MNI US MARKETS ANALYSIS - JPY, EUR Slide on Building Risks

Highlights:

- JPY on backfoot as market fears Takaichi's approach to BoJ coordination

- EUR slips as market beds in expectations of prolonged French political difficulties

- Shutdown enters new week, little chance of progress in very near-term

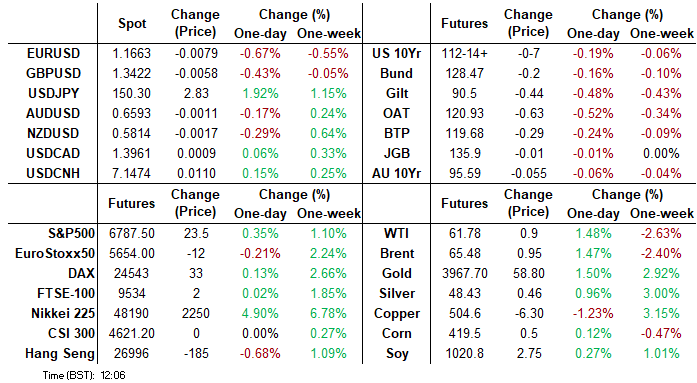

US TSYS: Curve Steeper On Japanese & French Cues, Shutdown Continues

TY futures trade back towards London morning lows after bulls failed to close the opening gap lower during a relief rally, last -0-06+ at 112-15.

- Immediate support at the 50-day EMA (112-12+) protects retracement support (112-01). Conversely, bulls look to break the Sep 24 top (113-00).

- Spill over from Japan (where a new LDP Party leader & PM promoted twist steepening) and France (with another PM resignation seen) provides bear steepening pressure, yields 0.5-5.0bp higher.

- 2s10s at 57.2bp, 5s30s at 102.9bp, consolidating within multi-week ranges. 2s10s ~7bp off cycle closing highs, 5s30s ~20bp off cycle closing top, after some modest steepening last week.

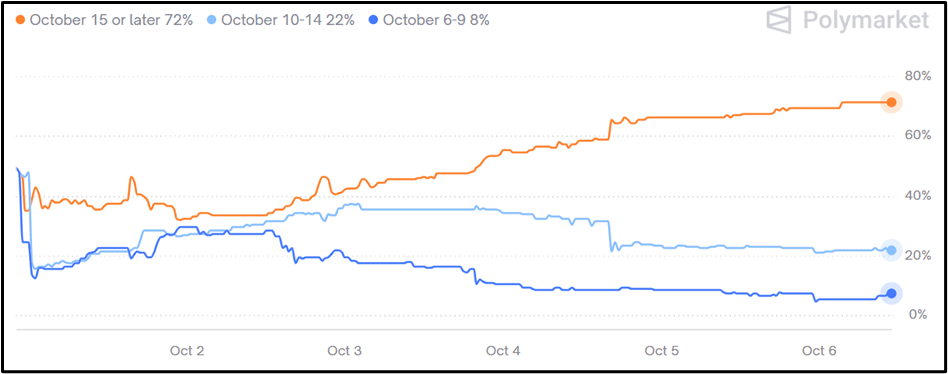

- The government remains in shutdown. ~75% of Polymarket bettors believe the shutdown will last until October 15 at the earliest.

- Markets remain focused on the timing of delayed data releases, most notably the September Employment report.

- This week’s supply (including 3-, 10- & 30-Year Tsy auctions) will go ahead as scheduled.

- Fed pricing little changed to start the week, OIS near enough fully discounts a 25bp cut at this month’s meeting and prices ~47bp of easing through year-end.

- Just over 100bp of cuts priced between now and the end of the September ’26 FOMC, while SOFR-implied terminal rate pricing sits at 3.065% (vs. ~2.80% at one point in September).

- Kansas City Fed President Schmid well speak on the economic outlook and monetary policy later today (17:00 NY/22:00 London).

US: Government Shutdown Day 6: Standoff Continues Unchanged

Senate Majority Leader John Thune (R-SD) is expected to hold a fifth vote at 17:30 ET 22:30 BST on the GOP's CR to fund the government through Nov. 21. The vote is likely to fail again. Thune has shown no sign of pivoting on his strategy to keep re-running the vote until enough Democratic Senators fold amid a pressure campaign led by OMB Director Russell Vought.

- Thune likely needs at least eight Democrats to clear the 60-vote Senate filibuster. There is no sign yet any new Democrats will join the three who have voted in favour of the bill in the previous ballots. There are still no leader-level talks on Democrats' demands for an Obamacare deal to reopen the government. House Speaker Mike Johnson (R-LA), is expected to keep the House recessed for a second successive week, effectively closing the door to any rank-and-file bipartisan negotiations.

- Pressure will intensify on Democrats this week when some federal workers miss their first paycheck on Friday. On October 15, active-duty service members will miss their first paycheck. House Majority Leader Steve Scalise (R-LA) told Republicans on Saturday to “hammer Democrats on the military pay deadline,” per Politico.

- Polling appears to give the Democrats a slight edge in public opinion. The Canvass found, "More than half of top Capitol Hill staffers (58%)” say the GOP is to blame for the shutdown. CBS notes, “Republicans and the president get relatively more [blame] than congressional Democrats." Polymarket sees a 72% implied probability the shutdown extends beyond October 15.

Figure 1: End Date of Govt Shutdown

Source: Polymarket

FRANCE: Oct.13 Budget Draft Deadline Looms w/No Clear Route To Functional Govt

French Minister for Public Accounts Amélie de Montchalin warned in an interview with Le Monde last month that the government must submit a draft budget to parliament by October 13 or enact a special law to avoid a shutdown, as it will no longer be possible to pass a budget by January 1.

- De Montchalin said a special law was used earlier this year, “There was no catastrophe because it only lasted six weeks.” However, she added, “France cannot go an entire year without a budget: It's a context in which revenues and expenditures are frozen. Political choices and priorities would give way to a purely accounting form of management.”

- According to de Montchalin, France cannot operate under special accounting, “because, in 2026, we need to allocate €8 billion more to paying interest on the debt. Without an approved budget, those €8 billion would have to be found elsewhere, in a top-down manner, without a debate in Parliament.”

- The resignation of Prime Minister Sébastien Lecornu has left President Emmanuel Macron with no obvious route to restoring the stability required to pass a budget, with any successor likely to encounter the same resistance from both the left and right in parliament.

- Emmanuel Cau, head of European equities strategy at Barclays, “The only way to stop this crisis is to have a new election. It’s making Europe hard to invest in and creating an excuse for investors to tread carefully… The market has to think about the far right being in a position to capitalise.”

- Jordan Bardella, president of the far-right Rassemblement National, said this morning. “We have no other possibility but to return to the French people because, once again, the longer we wait, the more we play with the stability of the country...”

US TSY FUTURES: Mix Of Short Setting & Long cover seen On Friday

OI data points to a mix of net short setting (FV, UXY & US) and long cover (TU, TY & WN) as Tsy futures ticked lower on Friday.

- The net short setting in US futures provided the only move of any real note and was enough to bias the curve-wide net positioning adjustment in that direction.

| 03-Oct-25 | 02-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,576,545 | 4,581,926 | -5,381 | -211,960 |

FV | 6,690,084 | 6,685,014 | +5,070 | +221,710 |

TY | 5,477,591 | 5,480,087 | -2,496 | -168,411 |

UXY | 2,464,473 | 2,463,578 | +895 | +80,678 |

US | 1,872,448 | 1,859,040 | +13,408 | +1,890,760 |

WN | 2,055,049 | 2,058,891 | -3,842 | -709,704 |

|

| Total | +7,654 | +1,103,074 |

SOFR: Net Long Cover In SFRZ6 Seen On Friday

OI data points to a mix of net short setting and long cover as SOFR futures ticked lower ahead of the weekend, with the most meaningful net positioning swing coming via net long cover in SFRZ6.

| 03-Oct-25 | 02-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,420,852 | 1,414,849 | +6,003 | Whites | +38,849 |

SFRZ5 | 1,487,101 | 1,470,780 | +16,321 | Reds | -17,608 |

SFRH6 | 1,169,991 | 1,160,711 | +9,280 | Greens | +3,007 |

SFRM6 | 1,033,260 | 1,026,015 | +7,245 | Blues | +14,229 |

SFRU6 | 984,717 | 978,621 | +6,096 |

|

|

SFRZ6 | 1,008,324 | 1,038,706 | -30,382 |

|

|

SFRH7 | 785,627 | 779,636 | +5,991 |

|

|

SFRM7 | 787,927 | 787,240 | +687 |

|

|

SFRU7 | 679,360 | 677,232 | +2,128 |

|

|

SFRZ7 | 729,508 | 729,624 | -116 |

|

|

SFRH8 | 423,491 | 423,536 | -45 |

|

|

SFRM8 | 357,122 | 356,082 | +1,040 |

|

|

SFRU8 | 290,435 | 285,771 | +4,664 |

|

|

SFRZ8 | 318,354 | 309,216 | +9,138 |

|

|

SFRH9 | 188,265 | 186,376 | +1,889 |

|

|

SFRM9 | 170,072 | 171,534 | -1,462 |

|

|

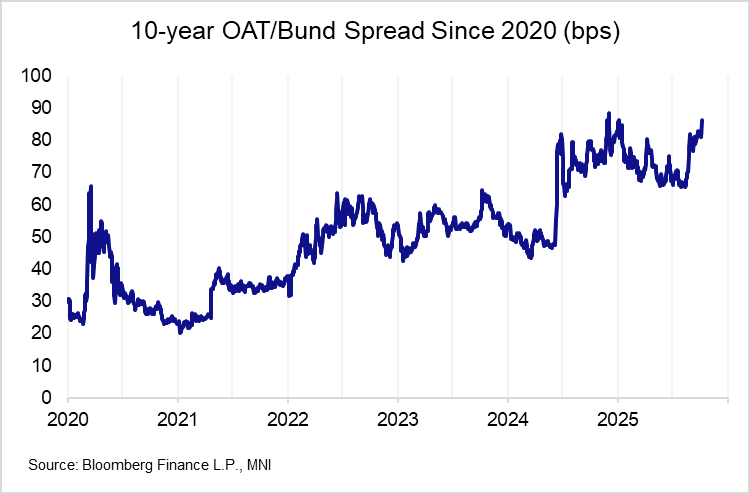

OAT/Bund Spread Consolidates Around 86bps; Analysts Flag '25 Election Risk

- After widening to a knee-jerk high of 89bps following PM Lecornu’s resignation, the 10-year OAT/Bund spread has consolidated around 86bps. While the timing of Lecornu’s resignation came as a surprise, intraday widening has been limited by the fact Lecornu’s prospects of passing a 2026 budget were appearing bleak from the onset. Lecornu’s resignation today may have just delayed the inevitable.

- Today’s moves in spreads can be classed as orderly and reflective of fundamentals (i.e. political/fiscal risk premium). That should dispel any fresh speculation around the use of the ECB’s TPI – something almost all Governing Council members have strongly pushed back on in recent months.

- In an interview with the MNI Policy Team, a Greek treasury source noted that “investors don't doubt that the ECB or the EU would step in the case of an unwarranted dysfunction in European sovereign debt markets.”. While not an immediate concern right now, this implicit backstop may also contain blowout episodes in spreads without requiring a formal triggering of the TPI.

- Sellside views following Lecornu’s resignation highlight the challenges facing France. Some note that fresh legislative elections may come as soon as this year:

- Barclays: Macron has two main options: "appointing a new Prime Minister or dissolving the National Assembly. Even if President Macron chooses the former, we now think that early legislative elections are the baseline before year-end."

- Commerzbank: “After two centrist politicians have failed in quick succession, the choice is likely to fall on a moderate right-wing politician or a left-wing politician. The latter is the more likely scenario”…“a prime minister from the left-wing camp is likely to focus on higher taxes in the budget dispute and intensify conflicts with Macron's camp”…“ there are no signs of a resolution to the political deadlock, and a consensus on ambitious reforms of public finances remains a long way off.”

- Berenberg: “This further increases the risk that France's fiscal troubles will remain unresolved and that economic policies will become less growth-friendly. It adds to the risk that France may be heading for new parliamentary elections in late 2025 or early 2026.”

FOREX: EUR and JPY Slide on Political Risks, USD Main Beneficiary

- The EUR is weaker in early Europe, following the resignation of the French PM Lecornu - and bedding markets in for an extended period of political risk and budget brinkmanship. French equities also see weakness - with the CAC40 easily the underperformer in Europe. Next major support in EURUSD crosses at 1.1646, the late Sept low. Weakness through here snaps the weak uptrend posted off the August 1st low.

- Lecornu's resignation opening up more criticism from other parties: National Rally's Bardella says the government have shown they have understood

"nothing" regarding the country's problems. - Meanwhile, the JPY is lower against all others in G10, helping trigger a new all-time high for EURJPY, after the surprise victory of Takaichi in the LDP leadership race. This was no doubt a surprise to the market given market odds, with most bettors favouring Koizumi winning the race. An extraordinary session of the Diet will be held around Oct to choose a new PM.

- Takaichi's policy bias around pro-fiscal policy may mean the coalition could expand to incorporate more like-minded parties, and she is expected to focus on cash handouts and tax rebates for households to reduce cost of living pressures. While she toned down her criticism of the BoJ during the leadership campaign, her well known views around BoJ rate hikes (she previously deemed them "stupid") is weighing on the currency. USD/JPY rallied to touch 150.44, paving the way for a test of the key medium-term resistance at 150.92, the Aug 1 high. A break of this hurdle would confirm a resumption of the bull leg that started Apr 22. Today's intraday low at 149.05 is the first support.

- The US government remains in shutdown, leaving official data on the sidelines for now. As such, market focus remains on central bank speak. ECB members due today include ECB's Escriva & Lagarde, Fed's Schmid and BoE's Bailey.

- USDJPY consolidates above the 150.00 handle on elevated volumes (Z5 JPY futures have printed more than double their average volume for this time of day) as markets digest the unexpected victory for fiscal dove Takaichi at the LDP leadership contest, and the spillover impacts on reduced pricing for the BoJ's October meeting.

- From a technical perspective, the USDJPY breach of key short-term resistance at 149.96 paves the way for a test of the key medium-term resistance at 150.92, the Aug 1 high. A break of this hurdle would confirm a resumption of the bull leg that started Apr 22. Today’s intraday low at 149.05 is the first support.

- EURJPY meanwhile has faded off alltime highs on French PM Lecornu's resignation. EMAs in EURJPY continue to point to the upside, clearance of 175.13 resistance confirmed a resumption of the primary uptrend opens the 177.00 handle next. On the downside, key short-term support has been defined at 172.27, the Oct 2 low.

- Conversely, Takaichi moderated her firmer views on the BoJ during the campaign trail, and stressed the responsible approach to spending her government would adopt. As a result, JPY weakness could prove limited beyond today's moves, in which case 149.56 and 148.54 mark intraday supports before 147.47 would close the Takaichi gap.

OPTIONS: Expiries for Oct06 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1675-80(E1.4bln), $1.1700(E1.2bln), $1.1750(E926mln), $1.1800(E943mln)

- USD/JPY: Y146.00($1.3bln), Y147.00($2.6bln), Y147.70-80($877mln), Y147.95-00($756mln)

- AUD/USD: $0.6568-70(A$1.3bln), $0.6700(A$1.1bln)

EQUITIES: EuroStoxx 50 Futures Maintain a Bullish Theme Following Recent Climb

- Eurostoxx 50 futures maintain a bullish theme. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Initial firm support is 5525.00, the Aug 22 high.

- A bull cycle in S&P E-Minis remains intact. The contract traded to a fresh cycle high last week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 66.84.22. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6566.78.

COMMODITIES: WTI Futures Remain in a Bear-Mode Condition

- WTI futures remain in a bear-mode condition. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens a bearish theme and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal.

- A bull cycle in Gold remains in play and today’s fresh cycle high, reinforces current conditions. This maintains the bullish price sequence of higher highs and higher lows and note too that corrections, when they do occur, are shallow. Furthermore, moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3987.33 next, a Fibonacci projection. Support to watch lies at $3715.0, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 06/10/2025 | 1500/1600 | BOE Bailey Keynote at Scotland Global Investment Summit | ||

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 06/10/2025 | 1700/1900 | ECB Lagarde at ECON Hearing, European Parliament | ||

| 06/10/2025 | 2100/1700 | Kansas City Fed's Jeff Schmid | ||

| 07/10/2025 | 2330/0830 | ** | Household spending | |

| 07/10/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/10/2025 | 0645/0845 | * | Foreign Trade | |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 07/10/2025 | 1400/1000 | * | Ivey PMI | |

| 07/10/2025 | 1405/1005 | Fed's Miki Bowman | ||

| 07/10/2025 | 1430/1030 | Fed Governor Stephen Miran | ||

| 07/10/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/10/2025 | 1530/1130 | Minneapolis Fed's Neel Kashkari | ||

| 07/10/2025 | 1610/1810 | ECB Lagarde Speech at Business France Event | ||

| 07/10/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 07/10/2025 | 1900/1500 | * | Consumer Credit | |

| 07/10/2025 | 2005/1605 | Fed Governor Stephen Miran |