MNI US MARKETS ANALYSIS - Takaichi Confirmed, Policy in Focus

Highlights:

- Fed rate path comfortably discounting 2x25bps Fed cuts, even with CPI risk

- Takaichi confirmed as new Japanese PM, focus shifts to early fiscal policy set

- Canadian CPI the first of three key inflation prints this week

US TSYS: Small Gains Reversed Ahead Of A Headline Watching Session

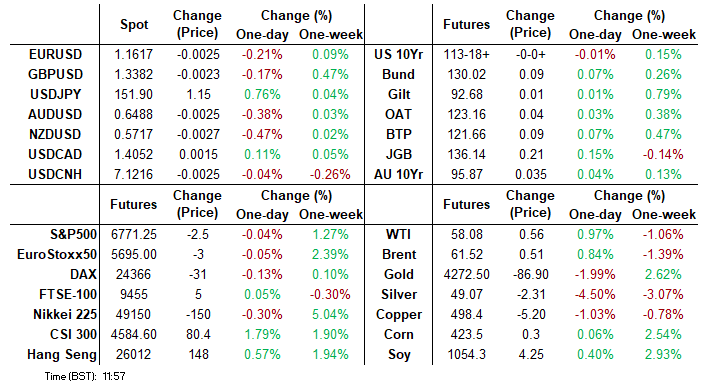

- Treasuries have over the past hour reversed earlier gains to leave them modestly lower on the day across the curve.

- Recent losses have come with crude oil futures pushing higher (+0.9%) although precious metals have extended the day's losses (gold -2.2%, reversing yesterday's increase, and a particularly notable -4.3% for silver).

- Cash yields are 0.3-1bp higher across the curve, led by the front end.

- TYZ5 trades at 113-18+ (-00+) having pulled back from earlier highs of 113-24, on subdued cumulative volumes of 235k.

- The trend signal remains bullish, with resistance at 114-02 (Oct 17 high) before 114-10 (Apr 7 continuation) whilst support is seen at 113-01+ (20-day EMA).

- Today’s data is limited to the Philly Fed non-manufacturing survey and weekly Redbook retail sales, with potential spillover from Canadian CPI at 0830ET ahead of Friday’s US release.

- Political headlines are likely more in focus, both on trade and government shutdown prospects, with various potential appearances from President Trump. Trump yesterday signed a landmark pact with Australia’s Albanese to boost America’s access to rare earths and other critical minerals.

- Data: Philly Fed non-mfg Oct (0830ET), Weekly Redbook retail sales (0855ET)

- Bill issuance: US Tsy $95B 6W bill auction (1130ET)

- Politics: Trump in peace award ceremony (1100ET), Trump hosts Rose Garden Club Lunch (1200ET, WH press pool), Trump participates in Diwali celebration (1600ET, WH press pool), Trump hosts Rose Garden Club Dinner (1900ET)

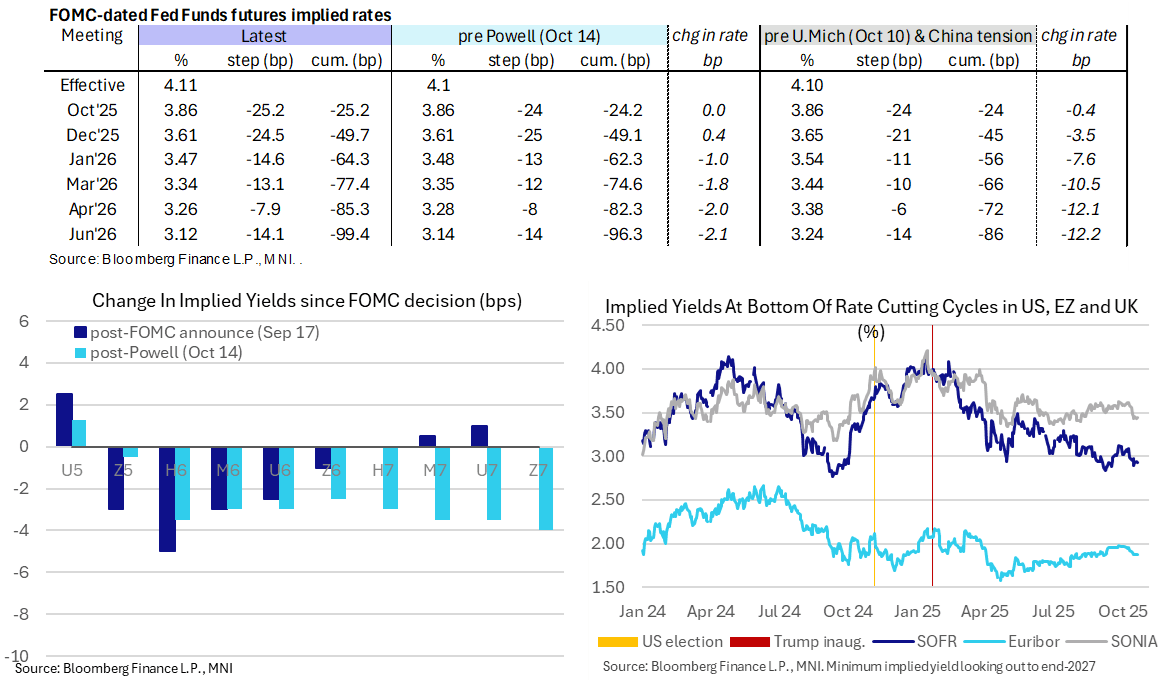

STIR: Fed Rate Path Holding Two Consecutive Cuts Before Quarterly Clips

- Fed Funds implied rates are little changed on net overnight, holding close to 50bp of cuts to year-end (consecutive 25bp cuts) before an additional ~50bp of cuts with the June FOMC.

- Cumulative cuts from 4.11% effective: 25bp Oct, 49.5bp Dec, 64.5bp Jan, 77.5bp Mar, 85.5bp Apr and 99.5bp Jun.

- SOFR futures range from -/+1 tick on the day looking out to end-2027, with small losses led by the M6 and gains by 2027 contracts after paring an earlier rally.

- The SOFR implied terminal yield of 2.93% (-0.5bp) holds at recent levels having closed at 2.93/2.935% in the past two sessions. Timing of this terminal continues to flit between the Z6 and H7.

- Thursday’s 2.89% close was the lowest in a month whilst cycle lows were seen at 2.77% back in Sep 2024 in anticipation of an aggressive start to the Fed’s easing cycle at the time.

- Today sees another light data docket, with the Philly Fed non-mfg index along with weekly Redbook retail sales, leaving greater scope for potential spillover from the Canadian CPI report for September ahead of the delayed US release on Friday.

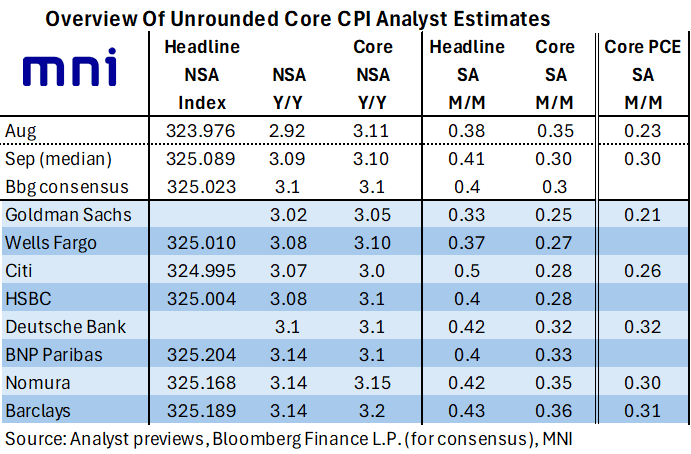

US OUTLOOK/OPINION: Core CPI and Early PCE Estimates Eye 0.30% M/M For Sept

- An early look at analyst unrounded core CPI estimates for Friday’s delayed September release sees a median estimate of 0.30% M/M, with a reasonably wide range of 0.25-0.36% M/M.

- As such, core CPI inflation is mostly expected to moderate from the 0.35% in August although it would be a third consecutive strong month after the 0.32% in July as well.

- Indeed, if accurate, it would leave there having been only two months in the past twelve with a monthly rate equivalent to less than 2% annualized (March and May). That sets it up for a more clearly cut 3.1% Y/Y after accelerating to 3.06% in August.

- Of course, the Fed targets PCE inflation, with a median of the five forecasts for core PCE also at 0.30% M/M for September. In contrast to core CPI, this would be an acceleration after 0.23% M/M in August and 0.24% in July (prior to revisions, which should be more extensive being part of the annual update).

- It's still only seen two months in the past twelve with monthly inflation below 2% annualized (March and November) whilst annual core PCE inflation was still elevated at 2.9% Y/Y in August. The median FOMC member sees this accelerating further to an average 3.1% Y/Y in Q4 before moderating to 2.6% Y/Y in 4Q26 and 2.1% Y/Y in 4Q27.

EUROPE ISSUANCE UPDATE

Estonia syndication: Revised guidance

- E500bln (WNG) tap of the 3.25% Jan-34 ESTONI. Guidance revised to MS + 75bps area (from MS + 80bps area), books in excess of E1.4bln.

UK auction results

- GBP1.5bln of the 1.50% Jul-53 Green Gilt. Avg yield 5.294% (bid-to-cover 3.17x, tail 0.8bp).

Germany auction results

*E750mln (E733mln allotted) of the 1.30% Oct-27 Green Bobl. Avg yield 1.86% (bid-to-offer 3.89x; bid-to-cover 3.97x).

- E750mln (E718mln allotted) of the 2.50% Feb-35 Green Bund. Avg yield 2.52% (bid-to-offer 2.10x; bid-to-cover 2.20x).

Finland auction results

- E548mln of the 2.625% Apr-32 RFGB. Avg yield 2.578% (bid-to-cover 1.48x).

- E869mln of the 3.00% Sep-35 RFGB. Avg yield 2.936% (bid-to-cover 1.40x).

FRANCE: Macron Re-iterates That Pension Reform Referendum A Possibility

Note these headlines from ~15 mins ago from French President Macron:

- " FRENCH PRESIDENT MACRON: PENSION REFORM THAT HAD BEEN VOTED UPON WAS NECESSARY FOR THE COUNTRY" Reuters

- "FRENCH PRESIDENT MACRON: WE NEED MOMENT OF STABILITY REGARDING PENSION REFORM DEBATE" Reuters

- "FRENCH PRESIDENT MACRON REITERATES THAT A REFERENDUM ON PENSION REFORM REMAINS A POSSIBILITY" Reuters

A reminder that as a concession to the Socialist party, PM Lecornu announced a temporary suspension of pension reform until the next Presidential election in 2027.

FOREX: JPY Weaker, Anticipating Takaichi Policy Set

- The USD sits higher against most others in G10 early Tuesday, although price action is generally contained, despite moderately lower equities from the off.

- JPY is in focus on the confirmation for Takaichi as prime minister, with Katayama taking the finance minister role, reinforcing expectations for a fiscal phase prioritizing an Abenomics-like policy set. Resultantly, JPY is weaker against all others in G10, helping USD/JPY to make light work of Y151.50 and reverse a large part of last week's late weakness. Finance Minister Katayama stopped well short of any critique of the Bank of Japan, instead referring to the currency, which should: "move stably, reflecting fundamentals".

- The recovery from last Friday’s low in USDJPY is beginning to highlight a stronger bullish signal. The pair has found support below the 20-day EMA and note that Friday’s price pattern is a hammer candle formation. If correct, the pattern signals the end of a corrective pullback that started Oct 10, and highlights the fact that support at the 50-day EMA, at 148.94, remains intact. The bull trigger is at 153.27, the Oct 10 high.

- AUD, NZD naturally underperform as a function of cautious risk sentiment and lower equity markets today. AUDUSD continues to trade both sides of the 0.6500 handle, retaining the phase of consolidation. A breach of 0.6440, the Oct 14 low, would cancel any reversal signal and reinstate a bear threat.

- Three CPI prints, Canada scheduled for today, the UK for tomorrow, and the US for Friday, provide the highlights for this week, with the UK release standing out in particular as a downside surprise could bring the potential for a notable BoE repricing. Elsewhere, we watch for fiscal policy signals in Takaichi's press conference later today. A set of ECB speakers is expected to mostly reiterate previous "rates are in a good place" rhetoric, while the Fed remains inside the media blackout.

OPTIONS: Expiries for Oct21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E961mln), $1.1640(E550mln), $1.1700(E941mln), $1.1800(E1.0bln)

- USD/JPY: Y149.90-00($1.4bln)

- GBP/USD: $1.3270(Gbp478mln), $1.3290-00(Gbp850mln)

- AUD/USD: $0.6495-00(A$800mln)

- USD/CNY: Cny7.1075($715mln), Cny7.1400($759mln)

EQUITIES: Monday's Gains Reinforce Bullish Eurostoxx Futures Theme

- The trend direction in Eurostoxx 50 futures is up and Monday's gains reinforce this theme. The breach of 5689.00, the Oct 2 and bull trigger, confirms a resumption of the uptrend. This maintains the price sequence of higher highs and higher lows and note that MA studies are in a bull-mode position, highlighting a dominant M/T uptrend. Sights are on 5727.18, a Fibonacci projection. First support lies at 5585.83, the 20-day EMA.

- A bullish theme in S&P E-Minis remains intact and the contract is trading above support at the 50-day EMA. The average, currently at 6621.98, has been pierced but remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

COMMODITIES: Gold Falls From Recent Highs But Overall Bullish Theme Intact

- A bearish theme in WTI futures remains intact and the move down last week reinforces current conditions. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. Sights are on $54.89 next, the May 5 low, where a break would open $54.10, the Apr 9 low and a key support. Initial firm resistance is seen at $61.76, the 50-day EMA. Key resistance has been defined at $66.42, the Sep 26 high.

- A bull cycle in Gold remains intact. The latest climb maintains the price sequence of higher highs and higher lows. Sights are on the $4400.00 handle next, and $4404.9, a Fibonacci projection point. Note that the trend is in overbought territory. A move down - a correction - would allow the overbought set-up to unwind. Support to watch lies at $4021.6, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 21/10/2025 | 1100/1300 | ECB Lagarde Keynote at Norges Bank Climate Conference | ||

| 21/10/2025 | 1230/0830 | *** | CPI | |

| 21/10/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 21/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 21/10/2025 | 1915/2015 | BOE Mann Fireside Chat at Lazard | ||

| 22/10/2025 | 0600/0700 | *** | Consumer inflation report | |

| 22/10/2025 | 0600/0700 | *** | Producer Prices | |

| 22/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 22/10/2025 | 1100/1300 | ECB de Guindos at Barcelona Real Assets Meeting | ||

| 22/10/2025 | 1225/1425 | ECB Lagarde Keynote at Frankfurt Finance & Future Summit | ||

| 22/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 22/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 22/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 22/10/2025 | 2000/1600 | Fed Governor Michael Barr | ||

| 23/10/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 23/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/10/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/10/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 23/10/2025 | - | ECB Lagarde at Euro Summit in Brussels | ||

| 23/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 23/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1230/0830 | ** | Retail Trade | |

| 23/10/2025 | 1330/1530 | ECB Lane Award Acceptance Speech | ||

| 23/10/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/10/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 23/10/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/10/2025 | 1425/1025 | Fed Governor Michael Barr | ||

| 23/10/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 23/10/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 23/10/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 24/10/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI |