MNI US MARKETS ANALYSIS - Political Fragility Returns

Highlights:

- Market fragility returns as German politics becomes unsettled

- Bessent set to testify later today, with 10y supply to follow

- APAC FX remains volatile, Hong Kong intervene for a third session

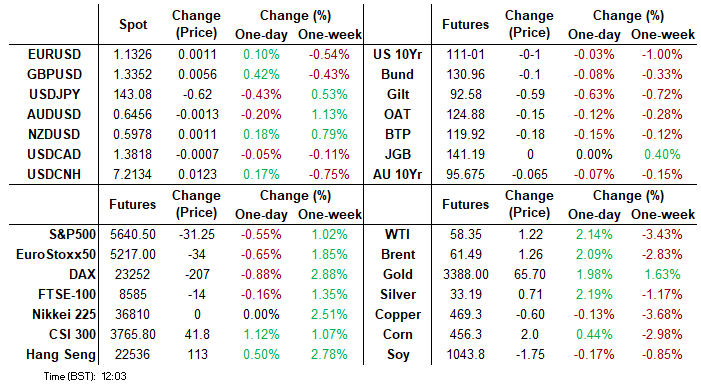

US TSYS: TYA Extended Support Clearance Overnight, Bessent and 10Y Supply Ahead

- Treasuries are relatively little changed on thin volumes after another late open for cash markets (Japan today after Japan and London yesterday), broadly consolidating sizeable sell-offs seen since Thursday’s ISM manufacturing report.

- Today sees focus on Tsy Sec Bessent testifying to a House hearing at 1000ET before 10Y supply at 1300ET.

- Recall that last month’s 10Y auction helped stabilize particularly fraught markets, stopping through by more than 3bps and with an all-time high for indirect take-up (87.9%) having been watched closely as a proxy for foreign demand for Treasuries.

- Whilst looking at data that is increasingly in the rearview, today’s final trade data can also have implications for how we assess trade developments prior to April’s reciprocal policies.

- Cash yields are 1.2bp higher (2s) to 0.3bp lower (7s).

- TYM5 at 111-01 (-01) trades within overnight ranges on particularly low volumes of 200k.

- An overnight low of 110-27+ extended yesterday’s clearance of support at 110-30+ (50-day EMA) with a clear breach potentially strengthening a bearish threat to expose 110-16+ (Apr 22 low). To the upside, resistance at 112-01+ (Mar 2 high).

- Data: Trade balance Mar (0830ET)

- Coupon issuance: US Tsy $42B 10Y Note auction - 91282CNC1 (1300ET)

- Bill issuance: US Tsy $70B 6W bill auction (1130ET)

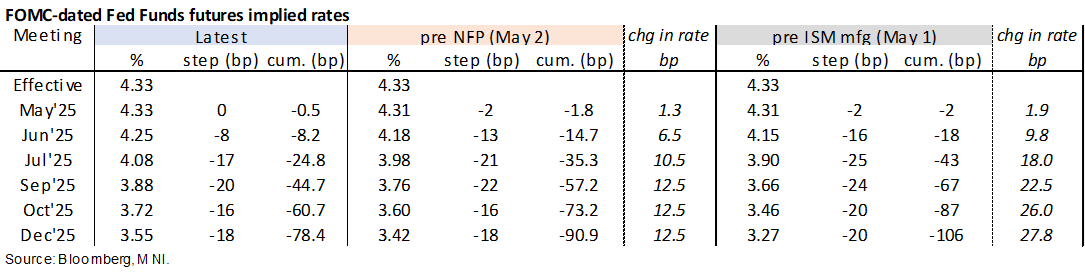

STIR: US Rates Holding Bulk Of Recent Hawkish Shift

- Fed Funds implied rates are 0-2.5bp lower on the day as they give back some of yesterday’s increase on ISM Services although are still biased increasingly higher on pre-ISM Services levels as you look later into the year.

- Cumulative cuts from 4.33% effective: Just 0.5bp for tomorrow’s decision, 8bp Jun, 25bp Jul, 45bp Sep and 78bp Dec.

- Yesterday saw sub-75bp of cuts for for 2025 for fresh recent hawkish extremes. There were fewer cuts priced briefly after the reciprocal tariff ‘pause’ on Apr 9 and before that prior to the Apr 2 initial Liberation Day announcements.

- SOFR implied terminal yields are 2bp lower overnight at 3.17% (SFRU6) for 22.5bp below pre-Apr 2 levels having removed 29bp of cuts since Thursday’s ISM manufacturing survey.

- It’s a quiet docket today, with data headlined by the full release for the trade balance (providing into important details and volumes), increasing focus on Tsy Sec Bessent testifying to the House at 1000ET.

- Tomorrow’s FOMC decision also looms large – MNI Fed Preview here.

GERMANY: Vote Defeat Scuppers Merz Plan For Early Meetings In France & Poland

Defeat for chancellor candidate Friedrich Merz in the first round of voting in the Bundestag is set to scupper his initial plans to travel to Paris and Warsaw in the coming days, in a trip that was viewed as demonstrating Merz's foreign policy priorities amid high tensions with the US over trade and support for Ukraine. Instead, the 'grand coalition' parties will be locked in crisis talks seeking a resolution that could bring about an overall majority for Merz in the Bundestag.

- There has been a flurry of reporting on when the next ballot could take place. The prospect of a second vote taking place today (6 May) is now seen as small, with some reporters claiming Friday 9 May as the most likely day, although tomorrow (7 May) is also an option. ARD reports comments from CSU General Secretary Carsten Linnemann claiming that the latest they want the vote is Wednesday.

- Commerzbank: "...the result of today's vote serves as a reminder of how narrow the majority of the new coalition is, which further dampens hopes for sweeping economic reforms."

- Berenberg: "Merz will most likely still be elected as chancellor in the end. But even so, the unprecedented failure to be elected in the first round would still be a bad start for him. It shows that he cannot fully rely on his two coalition parties. That will sow some doubts about his ability to fully pursue his agenda, damaging his domestic and international authority at least initially."

UK: Gov't Might Waver On Winter Fuel Payment Cut After Local Election Losses

Comments from Health Secretary Wes Streeting have added to speculation that the gov't could water down, or even fully reverse, its cuts to winter fuel payments for pensioners not in receipt of certain benefits. The Guardian reported on 5 May that the gov't is "rethinking its controversial winter fuel payment cut amid growing anxiety at the top of government that the policy could wreak serious electoral damage". Speaking to the BBC, Streeting denied that the policy is under formal review, but acknowledged that they are "reflecting on what the voters told us".

- In the 1 May local council elections, the governing centre-left Labour party lost around two-thirds of the seats it was defending. The main winner was the right-wing populist Reform UK, while the centrist Liberal Democrats also performed well. Considering that the last time the councils were contested was 2021, when the centre-right Conservatives made significant gains as the COVID vaccine was rolled out, Labour's underperformance on 1 May becomes even starker.

- In an effort to save an estimated GBP1.4bln, Chancellor of the Exchequer Rachel Reeves announced the restriction in payments to those in receipt of pension credit and other benefits related to income.

- It is unclear whether a U-turn would be enough to revive Labour's flagging support, while it might also contribute to market jitters regarding Labour's commitment to its fiscal rules (note: Streeting said earlier the gov't was committed to the fiscal rules as-is)

Chart 1. Government Approval Ratings, %

Source: YouGov. Latest data 3-5 May

FOREX: Fragility Returns, Pointing to Negative Open on Wall Street

- Equity markets globally are softer, with US futures on the backfood and pointing to a lower open on Wall Street later today. Markets trade with a risk-off feel as further signs of fragility begin to show in global markets. EUR/RON has spiked as much as 2% on local political uncertainty, the Hong Kong Monetary Authority are to diversify their FX holdings away from USD-denominated assets and Germany's Merz has faltered in his first step toward taking the Chancellery, as he fails to pass a first vote in parliament.

- As a result, the JPY is firmer against all others in G10 FX, with USD/JPY through yesterday's lows and only finding support at 142.90, the 50% retracement for the upleg posted off the April pullback low. Clearance through here will shift focus again to recent lows - with 139.89 the real bear trigger.

- AUD is the poorest performer in G10 as the currency retraces a small part of the election-triggered rally from Monday. The risk-off feel for markets will also be hampering the currency.

- Lastly, CHF underperforms - breaking the correlation with JPY as SNB's Schlegel talks up the possibility of negative rates again in the future should the economic situation warrant it.

- US and Canadian trade balance data mark the key releases for Tuesday trade, with the central bank speaker slate empty - the Fed remain inside their pre-decision media blackout period ahead of tomorrow's rate decision.

HONG KONG: HKMA Diversifies Away From USD, Reduces UST Duration in Holdings

HKMA chief Eddie Yue states that the HKMA Exchange Fund has been reducing duration in UST holdings, and has been diversifying into non-US assets. They also note they've been diversifying their FX exposure across the investment portfolio in order to manage risks.

HKMA's Exchange Fund holds assets totalling HKD 4trl ($525bln) as of end-2024, of which over half is 'Debt Securities', in which USTs would likely be the bulk of the category. HKMA's Exchange Fund has an objective of ensuring the "entire Monetary Base, at all times, is fully backed by highly liquid US dollar-denominated assets" as well as ensuring "sufficient liquidity for the purpose of maintaining monetary and financial stability".

- As such, any shifts to the duration of their UST holdings is likely made to keep HKMA's investment objectives on track, particularly as the USD/HKD trading band errs toward the strong-side - triggering HKD selling by the HKMA on both Friday and Monday.

US TSY FUTURES: Net Short Setting Seen In TY Futures On Monday

OI data points to a mix of net short setting (TY, US & WN) and long cover (FV & UXY) during Monday’s bear steepening of the Tsy curve.

- The only real positioning swing of note came via the apparent net short setting in TY futures, which titled the curve-wide positioning move in that direction.

| 05-May-25 | 02-May-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,072,896 | 4,071,317 | +1,579 | +58,013 |

FV | 6,910,288 | 6,913,100 | -2,812 | -120,431 |

TY | 4,960,597 | 4,931,083 | +29,514 | +1,898,593 |

UXY | 2,290,522 | 2,297,273 | -6,751 | -592,330 |

US | 1,784,206 | 1,781,930 | +2,276 | +287,243 |

WN | 1,887,381 | 1,884,433 | +2,948 | +536,669 |

|

| Total | +26,754 | +2,067,756 |

STIR: Exposure Built In Most SOFR Contracts On Monday

OI data points to a mix of net long and short setting through the SOFR greens on Monday, before net long cover came to the fore in the blues.

- SOFR futures were -3.5 to +1.5 come settlement.

| 05-May-25 | 02-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,080,637 | 1,077,781 | +2,856 | Whites | +40,223 |

SFRM5 | 1,253,073 | 1,250,241 | +2,832 | Reds | +23,112 |

SFRU5 | 1,004,235 | 986,929 | +17,306 | Greens | +7,611 |

SFRZ5 | 1,076,332 | 1,059,103 | +17,229 | Blues | -4,783 |

SFRH6 | 748,954 | 735,052 | +13,902 |

|

|

SFRM6 | 721,691 | 719,376 | +2,315 |

|

|

SFRU6 | 701,188 | 696,521 | +4,667 |

|

|

SFRZ6 | 856,627 | 854,399 | +2,228 |

|

|

SFRH7 | 667,611 | 665,267 | +2,344 |

|

|

SFRM7 | 551,371 | 548,856 | +2,515 |

|

|

SFRU7 | 361,800 | 361,694 | +106 |

|

|

SFRZ7 | 398,483 | 395,837 | +2,646 |

|

|

SFRH8 | 277,418 | 279,300 | -1,882 |

|

|

SFRM8 | 194,183 | 195,341 | -1,158 |

|

|

SFRU8 | 153,413 | 154,585 | -1,172 |

|

|

SFRZ8 | 164,928 | 165,499 | -571 |

|

|

OPTIONS: Expiries for May06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1275(E508mln), $1.1325(E717mln), $1.1400(E632mln), $1.1500-10(E2.2bln)

- GBP/USD: $1.2980-90(Gbp545mln)

- USD/JPY: Y142.00($1.1bln), Y144.50-55($638mln), Y146.00($1.9bln)

- EUR/GBP: Gbp0.8500-05(E535mln)

- AUD/USD: $0.6300(A$813mln), $0.6500(A$702mln)

- USD/CAD: C$1.3815-30($874mln)

- USD/CNY: Cny7.3000($1.5bln)

EQUITIES: Eurostoxx 50 Futures Holding Onto Latest Gains

- Eurostoxx 50 futures maintain a positive tone and the contract is holding on to its latest gains. Price has recently cleared both the 20- and 50-day EMAs, and attention is on 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. It has been pierced, a clear break of it would pave the way for a climb towards 5341.00, the Mar 27 high. Initial support to watch lies at 5067.15, the 20-day EMA. Clearance of this level would signal a possible reversal.

- The latest recovery in the e-mini S&P reinforces current bullish conditions.The contract has breached the 50-day EMA, at 5622.87. A continuation of the bull phase would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low.

COMMODITIES: Short-Term Gains for WTI Futures Considered Technically Corrective

- A medium-term bearish trend in WTI futures remains intact and short-term gains are considered corrective. The move down that started Apr 23 signals the end of the correction between Apr 9 - 23. That cycle higher allowed an oversold condition to unwind. Attention is on $54.67, the Apr 9 low and a bear trigger. Clearance of this level would resume the downtrend and open $53.72, a Fibonacci projection. Resistance to watch is $64.32, the 50-day EMA.

- Gold has recovered from its recent lows and this suggests the correction between Apr 22 - May 1, is over. A continuation higher would refocus attention on key resistance and the bull trigger at $3500.1, the Apr 22 high. Clearance of this level would confirm a resumption of the primary uptrend. Key short-term support has been defined at $3202.0, the May 1 low. A break of this level is required to signal scope for a deeper retracement.

| Date | GMT/Local | Impact | Country | Event |

| 06/05/2025 | - | FOMC Meeting | ||

| 06/05/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 06/05/2025 | 1230/0830 | ** | Trade Balance | |

| 06/05/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 06/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 06/05/2025 | 1400/1000 | * | Ivey PMI | |

| 06/05/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 07/05/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 07/05/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 07/05/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/05/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/05/2025 | 0645/0845 | * | Foreign Trade | |

| 07/05/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 07/05/2025 | 0800/1000 | * | Retail Sales | |

| 07/05/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 07/05/2025 | 0900/1100 | ** | Retail Sales | |

| 07/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 07/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 07/05/2025 | 1400/1000 | Treasury Secretary Scott Bessent | ||

| 07/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/05/2025 | 1800/1400 | *** | FOMC Statement | |

| 07/05/2025 | 1900/1500 | * | Consumer Credit |