MNI US MARKETS ANALYSIS - Stocks on Top as Trump-Xi Meet Nears

Highlights:

- Equities rally as markets narrow in on Trump-Xi meeting

- CNY fix comes in at strongest of the year

- With government still in shutdown, Fed meeting takes focus on Wednesday

US TSYS: TYA Probes Support Overnight On US-China Optimism, Heavy Supply Today

- Treasuries have pared losses but still trade lower ahead of this week’s Trump-Xi meeting after encouraging headlines and agreements surrounding working meetings in Malaysia over the weekend.

- Today sees heavy Treasury issuance headline an otherwise quieter docket, with 2Y and 5Y auctions as a result of month-end timing and Wednesday’s FOMC decision. President Trump is in Japan.

- Cash yields are 1.7-2bp lower across the curve, with no sign of upcoming front-end/belly supply weighing on curves.

- TYZ5 trades at 113-08+ (-05+) on reasonable cumulative volumes nearing 300k.

- It shifts further away from post-CPI fleeting highs of 113-24 (which didn’t trouble resistance at 114-02, Oct 17 high) and has sustained moves below pre-CPI levels of ~113-11. Moving average studies highlight a bullish structure but the 113-04 seen overnight probed support at 113-06+ (20-day EMA), with a clearer breach then opening 112-30 (Oct 13 low).

- Data: Dallas Fed Mfg Activity (1030ET)

- Coupon issuance: US Tsy 2Y auction - 91282CPE5 (1130ET), $70B 5Y auction - 91282CPD7 (1300ET)

- Bill issuance: US Tsy $77B 26W bill (1130ET), $86B 13W bill (1300ET)

- Politics: Trump in courtesy call and visit with Emperor of Japan (0530ET), Trump in extended bilateral meeting with Japan PM (2030ET)

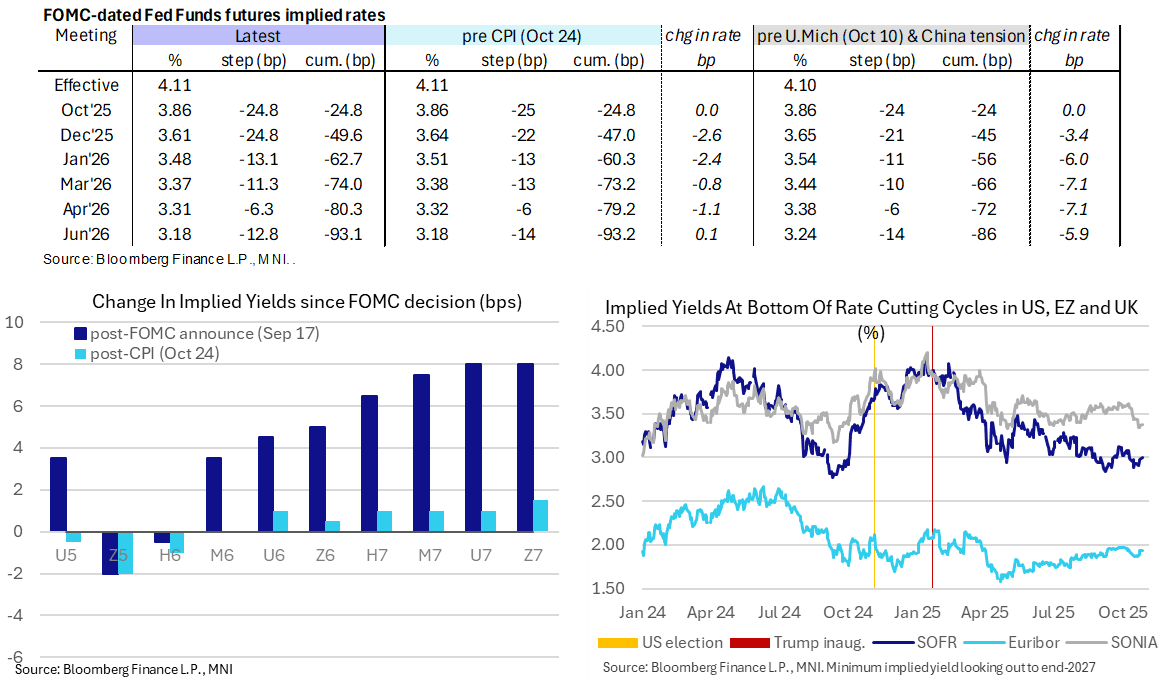

STIR: US-China Trade Deal Optimism Limits Dovish CPI Impact

- US-China trade deal optimism ahead of Trump-Xi meeting this week sees Fed Funds implied rates 1-2bp higher since Friday’s close, Wednesday’s decision aside where the Fed is still fully priced to cut 25bps.

- It’s seen these nearer term meetings reverse a large part of the dovish reaction to Friday’s CPI miss – see table.

- Cumulative cuts from 4.11% effective: 25bp for Wed, 49.5bp Dec, 62.5bp Jan, 74bp Mar, 80.5bp Apr and 93bp Jun

- Look beyond mid-2026 and SOFR futures are now a little lower than pre-CPI levels, albeit only just with a modest 1.5-2.5 tick decline since Friday’s close looking out to end-2027 contracts.

- The terminal implied yield is currently at 2.995% (SFRZ6) having last closed higher on Oct 9 prior to the initial flare-up in US-China trade tensions.

- MNI Fed Preview here: https://media.marketnews.com/Fed_Prev_Oct2025_6a6731f139.pdf with the analyst update to follow later today.

UK FISCAL: Headlines from the weekend: More sources on income tax hikes

Last week the Guardian broke the news that income tax hikes were being discussed by the Treasury (although noted that Chancellor Rachel Reeves was still not sure if she wanted to break a manifesto pledge). Some of the weekend news has fleshed out these stories.

- The Sun on Sunday (link here) has run a sourced story that the income tax rise under consideration is 2ppt. This is the top end of expectations - we had expected 1-2ppt to be under discussion. However, it is probably too much to read into this that 2ppt will be the eventual outcome - it would be strange to not at least discuss 2ppt if any income tax raise was under consideration. The article runs with the numbers of around GBP20bln/year additional revenue. This is presumably from a 2ppt increase to both basic rate and higher rate. Based on the Treasury's January estimates a 1ppt increase to basic rate would raise around GBP8.2bln/year and higher rate GBP2.1bln/year.

- The Independent (link here) runs a story on potential increases to the additional rate of income tax - or potentially lowering the threshold where it kicks in (currently just above GBP125k). However, as the story notes there are already kinks in the tax code that make lowering the threshold problematic. At GBP100k the personal allowance is gradually withdrawn, leading to an effective tax rate of 60%. So reduction to GBP110k for example would lead to a marginal tax rate of 67.5%. Alternatively raising the 45% rate by 5ppt would only raise a little more than GBP1bln/year.

- Remember, that we look at the options for income tax, VAT and national insurance increases in our analysis piece here.

UK FISCAL: Headlines from the weekend: Fuel duty, former PM, food prices

- The Sun on Sunday also runs that the 5p/litre "temporary" cut to fuel duty is expected to be scrapped. This would of course raise revenue (around GBP900mln per year). But would not help with Reeves' pledge to help cut the cost of living.

- Former PM Rishi Sunak wrote an op ed in Sunday Times. He urges Chancellor Rachel Reeves to increase headroom at the Budget. One of the more interesting points he notes is that he notes that Reeves would probably not be discussing increasing the headroom if she wasn't given opening numbers from the OBR that had been better than those at the more pessimistic end of the range. Most of the rest of the interview was broadly in line with what you would expect from a former leader of the opposition.

- There are also continued reports that supermarkets are lobbying against any increases in business rates - noting that margins for supermarkets are incredibly thin. And that any increase in taxes would lead to further increases in food prices.

- A number of media reports point to reductions in the cash ISA limit to GBP10k from GBP20k (this has been speculated on for a long time now so isn't huge news).

JAPAN: Moody's Affirm Japan at A1; Outlook Stable

"*MOODY'S RATINGS AFFIRMS JAPAN'S A1 RATINGS, MAINTAINS STABLE" - bbg

- "JAPAN RATING ACTION REFLECTS TRACTION ON REFLATION & FISCAL POLICY GEARED TOWARDS CONSOLIDATION

- DO NOT EXPECT RECENT LEADERSHIP TRANSITION TO SIGNIFICANTLY REVERSE JAPAN'S GAINS IN FISCAL CONSOLIDATION" - Reuters

EUROPE ISSUANCE UPDATE

Belgium auction results

- E1.064bln of the 2.60% Oct-30 OLO. Avg yield 2.533% (bid-to-cover 1.51x).

- E605mln of the 1.25% Apr-33 Green OLO. Avg yield 2.804% (bid-to-cover 1.63x).

- E1.335bln of the 3.10% Jun-35 OLO. Avg yield 3.149% (bid-to-cover 1.53x).

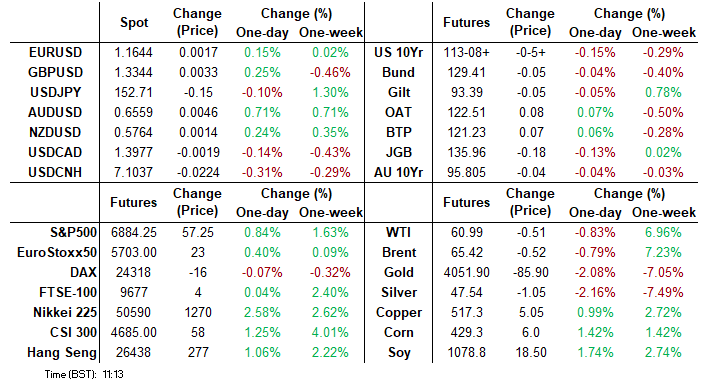

FOREX: US-China Optimism Boosts AUD, USDJPY Winning Streak in Focus

- Risk sentiment has been positively impacted to start the week, amid optimism surrounding US-China trade negotiations ahead of Thursday's Trump-Xi meeting. AUD outperforms all others in G10 today, reacting positively in particular given its high beta status and sensitivity to the Chinese economy.

- Additionally, RBA Bullock's comments playing down recent job weakness and mentioning they are in a "pretty good" position on both jobs and CPI added to topside momentum for AUDUSD, now up 0.68% on the session at 0.6552. Today’s extension higher has strengthened a bullish theme, narrowing the gap to initial resistance at 0.6574, the 50.0% retracement of the Sep 17 - Oct 14 bear leg.

- Higher core yields initially weighed on the Japanese Yen, with USDJPY extending its most recent rally ahead of the European open. The pair traded to within one pip of 153.27, the Oct 10 high and a bull trigger. Clearance of this hurdle would confirm a resumption of the medium-term uptrend. Japan officials noted they were monitoring FX markets for disorderly moves, and although USDJPY has reverted back below the 153.00 handle, the remarks didn't suggest intervention risks were more heightened for now.

- Despite the generally flat USD Index, USDCNH is breaking lower again, building on a strong session for China FX overnight. The rate is testing 7.1050 at typing for the lowest print since September, narrowing the gap with key support into 7.0851, the cycle low. Moves follow the stronger-than-expected CNY fix (7.0881, the lowest in over 12 months), consistent with the bank's long-held push for further internationalization and expanded use - which the bank reiterated on Friday last week after the conclusion of the government's 4th plenum.

- Central banks highlight this week's calendar, with the Bank of Canada and the Fed holding policy meetings on Wednesday, before the Bank of Japan and the ECB follow Thursday.

CNH: USDCNH at New Lows in Europe on Fix, Positive Trade Deal Language

- Despite the generally flat USD Index, USDCNH is breaking lower again, building on a strong session for China FX overnight. Rate is testing 7.1050 at typing for the lowest print since September, narrowing the gap with key support into 7.0851, the cycle low.

- Moves follow the stronger-than-expected CNY fix (7.0881, the lowest in over 12 months), consistent with the bank's long-held push for further internationalization and expanded use - which the bank reiterated on Friday last week after the conclusion of the government's 4th plenum. Moves come after the likely absorption of early USD demand. Bloomberg sources reported state banks on the bid in USDCNY shortly after the local open, which may have contained any break lower on the positive trade news and the fix - but this pressure seems to have given way in early Europe.

- Positive language around this week's trade talks between the US and China will also be a major contributor, particularly as Bessent confirmed over the weekend that Trump's 100% additional tariff threat is "effectively off the table". In signs that a framework agreement is getting closer, concessions are also supposedly likely to be made from the Chinese side, with additional soybean purchases as well as a delay to the implementation of rare earths controls floated.

- The timing of the stronger fix is notable here - moves to strengthen the CNY

- In addition, we wrote last week of the shoot higher in the FX Settlement-Sales Spread in the September data being consistent with a faster pace of corporates closing out of FX positions relative to new FX exposure - https://www.mnimarkets.com/articles/safe-data-shows-fx-settlement-sales-spread-at-new-high-1761130823546

OPTIONS: Expiries for Oct27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1520-35(E1.5bln), $1.1620-40(E1.6bln), $1.1650(E548mln), $1.1670-80(E1.4bln), $1.1700-10(E1.1bln)

- USD/JPY: Y152.00($531mln)

- AUD/USD: $0.6490(A$2.0bln)

- USD/CAD: C$1.4100($793mln)

COMMODITIES: Gold Pullbacks Still Deemed Corrective

A sharp pullback in Gold last week appears corrective - for now. Note that the trend is overbought and a deeper retracement would allow this condition to unwind. Attention is on support at the 20-day EMA, at $4052.6, has been pierced. The latest recovery in WTI futures appears corrective for now, however, note that price has traded through resistance at the 50-day EMA, at $61.13. The breach of this average signals scope for a stronger recovery.

EQUITIES: Stocks Extend Bullish Price Sequence

The trend condition in S&P E-Minis remains bullish and the contract is trading higher today, as it begins the week on a bullish note. The fresh cycle high confirms a resumption of the primary uptrend. The trend structure in Eurostoxx 50 futures is bullish. The recent breach of 5689.00, the Oct 2 high and bull trigger, confirms a resumption of the uptrend. This maintains the price sequence of higher highs and higher lows.

| Date | GMT/Local | Impact | Country | Event |

| 27/10/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 27/10/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/10/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/10/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 27/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 27/10/2025 | 1530/1130 | * | US Treasury Auction Result for 2 Year Note | |

| 27/10/2025 | 1700/1300 | * | US Treasury Auction Result for 13 Week Bill | |

| 27/10/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/10/2025 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 28/10/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 28/10/2025 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 28/10/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/10/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 28/10/2025 | - | FOMC Meeting | ||

| 28/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/10/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 28/10/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/10/2025 | 1400/1000 | ** | housing vacancies | |

| 28/10/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 28/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note |