MNI US MARKETS ANALYSIS - Sept Fed Pricing Lingers Below 25bps

Highlights:

- 'Coalition of the Willing' set to brief European leaders on Ukraine-Russia-US Summit outcomes

- Sept Fed pricing still lingers short of 25bps

- Canadian Core CPI seen inching higher on a trimmed mean basis

US TSYS: Mildly Firmer Awaiting Fresh Impetus, TYA Support Monitored

- Treasuries are mildly firmer, gaining through London hours, but with relatively little net reaction to yesterday’s meetings between Trump, Zelenskyy and EU leaders.

- The most important outcome of the talks from the perspective of Ukraine and its European allies will be the pledge from Trump on security guarantees for Kyiv. Trump instructed Secretary of State Marco Rubio to begin work on establishing what these will look like.

- Today sees housing data, a dovish Bowman and then scheduled White House/Trump comments from 1300ET.

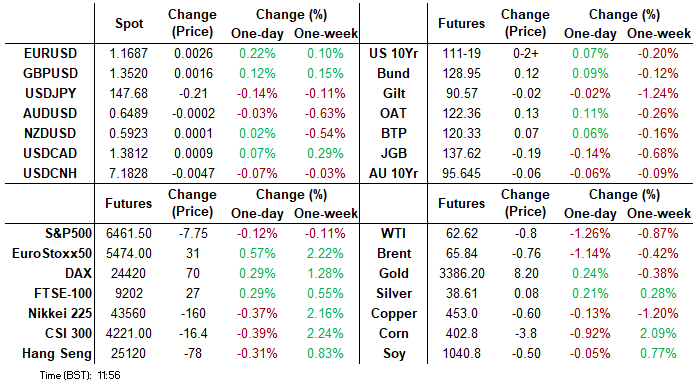

- Cash yields are 0.3-1.0bp lower on the day.

- 5s30s at 108.4bps continues to hold close to yesterday’s fresh ytd high of 109.6bps as the year’s steepening theme clearly holds (40bps on Dec 31).

- TYU5 trades at 111-19+ (+03) on thin cumulative volumes of 215k.

- Support is being monitored after yesterday’s low of 111-13+ came close to the 50-day EMA of 111-10+. A push lower could then open 110-23+ (Aug 1 low). To the upside sits resistance at 112-15+ (Aug 5 high) having hit 112-14 prior to Thursday's strong PPI report.

- Data: Housing starts/building permits Jul/Jul prelim (0830ET)

- Fedspeak: Bowman on BBG TV (1000ET), Bowman at Blockchain Symposium (1410ET, text only) – see STIR bullet

- Bill issuance: US Tsy $85B 6W bill auction (1130ET)

- Politics: White House Press Sec Leavitt briefing (1300ET), President Trump signs a Congressional Bill (1300ET)

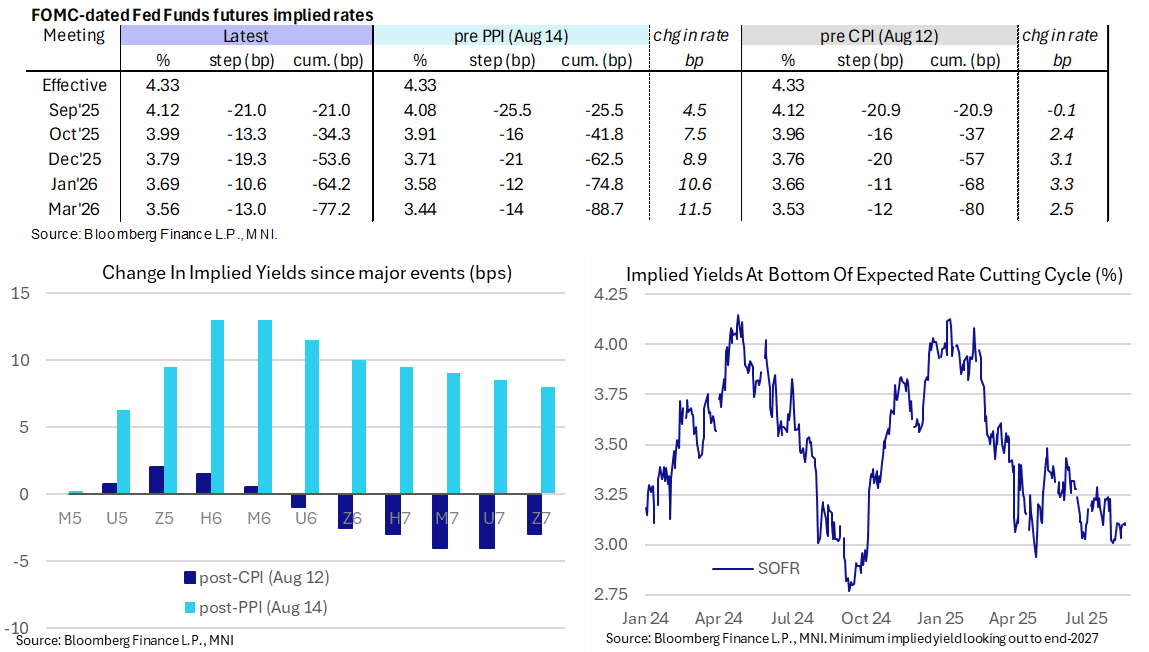

STIR: Sept Fed Cut Still No Longer Fully Locked In, A Dovish Bowman Ahead

- Fed Funds implied rates are unchanged on the day, with 21bp of cuts priced for next month’s FOMC meeting.

- Cumulative cuts from 4.33% effective: 21bp Sep, 34.5bp Oct, 53.5bp Dec, 64bp Jan and 77bp Mar.

- The SOFR implied terminal yield of 3.11% (SFRH7) is essentially unchanged from the past two closes, holding the +/-5bp of 125bp of cuts from current levels range seen since the Aug 1 payrolls report.

- Fed VC Supervision Bowman (permanent voter, dove) speaks on Bloomberg TV at 1000ET before at a Blockchain Symposium at 1410ET (text only), with greater scope for market moving comments at the former. We suspect it might be hard to generate a dovish reaction though unless she canvasses larger cuts, something other FOMC colleagues have pushed back on.

- These will be her first remarks since last week’s mixed inflation data. She said on Aug 9 that she favors three cuts this year (unsurprising having dissented in July) and saw recent labor data as reinforcing this view.

- Tomorrow then sees the FOMC minutes before Powell’s Jackson Hole address on Friday. However, when it comes to Sept cut prospects, the August payrolls and CPI releases plus QCEW details (for preliminary payroll benchmark revision estimates) are all still to come before the next FOMC decision on Sep 17.

EUROPE ISSUANCE UPDATE

UK auction results

- GBP1.6bln of the 1.125% Sep-35 Linker. Avg yield 1.728% (bid-to-cover 3.10x).

German auction results

- E4.5bln (E3.424bln allotted) of the 2.20% Oct-30 Bobl. Avg yield 2.32% (bid-to-offer 1.47x; bid-to-cover 1.93x).

Finland 7-year Apr-32 RFGB Mandate:

- "The Republic of Finland has mandated Barclays, BofA Securities, Danske Bank, Deutsche Bank and J.P. Morgan to lead manage its forthcoming new short 7-year Benchmark transaction. The transaction will have a 15 April 2032 maturity and is expected to be launched in the near future subject to market conditions." From market source

- This is not a surprise, as we noted two week ago: We expect the final Finnish syndication of the year in either the W/C 18 August or W/C 25 August. The Treasury noted in its Q3 issuance guidance that the maturity will likely be in the 5-7 year sector (note that in the annual funding plan this was seen as either a 7-year or 15-year).

- We pencil in a E3bln WNG transaction tomorrow.

SECURITY: 'Coalition Of The Willing' To Hold Call After White House Talks

The 'coalition of the willing' group, formed by countries that have committed to 'boots on the ground' in Ukraine in the event of a ceasefire/peace deal, will hold a national leaders videoconference at 06:00ET/11:00BST/12:00CET. The call will allow those leaders present at the White House talks on 18 August to brief the other leaders on the situation vis-a-vis US security guarantees, a trilateral meeting, and other key outcomes from the talks.

- The most important outcome of the talks from the perspective of Ukraine and its European allies will be the pledge from US President Donald Trump on security guarantees for Kyiv. Trump instructed Secretary of State Marco Rubio to begin work on establishing what these will look like. They could range from US boots on the ground (the best outcome for Ukraine, but the least likely), to aerial and/or maritime patrols, to providing intelligence and logistical support for Ukraine and its allies.

- For the 'coalition of the willing' countries, there remains significant trepidation as to the prospect of a workable peace deal that works in Ukraine's interest. Both German Chancellor Friedrich Merz and French President Emmanuel Macron voiced backing for a ceasefire before Russian President Vladimir Putin meets with Ukraine's Volodymyr Zelenskyy (which could take place in two weeks).

- Following the 'coalition of the willing' call, the European Council will hold an extraordinary leaders' summit on the same topic. Set to take place at 07:00ET/12:00BST/13:00CET.

SECURITY: Russia Foreign Minister Vague On Trump-Backed Putin-Zelenskyy Meeting

Speaking to Russia-24 TV, Foreign Minister Sergey Lavrov says that "Russia does not reject any formats to discuss the peace process in Ukraine", but adds "any contacts of [national] leaders should be prepared thoroughly," hardly a firm commitment to talks taking place. Lavrov's comments come after the high-profile White House summit where leaders, including US President Donald Trump, called for a meeting between Russian President Vladimir Putin and Zelenskyy.

- Trump confirmed on Truth Social that he had called Putin and "began the arrangements for a meeting, at a location to be determined, between President Putin and President Zelenskyy. After that meeting takes place, we will have a Trilat, which would be the two Presidents, plus myself."

- Lavrov went on to praise Trump's stance towards only focusing on a permanent peace deal. Ukraine and its European allies have called for a ceasefire before full peace talks get underway, but Russia and Trump have gone the other way. Trump claims ceasefires often "do not hold up", and Russia is likely to view the different viewpoints as an opportunity to drive a wedge between the US, and Ukraine/Europe.

- Lavrov said that "[Russia] have never talked about simply seizing some territories. Neither Crimea, nor Donbass, nor Novorossiya as territories have ever been our goal." Instead, he claimed the war is about protecting Russian speakers. The minister also claims that Trump has "taken a much deeper approach to resolving this crisis, understanding that it is necessary to eliminate the root causes," referring to NATO's expansion.

UK DATA: Retail sales delay due to "further quality assurance needed"

- The ONS has said the retail sales delay is due to "further quality assurance needed".

- This is the latest in a series of ONS delays to data releases (with PPI data still not being released monthly, trade data having to be corrected recently etc too)

- Link here: https://www.ons.gov.uk/releases/retailsalesgreatbritainjuly2025#changestothisreleasedate

FOREX: Coalition of the Willing Set to Discuss Structure of Security Guarantees

- Follows yesterday's drift into the Monday close, EUR/USD is higher early Tuesday, but the recent range is being largely respected. Near-term focus remains on the tentative progress made at the meeting between President Trump, European leaders and Ukraine's Zelenskyy in the Oval Office yesterday. The so-called 'coalition of the willing' is now due to be holding conferences later today, at which the topic of security guarantees is highly likely to be discussed. The shape and structure of these guarantees could have a material impact on the sustainability of any peace deal or ceasefire.

- Following yesterday's sharp gains for the UK yield curve, GBP still appears fragile. GBPUSD has pulled back from its latest highs but a bull cycle remains intact. Recent gains resulted in a breach of resistance at 1.3589, the Jul 24 high. Sights are on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1.

- The Canadian inflation print is set for release later today, at which markets expect core CPI to tick higher on a trimmed mean basis to 3.1% from 3.0% - a release that should again feed into the October rate decision pricing - which currently sits close to 50/50 on the potential for a 25bps cut. Ahead of the print, USD/CAD remains toward the top-end of the recent range, with the 1.3831 level the short-term bull trigger. Clearance here puts the price at the best level since early August.

- Outside of the Canadian inflation print, US housing starts and building permits are due for release. Fed's Bowman is set to speak again, with broader focus still on Powell's appearance at Jackson Hole later in the week.

OPTIONS: Expiries for Aug19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E731mln), $1.1620-25(E2.3bln), $1.1650-65(E682mln), $1.1700(E1.3bln)

- USD/JPY: Y148.30-35($709mln)

- AUD/USD: $0.6515(A$745mln)

- USD/CAD: C$1.3750-70($646mln)

EQUITIES: Eurostoxx 50 Futures Remain Close to Recent Highs

- A bullish theme in Eurostoxx 50 futures remains intact and the contract is trading closer to its latest highs. The print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies remain in a bull-mode position, highlighting an uptrend. Support to watch lies at 5349.70, the 50-day EMA.

- The dominant uptrend in S&P E-Minis remains intact and the contract is trading at its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6399.62, the 20-day EMA, and 6275.78, the 50-day EMA.

COMMODITIES: Moving Average Studies for Gold Remain in Bull-Mode Position

- WTI futures remain in a clear bear cycle and the contract is trading closer to its recent lows. A key support at $61.99, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $64.00, the 50-day EMA.

- A bull cycle in Gold remains intact and this is highlighted by moving average studies that remain in a bull-mode position. The sideways trend that has been in place since the Apr peak appears to be a corrective phase - a pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 19/08/2025 | 1230/0830 | *** | CPI | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 19/08/2025 | 1810/1410 | Fed Vice Chair Michelle Bowman | ||

| 20/08/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 20/08/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 20/08/2025 | 2350/0850 | * | Machinery orders | |

| 20/08/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 20/08/2025 | 0600/0700 | *** | Consumer inflation report | |

| 20/08/2025 | 0600/0800 | ** | PPI | |

| 20/08/2025 | 0710/0910 | ECB Lagarde at WEF Intl Business Council | ||

| 20/08/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 20/08/2025 | 0900/1100 | *** | HICP (f) | |

| 20/08/2025 | 0900/1100 | Q2 Flash Vacancies and Labour Cost Index | ||

| 20/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 20/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 20/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 20/08/2025 | 1500/1100 | Fed Governor Christopher Waller | ||

| 20/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 20/08/2025 | 1800/1400 | FOMC Minutes | ||

| 20/08/2025 | 1900/1500 | Atlanta Fed's Raphael Bostic |