MNI US MARKETS ANALYSIS - Hopes of US-China Trade Deal Recede

Highlights:

- Hopes of near-term US-China trade resolution dwindle as Trump calls Xi "EXTREMELY HARD TO MAKE A DEAL WITH"

- USD holding most of Tuesday's JOLTS relief rally, EUR/USD has hard time above 1.1400

- Equities improve as US curve modestly twists flatter

US TSYS: Modest Twist Flattening, ISM Services Later On

- Treasuries sit slightly twist flatter on the day, having remained within yesterday’s range across all benchmark tenors overnight.

- The long end appeared to be helped off lows by Reuters reporting the BoJ is considering slowing the pace of tapering in its bond purchases from next fiscal year onward. It’s not a new idea but helped some demand for JGB futures even if they’ve since pared gains.

- Trade discussions: President Trump on Truth Social: "I like President XI of China, always have, and always will, but he is VERY TOUGH, AND EXTREMELY HARD TO MAKE A DEAL WITH!!!"

- Separately, the EC’s Sefcovic said on X that there has been a productive and constructive discussion with USTR Greer. “We're advancing in the right direction at pace - and staying in close contact to maintain the momentum.”

- Today sees primary data focus on ISM Services although with some sensitivity to ADP and final PMIs before the Fed’s Beige Book for an update on what the Fed is hearing in liaison programs ahead of the Jun 17-18 decision.

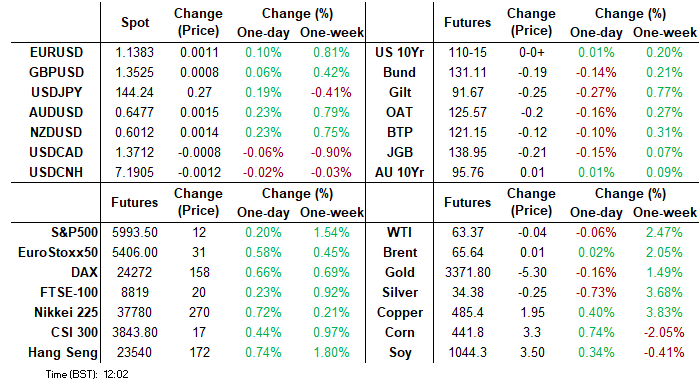

- Cash yields are 0.6bp higher (3s) to 1.2bp lower (30s).

- 5s30s at 94.6bp (-1.8bp) is back to Friday’s levels.

- TYU5 trades at 110-15 (00+) on very low volumes of just 215k. It has remained within yesterday’s range throughout.

- Resistance continues to be watched at 110-30 (May 30 and Jun 2 highs), having topped out at 110-26+ yesterday, whilst support is seen at 109-26 (May 29 low) after which lies a bear trigger at 109-12+ (May 22 low).

- Data: MBA mortgage apps (0700ET), ADP May (0815ET), S&P Global US serv/comp final PMIs (0945ET), ISM Services May (1000ET)

- Fedspeak: Bostic & Cook moderate Fed Listens event (0830ET) – see STIR bullet – before Beige Book (1400ET)

- Bill issuance: US Tsy $60B 17W bill auction (1130ET)

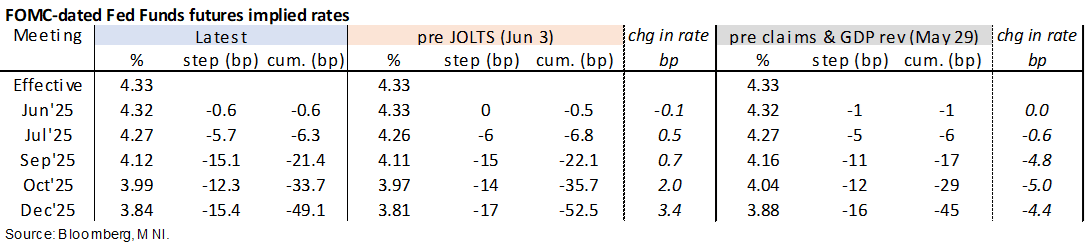

STIR: Holding At ~50bp Of Fed Cuts For 2025

- Fed Funds implied rates for 2025 meetings are marginally higher on the day, leaving end-2025 rates close to highs seen in the hours after yesterday's JOLTS release.

- There is mild intraday spillover from better-than-expected Eurozone final service PMIs ahead of today’s US release and the ISM services print.

- Cumulative cuts from 4.33% effective: 0.5bp Jun, 6.5bp Jul, 21.5bp Sep, 33.5bp Oct and 49bp Dec.

- The SOFR implied terminal yield of 3.325% (SFRZ6, +1bp) last closed higher on May 22.

- Today’s Fedspeak is limited to just Bostic (non-voter) and Cook (permanent voter) moderating a Fed Listens Event (text only) at 0830ET.

- We think it’s unlikely anything market moving comes from the event, with the Beige Book at 1400ET more notable from a communications angle.

- Cook yesterday gave a speech that hewed very close to the FOMC majority's view on monetary policy without giving much away on her personal views on future rates (“well positioned to respond to a range of potential developments”). However, in Q&A she intriguingly noted that "we have to be open to all possibilities. We don't know how tariffs are going to play out. One could imagine those scenarios - cutting, staying or hiking, happening."

- Bostic yesterday reiterated that he thinks there’s space for one rate cut this year. He sees some indications of potential weakness in the labor market but no glaring signs of serious deterioration.

STIR: Mix Of Short Setting & Long Cover Seen In Most SOFR Futures On Tuesday

OI data points to a mix of net short setting and long cover through the SOFR blues on Tuesday.

- The unchanged price status across the front 3 contracts means that we can’t make any definitive inference re: the direction of the apparent positioning adds and cover in those contracts.

| 03-Jun-25 | 02-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,070,435 | 1,068,762 | +1,673 | Whites | -7,428 |

SFRM5 | 1,428,383 | 1,452,788 | -24,405 | Reds | +10,569 |

SFRU5 | 1,121,424 | 1,119,211 | +2,213 | Greens | -5,547 |

SFRZ5 | 1,091,459 | 1,078,368 | +13,091 | Blues | +7,078 |

SFRH6 | 796,343 | 782,440 | +13,903 |

|

|

SFRM6 | 757,451 | 767,340 | -9,889 |

|

|

SFRU6 | 717,190 | 709,677 | +7,513 |

|

|

SFRZ6 | 837,979 | 838,937 | -958 |

|

|

SFRH7 | 671,938 | 669,179 | +2,759 |

|

|

SFRM7 | 585,423 | 586,744 | -1,321 |

|

|

SFRU7 | 414,903 | 415,716 | -813 |

|

|

SFRZ7 | 412,156 | 418,328 | -6,172 |

|

|

SFRH8 | 291,362 | 289,661 | +1,701 |

|

|

SFRM8 | 214,547 | 213,817 | +730 |

|

|

SFRU8 | 164,228 | 162,654 | +1,574 |

|

|

SFRZ8 | 173,212 | 170,139 | +3,073 |

|

|

FOREX: Global Carry Trades See Threat From Crowded Positioning, Return of Vol

- The sustained fade in G10 FX implied vol off the post-Liberation Day highs is helping provide a supportive backdrop for FX carry, and while the long-held status of JPY as a funding currency has ebbed since last year's intervention, other currencies have stepped in to take advantage of regional dislocations (most recently HKD and CNY), which are compensating for falling policy rates among traditional carry targets such as the MXN, AUD and others.

- BNY Mellon write that while there is little sign of market volatility picking up (meaning better risk-reward on carry trades) they believe conviction in these carry trades is not strong - and markets need to exercise greater caution amid an increasingly crowded strategy. They flag CHF, CNY and SEK low-yielding, funder currencies, all of which have large current account surpluses (which support a home investment bias in the context of US trade rebalancing), meaning the risk-reward profile for carry trades is likely to become structurally less attractive, tempering expectations around future returns.

- We see the sharp pull lower in local Hong Kong rates (both HIBOR and HKD funding rates) and the TWD spot rally has boosted the currency's status as an APAC funding currency, however persistent pressure on the weak-side of the FX trading band, a building 2025 IPO pipeline and improved corporate activity (bond sales, dividends) may mean pressured local rates are short-lived through the rest of 2025.

STIR: Slight Hawkish SNB Repricing As Tschudin Comments Garner Attention

Market expectations of near-term SNB policy edged hawkishly overnight on late comments yesterday from SNB's Tschudin, with implied odds for an outsized 50bp cut at the upcoming meeting now standing at around 1/4 (from about 1/3 yesterday). Through December 2025, markets price around 56bps of cuts (broadly unchanged from yesterday).

- Recapping, the key comments were

- a) a reiteration of the previous rhetoric that inflation "can" move into negative territory temporarily in Switzerland, and that the SNB is focussed on mid-term price stability - that is noteworthy as Swiss CPI indeed moved below zero in the May for the first time since 2021.

- b) an acknowledgement that market expectations for interest rates have fallen but that economists don't expect negative SNB rates in this cycle.

- Overall, Tschudin's comments lean marginally hawkish through implying the SNB is not panicking on yesterday's sub-zero CPI print. Despite this, Tschudin did not close the door for an outsized move at the upcoming meeting - "the situation changes every day, we will have to look and see what to do at next meeting".

- As Tschudin said, the analyst base case is for a regular 25bp cut to 0% at the June SNB meeting. Key comments we've seen following yesterday's CPI data:

- CIBC: "We anticipate that the central bank remains acutely aware of competitiveness pressures and disinflationary tendencies [...] given such concerns we remain mindful of the return to negative rates, albeit we only expect such a scenario in Q3."

- Danske: "We expect a final 25bp cut at the next meeting [...] and the SNB to opt for FX intervention before resorting to negative territory. Growth data to the strong side also supports this [...] the risk of a larger 50bp cut is definitely on the table following the print yesterday further amplified by the negative effects from the trade war with Switzerland set to be hit by a 32% tariff rate."

- ING: "We expect the SNB to cut its policy rate by 25 basis points at its next meeting on 19 June, with further cuts likely. Based on current data, a return to negative interest rates before year-end appears increasingly probable. Our base case includes a second 25bp cut in September, bringing the policy rate to -0.25%. While the SNB would prefer to avoid deeper cuts, a 50bp reduction in June cannot be ruled out."

- Wells Fargo: "We now see one more 25 bps SNB rate cut, to a policy rate of 0.00%, at the June 19 meeting. Beyond the June meeting, we see a less persuasive case for further easing, as the Swiss economy has shown a degree of resilience. In our view, further rate cuts after June would likely only materialize if there was a significant deceleration in economic activity and if we saw deflation become evident in underlying price measures as well. At this time, we believe that 0.00% will be the low for this monetary easing cycle."

EUROPE ISSUANCE UPDATE:

Italy dual-tranche syndication:

New 5-year:

- E12bln (MNI expected E7-10bln) of the new 5y Oct-30 BTP. Spread: 2.95% Jul-30 +8bps (guidance was +10bps area), books closed in excess of E120bln.

10y Green Tap:

- E5bln WNG tap of the 4.05% Oct-37 Green BTP. Spread: 0.95% Mar-37 +6bps (guidance was +9bps area), books closed in excess of E94bln.

EFSF RfP

- "Today ESM, the European Stability Mechanism, rated Aaa (Moody's) / AAA (Fitch) / AAA (S&P), has sent a Request for Proposal to a selection of banks from the

EFSF/ESM Market Group with regards to an upcoming transaction, subject to market conditions."

UK auction results

- The results of today’s 4.375% Mar-28 Gilt auction were broadly in line with previous re-openings for this line.

- The secondary market price for the Gilt inched lower into the bidding deadline (pre-auction mid 100.788) but has reversed the move since results were published.

- The lowest accepted price of 100.796 exceeded the pre-auction mid-price.

- The 0.3bp yield tail was within the 0.2-0.5bp range seen in the four previous re-openings this year.

- The 3.08x bid-to-cover ratio was slightly below the 3.26x average for this year’s previous sales (prior 3.48x).

- GBP4.75bln of the 4.375% Mar-28 Gilt. Avg yield 4.062% (bid-to-cover 3.08x, tail 0.3bp).

EURJPY and EURGBP Displaying Divergent Trend Signals

- A bullish theme in EURJPY remains intact. The latest recovery from the May 23 low, signals the end of the corrective pullback between May 13 - 23. If correct, the move higher also marks a resumption of the uptrend. Sights are on a cluster of resistance around the 165.00 mark, which has been of pivotal significance dating back to the BOJ’s intervention back in July last year.

- 165.21, the May 13 high remains the technical bull trigger, of which a breach would target a move towards 166.10 (Nov 6 high) and 167.40, a Fibonacci retracement. Key short-term support lies at 161.09, the May 23 low, where a break is required to highlight a stronger reversal and suggest scope for a deeper correction.

- Conversely, a downtrend in EURGBP remains intact following a false breach of the 50-day EMA. A sustained break of this average is required to highlight a stronger reversal higher. On the downside, support to watch lies at 0.8356, the May 29 low. Clearance of this level would resume the downtrend and open 0.8316, the Mar 28 low and a key support.

FOREX: USD Index Holds JOLTS Rally, Hopes for US-China Breakthrough Dwindle

- The USD Index remains either side of the 99.00 handle, but is holding the majority of the rally off lows yesterday. Despite this recovery, the dollar remains well inside the downtrend drawn off the mid-May highs, with the firm downward bias in the 50-dma cementing the recent momentum lower.

- EUR trades off the overnight lows, either side of 1.1400 headed into the NY crossover having failed to make progress above 1.1455 yesterday. A stabilisation in the long-end of the EGB curve is helping contain the currency, although trade tensions and the risk of headlines remain at the forefront. EU's Sefcovic this morning stated that talks with the US are going in the right direction "at pace" - however markets are growing increasingly used to the slow progress made in negotiations with the White House.

- Similarly, Trump posted overnight that the Chinese President Xi is "extremely hard to make a deal with" - hampering sentiment somewhat, but the lack of follow through for currency markets is the latest signal that expectations for a near-term breakthrough are limited.

- The Bank of Canada rate decision takes focus going forward, with markets expecting no change on rates from the Bank although a not insignificant minority see risks of a further dovish tilt at the Bank. Markets see the BOC in a position to wait for further developments in the US-Canada trade dispute before pulling the trigger on further moves, incoming economic data have tilted toward a further hold. In particular, better-than-expected GDP and a pickup in core inflation should tilt the balance toward a hold.

- US ADP Employment Change is a calendar highlight, with the ISM services index for May set to follow. Markets continue to watch for any signals ahead of Friday's nonfarm payrolls print from the data, particularly in the context of yesterday's stronger-than-expected job openings numbers. Fed's Bostic & Cook are set to moderate a session at the Fed Listens event series.

OPTIONS: Expiries for Jun04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E1.5bln), $1.1250(E885mln), $1.1350-55(E1.2bln), $1.1400-05(E1.1bln), $1.1450(E1.3bln)

- USD/JPY: Y143.50($698mln), Y144.15-25($580mln), Y145.00($630mln)

- AUD/USD: $0.6435-55(A$1.7bln)

- USD/CAD: C$1.3600($560mln), C$1.3735-50($1.4bln), C$1.3800($621mln)

EQUITIES: Eurostoxx 50 Moving Average Studies Remain in Bull-Mode Position

- The trend cycle in Eurostoxx 50 futures remains bullish and a recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5262.93, the 50-day EMA. A clear break of this average is required to signal a possible reversal.

- The trend condition in S&P E-Minis is unchanged and remains bullish and the contract is trading just ahead of its recent high. A print above 5993.50 last week, the May 20 high and a bull trigger, highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. An extension would open 6057.00 next, the Mar 3 high. Key support lies at 5765.62, the 50-day EMA.

COMMODITIES: WTI Futures Close to Recent Highs But Bear Threat Remains Present

- WTI futures continue to trade closer to their recent highs. A bear threat remains present and the recovery since Apr 9 still appears corrective. A key resistance area to monitor is $62.51, the 50-day EMA. It has again been pierced. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger.

- A bullish theme in Gold remains intact and this week’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Sights are on $3435.6 next, the May 7 high. A break of this hurdle would strengthen bullish conditions. On the downside, key support and the bear trigger to watch has been defined at $3121.0, the May 15 low.

| Date | GMT/Local | Impact | Country | Event |

| 04/06/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/06/2025 | 1230/0830 | Atlanta Fed's Raphael Bostic | ||

| 04/06/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 04/06/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/06/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/06/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/06/2025 | 1430/1030 | BOC press conference | ||

| 04/06/2025 | 1800/1400 | Fed Beige Book | ||

| 05/06/2025 | - | European Central Bank Meeting | ||

| 05/06/2025 | 2330/0830 | ** | average wages (p) | |

| 05/06/2025 | 0130/1130 | ** | Trade Balance | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/06/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/06/2025 | 0545/0745 | ** | Unemployment | |

| 05/06/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 05/06/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 05/06/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/06/2025 | 0745/0845 | BOE's Greene Opening Remarks at Econdat Conference 2025 | ||

| 05/06/2025 | 0800/1000 | * | Retail Sales | |

| 05/06/2025 | 0830/0930 | Decision Maker Panel data | ||

| 05/06/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/06/2025 | 0900/1100 | ** | PPI | |

| 05/06/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 05/06/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 05/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 05/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 05/06/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1230/0830 | ** | Non-Farm Productivity (f) | |

| 05/06/2025 | 1230/0830 | ** | Trade Balance | |

| 05/06/2025 | 1245/1445 | ECB Press Conference | ||

| 05/06/2025 | 1400/1000 | * | Ivey PMI | |

| 05/06/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 05/06/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 05/06/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 05/06/2025 | 1600/1200 | Fed Governor Adriana Kugler | ||

| 05/06/2025 | 1620/1220 | BOC Deputy Kozicki speech |