative cuts from 4.33% effective: 20.5bp Sep, 33.5bp Oct, 53.5bp Dec, 67bp Jan and 81.5bp Mar.

- SOFR implied yields are up to 3bp lower on the day (SFRM6) whilst the terminal yield is 2.5bp lower at 3.02% (SFRH7). The latter unwinds half of yesterday’s 4.5bp increase as it remains close to recent dovish extremes, having closed at 3.00% after Powell on Friday.

- Dallas Fed’s Logan (’26 voter, hawk) yesterday said she anticipates use of the Fed’s rate ceiling tools in September amidst room to reduce reserves. She added that the Fed should explore ways to avoid overemphasizing the median view on the FOMC in projections.

- NY Fed’s Williams (permanent voter) late yesterday reiterated that the era of low neutral rates “appears far from over” echoing NY Fed research that he had co-authored published earlier in the day.

- Ahead, Richmond Fed’s Barkin (non-voter) repeats a speech from Aug 12 on the economy at 0830ET. It will be followed by audience questions but there won’t be a livestream.

BONDS: OAT-Bund Spread Off Fresh Highs But Bayrou Vote Still Weighs

The tone in EGBs continues to be set by French PM Bayrou yesterday effectively calling a confidence vote in his own government with an extraordinary session convened on Sep 8. Bunds see outperformance in relative haven flow whilst Gilts play catch-up after yesterday’s bank holiday closures.

- French paper underperforms across the curve, with yields 2.4bps (5s) lower to 1bp higher (30s).

- The French 10yr Yield (currently 3.504%, -0.3bps) has fully cleared the 3.50% level with a high of 3.531%, highest since March.

- OATA trades at 121.82 (-0.10) off earlier lows of 121.54. Next stop: 3.550% = 121.39 and 3.631% = 120.61 (highest Yield print since Nov 2011).

- The 10Y OAT-Bund spread is off earlier highs of 79.4bps (fresh highs since April) but still 1.7bp wider on the day at 76.9bp. It was under 71bp prior to yesterday’s headlines.

- Related, S&P Global report that 5Y CDS spreads have increased to a three-month high of 37bps.

- RXA trades at 129.28 (+0.29) within session ranges of 129.15 and 129.49, on strong cumulative volumes over 400k. It briefly cleared resistance at 129.46 (20-day EMA), with a stronger clearance opening 129.80 (50-day EMA). Support is seen at 128.64 (Aug 15 low).

- Gilts see underperformance on the day in catch-up from bank holiday closures.

- There was a big move on the open, some of the calls were 90.90/91.00, it was netting at 90.87, but it’s dropped more than 50 ticks at 90.39. The Dec is still not front month but expected to be today. Immediate support in G Z5 is at 90.31, but the big Yield levels are still at: 4.800% = 89.98 before 4.921% = 88.93.)

EUROPE ISSUANCE UPDATE:

Austria syndication: Final terms

- E3bln WNG (excl. E250mln issuer retention) of the new 7-year Sep-32 RAGB. Spread set earlier at MS+30 (guidance was MS+33 area), books closed in excess of E19bn.

Italy auction results

- E3bln of the 2.10% Aug-27 BTP Short Term. Avg yield 2.2% (bid-to-cover 1.56x).

FRANCE: Justice Min Raises Prospect Of Early Election If Bayrou Gov't Falls

France looks set for another period of significant political instability after PM Francois Bayrou effectively called a confidence vote in his own gov't on 25 Aug. Bayrou said that he had requested an extraordinary session of the National Assembly to be convened on Monday, 8 September to "confirm the scale" of spending cuts in the upcoming 2026 state budget, adding that "If you have a majority, the government is confirmed. If you do not have a majority, the government falls".

- The Bayrou gov't has been living on borrowed time for a while now. Formed by the centrist Ensemble bloc and the centre-right Les Republicains (LR), the gov't holds only 210 seats in the 577-member legislature. With the leftist New Popular Front alliance and the far-right Rassemblement National both set to vote against Bayrou, the gov'ts dismissal appears more likely than not.

- With more than a year having passed since that vote, President Emmanuel Macron is at liberty to call another set of legislative elections. Speaking to France 2 TV earlier, Justice Minister Gerald Darmanin said, "Dissolution [of the Assembly] is costly for France, of course, but this hypothesis should not be ruled out."

- Jean-Luc Melenchon, leader of the far-left La France Insoumise (LFI), confirmed in an interview with France Inter that his group will move forward with a motion of impeachment against Macron on 23 September. Melenchon claimed Macron must be removed from office as he is the "cause" of the current political paralysis.

- The collapse of the Bayrou gov't could come at the same time as a major effort by the left to pressure the Macron administration, with the 'bloquons tout' ('black everything') efforts to call a general strike, as well as road blockades and corporate boycotts.

IRAN: Little Expectation Of Progress In E3 Geneva Talks

Representatives from Iran hold talks with counterparts from the E3 countries (France, Germany, the UK) today (26 Aug) in Geneva, Switzerland, in what are viewed as the last chance for Tehran to avoid the imposition of 'snapback' sanctions from mid-October. The chances of sufficient progress being made to avoid the sanctions are viewed as very slim.

- Reuters reports one E3 official stating, "We are going to see whether the Iranians are credible about an extension or whether they are messing us around. We want to see whether they have made any progress on the conditions we set to extend". The E3 are demanding the resumption of International Atomic Energy Agency (IAEA) inspections of Iran's nuclear stockpiles (halted in the aftermath of the 12 Day War), and Tehran re-engaging in diplomatic relations with countries including the US.

- On 25 Aug, Amwaj Media reported that Russia has put forward a draft resolution that intends to extend UN Security Council Resolution 2231 (the expiry of which brings in snapback sanctions) for another six months. The E3 has set its deadline of 31 August for the conditions to be met. As the article notes, "By triggering the mechanism this month, the E3 is believed to seek to avoid any Russian subterfuge as Moscow will assume the presidency of the UN Security Council in September. "

- Tehran is believed to be reluctant to allow inspectors to visit its nuclear sites in order to avoid "indirectly providing the Trump administration with battle damage assessment and information on its uranium stockpile".

FOREX: USD Recovers Following Trump-Cook Inspired Dip

- Volatility in currency markets Tuesday was stoked by President Trump declaring he was firing Federal Reserve governor Lisa Cook “effective immediately”, in an escalation of the US president’s attacks on the central bank. The immediate impact was dollar negative, with USDJPY bearing the brunt of the move, depreciating around 90 pips in the aftermath.

- This allowed USDJPY to trade down to 147.00, reversing much of Monday’s ascent. However, weakness was short-lived as the dollar began to reverse on potential safe haven demand, while Governor Cook stating that she will not resign and will continue to carry out her duties may have also exacerbated the dollar’s full intra-day reversal.

- FX futures volumes are healthy - likely a result of the catch-up after the UK bank holiday on Monday: GBP, JPY futures see volumes of 40%-80% above average, but EUR futures are the standout: heavy trade through Asia-Pac saw total activity over double what might be expected in at this stage of the trading day.

- Overall, the dollar index’s resilience to start the week has seen the majority of Powell's dovish JH inspired selloff reverse. Activity is also backed up by WSJ's overnight report that China have sent a "senior" trade negotiator to the US - a likely signal that a trade deal can be reached that could unlock a Trump-Xi Jinping summit in the near future.

- While the EURUSD’s fall this week is reflective of broader greenback themes, political uncertainty has also ratcheted up following French Prime Minister Francois Bayrou’s plan to call a confidence vote. The trend set-up in EURUSD remains bullish and short-term weakness is for now considered corrective. Support at the 50-day EMA remains intact, at 1.1597. A clear break of it would signal scope for a deeper retracement and potentially expose key support at 1.1392, the Aug 1 low.

- US durable goods, consumer confidence and Richmond manufacturing data are all due later in the session. ECB’s Villeroy, BOE’s Mann and BOC Governor Macklem are all due to speak.

FOREX: Deutsche Bank See Month-End Model Signals Too Weak to Trade

Deutsche Bank write that the relatively quiet period for FX over summer has meant that relative equity performance gaps have been narrow.

- The largest USD based differential is Japan's Nikkei vs. The S&P 500, but at 4% the gap is small by historical standards. Nevertheless, it points to USDJPY buying on month end.

- USDNOK has the largest seasonal signal for August, with selling evident on T-2 (Weds) and buying on T-1 and T+1 (Thurs/Mon). This could work well if Nvidia earnings are weak tomorrow.

- They caution that given the strength of the signals are small this month, they are not looking to actively trade them.

EQUITIES: Trend Set-Up in EStoxx Remains Bullish

- The dominant uptrend in S&P E-Minis remains intact and last Friday’s rally reinforces current conditions. Moving average studies are in a bull-mode position, highlighting a clear uptrend and positive market sentiment.

- The trend set-up in Eurostoxx 50 futures is bullish and the pullback from last Friday’s high is for now, considered corrective. The recent print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00.

COMMODITIES: S/T WTI Gains Appear Corrective For Now

- The medium-term trend condition in Gold remains bullish - moving average studies remain in a bull-mode position highlighting a dominant uptrend. The sideways direction that has been in place since the Apr peak appears to be a pause in the uptrend.

- A bear cycle in WTI futures remains intact and the latest round of short-term gains appear corrective - for now. A key support at $61.99, the Jun 30 low, has recently been breached, strengthening a bearish theme.

| Date | GMT/Local | Impact | Country | Event |

| 26/08/2025 | - | DMO to hold FQ3 consultations with investors / GEMMs | ||

| 26/08/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/08/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 26/08/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 26/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 26/08/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 26/08/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 26/08/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 26/08/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 26/08/2025 | 1400/1500 | BOE Mann at Banxico Conference (text release) | ||

| 26/08/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 26/08/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 26/08/2025 | 1830/1430 | BOC Governor speech in Mexico City | ||

| 27/08/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 27/08/2025 | 0130/1130 | *** | Quarterly construction work done | |

| 27/08/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 27/08/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 27/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 27/08/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 27/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 27/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 27/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 27/08/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 27/08/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note |