MNI US MARKETS ANALYSIS - Tariff Talk Reaches Fever Pitch

Highlights:

- Tariff talk reaches fever pitch as deadline looms

- Equities, AUD, NZD sold, while core bonds and JPY are in demand

- MNI Chicago PMI expected to confirm soft economic activity

US TSYS: Risk-Off Start To Quarter-End

- Treasuries have been confined to relatively tight ranges since opening markedly higher in Japan trading, reflecting broad risk-off flows on a combination of tariff concerns ahead of April 2 "Liberation Day" and geopolitical fears

- Goldman Sachs for example have marked up their 12-month US recession probability from 20% to 35% on the assumption of a 15pp increase in the average US tariff rate vs 10pp previously.

- Cash yields are 4.5-6bp lower on the day, with declines led by the front end.

- 2Y yields have stabilized around 3.85% (touched Mar 11 but last sustainably lower in Oct 2024) whilst 10Y yields have stabilized around 4.20% (hit a few times throughout March).

- 2s10s at 35bp (+1bp) remains off last week’s recent high of above 38bps.

- TYM5 trades at 111-18 (+11+) off an earlier high of 111-22+, on strong overnight volumes of 545k. Resistance at the March 20 high (111-17+) has been pierced, with bulls now looking to force a break above the March 11 high (111-25) as they aim to build further on last week's gains. Attention is on key resistance at 112-01 (Mar 4 high).

- Data: MNI Chicago PMI Mar (0945ET), Dallas Fed mfg Mar (1030ET)

- Bill issuance: US Tsy $76B 13W & $68B 26W Bill auctions (1130ET)

STIR: A Notable Build In Fed Rate Cut Expectations Overnight

- Fed Funds implied rates hold their dovish adjustment seen at the open on a combination of tariff concerns ahead of April 2 "Liberation Day" and geopolitical fears.

- Cumulative cuts from 4.33% effective: 5.5bp May (unch), 24bp Jun (+2bp from Fri), 41bp Jul (+4.5bp) and 80.5bp Dec (+7bp).

- It sees a notable extension of Friday’s rates rally which saw added impetus from another markdown in Atlanta Fed’s GDPNow with its gold-adjusted estimate at -0.5% for Q1. See a review of last week’s many pertinent macro developments here.

- Today sees further manufacturing surveys watched for signs of stagflation, with the MNI Chicago PMI at 0945ET and Dallas Fed survey at 1030ET. There’s no scheduled Fedspeak today.

US TSY FUTURES: Net Long Setting Most Prominent On Friday

OI data suggests that net long setting in FV and UXY futures comfortably outweighed net short cover in TU, TY, US & WN futures during Friday’s rally.

| 28-Mar-25 | 27-Mar-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,909,210 | 3,939,976 | -30,766 | -1,187,061 |

FV | 6,542,114 | 6,436,119 | +105,995 | +4,635,242 |

TY | 4,946,319 | 4,952,115 | -5,796 | -374,682 |

UXY | 2,304,818 | 2,288,507 | +16,311 | +1,463,918 |

US | 1,802,689 | 1,804,438 | -1,749 | -230,609 |

WN | 1,789,756 | 1,792,826 | -3,070 | -594,090 |

|

| Total | +80,925 | +3,712,717 |

STIR: Long Setting Most Prominent In SOFR Futures On Friday

OI data suggests that net long setting outweighed instances of net short cover during Friday’s SOFR futures rally, with the most concentrated round of net long setting coming in SFRM5 through SFRZ5.

| 28-Mar-25 | 27-Mar-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,176,188 | 1,178,337 | -2,149 | Whites | +41,621 |

SFRM5 | 1,299,968 | 1,289,384 | +10,584 | Reds | -13,396 |

SFRU5 | 988,385 | 960,566 | +27,819 | Greens | -6,934 |

SFRZ5 | 1,100,196 | 1,094,829 | +5,367 | Blues | +7,584 |

SFRH6 | 642,893 | 647,619 | -4,726 |

|

|

SFRM6 | 679,714 | 670,682 | +9,032 |

|

|

SFRU6 | 637,794 | 643,266 | -5,472 |

|

|

SFRZ6 | 802,284 | 814,514 | -12,230 |

|

|

SFRH7 | 507,456 | 502,827 | +4,629 |

|

|

SFRM7 | 488,205 | 500,603 | -12,398 |

|

|

SFRU7 | 318,777 | 324,489 | -5,712 |

|

|

SFRZ7 | 433,368 | 426,821 | +6,547 |

|

|

SFRH8 | 232,386 | 225,144 | +7,242 |

|

|

SFRM8 | 190,300 | 190,340 | -40 |

|

|

SFRU8 | 130,602 | 129,956 | +646 |

|

|

SFRZ8 | 135,441 | 135,705 | -264 |

|

|

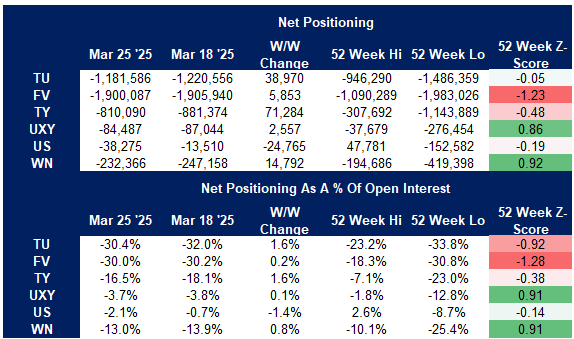

US TSY FUTURES: CFTC CoT Sees Funds Trim Short, Asset Managers Add To Long

The latest CFTC CoT revealed a covering of some of the existing net short position held across leveraged funds, with net short cover in TU, TY & WN futures outweighing net short setting in FV, UXY & US futures (in DV01 equivalent terms). The cohort remains net short across all contracts.

- Elsewhere, asset managers added modestly to their overall net long position, with long setting in FV, TY, UXY and US futures outweighing long cover in TU & WN futures. The cohort remains net long across all contracts.

- Non-commercial accounts trimmed their overall net shorts in all contracts outside of US futures. The cohort remains net short across all contracts (further details of that cohort’s positioning available in the image below).

Source: MNI - Market News/CFTC/'Bloomberg

EUROPEAN INFLATION: EZ HICP Tracking Points to 2.1-2.2%Y/Y Ahead of Germany

- MNI's tracking estimate for EZ HICP is currently between 2.1-2.2%Y/Y with around 55% of country-level data having been released.

- German data (which accounts for 27.6% of the EZ HICP) is due for release at 13:00BST / 14:00CET / 8:00ET. We have assumed that comes in line with consensus at 2.4%Y/Y. Our tracking estimate for the national non-HICP measure is coming in at 2.2% with marginal upside risks - which is also in line with consensus expectations.

- We assume that Dutch HICP (5.9% of EZ weighting) also comes in inline with consensus and that there is no big change to the Y/Y rates of Austria (3.4% of EZ weighting) versus February's print.

- The Bloomberg median is at 2.2% - but there are more analysts forecasting 2.3%Y/Y than 2.1%, so there may be some very modest downside risks.

- We will update our tracking estimate later today following the German HICP print.

EUROPEAN INFLATION: MNI Projects 2.2% Y/Y German National CPI, Core 2.6%

From state-level index data that equates to 89.1% weighting of the national February flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates that national CPI (non-HICP print) rose by 0.3-0.4% M/M (Feb 0.4%) and rose 2.2-2.3% Y/Y (Feb 2.3%). See the tables below for full calculations.

- Analyst consensus stands at 2.2% Y/Y and 0.3-0.4% M/M, so the release appears to come in inline.

- Current tracking of core CPI (ex-energy and food, based on 50% of the national index) implies around 2.6% Y/Y (2.7% in Feb) and 0.6% M/M (0.3% Feb).

- We will provide a follow-up bullet looking at underlying drivers in due course.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP - but the direction of the surprise is normally the same.

| Y/Y | March (Reported) | February (Reported) | Difference |

| North Rhine Westphalia | 1.9 | 1.9 | 0.0 |

| Hesse | 2.4 | 2.3 | 0.1 |

| Bavaria | 2.3 | 2.4 | -0.1 |

| Brandenburg | 2.3 | 2.3 | 0.0 |

| Baden Wuert. | 2.2 | 2.5 | -0.3 |

| Berlin | 1.9 | 2.0 | -0.1 |

| Saxony | 2.5 | 2.3 | 0.2 |

| Rhineland-Palatinate | 2.0 | 2.4 | -0.4 |

| Lower Saxony | 2.4 | 2.5 | -0.1 |

| Saarland | 2.0 | 2.4 | -0.4 |

| Saxony-Anhalt | 2.9 | 3.0 | -0.1 |

| Weighted average: | 2.22% | for | 89.1% |

| M/M | March (Reported) | February (Reported) | Difference |

| North Rhine Westphalia | 0.3 | 0.4 | -0.1 |

| Hesse | 0.4 | 0.3 | 0.1 |

| Bavaria | 0.3 | 0.4 | -0.1 |

| Brandenburg | 0.4 | 0.6 | -0.2 |

| Baden Wuert. | 0.2 | 0.5 | -0.3 |

| Berlin | 0.6 | 0.4 | 0.2 |

| Saxony | 0.6 | 0.3 | 0.3 |

| Rhineland-Palatinate | 0.2 | 0.2 | 0.0 |

| Lower Saxony | 0.3 | 0.4 | -0.1 |

| Saarland | 0.2 | 0.3 | -0.1 |

| Saxony-Anhalt | 0.7 | 0.5 | 0.2 |

| Weighted average: | 0.36% | for | 89.1% |

EGB FUNDING UPDATE: Finland Q2 Funding Plans

- 3 RFGB auctions for E1.0-1.5bln each on 15 April, 20 May and 10 June.

- "The net borrowing requirement is estimated at EUR 12.289 billion, resulting in a gross borrowing amount of EUR 41.744 billion. Approximately EUR 24.3 billion of this amount is expected to be covered with long-term debt, and the rest (17.4 billion) with short-term debt."

- Finland has confirmed they are "planning to issue a second new euro benchmark bond of the year, likely in a 10-year maturity" - we had pencilled in an April (or potentially May) E4bln launch for a new 10-year Sep-35 RFGB in our Eurozone Issuance Deep Dive.

- 2 ORI operations in Q2 for E0-400mln each on 3 April and 26 June. For Q3/4, ORIs scheduled for 28 August, 30 October, and 27 November, all E0-400mln.

- "As in previous years, bonds may be issued under the EMTN programme to complement the funding in euro benchmark bonds during the year, market conditions permitting."

- 3 RFTB auctions are planned for E1-2bln each on 8 April, 13 May, and 3 June.

- "In addition to Treasury bill auctions, a tap issuance window may open during the second quarter of the year."

- "The next Quarterly Review will be published on 27 June 2025."

5-year EFSF syndication

- E5bln of the new 5-year May-30 EFSF-bond. Spread set at MS+30bps with books closing in excess of E19.5bln.

AUD: Weakness Prevailing as RBA Decision & Tariff Deadline Loom

- Analysts have been pointing out that the shifting market response to tariffs over the past two weeks has made it more difficult to position tactically, especially in currency markets. The Australian dollar has been one of the key underperformers over this period, remaining one of the best barometers for pessimism surrounding China and global risk sentiment.

- The renewed weakness in equity markets is weighing on AUD to start the week, and the close proximity to both the RBA decision and ‘liberation day’ should keep all eyes on AUD. Pricing for an AUDUSD straddle expiring on Friday (which includes NFP) incorporates a move of +/- 65 pips from current spot levels of 0.6260.

- Should AUD weakness prevail, this could place pressure on a key short-term support to watch at 0.6187, the Mar 4 low. Importantly, clearance of this level would reinstate a bearish technical theme for the pair.

- As has been well noted, lower US equities and lower US yields continue to bolster the bearish threat for AUDJPY, and the cross has recently respected downtrend resistance, drawn from the July 2024 high (shown below). Moving average studies remain in a bear mode position, and today’s sharp 1% move south renews the focus on the March double bottom at 91.86. Below here, the August global carry unwind lows ~90.15 remain a key medium-term target for the move.

FOREX: Tariff Clouds Press AUD/JPY Toward Support

- The final shape and structure of Trump's reciprocal tariffs pledge on Wednesday remains to be seen, with little clarity from the White House on whether Liberation Day will entail blanket tariff rates set against all imports, or more targeted levies against specific countries. Should convention for the previous phases of tariffs be followed, tariffs will come into effect at 0001ET/0501BST on Wednesday - leaving a tight timeline for the White House to provide further details.

- As a result of the tariff-tied uncertainty, equities are slipping alongside high-beta, growth-oriented currencies - keeping AUD and NZD at the bottom of the G10 pile. the USD Index is lower, markets are still above the mid-March lows, meaning the 200-dma resistance holds firm for now; just above last week's 104.683 highs at 104.925.

- This has boosted the JPY in early trade, confirming the risk-off picture. US equity futures are markedly lower, and growth sensitive tech names are the hardest hit - keeping the NASDAQ future off 1.3% at typing. AUD/JPY is being pressed toward support of Y93.32 - the 61.8% retracement of the upleg posted off the March 11th low.

- The MNI Chicago PMI release for March is the data highlight Monday, with markets expecting activity to remain subdued across the month. Dallas Fed manufacturing activity follows shortly afterward - with to remain the key focus given the light central bank speaker slate today.

OPTIONS: EUR Sees Sizeable Expiry Interest Against Both GBP, USD

Spot EUR/USD remains pinned between two relatively decently sized expiries rolling off at the cut today: $1.0800(E957mln), $1.0875-90(E672mln), which could contain range barring any major German inflation surprise or renewed tariff risk from Trump today.

USD/JPY, meanwhile, sees $868mln rolling off at Y150.00 and EUR/GBP with E1.1bln layered between 0.8360-70.

- AUD/USD: $0.6300(A$542mln)

- USD/CNY: Cny7.2800($915mln)

EQUITIES: Eurostoxx 50 Futures Breach Key Support, Undermining Bullish Theme

- Eurostoxx 50 futures are trading lower today and this has resulted in a breach of key support at 5229.00, the Mar 11 low. The print below this support undermines a bullish theme and signals scope for a deeper retracement. Sights are on the 5200 handle next, where a break would open 5079.00, the Feb 3 low. It is still possible that recent weakness is part of a broader correction. Initial resistance to watch is 5359.39, the 20-day EMA.

- S&P E-Minis traded sharply lower Friday and the contract maintains a softer tone. Attention is on key support and the bear trigger at, 5559.75, the Mar 13 low. A break of this level would confirm a resumption of the downtrend that started Feb 19, and open 5483.30, a Fibonacci projection. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. Key short-term resistance has been defined at 5837.25, the Mar 25 high.

COMMODITIES: Despite Some Recent Gains, WTI Future Trend Remains Bearish

- Despite recent gains, a bearish trend condition in WTI futures remains intact, and gains this month are considered corrective. However, a key resistance at $69.17, the 50-day EMA, has been pierced. The breach strengthens a bullish theme and opens $70.98, the Feb 25 high. For bears, a reversal lower would expose the bear trigger at $64.85, the Mar 5 low. Clearance of this level would resume the downtrend and open $63.73, the Oct 10 ‘24 low.

- The trend condition in Gold is unchanged, it remains bullish. Today’s strong gains highlight a bullish start to this week’s session and confirm a continuation of the primary uptrend. The rally also once again, highlights fresh all-time highs for the yellow metal. Sights are on the $3151.5, a Fibonacci projection. Support to watch lies at $2992.4, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 31/03/2025 | - | DMO Quarterly Investors/GEMM consultation | ||

| 31/03/2025 | 1200/1400 | *** | HICP (p) | |

| 31/03/2025 | 1345/0945 | *** | MNI Chicago PMI | |

| 31/03/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 31/03/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 31/03/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 31/03/2025 | 1600/1200 | ** | USDA GrainStock - NASS | |

| 31/03/2025 | 1600/1200 | *** | USDA PROSPECTIVE PLANTINGS - NASS | |

| 01/04/2025 | 2200/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 01/04/2025 | 2330/0830 | * | Labor Force Survey | |

| 01/04/2025 | 2350/0850 | *** | Tankan | |

| 01/04/2025 | 0030/1130 | ** | Retail Trade | |

| 01/04/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/04/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 01/04/2025 | 0330/1430 | *** | RBA Rate Decision | |

| 01/04/2025 | 0630/0830 | ** | Retail Sales | |

| 01/04/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/04/2025 | 0815/0915 | BoE's Greene on ‘UK MP/macro conjuncture’ | ||

| 01/04/2025 | 0820/1020 | ECB's Cipollone At Croatian National Bank Meeting | ||

| 01/04/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/04/2025 | 0900/1100 | *** | HICP (p) | |

| 01/04/2025 | 0900/1100 | ** | Unemployment | |

| 01/04/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/04/2025 | 1230/1430 | ECB's Lagarde At AI Conference | ||

| 01/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 01/04/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 01/04/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/04/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/04/2025 | 1400/1000 | * | Construction Spending | |

| 01/04/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 01/04/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 01/04/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 01/04/2025 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 01/04/2025 | 1630/1830 | ECB's Lane At AI Conference |