MNI US MARKETS ANALYSIS - Treasuries Under Early Pressure

Highlights:

- Treasuries under pressure at beginning of Fedweek, this week's cut close to fully priced

- NY Fed inflation expectations data watched carefully for any repeat of last week's UMichigan softness

- USDCAD looks bearish headed into BoC decision

US TSYS: Futures Revisit Mid-December Lows Ahead Wednesday's FOMC

- Treasuries are under moderate pressure at the moment, reversing early overnight gains on average volumes. Today's data limited to NY Fed Survey of Consumer Expectations at 1100ET. Pres Trump participates in a roundtable meeting at 1400ET.

- The main focus is on Wednesday's FOMC decision, widely expected to deliver a third consecutive 25bp cut after NY Fed Williams’ uncharacteristic guidance following the delayed September payrolls report. Potentially contentious meeting with many FOMC members preferring to have paused.

- The dot plot distribution will be watched keenly whilst we expect the economic projections to show an upward revision for GDP growth and downward revision for core PCE inflation.

- The FOMC will see two months of JOLTS data on the first day of their two-day meeting otherwise must wait until the following week for NFP (Dec 16) and CPI (Dec 18) reports for November.

- Treasury Mar'26 10Y futures are revisiting November 20 levels: currently trading -3.5 at 112-13 vs. -12 low, 10Y yield +.0195 to 4.1545%. Bearish conditions resume with sights on 112-07, the Nov 5 high and a bear trigger. A reversal higher is required to once again refocus attention on the key resistance and bull trigger at 113-29+, the Oct 17 high.

SOFR: Mix Of Net Short Setting & Long Cover In Futures On Friday

OI data points to net short setting dominating in the white, green and blue SOFR packs on Friday, while net long cover was more prominent in the reds as most SOFR futures ticked lower on the day.

| 05-Dec-25 | 04-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,302,569 | 1,303,410 | -841 | Whites | +55,934 |

SFRZ5 | 1,603,394 | 1,590,932 | +12,462 | Reds | -4,299 |

SFRH6 | 1,430,509 | 1,388,938 | +41,571 | Greens | +26,517 |

SFRM6 | 1,148,072 | 1,145,330 | +2,742 | Blues | +9,500 |

SFRU6 | 1,081,547 | 1,080,245 | +1,302 |

|

|

SFRZ6 | 1,104,360 | 1,120,049 | -15,689 |

|

|

SFRH7 | 855,810 | 836,729 | +19,081 |

|

|

SFRM7 | 770,549 | 779,542 | -8,993 |

|

|

SFRU7 | 834,190 | 818,379 | +15,811 |

|

|

SFRZ7 | 850,283 | 845,239 | +5,044 |

|

|

SFRH8 | 446,954 | 441,690 | +5,264 |

|

|

SFRM8 | 404,177 | 403,779 | +398 |

|

|

SFRU8 | 380,155 | 381,784 | -1,629 |

|

|

SFRZ8 | 319,892 | 321,438 | -1,546 |

|

|

SFRH9 | 201,582 | 195,315 | +6,267 |

|

|

SFRM9 | 217,512 | 211,104 | +6,408 |

|

|

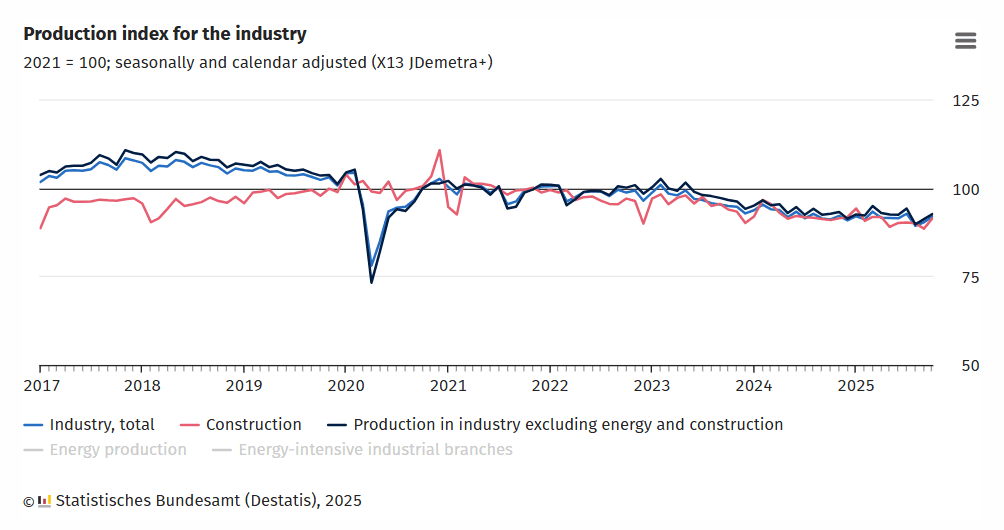

GERMAN DATA: IP Starts Off Q4 On Comparably Strong Note

- German industrial production was stronger than expected in October, even considering the downward September revision.

- "The less volatile three-month on three-month comparison showed that production was 1.5% lower in the period from August 2025 to October 2025 than in the previous three months [...] In October 2025, production in industry excluding energy and construction was up 1.5% [M/M] from September 2025 after seasonal and calendar adjustment."Destatis comments.

- On drivers within manufacturing (excl. energy and constr): "increases registered in the manufacture of machinery and equipment (+2.8%) and in the manufacture of computer, electronic and optical products (+3.9%) also made a significant contribution to the overall result. By contrast, the decline in production in the automotive industry (-1.3%), which is an important sector, had a negative impact"

- An increase in construction (+3.3% M/M) follows strong increases in dwelling approvals over the last couple of months in Germany which may be starting to filter through.

- Sentiment in German industry has faded most recently, with both the Manufacturing PMI and IFO index slightly lower in their December readings than in November. The IFO saw some reduction the difference between its expectations and current conditions subreadings - the spread between these remains notable, though.

BOE: 6 MPC members to make public appearances this week

We have scheduled appearances from six of the nine MPC members in the first half of the week.

- Wed 10:45: Governor Bailey will take part in a pre-recorded fireside chat with Chris Giles at the FT Global Boardroom event that will be shown around 10:45. This is likely to be the main event of the week, given that Bailey is the swing voter. We are not sure how forthright he will be with his views in this event, so he may not give much more colour than we already have. But the market will be closely watching whether he continues to reference data ahead of the December meeting, or if he is more vague. Bailey will also be giving evidence ahead of the Covid-19 inquiry on Thursday (starting at 10:00 and he's scheduled for both the morning and afternoon sessions - but don't expect anything market moving from this appearance).

- Today (17:00): Professor Taylor will give a speech on "What’s next for growth, wealth, and debt" at the McKinsey Global Institute. Given that he is a clear dove, it is unlikely his comments will be market moving.

- Today (18:30): Lombardelli will speak at the LSE's conference on "Women in economics: progress, challenges and perspectives." We don't expect her to make market-relevant comments at this event, but cannot rule it out.

- Tomorrow 14:15: Lombardelli, Ramsden, Dhingra and Mann will testify ahead of the Treasury Select Committee with respect to the November MPR. Annual reports from Mann and Ramsden will also be published. Ramsden and Dhingra cemented their views on the dovish side in November while Mann is a known hawk. Lombardelli's comments in the November Minutes seemed a bit more entrenched into the hawkish camp than had been expected by some too - so we will be watching her comments in particular. We think it would take a huge surprise for any of these members to change their view for the December MPC meeting.

RBA: MNI RBA Preview-Dec 2025: On Hold, Could Be A Hawkish Shift?

- Download Full Report Here

- With October trimmed mean inflation printing at 3.3%, the RBA is unanimously expected to be on hold at its December meeting.

- The strength of the data since the November meeting plus inflation rising further above the top of the band increases the chance that the RBA now sees risks skewed to the upside and as a result it may sound more hawkish and at a minimum will remain “cautious”.

- RBA-dated OIS pricing is showing the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- With core inflation rising over H2 2025 and stronger demand increasing upside risks, future rate decisions will be even more data dependent to give clarity to the outlook. November CPI is released 7 January & Q4/December 28 January ahead of the next RBA meeting on 4 February. At this stage policy is likely to be unchanged then too.

FOREX: AUD and CAD Consolidating Gains Ahead of Central Bank Decisions

- G10 currency markets are trading with moderate adjustments Monday, as markets digest increasing China/Japan tensions over the weekend and await a busy calendar of central bank decisions ahead. Despite US yields continuing to edge higher, the USD index holds close to unchanged, hovering within 20 pips of the recent pullback lows.

- EURUSD was given a brief boost in early trade, matching its 1.1672 Friday high after ECB Executive Board member Schnabel noted that she is “rather comfortable” with markets pricing the next move from the ECB as a hike. The recent break above 1.1656 in EURUSD highlighted a potential reversal, although topside momentum has failed to immediately gain traction.

- JPY meanwhile is a modest underperformer after Chinese military aircraft breached Japanese airspace and Q3 Japanese GDP was downwardly revised. Moves have been contained, with USDJPY broadly remaining in a 155.00/50 range as verbal jawboning from Finmin Katayama somewhat offsets the yen pessimism.

- AUDUSD traded up to 0.6649 overnight and the subsequent dip as remained very shallow. This follows 10 consecutive sessions of higher highs as we approach tomorrow’s RBA decision. With a hold tomorrow widely expected, the tone of the statement and press conference will be scrutinised given the recent increase of hike pricing in 2026.

- Elsewhere, NZDUSD has been edging closer to the medium-term pivot at the 0.5800 mark, while USDCAD is holding the entirety of its post-data plunge from Friday. Technical developments have significantly bolstered the bearish USDCAD theme, following a breach of the bull channel and clean break of 1.3888.

- NY Fed inflation expectations is the main datapoint for today, while ECB's Cipollone and Villeroy as well as BoE's Taylor and Lombardelli are scheduled to speak.

OPTIONS: Expiries for Dec08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E831mln), $1.1670(E587mln), $1.1800(E1.8bln), $1.2140(E2.9bln)

- USD/JPY: Y155.00($1.2bln), Y156.00($1.5bln)

- AUD/USD: $0.6475-80(A$1.0bln)

- USD/CAD: C$1.3940($841mln)

EQUITIES: Bull Cycle in Eurostoxx 50 Futures Remains Intact

- A bull cycle in Eurostoxx 50 futures remains intact. Price has recently cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next (pierced), the 76.4% retracement of the Nov 13 - 21 bear leg. Clearance of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support lies at 5621.75, the 50-day EMA.

- A bullish theme in S&P E-Minis is intact. Price remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6797.09, the 20-day EMA.

COMMODITIES: WTI Future Moving Average Studies in a Bear-Mode Position

- Short-term gains in WTI futures appear corrective - for now. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend needle in Gold continues to point north. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4031.1. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 08/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/12/2025 | 1500/1600 | ECB Cipollone Lecture at Frankfurt School of Finance & Management | ||

| 08/12/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 08/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 08/12/2025 | 1700/1700 | BOE Taylor Panel on Growth/Wealth/Debt | ||

| 08/12/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/12/2025 | 1830/1830 | BOE Lombardelli Panel on Women in Economics | ||

| 09/12/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 09/12/2025 | 0330/1430 | *** | RBA Rate Decision | |

| 09/12/2025 | 0700/0800 | ** | Trade Balance | |

| 09/12/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 09/12/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 09/12/2025 | - | FOMC Meetings with S.E.P. | ||

| 09/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 09/12/2025 | 1415/1415 | BOE Lombardelli, Ramsden, Dhingra, Mann at TSC | ||

| 09/12/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 09/12/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 09/12/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 09/12/2025 | 1800/1300 | ** | US Note 10 Year Treasury Auction Result |