MNI US MARKETS ANALYSIS - High Bar to Derail Sept Fed Cut

Highlights:

- Y/Y CPI seen ticking higher on both a headline and core basis

- High bar to derail Sept Fed hike, however, with over 20bps priced

- GBP improves as UK jobs data not as bad as feared

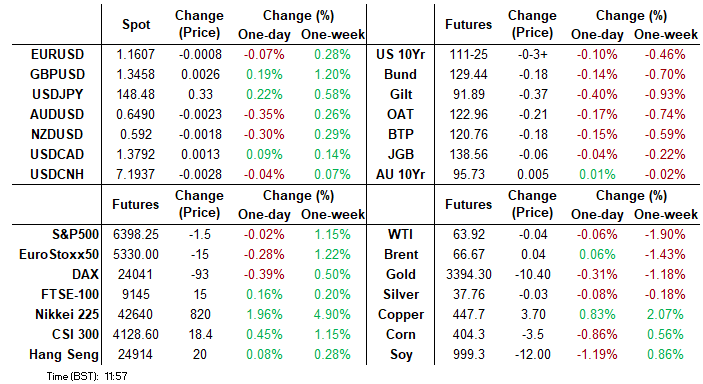

US TSYS: Little Changed Ahead Of CPI Report

- Treasuries are near unchanged across the curve ahead of the July CPI report (MNI CPI Preview).

- Cash yields are 0-0.5bp lower on the day across the curve, with 2Y yields at 2.768% hovering around a 38.2% retrace of the slide from 3.95% to 3.655% on the July payrolls report from Aug 1.

- TYU5 trades at 111-25 (-03+) on another thin session for overnight volumes nearing a cumulative 200k. The overnight low of 111-23 takes it a little further away from resistance at 112-15+ (Aug 5 high) whilst support isn’t seen until 110-19+ (Jul 24 low).

- Data: CPI Jul (0830ET), Real av earnings Jul (0830ET), Federal budget bal Jul (1400ET)

- Fedspeak: Barkin (1000ET), Schmid (1030ET) - see STIR bullet

- Bill issuance: US Tsy to sell $85B 6-W bills (1130ET)

- Politics: White House Press Secretary Leavitt Briefing (1300ET). A limited public schedule for President Trump but with post-CPI remarks watched after his extraordinary termination of BLS’s McEntarfer after this month’s weak payrolls report.

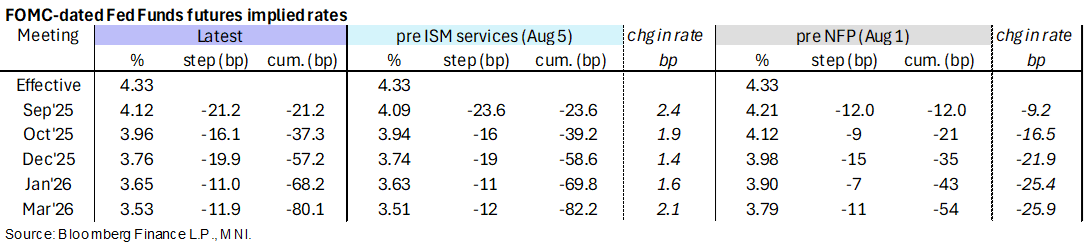

STIR: 21bp Fed Cut Seen Next Month Ahead Of CPI, Fedspeak To Follow

- Fed Funds implied rates have nudged a little higher for September (21bp cut priced, close to least since the Aug 1 NFP report) but are otherwise unchanged on the day ahead of CPI.

- MNI US CPI Preview: https://media.marketnews.com/USCPI_Prev_Aug2025_2fe4cdf4a1.pdf

- Cumulative cuts from 4.33% effective: 21bp Sep, 37.5bp Oct, 57bp Dec, 68bp Jan and 80.5bp Mar.

- The SOFR implied yield of 3.12% (SFRH7) is 1.5bp higher on the day having last closed higher prior to the July payrolls report on Aug 1.

- Today’s Fedspeak comes after US CPI:

- 1000ET – Barkin (non-voter) speaks at Health Management Academy (text + Q&A – no livestream). He last spoke on Jul 15, noting the most recent inflation data revealed some growing price pressures, and that more were on the way, with suppliers trying to pass on cost pressures to consumers who may not be able to absorb more price increases.

- 1030ET – Schmid (’25 voter, hawk) speaks on mon pol and economic outlook (text + Q&A). Previously one of the most hawkish members on the FOMC, he last spoke on Jun 25 saying he was watching data for signs of broad-based price increases. He also wanted to replace core inflation with a gauge that includes food.

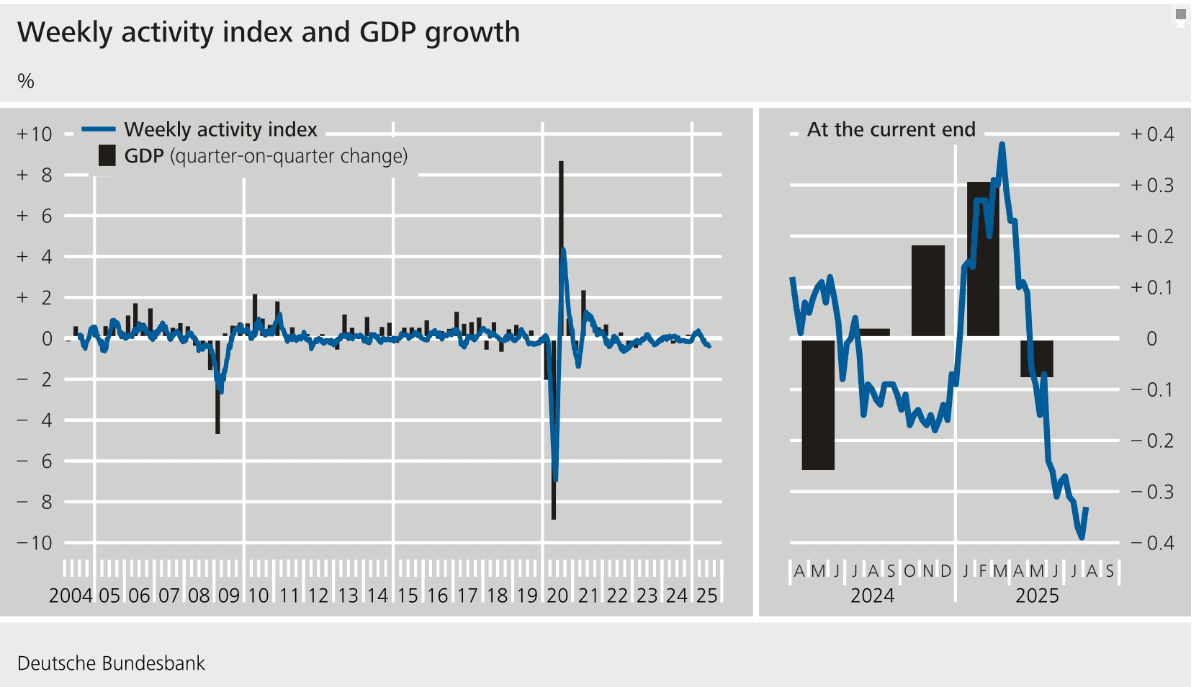

GERMAN DATA: Bundesbank Weekly Activity Tracker Holds Recent Deterioration

The Bundesbank weekly activity tracker firmly points towards weak developments in the first half of Q3 in Germany.

- Most recently published data (from yesterday) for the w/c August 3 implies a German GDP growth rate for the last 13 weeks compared with the preceding 13 weeks of -0.3%. The current weakness started to intensify in early June, coinciding with weak industrial activity data for that month (June Industrial Production Weaker Then Expected).

- Note that the indicator can see material revisions as more data is collected over time and tracking performance to GDP has not always been consistent (see charts below). For now though the trends indicated appear to be quite clear-cut, with the current period of weakness holding up weeks after the initial deterioration. Nevertheless, we do advise some caution around putting too much weight on the data.

- The WAI fluctuates around its long-term mean of 0. Positive values indicate above-average growth in real economic activity, while negative values signal a below average increase or a decline in economic output. The index takes into account data on electricity consumption, truck mileage, flight activity, foot traffic, air pollution, credit card payments, as well as German google searches for "unemployment", "short-time work", and "state support".

UKRAINE: 26 EU Leaders Reiterate Support For Kyiv Ahead Of Wednesday Trump Call

All but one of the European Union's member state leaders have added their signature to a statement reiterating their support for Ukraine, opposing any changes to the country's borders, and calling for Kyiv's direct involvement in any negotiations. The statement comes ahead of a high-profile meeting between US President Donald Trump and Russian President Vladimir Putin in Alaska on Friday, 15 August. At present, it is seen as unlikely, but not impossible, that Ukrainian President Volodymyr Zelenskyy is invited to take part as well.

- Hungarian Prime Minister Viktor Orban was the one holdout among EU leaders. Posting on X, Orban outlined his three reasons for not signing: "[1] The statement attempts to set conditions for a meeting to which leaders of the EU were not invited. [2] The fact that the EU was left on the sidelines is sad enough as it is. The only thing that could make things worse is if we started providing instructions from the bench. [3] The only sensible action for EU leaders is to initiate an EU-Russia summit, based on the example of the US-Russia meeting."

- The statement comes ahead of a call between European leaders and Trump on Wednesday, 13 August. As Politico notes, "European countries are now by far the largest source of financial and military support for Ukraine, and hold tens of billions of euros worth of frozen Russian assets crucial to any long-term peace settlement. Both factors make it difficult for Trump to ignore the European side."

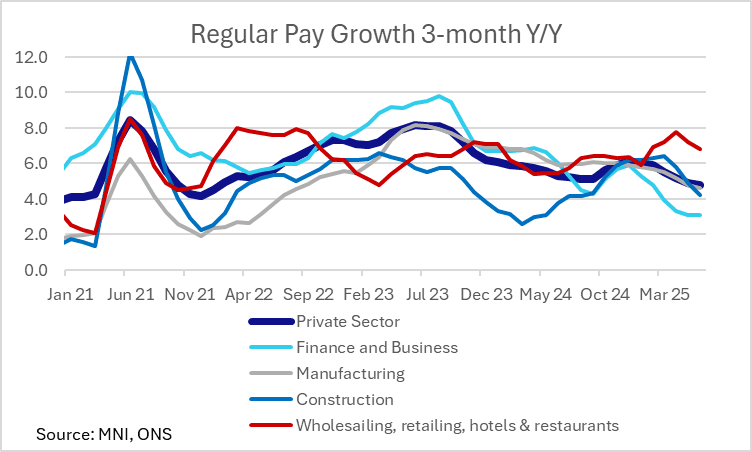

UK DATA: MNI UK Labour Market Review: August 2025 Release

- The August UK labour market release was on balance stronger-than-expected, with 3m/3m employment growth surprising to the upside and the unemployment rate holding steady despite some risks of a one tenth increase.

- However, private sector regular pay data remains consistent with the idea that wage growth is slowing. Meanwhile, data such as vacancies, RTI-PAY payrolls and other labour market metrics/surveys point to more subdued developments than the headline LFS figures suggest.

- We have argued that a continually softening labour market is a necessity for another quarterly cut in November. The August release was worth a modest hawkish reaction in BOE implied pricing, but there’s still far too much data (on both inflation and the labour market) to come before excluding a November cut. OIS markets currently price ~11bps of easing through that meeting.

EUROPE ISSUANCE UPDATE

Gilt auction results

- The 0.1bp tail is the tightest that has been seen for this line across eight auctions including the launch.

- 3.15x bid-to-cover ratio in line with the prior average.

- Lowest accepted price of 101.450 in excess of the 101.431 pre-auction mid.

- The secondary price of the Gilt has moved up to 101.440 at typing.

- Gilt futures have inched off lows since the results were published, though remain -28 ticks at 91.98 following this morning’s labour market data.

- GBP4.75bln of the 4.375% Mar-30 Gilt. Avg yield 4.022% (bid-to-cover 3.15x, tail 0.1bp).

Finland auction results

- E797mln of the 3.00% Sep-35 RFGB. Avg yield 3.05% (bid-to-cover 1.73x).

- E702mln of the 0.25% Sep-40 RFGB. Avg yield 3.411% (bid-to-cover 1.83x).

FOREX: GBP Improves as Jobs Data Not as Poor as Feared

- UK jobs data came in broadly inline with expectations however, looking through the headlines may suggest more limited space with which the BoE can ease policy into year-end, largely due to the decelerating pace of job losses and a surprisingly sticky unemployment rate for the June release.

- GBP has improved as a result, and is firmer against all others in G10. GBP/USD is testing yesterday's 1.3477 high for direction and clearance here would mark the highest rate since late July - marking a resumption of the bounce off early August's pullback low. The next notable upside level is the 1.3502 50-dma, a level that could prove consequential into Thursday's prelim Q2 GDP numbers.

- US CPI is the focus going forward, with markets expecting both Y/Y and Y/Y core to inch higher by 0.1ppts apiece. Despite firmer inflation, the numbers are not expected to deter the FOMC from trimming the policy rate at the September FOMC meeting - but a much firmer reading today could limit the scope for further cuts into year-end.

- AUD is softer on the RBA rate decision. AUD/USD has extended losses on the break back below the 50-dma, with 0.6468 the next level of note. The Bank cut rates by 25bps to 3.60%, and signaling strongly that further easing would follow. EUR/AUD has snapped yesterday's weakness as a result, making layered resistance at 1.7945 the focus.

- Central bank speakers today include Fed's Barkin and Schmid.

OPTIONS: Expiries for Aug12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.5bln), $1.1535-50(E1.2bln), $1.1650(E1.1bln)

- USD/JPY: Y147.30-50($1.6bln)

- AUD/USD: $0.6560-75(A$1.5bln)

- USD/CAD: C$1.3785($664mln)

EQUITIES: Eurostoxx 50 Futures Remain Above 50-Day EMA

The bounce off post-NFP lows in global equity indices has held, with the Eurostoxx 50 future still above the 50-day EMA. Additional strength refocuses attention on 5486.00, the May 20 high. To the downside, recent impulsive weakness did result in a temporary breach of the bear trigger - this makes the April 30 hi/lo range at 5078-5138 the area of downside interest. E-mini S&P prices recovered well Friday, meaning the bulk of the bounce off the NFP low is holding firm, keeping the underlying uptrend intact for now. The index holds above support at the 20-day EMA, at 6354.55. Through recent phases of weakness, the 50-day EMA at 6237.80, has held as support - and will be important on any intraday declines. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.

- Japan's NIKKEI closed higher by 897.69 pts or +2.15% at 42718.17 and the TOPIX ended 42.16 pts higher or +1.39% at 3066.37.

- Elsewhere, in China the SHANGHAI closed higher by 18.371 pts or +0.5% at 3665.918 and the HANG SENG ended 62.87 pts higher or +0.25% at 24969.68.

- Across Europe, Germany's DAX trades lower by 22.8 pts or -0.09% at 24059.48, FTSE 100 higher by 24.91 pts or +0.27% at 9154.53, CAC 40 up 27.52 pts or +0.36% at 7725.44 and Euro Stoxx 50 up 3.51 pts or +0.07% at 5335.08.

- Dow Jones mini up 51 pts or +0.12% at 44134, S&P 500 mini up 3.25 pts or +0.05% at 6402.75, NASDAQ mini up 4.5 pts or +0.02% at 23641.

COMMODITIES: Gold Reapproaches 50-Day EMA Support Following Monday's Weakness

WTI futures traded poorly Friday, cracking the 50-day EMA and piercing the bear trigger. This keeps S/T momentum pointed lower. The clear break exposes $58.17, the May 30 low. Gains early last week marked an extension of a corrective cycle - which may now have concluded. $69.41 marks the 50.0% retracement of the Jun 23-24 downleg - an important level at the close. A continuation higher would open $70.96 next, the 61.8% retracement point. Gold traded lower Monday, but last week's strength returned prices toward the top-end of the recent range and supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal is within close proximity to support at $3334.23, the 50-day EMA. A clear break of this level continues to signal scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high.

- WTI Crude down $0.11 or -0.17% at $63.84

- Natural Gas up $0 or +0.1% at $2.957

- Gold spot up $6.15 or +0.18% at $3349.07

- Copper up $3.15 or +0.71% at $447.1

- Silver up $0.17 or +0.46% at $37.7883

- Platinum up $8.07 or +0.61% at $1341.03

| Date | GMT/Local | Impact | Country | Event |

| 12/08/2025 | 1100/1200 | BOE APF Quarterly Report | ||

| 12/08/2025 | 1230/0830 | * | Building Permits | |

| 12/08/2025 | 1230/0830 | *** | CPI | |

| 12/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 12/08/2025 | 1400/1000 | Richmond Fed's Tom Barkin | ||

| 12/08/2025 | 1430/1030 | Kansas City Fed's Jeff Schmid | ||

| 12/08/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/08/2025 | 1800/1400 | ** | Treasury Budget | |

| 13/08/2025 | 0130/1130 | *** | Quarterly wage price index | |

| 13/08/2025 | 0600/0800 | *** | HICP (f) | |

| 13/08/2025 | 0700/0900 | *** | HICP (f) | |

| 13/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 13/08/2025 | - | *** | Money Supply | |

| 13/08/2025 | - | *** | New Loans | |

| 13/08/2025 | - | *** | Social Financing | |

| 13/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 13/08/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 13/08/2025 | 1730/1330 | Atlanta Fed's Raphael Bostic |