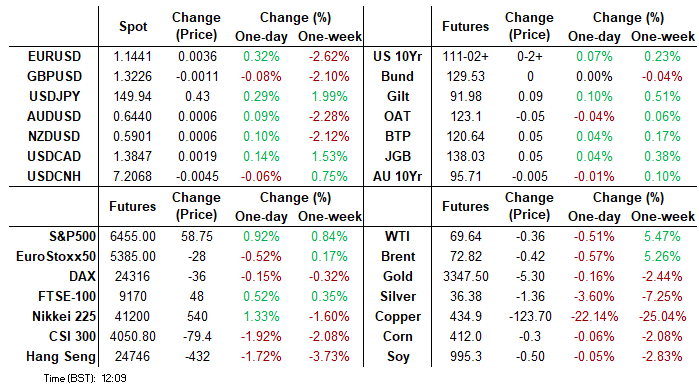

MNI US MARKETS ANALYSIS - JPY Through 150 Ahead of Key US Data

Highlights:

- Treasuries consolidate Powell's bear-flattening ahead of another phase of key data

- Tariff deals still in focus; South Korea general tariff rate set

- USD/JPY shows above Y150.00 for first time since April

US TSYS: Powell Bear Flattening Broadly Consolidated, Important Data Ahead

- Treasuries are off yesterday's lows but broadly consolidate yesterday’s bear flattening on a hawkish reaction to Fed Chair Powell’s lack of nod to a September cut amidst pressure from the Trump administration to cut interest rates.

- See the MNI Fed Review for a comprehensive re-cap: https://media.marketnews.com/Fed_Review_Jul2025_c74a594da3.pdf

- Cash yields are 0.5-1.5bp lower, with the front end lagging declines.

- TYU5 trades at 111-02+ (+02+), within yesterday’s range which saw a post-FOMC low of 110-30+, on thin cumulative volumes of 225k.

- The contract has pulled back away from resistance at 111-14+ (Jul 22/30 highs) but hasn’t tested support at 110-19+ (Jul 24 low) after which lies 110-08+ (Jul 14/16 low)

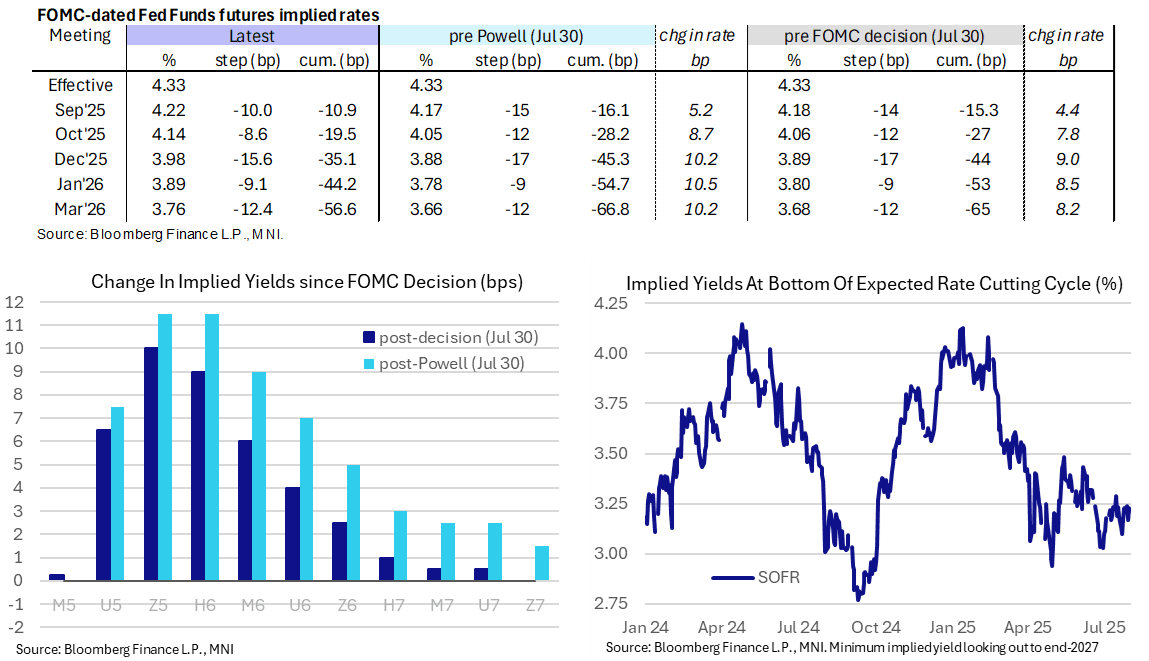

- STIR: There are 11bp of cuts for the next meeting in September (vs 15bp pre FOMC) before a cumulative 19.5bp for October and 35bp for year-end (vs 44bp pre FOMC).

- Markets still see it as a question of when not if we see deeper rate cuts though, with the SOFR implied terminal yield of 3.21% in the Mar 2027 contract implying at least four cuts from current levels. That’s firmly within the 3.1-3.3% range seen in July to date and comfortably at the low end of the range for the past eighteen months.

- Data: Challenger job cuts Jul (0730ET), PCE/Incomes Jun (0830ET), ECI Q2 (0830ET), Jobless claims (0830ET), MNI Chicago PMI Jul (0945ET)

- Fedspeak: FOMC blackout lasts until 0000ET Friday

- Bill issuance: US Tsy $95B 4W & $85B 8W bill auctions

- Latest tariff news: The US reached a trade agreement with South Korea that will impose a 15% tariff on imports, including autos. It also sets up major investment in American energy and shipbuilding. President Trump meanwhile said early Thursday that it would be “very hard” to make a trade deal with Canada after PM Carney said he planned to recognize Palestine as a state.

SOFR: Net Short Setting Most Prominent In Futures On Wednesday

Net short setting provided the dominant positioning impulse in the white, red and blue SOFR futures packs on Wednesday, with net long cover slightly more prominent in the greens.

- SFRM8 saw the largest net OI swing, with short setting seemingly dominating there.

| 30-Jul-25 | 29-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,270,869 | 1,260,054 | +10,815 | Whites | +22,169 |

SFRU5 | 1,298,866 | 1,311,877 | -13,011 | Reds | +23,633 |

SFRZ5 | 1,349,150 | 1,334,751 | +14,399 | Greens | -2,286 |

SFRH6 | 1,057,655 | 1,047,689 | +9,966 | Blues | +25,535 |

SFRM6 | 870,506 | 856,272 | +14,234 |

|

|

SFRU6 | 835,151 | 837,498 | -2,347 |

|

|

SFRZ6 | 932,315 | 923,458 | +8,857 |

|

|

SFRH7 | 711,037 | 708,148 | +2,889 |

|

|

SFRM7 | 692,894 | 696,463 | -3,569 |

|

|

SFRU7 | 516,895 | 526,477 | -9,582 |

|

|

SFRZ7 | 462,754 | 452,477 | +10,277 |

|

|

SFRH8 | 332,567 | 331,979 | +588 |

|

|

SFRM8 | 248,494 | 231,225 | +17,269 |

|

|

SFRU8 | 199,537 | 198,932 | +605 |

|

|

SFRZ8 | 208,068 | 201,281 | +6,787 |

|

|

SFRH9 | 144,919 | 144,045 | +874 |

|

|

US TSY FUTURES: Net Short Setting Most Prominent On Wednesday

OI data points to net short setting across most of the curve as Tsy futures settled lower in the wake of yesterday’s FOMC decision.

- The broader theme was only broken by a round of net long cover in US futures, which provided the largest DV01 equivalent swing on the curve (~$3.3mln).

- Still, the net curve positioning bias was tilted towards net short setting.

| 30-Jul-25 | 29-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,450,556 | 4,420,912 | +29,644 | +1,093,319 |

FV | 6,975,022 | 6,936,952 | +38,070 | +1,621,261 |

TY | 4,954,611 | 4,936,080 | +18,531 | +1,214,957 |

UXY | 2,425,081 | 2,417,442 | +7,639 | +663,462 |

US | 1,765,662 | 1,789,801 | -24,139 | -3,342,112 |

WN | 1,954,031 | 1,951,657 | +2,374 | +427,845 |

|

| Total | +72,119 | +1,678,733 |

US LABOR MARKET: MNI Payrolls Preview: An Early Test Of Latest Powell Patience

- “We have published and e-mailed to subscribers the MNI US Payrolls Preview.

- Please find the full report including MNI analysis and views from sellside analysts here: https://media.marketnews.com/USNFP_Aug2025_Preview_3bfda52c8f.pdf

Executive Summary

- Nonfarm payrolls growth is seen at 104k in July (sa) per the broad Bloomberg survey after 147k in June.

- The median primary dealer analyst eyes 100k whilst the Bloomberg whisper currently sits at 115k after little net reaction to the stronger than expected ADP report for July.

- Government payroll growth is expected to be much softer after a surprise 73k surge in June, which we think was more likely down to seasonal adjustment quirks. There’s a wide range of primary dealer estimates for public payrolls growth in July, from +20k to -55k.

- Consensus sees private sector payrolls rising 100k after a disappointing 74k in June and the breadth of gains should again be watched. 59k of this came from the cyclically insensitive health & social assistance category, whilst roughly as many of the 250 industries increased on the month as those that decreased.

- Payrolls growth should continue to be viewed against long-run breakeven estimates of around the 100k mark although some, such as Deutsche Bank, see this potentially being as low as 50k owing to continued immigration curbs.

- The unemployment rate is widely expected to tick up a tenth to 4.2% after a surprisingly low 4.11% in June as it pulled back from a cycle high of 4.244% in May. A faster-than-expected deterioration will be required for the final six months of the year to reach the FOMC's June Q4 median projection of 4.5%.

- We highlight FOMC discussions on QCEW data pointing to softer payrolls growth, with Powell citing the unemployment rate as suggesting labor demand and supply are cooling in tandem.

- We expect two-sided risks but with greater sensitivity to a dovish report after a hawkish shift on a patient Powell at Wednesday's FOMC press conference. There is 11.5bp of cuts priced for Sept and 36bp for end-2025.

- We’re still to get the Aug NFP report, preliminary benchmark revision estimates and two CPI reports before the Sept 16-17 FOMC meeting.

US: Trump Says US Would Be "Dead" w/o Tariffs As Court Case To Start

President Donald Trump posts on Truth Social: "To all of my great lawyers who have fought so hard to save our Country, good luck in America’s big case today. If our Country was not able to protect itself by using TARIFFS AGAINST TARIFFS, WE WOULD BE “DEAD,” WITH NO CHANCE OF SURVIVAL OR SUCCESS. Thank you for your attention to this matter!"

- Trump is referring to a court case getting underway in New York City at 10:00ET (15:00BST, 16:00CET), in which 11 judges will hear 45 mins of arguments from the Trump administration and two small businesses that argue the president's tariff regime is illegal. The firms argue that Trump's use of the International Emergency Economic Powers Act of 1977 to impose tariffs without congressional approval was in breach of the law's standards.

- As NBC reports, "The Court of International Trade initially blocked the tariffs in late May. It found that the import duties lacked “any identifiable limits” and that the law Trump cited in many of his executive orders did not “delegate an unbounded tariff authority to the President.” It also said the tariffs did not meet the test of an “unusual and extraordinary” risk to the country."

- If the court finds against the Trump administration, this does not mean an end to the tariff drive. Tariffs on steel and aluminium have been imposed under other laws. Utilising other legislation, such as Section 301 of the 1974 US Trade Act, Section 232 of the 1962 trade law, or Section 338 of the Trade Act of 1930, may all provide avenues should the court rule against the administration.

CANADA: Trump-Palestinian State Recognition Makes Trade Deal 'Very Hard' To Make

Earlier this morning, US President Donald Trump posted on Truth Social, "Wow! Canada has just announced that it is backing statehood for Palestine. That will make it very hard for us to make a Trade Deal with them. Oh’ Canada!!!". Trump's comments come after PM Mark Carney stated on 30 July that Canada plans to recognise a Palestinian state in September, provided the Palestinian Authority meets certain criteria on reforms.

- Carney's shift makes Canada the third G7 country in a week to announce the future recognition of a Palestinian state. It comes after French President Emmanuel Macron and UK PM Sir Keir Starmer both announced that their countries would formally recognise a Palestinian state at the UN General Assembly in September (again, subject to certain conditions regarding the actions of Israel in Gaza/the Palestinian Authority).

- With just hours remaining until the 1 Aug deadline for a trade deal to be reached to avoid 35% 'reciprocal' tariffs, it appears increasingly likely that sector-specific tariffs (at the very least) are due to remain in place.

- Minister responsible for Canada-U.S. Trade Dominic LeBlanc is in Washington, D.C., for last minute talks, but the Toronto Star reports, "While Carney called the talks “constructive” and “complex,” he said there are certain sectors Trump views as “strategic” for national security reasons. He named automobiles and steel — significant employers in Ontario — as well as aluminum, pharmaceuticals, lumber, and semiconductors."

JAPAN: LDP Sets 8 Aug For Crucial Meeting To Decide PM's Fate

The governing Liberal Democratic Party (LDP) will hold a General Assembly meeting of lawmakers from both houses of the National Diet on 8 August. This event could prove crucial in determining whether PM Shigeru Ishiba remains in office or faces a formal move to call a snap party leadership election.

- Earlier in the week, a similar meeting was convened to discuss the fallout from the 20 July House of Councillors election, in which the LDP-Komeito coalition lost its majority. However, this was labelled as a 'roundtable discussion', rather than a formal General Assembly.

- Ishiba has said that he will face down the Assembly and offer explanations for the poor performance without avoiding responsibility. The Assembly can pass a no-confidence motion that demands the resignation of a party president, but this is non-binding and non-enforceable.

- Instead, an emergency leadership election can be triggered if more than one-half of LDP lawmakers from both chambers, and leaders of half of the prefectural organisations formally submit a written request.

- If it appears likely that the recall provision threshold will be met, there is the prospect that Ishiba may offer his resignation, rather than face the ignominy of ouster/losing a leadership vote.

- While Ishiba has said he will look to stay in office to avoid a political vacuum, LDP Secretary-General Hiroshi Moriyama has indicated that he may resign in the wake of the elections. It remains to be seen whether this would be enough to placate restless LDP lawmakers.

USD: The Yen comes under renewed pressure

- The Dollar has started the session in the red against most of the majors, and that's despite the Hawkish leaning FOMC Yesterday.

- Mr Powell rejected the argument from two dissenting members, and maintained the need for the Fed to stay vigilant against inflation risk.

- Some of the Gains in the more sensitive to Risk, in the likes of the SEK, AUD and NZD, have been attributed to the Risk On tone, as the Emini Future printed a new Record high Overnight.

- The Emini initially plummeted on the Fed's Hawkish stance, but has quickly reversed all of its losses following a beat for Meta and Microsoft last night into the Overnight Open.

- The SEK is the best Performer, up half a percent, but the chart is getting interesting at present.

- The 9.8000 level has again provided some resistance for the USDSEK, this level has now held since the 13th May, but for now, the USDSEK has fallen down towards 9.7000, printed a 9.7291 earlier.

- The standout mover has been the Yen, BoJ Governor Ueda noted that the risk of the BoJ falling behind the curve on rate hikes is not that high at present, while he also notes that the JPY is not really deviating from the BoJ’s expectations, these comments have put pressure back against the Yen.

- Some Market participants will look at the 150.00 level next, and as quick side note, a test to 150.03 would reverse the Tariffs announcement in April.

- The 150.49 level is the 2nd April high.

OPTIONS: Expiries for Jul31 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1475-90(E1.3bln), $1.1490(E986mln), $1.1600-10(E2.6bln), $1.1650-70(E2.0bln), $1.1745-50(E1.1bln), $1.1800(E2.0bln)

- USD/JPY: Y146.00-20($1.5bln), Y147.40-50($728mln), Y148.00($522mln)

- AUD/USD: $0.6465(A$1.0bln), $0.6600(A$1.4bln)

- NZD/USD: $0.5965(N$505mln)

- USD/CAD: C$1.3670-75($1.0bln), C$1.3740($602mln)

- USD/CNY: Cny7.0700($1.4bln), Cny7.1500($897mln)

EQUITIES: Fresh Cycle Highs for E-Mini S&P Affirms Bullish Conditions

- The trend condition in Eurostoxx 50 futures remains bullish and short-term weakness appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. For bulls, a stronger resumption of gains would refocus attention on the bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00.

- The trend set-up in S&P E-Minis remains bullish. A fresh cycle high today confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6181.96. Support at the 20-day EMA is at 6329.36.

COMMODITIES: Gold Partially Pares Some of This Week's Earlier Decline

- WTI futures have traded higher this week highlighting an extension of the current corrective cycle. $69.41, the 50.0% retracement of the Jun 23-24 downleg, has been pierced. A continuation higher would open $70.96 next, the 61.8% retracement point. On the downside, support to watch is the 50-day EMA, at $65.21. The average has been pierced, a clear break of it would expose $58.17, the May 30 low.

- Gold has pulled back from its Jul 23 high. Short-term weakness is considered corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal has traded through support at $3321.1, the 50-day EMA. A clear break of this level signals scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high. A break of this hurdle would be bullish.

| Date | GMT/Local | Impact | Country | Event |

| 31/07/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 31/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 31/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 31/07/2025 | 1230/0830 | * | Payroll employment | |

| 31/07/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/07/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/07/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/07/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 31/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 31/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 01/08/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 2330/0830 | * | Labor Force Survey | |

| 01/08/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/08/2025 | 0130/1130 | * | Producer price index q/q | |

| 01/08/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 01/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0800/1000 | * | Retail Sales | |

| 01/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/08/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/08/2025 | 0900/1100 | *** | HICP (p) | |

| 01/08/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/08/2025 | 1230/0830 | *** | Employment Report | |

| 01/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/08/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 01/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 01/08/2025 | 1400/1000 | * | Construction Spending | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 01/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |