MNI US MARKETS ANALYSIS - Risk Surges on Tariff Cut Pledge

Highlights:

- Risk surges as US-China pledge hefty tariff cuts as prelude to trade talks

- USD on track for best session of the year, but strong resistance ahead

- BoE watchers conference sees tariff threat as secondary driver to inflation for rate cut votes

US TSYS: Heavy Bear Flattening On Temporary US-China Tariff Reductions

- Treasuries are firmly lower as signs of constructive US-China trade talks over the weekend were followed by tangible progress today in headlines at ~0300ET on US tariffs on China being cut from 145% to 30% and China tariffs on US from 125% to 10% for a 90-day period.

- Cash yields are 3-12bp higher, with increases led by 3s and with 30s lagging heavily.

- Some notable flow aiding the flattening: 13.9k TUM5 blocked at 103-10.375, suggested seller with the contract bid at 103-11.125 at the time the block was lodged (DV01 ~506K).

- 2s10s trades at 44.7bp (-4.2bp) off an intraday low of 42.4bp that was the lowest since Apr 10 (the day after the reciprocal tariff 90-day pause).

- 5s30s trades at 75bp (-7.3bp) vs Friday’s high of 89bp and May 1 highs of 100bp.

- TYM5 has recently set fresh session lows of 110-04+ (-21+) on solid overnight volumes of 565k.

- The extension of the reversal that started May 1 sees next support come into play at 110-01+ (76.4% retrace of Apr 11 – May 1 bull leg) after which lies a key 109-08 (Apr 24 low). To the upside, resistance at 111-08 (20-day EMA).

- Data: Federal budget balance Apr (1400ET)

- Fedspeak: Gov. Kugler on economic outlook (1025ET) - see broader Fedspeak context in STIR bullet.

- Bill issuance: US Tsy $76B 13W & $68B 26W Bill auctions (1130ET)

STIR: Next Cut In July Now Seen As 50/50 After US-China Progress

- Fed Funds implied rates are sharply higher on US-China trade headlines, with a next cut in July now seen as a 50/50 call and the Dec 2025 rate 10bp higher from Friday’s close.

- Signs of constructive US-China trade talks over the weekend were followed by tangible progress today in headlines at ~0300ET on US tariffs on China being cut from 145% to 30% and China tariffs on US from 125% to 10% for a 90-day period.

- Cumulative cuts from 4.33% effective: 3bp Jun, 12.5bp Jul, 28.5bp Sep, 41bp Oct and 56bp Dec.

- The 56bp of cuts for 2025 is the least priced since shortly ahead of the FOMC decision on Mar 19 and before that late Feb, i.e. now well before the initial Apr 2 Liberation Day reciprocal tariff announcements.

- The SOFR implied terminal yield meanwhile is 17.5bp higher from Friday’s close at 3.43% (SFRZ6) for now 3.5bp above Apr 2 announcement levels. This was sub-2.9% before ISM mfg as recently as May 1.

- Further Fedspeak ahead from Gov. Kugler (permanent voter) on the economic outlook at 1025ET. She spoke on Friday, saying the US is most likely close to maximum employment. A slew of other Fedspeak fresh from the FOMC blackout reiterated the need for patience amidst huge uncertainty (see a recap of last week’s heavy Fedspeak from pg 7 in the MNI Macro Weekly here)

FOREX: How Significant is Today's Move in the Greenback?

- A close at current or higher levels for the USD Index would mark the strongest one-day return since early April - which was the strongest session of 2025 so far. The rate is now facing meaningful resistance at 101.855 - the 50-day EMA, a level which helped cap a recovery rally in February, and provided support through Trump's inauguration.

- Clearance here would make today's move far more meaningful. The market is currently maintaining a net short USD Index position for the first time since the election last year, and further S/T gains here could prompt a reassessment of the aggressive trim of USD exposure since March, and establish a base for the Greenback.

- The reversal is certainly being borne out by equities. The much-publicized rally in the e-mini S&P is being outstripped by small-caps in the Russell 2000 - which is geared to open higher by as much as 4.5% at today's open - and may better reflect heightened optimism in a domestic US recovery.

- It's the endorsement of STIR markets that could add extra support here - we see a next cut in July now seen as a 50/50 call and the Dec 2025 rate 10bp higher from Friday's close. A further pullback in cut pricing and a break of key resistance in the USD Index would make today's move more meaningful.

US TSY FUTURES: Mix Of Positioning Swings Seen Friday, Exposure Added In Wings

OI data points to a mix of net long setting (TU), short cover (FV & TY) and short setting (US & WN) as the curve twist steepened on Friday.

- The addition of exposure in the wings outweighed any cover seen in the belly/intermediates.

| 09-May-25 | 08-May-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,094,163 | 4,070,176 | +23,987 | +870,564 |

FV | 6,852,906 | 6,870,988 | -18,082 | -765,878 |

TY | 4,941,162 | 4,964,960 | -23,798 | -1,494,543 |

UXY | 2,287,901 | 2,282,109 | +5,792 | +503,858 |

US | 1,816,658 | 1,802,151 | +14,507 | +1,820,132 |

WN | 1,886,352 | 1,881,713 | +4,639 | +841,348 |

|

| Total | +7,045 | +1,775,481 |

STIR: Modest Positioning Swings In SOFR On Friday

OI data points to net long setting and short cover in some SOFR futures on Friday, although the net OI changes were only modest and some contracts finished unchanged, which muddies the inference a little.

| 09-May-25 | 08-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,102,155 | 1,101,663 | +492 | Whites | -5,912 |

SFRM5 | 1,220,129 | 1,224,620 | -4,491 | Reds | -2,667 |

SFRU5 | 994,156 | 990,809 | +3,347 | Greens | +2,722 |

SFRZ5 | 1,091,628 | 1,096,888 | -5,260 | Blues | +2,656 |

SFRH6 | 757,810 | 758,421 | -611 |

|

|

SFRM6 | 741,591 | 739,807 | +1,784 |

|

|

SFRU6 | 727,795 | 726,615 | +1,180 |

|

|

SFRZ6 | 837,222 | 842,242 | -5,020 |

|

|

SFRH7 | 665,326 | 664,752 | +574 |

|

|

SFRM7 | 569,243 | 565,226 | +4,017 |

|

|

SFRU7 | 368,219 | 367,103 | +1,116 |

|

|

SFRZ7 | 397,457 | 400,442 | -2,985 |

|

|

SFRH8 | 276,259 | 278,762 | -2,503 |

|

|

SFRM8 | 187,995 | 191,064 | -3,069 |

|

|

SFRU8 | 159,239 | 152,800 | +6,439 |

|

|

SFRZ8 | 165,561 | 163,772 | +1,789 |

|

|

US TSY FUTURES: CFTC Shows Asset Managers Adding To Longs, Funds Increase Shorts

The latest CFTC CoT report pointed to continued extension of exposure for both asset managers and leveraged funds through May 6.

- The former extended their net long position by ~$11mln in DV01 equivalent terms, as they added to longs in FV through US futures, while they trimmed lightened long exposure in TU & WN contracts.

- Meanwhile, leveraged funds added ~$20.4mln DV01 equivalent across the curve, only trimming short exposure in TU futures. Note that they added ~$13mln DV01 equivalent of fresh net shorts in TY futures alone.

- Broader non-commercial net positioning remains net short across the curve.

Source: MNI - Market News/CFTC/Blooomberg

EGBS: Japanese Investors Continued To Shun OATs As Of March

Japanese investors continued to shun OATs as of March 2025, with balance of payments data (released overnight) pointing to a net JPY377bln of French sovereign bond selling. Japanese investors have sold a cumulative net JPY4trln of OATs since the start of 2024, spurred by the political and fiscal uncertainty stemming from President Macron’s snap general election announcement in June.

- The April BoP data will reveal whether Japanese investors re-allocated into French sovereign debt following the US “Liberation Day” announcement and associated market fallout, given the good liquidity the OAT market offers.

- However, political and risk risks remain present in France. Although a gradual consolidation of public finances is intact, officials have still highlighted the need to find E40bln of savings to meet the 4.6% 2026 budget deficit target. Meanwhile, our Political Risk team wrote last month that PM Bayrou is under significant political pressure amid an ongoing domestic scandal (see here).

- These risks are important to monitor, because President Macron is legally able to call another general election in July 2025 if desired (new elections cannot be held within 12-months of the last round). Such an announcement would see French political uncertainty ratchet higher once again, and drag on OAT performance versus peers.

- In March, Japanese investors were net buyers of JPY217bln of German sovereign debt and JPY109bln of Italian debt. The German figure may represent investor dip-buying, after yields rose notably in reaction to Merz’s defence/infrastructure spending announcement at the start of the month.

BOE: Greene: Tariffs were a factor in Greene's May vote to cut 25bp

"I think on net, tariffs will probably be disinflationary for the UK economy, and that was a factor in determining my most recent decision to cut bank rate by 25 basis points. So there are some inflationary factors. I think on net, there are more disinflationary ones. They'll all hit the economy at different times. But that's certainly a risk that I'm looking at."

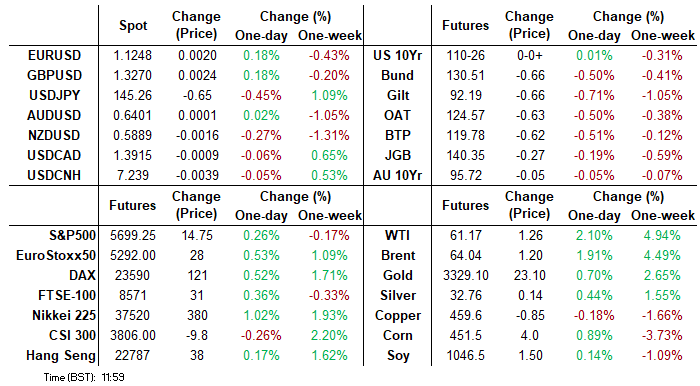

FOREX: EUR Slides, USD/JPY Gets Jolt in the Arm on Trade Talks

- USD/JPY got a jolt in the arm early Monday as the US and China trade negotiation teams confirmed an aggressive cut to trade tariffs. While the drop in tariffs is only entering a 90-day pause, markets are taking the step as a strong sign of intent that both sides want to maintain as healthy a trade relationship as possible - helping stimulate strong equity, USD and CNH gains.

- This leaves JPY comfortavly the poorest performing currency in G10 as the US/China headlines on reducing tariffs have significantly boosted risk sentiment across global markets. The yen's negative correlation to moves in equity markets has been in prime focus, with the hawkish repricing in core fixed income providing an additional headwind for the low yielders. Broad US dollar strength has translated into a sharp adjustment higher for USDJPY, exacerbated by a clean break of the 50-day EMA resistance that had capped the price action last week.

- Similarly, EUR is sliding. Having been one of the stronger currencies through trade tumult on relative haven status as well as the EU's perceived library of counter-tariff measures, the EUR is now performing poorly as while countries including the UK, Switzerland and China have taken notable steps toward a cleaner tariff regime, there are few signs of progress with Brussels.

- A BoE watcher conference will be carefully watched today, with appearances from BoE's Greene, Mann and Taylor still set to speak. Fed's Kugler similarly talks on the US economic outlook.

CROSS ASSET: Risk Surges as US/China Slash Tariffs for 90 Days

The US and China are to cut reciprocal tariffs for 90 days, with China to lower tariffs on US goods to 10% from 125%, and the US to cut tariffs on Chinese goods to 30% from 145% over the same period. Bessent is now conducting a press briefing, talking through the "great respect" between the two countries.

Risk surges on the US/China trade headline, with the USD popping to session highs, outdone only by the CNH, with USD/CNH pressing to new daily lows. This USD/JPY rally is meaningful - the pair is now through the 50-dma resistance and at new one-month highs. Equities rally in tamdem: e-mini S&P testing the 100-dma of 5837.75, hasn't been topped since February.

- TY to fresh session lows of 110-08+, seeing a clean break through support at the April 22 low (110-16+). Fibonacci support now eyed (110-01+). 10-Year yield to the highest level seen since early April (4.445%), although the April high is still ~15bp above prevailing levels (4.586%).

EQUITIES: E-Mini S&P Pierces Key Resistance and Bull Trigger at $5837.25

- Strong gains in Eurostoxx 50 futures contract today reinforce current bullish conditions. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial support to watch lies at 5127.08, the 20-day EMA. Clearance of this level would signal a possible reversal.

- The bullish trend condition in S&P E-Minis remains intact and today’s strong start to this week’s session reinforces bullish conditions. The contract has pierced an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the current bullish theme, paving the way for a continuation near-term. Sights are on 5896.25, a Fibonacci retracement. Initial firm support to watch lies at 5628.71, the 50-day EMA.

COMMODITIES: WTI Futures Approaching Key Short-Term Resistance at 50-Day EMA

- A downtrend in WTI futures remains intact and short-term gains are considered corrective. The corrective cycle remains in play for now and price has traded through the 20-day EMA. Key short-term resistance to watch is $63.62, the 50-day EMA, a clear break of this level would highlight a stronger reversal. For bears a reversal lower would refocus attention on $54.67, the Apr 9 low and bear trigger.

- The latest pullback in Gold appears corrective. The primary trend condition is bullish and a resumption of the uptrend would signal scope for a climb towards the bull trigger at $3500.1, the Apr 22 high. Clearance of this level would confirm a resumption of the uptrend. Key short-term support has been defined at $3202.0, the May 1 low. A clear break of this level is required to signal scope for a deeper retracement.

| Date | GMT/Local | Impact | Country | Event |

| 12/05/2025 | - | ECB's Cipollone At Eurogroup Meeting | ||

| 12/05/2025 | 1250/1350 | BOE Mann On Neutral Rate Of Interest | ||

| 12/05/2025 | 1425/1025 | Fed Governor Adriana Kugler | ||

| 12/05/2025 | 1430/1530 | DMO likely to publish FQ2 consultation agenda | ||

| 12/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 12/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 12/05/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/05/2025 | 1600/1700 | BOE Taylor Fireside Chat With Ed Balls | ||

| 12/05/2025 | 1800/1400 | ** | Treasury Budget | |

| 13/05/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 13/05/2025 | 0600/0700 | *** | Labour Market Survey | |

| 13/05/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 13/05/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 13/05/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 13/05/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 13/05/2025 | - | *** | Money Supply | |

| 13/05/2025 | - | *** | New Loans | |

| 13/05/2025 | - | *** | Social Financing | |

| 13/05/2025 | - | ECB's De Guindos At ECOFIN Meeting | ||

| 13/05/2025 | 1230/0830 | *** | CPI | |

| 13/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 13/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill |