MNI US MARKETS ANALYSIS - Sustainability of Bounce in Focus

Highlights:

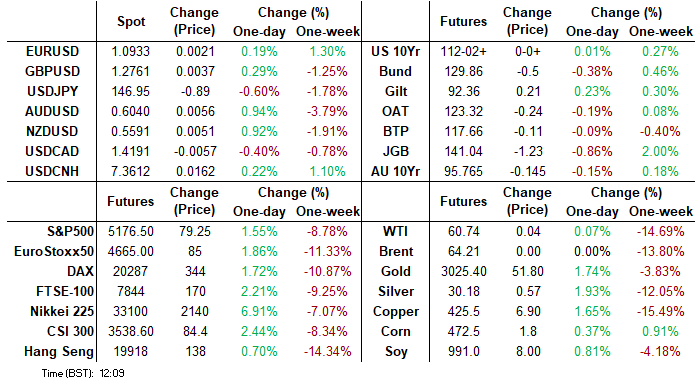

- Treasury curve modestly bull steeper

- Markets look to gauge sustainability of bounce off lows

- USD is weaker, but recent supports holding for now

US TSYS: Modestly Bull Steeper On Headline Watch

- Treasuries sit reasonably firmer on the day, although that’s only broad consolidation of yesterday’s bear steepening as they await a next material headline driver.

- Markets are likely to be on headline watch although later on, 3Y supply will prove an interesting test of demand in current volatility before SF Fed’s Daly speaks in her first remarks since Apr 2 tariff announcements.

- The steepening theme continues. Cash yields are 1-4bp lower as 30s lag with underperformance building on yesterday’s large shift steeper at the Asia open.

- 2s10s sits at 43bp (+0.5bp) as it holds near yesterday’s 45bps at fresh highs since May 2022.

- TYM5 trades at 112-02 (unch) in a relatively narrow range of 18+ ticks after yesterday’s huge 114-10 to 111-15+. Cumulative volumes have again been elevated at above 700k although down from particularly active recent overnight sessions.

- Yesterday’s low of 111-15+ marks new support with the pullback deemed corrective. Resistance is seen at 112-29 (50% of Apr 7 high/low range) after which lies that 114-10.

- Data: NFIB Mar – already released, see “US DATA: Small Business Optimism Reverses Further, Price Plans Drifting Higher”

- Fedspeak: SF Fed’s Daly on economic outlook (1400ET, Q&A only) - see STIR

- Coupon issuance: US Tsy $58B 3Y Note auction - 91282CMW8 (1300ET)

- Bill issuance: US Tsy $70B 6W Bill auction (1130ET)

STIR: Fed Rate Path Holds At Higher End Of Yesterday’s Huge Range

- Fed Funds implied rates sit at the high end of yesterday’s extremely wide range, although have still seen a 9bp range for the Dec 2025 meeting overnight.

- Cumulative cuts from an assumed 4.33% effective: 11.5bp May, 32bp Jun, 55bp Jul and 99bp Dec.

- Relative to yesterday’s close, the June meeting is 2bp higher whilst the Dec meeting is 3bp lower.

- Odds of an inter-meeting cut hold yesterday’s intraday pullback, with the FFJ5 (April) showing ~2bp of cuts (again from an assumed effective rate of 4.33%).

- The SOFR implied terminal yield at 3.115% (SFRU6) sits 2.5bp lower on the day for 28bp lower since Liberation Day.

- Ahead, SF Fed’s Daly (non-voter) speaks in a moderated discussion on the economic outlook at 1400ET (Q&A only). She hasn’t spoken since Apr 2 tariff announcements but told Reuters on Mar 28 that she still saw two rate cuts this year with the Fed able to take its time to assess the impact of tariffs. She followed up after the interview with she’s not comfortable starting rate path declines and that the Fed is 100% focused on inflation.

STIR: SONIA/Euribor Z5 Spread On Course For Tightest Close Since March 19

SONIA outperformance on the back of dovish ex-BOE official commentary sees the Z5 implied yield spread to Euribor narrow 10.0bps to 185.5bps. A close at current levels would be the tightest since March 19, and allow the spread to have fully retraced the widening seen following the March BOE decision (where the vote split was more hawkish than expected).

- The March 11 close at 178.0bps presents the next level of interest on the downside.

- This morning's Guardian report saw ex-MPC members Bean and Blanchflower argue for large imminent cuts. It is important to put the views of these former policymakers into context, however, with both having a dovish leaning.

- With UK confidence suffering we think a cut does look likely in May at least. And there is likely to be at least Dhingra voting for 50bp. We will be watching closely any further MPC comments to see if there is any change in view elsewhere.

- Today’s ECB speakers haven’t done much to shift ECB market pricing. Simkus said that he now supports a 25bp cut in April (on March 12, he was undecided between a cut and a hold), but this is already the prevailing view amongst market participants.

- SocGen are the latest to update their ECB call in light of the US tariffs. They now expect cuts in June and July, in addition to their previous call for a final cut in April.

- In addition, SocGen “do not rule out a 50bp cut to more clearly exit the restrictive stance”, but continue to expect a hike in late-2026 as “fiscal policy turns supportive, labour supply remains tight and uncertainty eases”.

- There was a light dovish reaction in front-end Euribor futures following the call change, but much smaller than the response to last week’s dovish MNI source report.

BOE: Larger MPC cuts possible - but it's former doves calling for them now

- There has been a lot of focus this morning on the Guardian article in which ex-MPC members Bean and Blanchflower argued for large imminent cuts. Bean has argued for a 50bp cut in May and Blanchflower for an intermeeting cut.

- It is important to put the views of these former policymakers into context, however, with both having a dovish leaning (albeit Blanchflower much more than Bean): Bean dovishly dissented in 5/166 MPC meetings (remember that meetings were monthly when he was on the MPC). Blanchflower dissented in half of his 36 meetings (including favouring a 50bp cut in September 2008 when the majority of the MPC voted to keep Bank Rate on hold).

- So in lots of ways, it is to be expected that two former doves remain dovish.

- Having said that, Bean does make some good points. He emphasises how much weight the MPC put on the Agents' feedback during the financial crisis - and we know that the current MPC also pays a lot of attention to the Agents now (particularly with regard to pay expectations). If the Agents' feedback is more concerning than things like the PMIs suggest, then there is a good chance the MPC acts more aggressively than the market expects.

- However, there are still inflationary challenges for the MPC to contend with: the potential passthrough from employer NICs to prices, higher wages than are consistent with a 2% inflation target, food prices starting to pick up and to move even higher later this year with a new packaging tax. For now it looks less likely the UK will introduce extra tariffs which would be inflationary (but can't be fully ruled out).

- However, with confidence suffering we think a cut does look likely in May at least. And there is likely to be at least Dhingra voting for 50bp. We will be watching closely any further MPC comments to see if there is any change in view elsewhere. Lombardelli is on a panel at 17:00BST today while Breeden is at an MNI Connect webinar Thursday (register here).

- What about past May? The next 5 days are hard to predict at the moment, let alone months into the future. We think the BOE will try and keep communications about future actions very restrained.

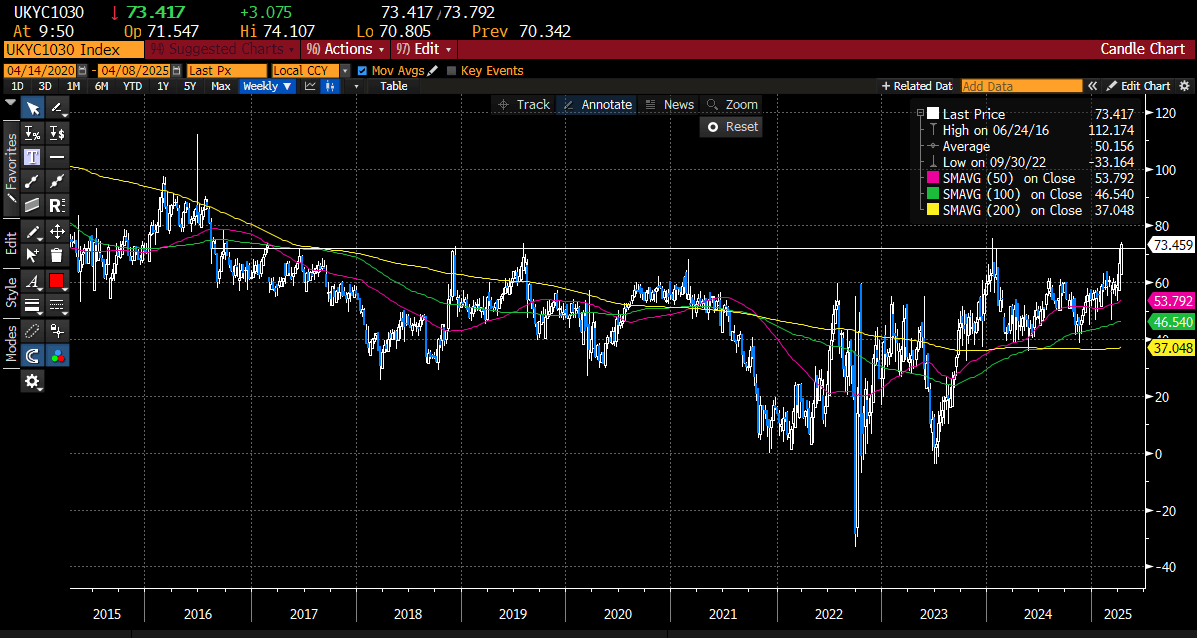

GILTS: 10s30s above 72bp - a level we haven't closed 2 days above since 2016

- 2-year gilts continues to outperform both USTs and Schatz this morning, largely due to the Guardian article out earlier with comments from former MPC members (who were both dovish) calling for larger / earlier cuts - see 9:00BST comment for our views on that. The 1.25% Jul-27 gilt has seen yields fall as low as 3.712% today from a close yesterday of 3.797% (an 8.5bp move at it's maximum today) although around half of the move has been retraced and we now trade around 3.75% at writing.

- We are also seeing 10s30s steepen more for gilts than for Germany or the US ahead of the 4.375% Jul-54 gilt auction (with the bidding window due to close at 10:00BST). The steepening of 10s30s has reached new highs for gilts (but not the other two markets this morning). 10s30s are trading around 73.6bp at writing - moving above 72bp for the first time since 2024. Note that we haven't closed two consecutive days above 72bp since 2016 - so this is a significant level.

- This leaves 10-year gilts outperforming Bunds this morning with a steepening of the curve.

- The auction is the obvious near-term focus but we will also hear from Lombardelli after gilts close later today.

FOREX: Looking to Gauge Sustainability of the Bounce

- Markets are bouncing Tuesday, led higher by the reversal off Monday's pullback lows for US stock futures. The E-mini S&P has bounced off yesterday's 4832.00 to reclaim near 350 points to point to a steadier outlook into the NY crossover today.

- For currencies, this has translated to AUD and NZD strength: AUD/USD has shown back above $0.6050 NZD/USD back above $0.5600. While these recoveries amount to over 1.5%, they still nurse significant losses off last week's highs, meaning any fade in the corrective bounce will have markets re-considering recent lows.

- This leaves the USD as the poorest performing currency in G10, although the ability of the market to hold above 103.00 keeps the market technically constructive in the short-term.

- Datapoints are few and far between Tuesday, keeping market focus on the sustainability of this recovery from lows. Monday's acute volatility is another sign that markets will read credibly into any well-sourced reports of policy U-turns, keeping attention on the US news cycle and any signals from the President.

- Trump's schedule Tuesday sees numerous events - most consequential of which are his executive order signing event at 1500ET/2000BST and comments set to be made at an NRCC dinner after markets close.

FOMC: AUD Remains Vulnerable to Tariff Conflict Intensification

- Stronger risk sentiment during Asia hours has prompted some moderate weakness for the US dollar, and has elevated the high-beta antipodean currencies to the top of the G10 board.

- AUDUSD is up 1.3% at 0.6063 but the looming deadline for further US tariff retaliation against China threatens the latest recovery, with the technical outlook for the pair remaining bearish.

- More broadly, ING "would be cautious in chasing big rebounds in high-beta currencies, and especially oil-sensitive currencies. Trump has given little signs of scaling back protectionism, and there is a risk that markets are again erring on the side of optimism.

- For AUDUSD, yesterday’s low print of 0.5933 matched closely with an initial technical support, the 1.764 projection of the Sep 30 - Nov 6/7 price swing. This will remain the key short-term mark on the downside. Below here, round number support at 0.5900 and another projection level at 0.5830 will garner attention. To the upside, initial resistance stands at 0.6127, the Apr 7 high.

- On the local calendar, Westpac consumer confidence and NAB business confidence showed decline from prior prints. Consumer inflation expectations for April are due Thursday.

OPTIONS: Expiries for Apr08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0950-65(E727mln), $1.1270(E2.0bln)

- USD/JPY: Y144.95-00($1.8bln), Y147.00-10($756mln), Y149.00($886mln)

- GBP/USD: $1.2785-10(Gbp590mln)

- EUR/GBP: Gbp0.8500(E638mln)

- AUD/USD: $0.6005-20(A$636mln), $0.6340-50(A$2.1bln)

EQUITIES: Stocks Undergo Corrective Bounce, But Vol Here to Stay

- S&P E-Minis continues to trade in a volatile manner. A bearish theme remains intact and the latest fresh cycle lows, strengthen current conditions. Scope is seen for an extension towards the 4800.00 handle next.

- Eurostoxx 50 futures remain in a bear cycle following the latest impulsive sell-off. Monday’s move down resulted in a breach of a key support at 4699.00, the Nov 19 ‘24 low (cont).

COMMODITIES: Gold Still Bullish Despite Fast Fade Off Highs

- The trend condition in Gold remains bullish and the latest pull back appears corrective. Moving average studies are in a bull-mode position highlighting a dominant uptrend and positive market sentiment.

- A bearish theme in WTI futures remains intact following the recent impulsive sell-off. The move down has resulted in the breach of a number of important support levels. The break reinforces a bearish threat and, despite being in oversold territory, signals scope for a continuation of the bear leg.

| Date | GMT/Local | Impact | Country | Event |

| 08/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/04/2025 | 1400/1000 | * | Ivey PMI | |

| 08/04/2025 | 1400/1600 | ECB's Cipollone at ECON Hearing On Digital Euro | ||

| 08/04/2025 | 1400/1000 | United States Trade Representative Jamieson Greer | ||

| 08/04/2025 | 1600/1700 | BoE's Lombardelli on 'What can the UK learn from the US' | ||

| 08/04/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 08/04/2025 | 1800/1400 | San Francisco Fed's Mary Daly | ||

| 09/04/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 09/04/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 09/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 09/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/04/2025 | - | Higher Reciprocal Tariffs On Imports | ||

| 09/04/2025 | 1230/1430 | ECB's Cipollone On Macro-Financial Stability Panel | ||

| 09/04/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/04/2025 | 1500/1100 | Richmond Fed's Tom Barkin | ||

| 09/04/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/04/2025 | 1800/1400 | *** | FOMC Minutes |