MNI US MARKETS ANALYSIS - Stocks Remain Fragile, UMich Up Next

Highlights:

- Equities remain fragile, providing latest signal that sentiment may be fading

- UMich sentiment data to take on extra weight given extended shutdown

- Trump meets Hungary's Orban in the White House, comments on Russia sanctions likely

US TSYS: Losses Pared To Consolidate Thursday Rally On Soft Labor Data

- Treasuries have pared earlier losses with equity futures extending some overnight weakness, leaving Treasuries broadly consolidating yesterday’s rally on a collection of soft lower tier data releases.

- There’s no BLS payrolls report today with the government shutdown ongoing, with today’s data instead likely highlighted by the preliminary U.Mich consumer survey for November despite susceptibility to early responses from those of differing political affiliation. The latest MNI data shutdown guide is here.

- Cash yields are back to just 0-0.5bp higher across the curve.

- TYZ5 trades at 112-27+ (+ 01) having recently lifted ~5 ticks, with modest overnight volumes of 285k.

- Yesterday’s high of 112-30 came close to a key near-term resistance at 113-02 (Nov 5 high) after which lies 113-18+ (Oct 28 high). A key near-term support remains exposed at 112-06 (Sep 25 low) although before that lies 112-09+ (Nov 5 high).

- Data: Manheim used cars Oct final (0900ET), U.Mich consumer survey Nov prelim (1000ET), NY Fed consumer survey Oct (1100ET), Consumer credit Sep (1500ET)

- Fedspeak: Jefferson on AI & economy (0700ET), Miran on stablecoins and mon pol (1500ET) – see STIR bullet

- Speaking overnight, NY Fed's Williams said "Based on recent sustained repo market pressures and other growing signs of reserves moving from abundant to ample, I expect that it will not be long before we reach ample reserves"

- Politics: Trump greets Hungary PM (1130ET) before bilateral lunch (1145ET), Trump departs for Florida (1530ET)

STIR: US Rates Pare Losses With Equity Pressure, Jefferson Leads Fedspeak

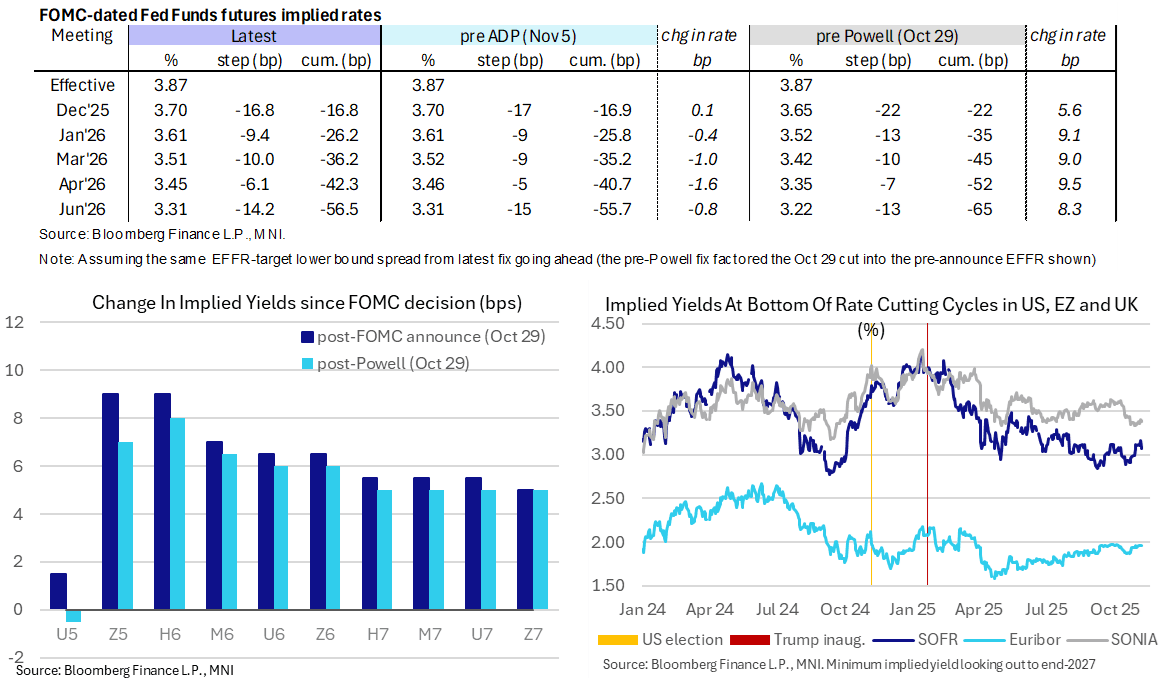

- Fed Funds implied rates have softened in recent trading with equity futures under pressure, to limit a lift off yesterday’s lows following softer labor data (Revelio Labs, Challenger and less so the Chicago Fed’s u/e rate nowcast).

- Dec FOMC pricing is unchanged on the day although 1H26 meetings are 1-1.5bp higher.

- Cumulative cuts from 3.87% effective: 17bp Dec, 26bp Jan, 36bp Mar, 42.5bp Apr and 56.5bp Jun.

- SOFR futures are 0.5-1 tick firmer, with the terminal yield at 3.075% (H7) as it consolidates yesterday’s 8bp decline from Wednesday’s highest close since late July (post ADP and ISM services).

- Today sees more limited Fedspeak after yesterday’s heavy schedule, with our focus on Vice Chair Jefferson for his first post-FOMC appearance.

- 0700ET – VC Jefferson (voter) on AI and the economy (text + Q&A). A Sep 29 speech suggested a monetary policy outlook in line with that of most of the rest of the Fed leadership, including Chair Powell. We guess he is among the 9 FOMC participants who anticipate making a further 2 25bp rate cuts by year-end to 3.6% (per the median dot from the September SEP). We’ll watch his comments on recent labor market developments in particular.

- 1500ET – Gov. Miran (voter) on stablecoins and mon pol (text + Q&A). Clearly the most dovish member on the FOMC with two dissents for larger than 25bp cuts since joining the Board, he earlier this week reiterated that policy remains too restrictive with “neutral quite a ways below” and also cited recent signs of stress in credit markets. Discussing the better-than-expected ADP data on Wednesday, subsequent weakness in lower tier data will likely be noted.

SOFR: Net Long Setting Most Prominent In Futures On Thursday

OI data points to net long setting dominating in SOFR futures on Thursday, albeit with some pockets of net short cover (including SFRU5 & SFRZ5) seen.

- Net long setting in SFRH6 provided the largest net positioning shift.

- Pricing moved in a dovish direction onsoft lower tier labour market indicators as official data releases remain a casualty of the government shutdown.

- Weakness in equities also factored in.

| 06-Nov-25 | 05-Nov-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,379,588 | 1,382,462 | -2,874 | Whites | +24,140 |

SFRZ5 | 1,453,232 | 1,458,766 | -5,534 | Reds | +21,662 |

SFRH6 | 1,204,667 | 1,180,343 | +24,324 | Greens | +17,842 |

SFRM6 | 1,100,169 | 1,091,945 | +8,224 | Blues | +11,791 |

SFRU6 | 1,102,099 | 1,093,954 | +8,145 |

|

|

SFRZ6 | 1,203,345 | 1,207,732 | -4,387 |

|

|

SFRH7 | 835,047 | 827,766 | +7,281 |

|

|

SFRM7 | 799,894 | 789,271 | +10,623 |

|

|

SFRU7 | 753,440 | 756,272 | -2,832 |

|

|

SFRZ7 | 804,190 | 791,533 | +12,657 |

|

|

SFRH8 | 426,474 | 418,548 | +7,926 |

|

|

SFRM8 | 403,754 | 403,663 | +91 |

|

|

SFRU8 | 343,579 | 338,725 | +4,854 |

|

|

SFRZ8 | 332,094 | 332,567 | -473 |

|

|

SFRH9 | 206,411 | 201,796 | +4,615 |

|

|

SFRM9 | 188,797 | 186,002 | +2,795 |

|

|

US TSY FUTURES: Long Setting Most Prominent During Thursday Rally

OI data points to a mix of net long setting (TU, FV, UXY & WN) and short cover (TY & US) as Tsy futures ticked higher on Thursday, with soft lower tier labour market indicators providing support as official data releases remain a casualty of the government shutdown.

- The curve-wide positioning bias was tilted towards net long setting, with the largest swings coming in TU & FV futures.

| 06-Nov-25 | 05-Nov-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,682,057 | 4,625,515 | +56,542 | +2,126,257 |

FV | 6,852,516 | 6,812,126 | +40,390 | +1,734,067 |

TY | 5,448,855 | 5,449,874 | -1,019 | -68,163 |

UXY | 2,479,209 | 2,477,731 | +1,478 | +132,753 |

US | 1,854,990 | 1,865,605 | -10,615 | -1,351,619 |

WN | 2,154,161 | 2,153,410 | +751 | +140,325 |

|

| Total | +87,527 | +2,713,619 |

FOREX: USDJPY Recovers From Lows, AUDNZD Pushes To Fresh 12-Year Highs

- The Yen has seen some moderate weakness this morning following Takaichi headlines saying the government's target achieving a primary balance surplus would no longer be reviewed on a single-year basis, adding to fiscal easing expectations. Combined with a modest firming of the dollar, this has prompted a recovery for USDJPY to the 153.50 region. Markets will remain focused on the cluster of daily highs between 154.36-48, while first important support to watch lies at 152.46, the 20-day EMA.

- Meanwhile, AUDNZD has pushed to a fresh 12-year high of 1.1567 overnight as the New Zealand dollar remains in a downtrend amid the lacklustre NZ economy. Chinese trade data, seeing the weakest Y/Y rate since February, may have contributed to the NZD price action today, while AUD outperformed amid headlines on a China - Australia multilateral trading system. The next target for AUDNZD would be 1.1586, the October 2013 high.

- GBP underperforms as markets digest yesterday's BoE meeting, resulting in a knife edge bank rate hold which firmly put a December cut on the table. Governor Bailey said he "would prefer to wait and see if the durability in disinflation is confirmed in upcoming economic developments" - but a disinflationary budget on November 26 may well be associated with fiscal tightening, which would weigh on the UK economy, adding to GBP pressures.

- Importantly for GBPUSD, the pair respected the initial resistance overnight, holding the prior breakdown level around the 1.3140 mark. The move higher is allowing an oversold trend condition to unwind, and the bear trigger now lies at 1.3010, the Nov 4 and 5 low.

- Canadian labour market data later today is seen as a relatively stable month after a string of volatile prints. In the US, Michigan consumer sentiment and inflation expectations are scheduled ahead of NY Fed inflation expectations. Fed's Jefferson and Miran are scheduled to speak next to a series of ECB speakers.

OPTIONS: Expiries for Nov07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.1bln), $1.1700(E1.0bln)

- USD/JPY: Y153.00($1.1bln), Y153.85($725mln)

- AUD/USD: $0.6500(A$1.1bln)

- USD/CAD: C$1.3900($2.3bln)

EQUITIES: E-Mini S&P Corrective Cycle Exposes 50-Day EMA

- A bullish trend in Eurostoxx 50 futures remains intact and recent weakness appears to have been corrective. The contract has found support at the 50-day EMA, currently at 5577.05. Support below the EMA lies at 5566.00, the base of a bull channel drawn from the Aug 1 low. A breach of this level and the 50-day EMA, is required to highlight a stronger reversal. Sights are on resistance and the bull trigger at 5742.00, the Oct 29 high.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the pullback since the Oct 30 high appears corrective. Support at the 20-day EMA, at 6800.30, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6708.51 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

COMMODITIES: Corrective Bear Cycle in Gold Remains Intact for Now

- The latest pullback in WTI futures appears to be a flag formation - a bullish continuation pattern. This suggests that a bullish corrective cycle remains intact for now. Price has recently traded through the 50-day EMA, at $60.91, signalling scope for a stronger recovery. Note too that resistance at $62.34, the Oct 8 high, has been pierced. A clear move through it would expose key resistance at $65.77, Sep 26 high. The bear trigger is $55.96, the Oct 20 low.

- A corrective bear cycle in Gold remains intact for now. The move down since Oct 20 has allowed an overbought trend condition to unwind. Support around the 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3875.8 - a key pivot support. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

| Date | GMT/Local | Impact | Country | Event |

| 07/11/2025 | 1200/0700 | Fed Vice Chair Philip Jefferson | ||

| 07/11/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 07/11/2025 | - | BOE MPG Agenda Published | ||

| 07/11/2025 | 1330/0830 | *** | Labour Force Survey | |

| 07/11/2025 | 1330/1430 | ECB Elderson At Bundesbank Event | ||

| 07/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 07/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 07/11/2025 | 1515/1515 | BOE Pill At National Agency Briefing | ||

| 07/11/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 07/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 07/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 07/11/2025 | 2000/1500 | Fed Governor Stephen Miran |