MNI US MARKETS ANALYSIS - Kyiv Sees Little Hope in RU-US Meet

Highlights:

- Trump's deal with Putin a work-in-progress, but finds poor reception in Kyiv

- NOK on top as CPI restrains Norges Bank room to ease policy

- POTUS press conference today set to focus on law enforcement

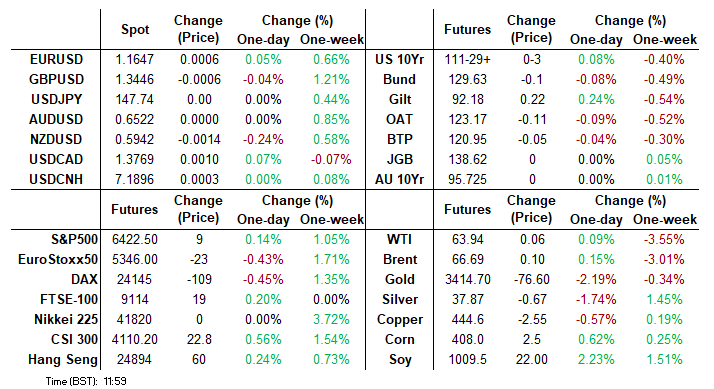

US TSYS: Summer Overnight Volumes, Trump Press Conference Headlines Docket

- Treasuries are mildly firmer after a late open with a Japan holiday, with benchmark tenors within Friday’s range.

- They see mixed European spillover, with Gilts outperforming as they retrace losses last week whilst EGBs underperform.

- With such a quiet docket, expect headlines/flow to dominate proceedings with tomorrow’s CPI report looming large.

- Today’s main scheduled event is President Trump’s press conference at 1000ET, with the focus set to be on law enforcement in the District of Columbia but always with scope for discussions on wide-ranging topics.

- Some areas worth watching: White House administration to issue an executive order clarifying gold tariffs in “the near future”, announcement of the new BLS commissioner due after Trump fired McEntarfer after the weak July payrolls report, and geopol-related headlines ahead of Friday’s Trump-Putin meeting in Alaska.

- Cash yields are 1-5-2bp lower from Friday’s close.

- TYU5 trades at 11-29+ (+03) on extremely thin cumulative volumes of 145k. It holds its ground, with resistance seen at 112-15+ (Aug 5 high) and support at 110-19+ (Jul 24 low).

- Data: None scheduled

- Fedspeak: None scheduled

- Bill issuance: US Tsy to sell $82B 13-W, $73B 26-W bills (1130ET)

- Politics: Trump press conference on law enforcement (1000ET)

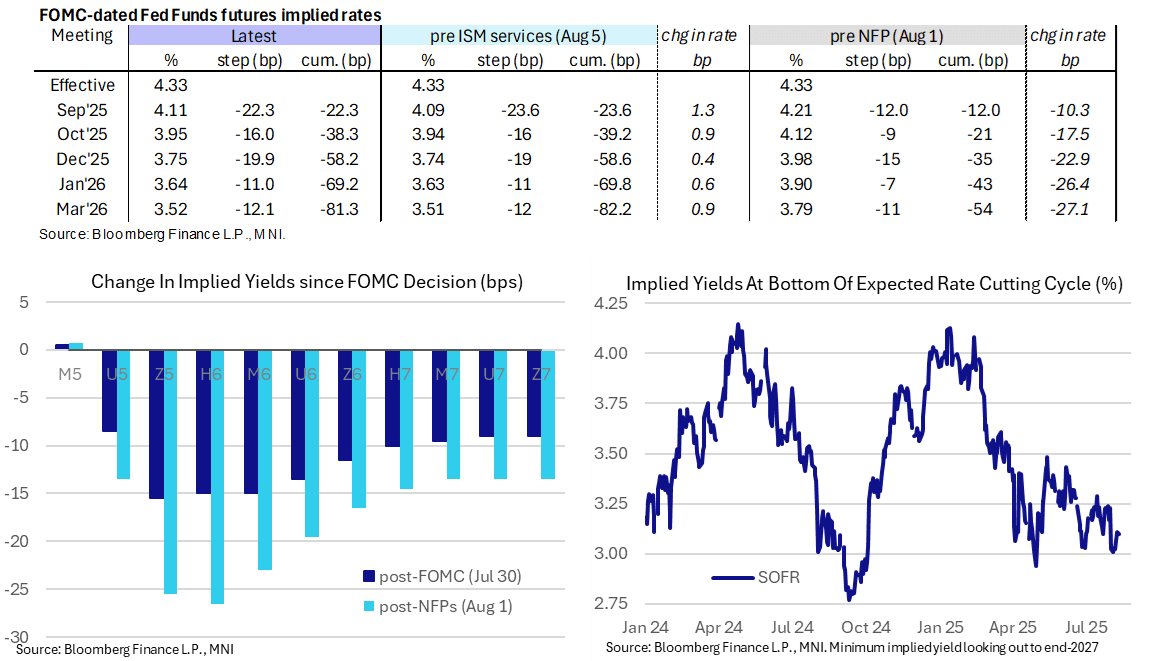

STIR: Fed Rate Path Treading Water With Tomorrow’s CPI Eyed

- Fed Funds implied rates for near-term meetings hold Friday’s drift higher ahead of a particularly thin docket with focus firmly on tomorrow’s CPI report.

- Cumulative cuts from 4.33% effective: 22.5bp Sep, 38.5bp Oct, 58bp Dec, 69bp Jan and 81.5bp Mar.

- The SOFR implied terminal yield of 3.10% (SFRH7) is 1bp lower after Friday’s 3.11% marked the highest since the July NFP report. It has recently ticked to just under five cuts priced from current levels.

- There is no notable data or Fedspeak scheduled today. Barkin (non-voter) and Schmid (’25 voter, hawk) are next of the scheduled FOMC speakers, both coming after CPI tomorrow.

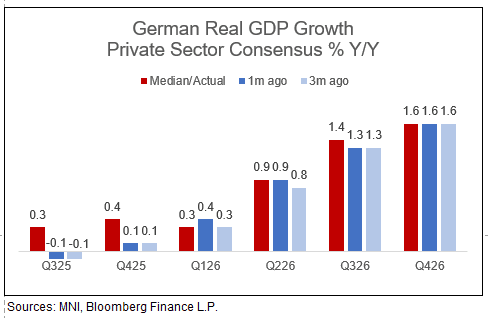

MACRO UPDATE: Analysts' German Growth Projections Picking Up

Revisions to consensus on German GDP during the last months swayed towards growth being a bit more pronounced on a Y/Y basis in the coming quarters than seen previously. The chart below shows growth estimates (from seven primary dealer analysts via Bloomberg) for Q3 / Q426 stand higher than where they were one (and also three) months ago. Growth then continues to be expected to pick up towards 2026, with a similar pace as before.

- However, note that these forecast updates came after the Q2 Destatis GDP print seeing an inline Q/Q reading (of -0.1%) but a higher-than-expected Y/Y print (of 0.4% vs 0.2% cons) amid some partially notable revisions of the prior GDP data. This may well have had an influence on analysts' projections for the quarters ahead.

- From a fundamental perspective, the analyst updates came following the US-EU trade deal, finance minister Klingbeil's presentation of the 2026 budget (amid his updated financial plan for 2027-29, recap here) as well as the reveal of the details of a private sector investment initiative in Germany.

- Revisions for both private investment and government spending in Germany appear materially unchanged over the last month (a contained pick-up of the private investment near-term f'cast stands out to some degree - now seen at 1.1% Y/Y in Q325). Net exports meanwhile are seen a little lower in the short term than before.

- Elsewhere, RBC today has published a report on fiscal stimulus in Germany, finding that "a high share of additional spending is going to go on 'high multiplier'" items - leading to their conclusion that "what we do know looks very promising for German growth" at least for 2025 and 2026. Beyond that, they see the effects to fade, though.

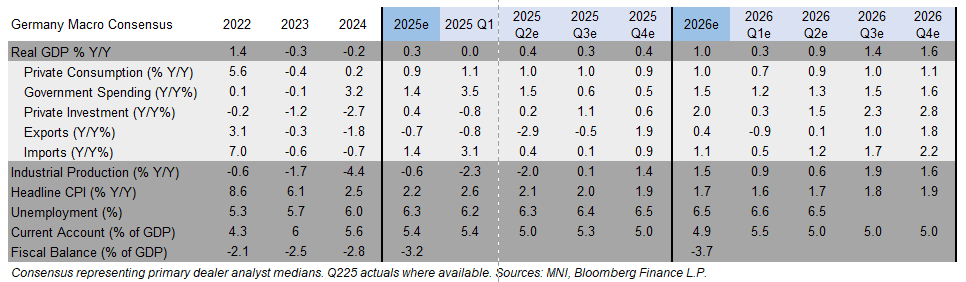

MACRO UPDATE: Private Sector Cons Sits Inbetween Government and IFO Projections

For an updated full view of private sector consensus on German economic indicators see below. Again, momentum to generally pick up over the coming quarters.

- Growth estimates for 2025 and 2026 stand at 0.3% Y/Y and 1.0% Y/Y, respectively. This would mean an end to the two-year contraction period which just passed, and does represent an improvement in sentiment over views for a potential third consecutive year of negative growth present ahead of the German fiscal stimulus announcement.

- For comparison, the German government continues to be more pessimistic than this, seeing flat real GDP (0.0% Y/Y) this year ahead of "around 1%" in 2026 in their forecast published late April. Note that this was before the current government took over in the economy ministry, which is responsible for the forecast. IFO institute meanwhile sees a stronger 0.3% in 2025 and 1.5% in 2026, citing "numerous indicators suggest that the crisis in the German economy reached its low point in the winter half-year 2024/2025" back in June.

SOFR: Net Short Setting Most Prominent In Futures On Friday

OI data points to a slight bias towards net short setting across much of the SOFR futures strip on Friday, with pockets of net long cover also seen.

- Note the only exception to those positioning swing directions came via apparent modest net short cover in the very front (SFRM5), with the strip twist steepening on the day.

| 08-Aug-25 | 07-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,217,076 | 1,217,307 | -231 | Whites | +7,877 |

SFRU5 | 1,270,461 | 1,267,584 | +2,877 | Reds | +6,903 |

SFRZ5 | 1,371,711 | 1,377,023 | -5,312 | Greens | +4,943 |

SFRH6 | 1,053,918 | 1,043,375 | +10,543 | Blues | +4,683 |

SFRM6 | 882,314 | 880,401 | +1,913 |

|

|

SFRU6 | 846,090 | 853,619 | -7,529 |

|

|

SFRZ6 | 958,518 | 959,038 | -520 |

|

|

SFRH7 | 732,776 | 719,737 | +13,039 |

|

|

SFRM7 | 803,435 | 798,891 | +4,544 |

|

|

SFRU7 | 580,107 | 579,235 | +872 |

|

|

SFRZ7 | 517,699 | 515,922 | +1,777 |

|

|

SFRH8 | 331,959 | 334,209 | -2,250 |

|

|

SFRM8 | 263,039 | 262,305 | +734 |

|

|

SFRU8 | 206,242 | 205,282 | +960 |

|

|

SFRZ8 | 219,525 | 216,743 | +2,782 |

|

|

SFRH9 | 152,941 | 152,734 | +207 |

|

|

US TSY FUTURES: OI Data Points To Low Conviction Trade On Friday

OI data points to fairly non-committal trade during Friday’s downtick, with a slight bias towards net long cover

| 08-Aug-25 | 07-Aug-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,572,846 | 4,576,293 | -3,447 | -125,693 |

FV | 7,035,359 | 7,051,471 | -16,112 | -686,029 |

TY | 5,156,048 | 5,139,598 | +16,450 | +1,083,807 |

UXY | 2,465,513 | 2,462,510 | +3,003 | +262,652 |

US | 1,772,004 | 1,775,201 | -3,197 | -447,205 |

WN | 1,997,589 | 1,999,098 | -1,509 | -275,200 |

|

| Total | -4,812 | -187,669 |

UK DATA: UK Labour Supply Growing "Sharply", Second Fastest Pace in Near 5 Years

- Ahead of tomorrow's headline labour market data, the release of the KPMG-REC Report on Jobs for July is also significant in providing any clue if a continually softening UK labour market - a necessity for another quarterly cut in November - is materializing.

- The report showed that the supply of labour continued to expand "sharply", with the rate softening only slightly from June for the second-fastest reading of that subcomponent since December 2020. Permanent placements meanwhile continue their "steep" decline due to "weak confidence around the economic outlook and greater pressure on budgets due to recent increases in payroll cost".

- Wage increases continued to remain on the softer side with the report noting that starting salary wage growth fell to its lowest level since March 2021.

- Vacancies also continued to fall, now at the fastest rate in three months in July.

- Overall, there is little in this report to provide any real positive signs. With the MPC continuing to place strong emphasis on the labour market (and non-headline ONS data) this is another dovish leaning report. Our preview of tomorrow's ONS data will be released later today.

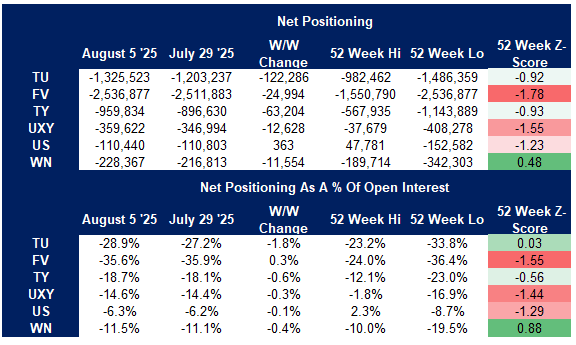

US TSY FUTURES: Swings In Long End Positioning Dominate Latest CFTC CoT

While headline adjustments in the latest CFTC CoT report pointed to extensions of existing positioning biases across asset managers, leveraged funds and non-commercial accounts, closer inspection revealed some nuances in the week ending August 5.

- Asset managers added ~$8.5mn DV01 equivalent of net longs across the curve, although ~$7.6mn of that came in WN futures alone. Elsewhere, net long setting in TU & TY futures was marginally more prominent than net long cover in FV, UXY & US futures. The cohort remains net long across the curve.

- Similarly, leveraged funds added ~$7.6mn DV01 equivalent of net shorts across the curve, with $8.2mln of fresh net shorts added in WN futures alone. Elsewhere, net short cover in FV & US futures proved slightly more sizeable than net short setting in TU, TY & UXY futures. The cohort remains net short across the curve.

- Wider non-commercial accounts added to existing net shorts in all contracts outside of US futures, where net positioning was essentially neutral. The cohort remains net short across the curve. See table below for greater details on net positioning swings for non-commercials.

Source: MNI - Market News/Bloomberg Finance L.P.

FOREX: Rally in EUR/NOK Capped by CPI, Schedule Quiet

- Early strength in EUR/USD has faded, with the pair now flat headed through to the NY crossover. Nonetheless, price remains within range of the new recovery high posted on Thursday. This keeps the recovery off the late July pullback low intact, working against the bearish backdrop that’s dominated the pullback from 1.1829. This week's schedule is light - leaving the USD the likely more active leg of the price this week.

- The rally in EUR/NOK may be capped by the Norwegian CPI print this morning, which saw Y/Y CPI surge to 3.3% vs. Exp. 3.0% - with underlying CPI also tilted higher. A corrective pullback in the price would first target 11.9326, the 23.6% retracement for the upleg off the late July high. NOK is now the strongest performing currency in G10.

- GBP is making further progress today: GBP/USD is through the Friday high and clear of 1.3450. This narrows the gap with the notable 50-dma at 1.3503 - clearance above which could signal a stronger upside reversal toward the cycle high printed at the beginning of July.

- Notably, jobs and wages data due tomorrow morning are the next hurdle here. MPC policymakers clearly remain concerned over perky wages and the feedthrough to prices: consensus looks for weekly earnings ex-bonus to hold at 5.0% this week - still considerably north of the pre-COVID norms.

- Focus today rests on speculation and expectations for the Trump-Putin meeting scheduled for later this week. Ahead of the meeting in Alaska, reports this weekend suggested that Moscow and Washington are working toward a deal to progress with a ceasefire in exchange for a freezing of territorial gains - an agreement that will likely receive heavy criticism among European leaders, and the Ukrainian President himself.

- There remain questions over whether Zelenskyy himself could attend the meeting in some capacity - but regardless of the outcomes this week, the meeting represents a significant thawing in tensions between Russia and the West.

OPTIONS: EUR Expiries Could Help Define Range into Monday Cut

Larger FX options rolling off at today's NY cut include sizeable strikes in EUR/USD, which may help contain the price inside 1.1600-1.1690 - particularly as the data and speaker calendar for today is muted. Unusually, there's a decent sized expiry in NZD/USD just below today's low of 0.5939 - equating to N$1.2bln. Full list here:

- EUR/USD: $1.1550(E1.2bln), $1.1600-05(E1.1bln), $1.1650-60(E940mln), $1.1690-00(E1.5bln), $1.1750(E1.0bln)

- USD/JPY: Y147.00($571mln)

- GBP/USD: $1.3331-45(Gbp552mln)

- NZD/USD: $0.5920-30(N$1.2bln)

EQUITIES: Underlying Uptrend for E-Mini S&P Remains Intact

- The bounce off post-NFP lows in global equity indices holds, with the Eurostoxx 50 future above the 50-day EMA Monday morning. Last week's strength refocuses attention on 5486.00, the May 20 high. To the downside, impulsive weakness did result in a temporary breach of the bear trigger - this makes the April 30 hi/lo range at 5078-5138 the area of downside interest.

- E-mini S&P prices recovered well Friday, meaning the bulk of the bounce off the NFP low is holding firm, keeping the underlying uptrend intact for now. The index holds above support at the 20-day EMA, at 6351.18. Through recent phases of weakness, the 50-day EMA at 6231.77, has held as support - and will be important on any intraday declines. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.

COMMODITIES: WTI Future S/T Momentum Points Lower Following Last Week's Weakness

- WTI futures traded poorly last week, cracking the 50-day EMA and piercing the bear trigger. This keeps S/T momentum pointed lower. The clear break exposes $58.17, the May 30 low. Gains early last week marked an extension of a corrective cycle - which may now have concluded. $69.41 marks the 50.0% retracement of the Jun 23-24 downleg. A continuation higher would open $70.96 next, the 61.8% retracement point.

- Gold is lower early Monday, however the price continues to benefit from the recent soft NFP print and broad USD weakness. This returns prices toward the top-end of the recent range and supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3332.8, the 50-day EMA. A clear break of this level continues to signal scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high.

| Date | GMT/Local | Impact | Country | Event |

| 11/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 11/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 12/08/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 12/08/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 12/08/2025 | 0600/0700 | *** | Labour Market Survey | |

| 12/08/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 12/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 12/08/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 12/08/2025 | 1100/1200 | BOE APF Quarterly Report | ||

| 12/08/2025 | - | *** | Money Supply | |

| 12/08/2025 | - | *** | New Loans | |

| 12/08/2025 | - | *** | Social Financing | |

| 12/08/2025 | 1230/0830 | * | Building Permits | |

| 12/08/2025 | 1230/0830 | *** | CPI | |

| 12/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 12/08/2025 | 1400/1000 | Richmond Fed's Tom Barkin | ||

| 12/08/2025 | 1430/1030 | Kansas City Fed's Jeff Schmid | ||

| 12/08/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/08/2025 | 1800/1400 | ** | Treasury Budget |