US LABOR MARKET: MNI Payrolls Preview: An Early Test Of Latest Powell Patience

Jul-31 10:40

- “We have published and e-mailed to subscribers the MNI US Payrolls Preview.

Please find the full report including MNI analysis and views from sellside analysts here: https://media.marketnews.com/USNFP_Aug2025_Preview_3bfda52c8f.pdf

Executive Summary

- Nonfarm payrolls growth is seen at 104k in July (sa) per the broad Bloomberg survey after 147k in June.

- The median primary dealer analyst eyes 100k whilst the Bloomberg whisper currently sits at 115k after little net reaction to the stronger than expected ADP report for July.

- Government payroll growth is expected to be much softer after a surprise 73k surge in June, which we think was more likely down to seasonal adjustment quirks. There’s a wide range of primary dealer estimates for public payrolls growth in July, from +20k to -55k.

- Consensus sees private sector payrolls rising 100k after a disappointing 74k in June and the breadth of gains should again be watched. 59k of this came from the cyclically insensitive health & social assistance category, whilst roughly as many of the 250 industries increased on the month as those that decreased.

- Payrolls growth should continue to be viewed against long-run breakeven estimates of around the 100k mark although some, such as Deutsche Bank, see this potentially being as low as 50k owing to continued immigration curbs.

- The unemployment rate is widely expected to tick up a tenth to 4.2% after a surprisingly low 4.11% in June as it pulled back from a cycle high of 4.244% in May. A faster-than-expected deterioration will be required for the final six months of the year to reach the FOMC's June Q4 median projection of 4.5%.

- We highlight FOMC discussions on QCEW data pointing to softer payrolls growth, with Powell citing the unemployment rate as suggesting labor demand and supply are cooling in tandem.

- We expect two-sided risks but with greater sensitivity to a dovish report after a hawkish shift on a patient Powell at Wednesday's FOMC press conference. There is 11.5bp of cuts priced for Sept and 36bp for end-2025.

- We’re still to get the Aug NFP report, preliminary benchmark revision estimates and two CPI reports before the Sept 16-17 FOMC meeting.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Tuesday Data Calendar: Policy Panel w/Fed Chair Powell, ISMs, JOLTs

Jul-01 10:40

- US Data/Speaker Calendar (prior, estimate)

- 07/01 0930 Policy panel in Sintra w/ Fed Powell, Lagarde, Bailey, Ueda, Rhee

- 07/01 0945 S&P Global US Manufacturing PMI (52.0, 52.0)

- 07/01 1000 ISM Manufacturing (48.5, 48.8), Prices Paid (69.4, 69.5)

- 07/01 1000 ISM New Orders (47.6, 48.1), Employment (46.8, 47.1)

- 07/01 1000 Construction Spending MoM (-0.4%, -0.2%)

- 07/01 1000 JOLTS Job Openings (7.391M, 7.300M), rate (4.4%, 4.4%)

- 07/01 1000 JOLTS Quits Level (3.194M, 3.188M), rate (2.0%, --)

- 07/01 1000 JOLTS Layoffs Level (1.786M, 1.831M), rate (1.1%, --)

- 07/01 1030 Dallas Fed Services Activity (-10.1, --)

- 07/01 1130 US Tsy $50B 6W bill auction

- Source: Bloomberg Finance L.P. / MNI

GOLD: Supported By Lower US Real Yields; Possible False Trendline Break

Jul-01 10:39

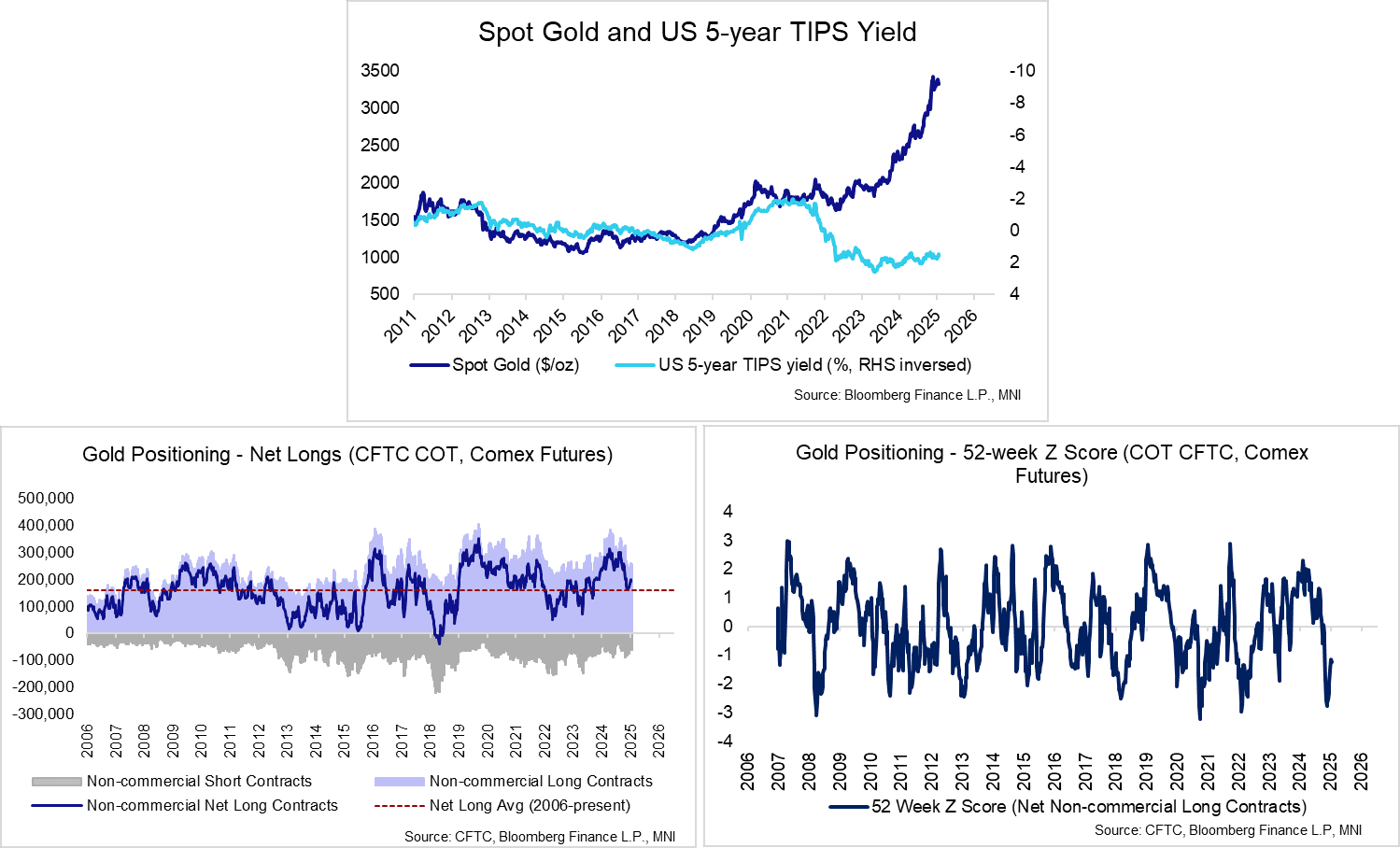

Spot gold has rallied around 3% from yesterday’s $3,248.7 low, currently at $3,347.2. The recovery highlights a possible false trendline break, after spot pushed through the 50-day EMA and trendline support drawn from the Dec 30 low last Friday. Gold has pierced initial resistance at $3,336.1 (20-day EMA), exposing the June 23 high at $3395.1.

- This week’s pullback in US real yields appears to have supported gold via two channels. First, weaker real yields (US 5-year TIPS is down 5bps from Friday’s close) makes non-interest-bearing gold relatively more attractive. Second, the dollar index is down 0.5% today, buoying dollar-denominated spot.

- Though the yield channel provides a reasonable explanation for this week’s price action in gold, it’s worth remembering that on a longer-term horizon, gold prices have diverged significantly from real yields since mid-2021.

- The latest positioning data only covers the week to June 24, so does not incorporate last week’s technical breaks. As of June 24, total non-commercial net longs were 195k, up from a low of 161k on May 13 and above the 162k long-term average.

STIR: US Terminal Rate Seen Close To Post-Election Lows, Powell Panel Ahead

Jul-01 10:34

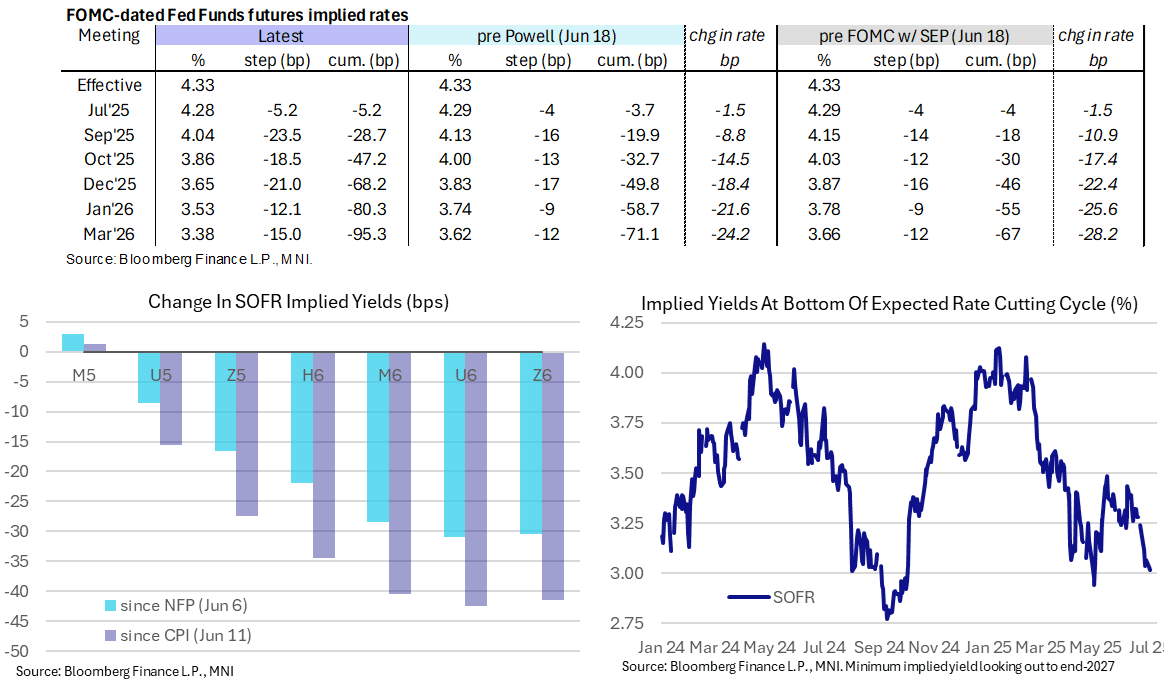

- Fed Funds implied rates are 0-1.5bp lower on the day for 2025 meetings, marginally shoring up a next cut in September whilst year-end expectations widen the gap with the median dot (68bp vs 50bp cuts pencilled in two weeks ago).

- Cumulative cuts from 4.33% effective: 5bp Jul, 28.5bp Sep, 47bp Oct, 68bp Dec, 80bp Jan and 95bp Mar.

- The SOFR implied terminal yield of 3.015% (SFRZ6, -1.5bp) last closed lower on Apr 29 and 30 (and before that pre-US election on Oct 2024) as it increasingly firmly prices five cuts for what’s left of the easing cycle.

- Today’s sole scheduled Fedspeak comes from Chair Powell speaking at the ECB’s Sintra conference. He’s on a panel with ECB’s Lagarde, BOE’s Bailey, BOJ’s Ueda and BOK’s Rhee at 0930ET.

- We have had limited major data releases since his congressional appearances last week, which in turn followed soon after the Jun 18 FOMC press conference, although Thursday did see surprisingly weak domestic demand revisions for Q1 before soft consumer spending in May on Friday.

- His House appearance saw treasuries rise and the USD pull back on headlines that appeared to suggest earlier rate cuts are possible "*POWELL: LOWER INFLATION, WEAKER LABOR COULD MEAN EARLIER CUT" (Bloomberg). However, the full context of this was that he was asked whether he concurs with Gov Waller about a potential path for "good news" to lead to rate cuts, Powell keeps the option conditionally open but not an unsolicited comment or an endorsement - and indeed he also notes potential for later cuts too.

- More broadly, Powell again implied that the September FOMC is the next live meeting.

Trending Top

May-22 16:54