MNI US MARKETS ANALYSIS - Gov Shutdown Risks Rise, RBA Unch

Highlights:

- Government shutdown looks more likely than not, furloughs, data releases and politics in focus

- RBA keeps rates unchanged, Bullock won't be drawn on further rate cuts

- Busy central bank schedule, with high ranking BoE, Fed and ECB members all due

US TSYS: Month End, Military Heads to Quantico, Data, US Govt Shutdown Looming

- A lot happening heading into month end in addition to looming US govt shutdown at midnight (barring last minute resolution), Pres Trump and Sec of War Hegseth to address senior military leaders at Quantico while data picks up with housing prices, Consumer Confidence, MNI Chicago PMI, JOLTS.

- The BLS plans to postpone key economic releases in the event of a shutdown: "BLS will suspend all operations. Economic data that are scheduled to be released during the lapse will not be released. All active data collection activities for BLS surveys will cease. The BLS website will not be updated with new content or restored in the event of a technical failure during a lapse." LINK

- Treasuries are trading modestly mixed w/ Bonds lagging 2s-10s: Tsy Dec'25 10Y contract (TYZ5) currently trades at 112-19 (+2.5) on moderate cumulative volumes of 220k. 10Y yield at 4.1309% (-.0078). Curves twist steeper: 2s10s +.236 at 51.852, 5s30s +1.404 at 98.214.

- A short-term bear cycle in Treasury futures remains in play. Last Thursday’s sell-off resulted in a print below the 50-day EMA, currently at 112-10+. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. On the upside, initial firm resistance to watch is 113-00, the Sep 24 high.

- Economic Data: FHFA & S&P Cotality House Price Indexes (0900ET), MNI Chicago PMI (0945ET), JOLTS Jobs data (1000ET), Consumer Confidence (1000ET) and Dallas Fed Services Activity (1030ET).

- Treasury Auctions: $85B 6W & $50B 52W bills at 1130ET.

- Fedspeak: Fed VC Jefferson keynote speech earlier at 0600ET, Boston Fed Collins Council on Foreign Relations (0900ET), Dallas Fed Logan wraps up with a moderated discussion later this evening (1910ET).

- Politics: President Trump delivers remarks to the Department of War, Quantico (0900ET), returns to White House to make announcements (1100ET), executive orders signing (1500ET).

SOFR: Mix Of Long Setting & Short Cover Seen On Monday

OI data points to net short cover being most prominent through the green pack on the SOFR futures strip as contracts ticked higher on Monday (albeit with some pockets of net long setting seen), before net long setting came to the fore in the blues.

| 29-Sep-25 | 26-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,438,087 | 1,436,167 | +1,920 | Whites | -45,020 |

SFRZ5 | 1,489,912 | 1,505,824 | -15,912 | Reds | -6,212 |

SFRH6 | 1,185,343 | 1,208,730 | -23,387 | Greens | -1,152 |

SFRM6 | 1,023,669 | 1,031,310 | -7,641 | Blues | +13,649 |

SFRU6 | 924,075 | 935,770 | -11,695 |

|

|

SFRZ6 | 1,035,060 | 1,040,660 | -5,600 |

|

|

SFRH7 | 767,773 | 758,297 | +9,476 |

|

|

SFRM7 | 777,537 | 775,930 | +1,607 |

|

|

SFRU7 | 672,566 | 669,626 | +2,940 |

|

|

SFRZ7 | 723,797 | 727,425 | -3,628 |

|

|

SFRH8 | 416,357 | 415,720 | +637 |

|

|

SFRM8 | 358,549 | 359,650 | -1,101 |

|

|

SFRU8 | 278,227 | 266,456 | +11,771 |

|

|

SFRZ8 | 300,650 | 298,637 | +2,013 |

|

|

SFRH9 | 189,383 | 188,454 | +929 |

|

|

SFRM9 | 176,736 | 177,800 | -1,064 |

|

|

US TSY FUTURES: Mix Of Short Cover & Long Setting Seen On Monday

OI data points to a mix of net short cover (TU, FV & TY) and long setting (UXY, US & WN) as Tsy futures rallied on Monday.

- The curve-wide bias was tilted towards net long setting (in DV01 terms), owing to the ~$4.2mln DV01 equivalent of net long setting in WN futures.

| 29-Sep-25 | 26-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,545,907 | 4,558,432 | -12,525 | -424,890 |

FV | 6,684,536 | 6,729,775 | -45,239 | -1,985,770 |

TY | 5,435,162 | 5,452,089 | -16,927 | -1,104,028 |

UXY | 2,429,790 | 2,413,949 | +15,841 | +1,386,896 |

US | 1,818,387 | 1,805,689 | +12,698 | +1,802,161 |

WN | 2,026,338 | 2,004,016 | +22,322 | +4,178,293 |

|

| Total | -23,830 | +3,852,663 |

EUROPE ISSUANCE UPDATE

[EGB FUNDING UPDATE] Spain cuts net debt issuance target from E60bln to E55bln:

- Earlier this morning, Tesoro Publico announced that it was cutting its 2025 net issuance target by E5bln to E55bln due to "strong economic growth" in particular a strong labour market "with record numbers of taxpayers, which has resulted in lower financing needs."

- The Treasury notes that the stronger finances are in spite of the costs of Storm Dana and increased defence spending.

- 2025's net issuance target is now the same as 2024's.

Finland Q4 Funding Plan

- 2 RFGB auctions for E1.0-1.5bln each on 21 October and 18 November (in line with MNI's expectation).

- 2 ORI auctions in Q4 (these were scheduled previously, minor date change) on 30 October and 26 November.

- 2 RFTB auctions for E1.0-2.0bln each on 14 October and 11 November.

- "Government’s latest supplementary budget proposal for 2025 increased the net borrowing requirement to EUR 14.298 billion, which implies gross borrowing of EUR 43.753 billion. Long-term funding operations for 2025 are well advanced with all of the euro-denominated supply in syndicated form completed." In the Q3 funding plan, net borrowing requirements stood at E13.233bln, while gross requirements were 42.688bln.

- "The next Quarterly Review will be published on 19 December 2025."

- Full release here: https://www.treasuryfinland.fi/yleinen-en/quarterly-review-q3-2025/

AUD: RBA Tilts Hawkish, AUDCAD Approaching Bull Triggers

- Broad dollar weakness has boosted AUDUSD back above the 0.66 handle on Tuesday, with a cautious central bank providing an additional Aussie tailwind. Governor Michele Bullock declined to say whether the RBA retains an easing bias after the Board held the cash rate at 3.6%, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- Overall, the AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Initial firm resistance to watch is 0.6628 (Sep 24 high). A stronger reversal higher would refocus attention on 0.6707, the Sep 17 and post-Fed high.

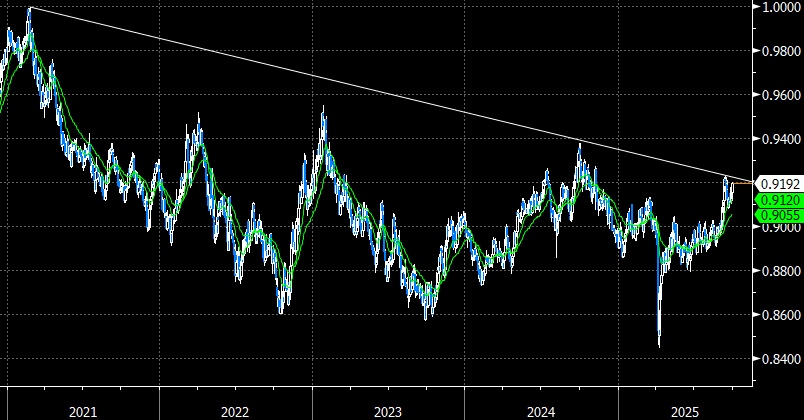

- Price action prompted another impressive surge for AUDNZD, rising to a fresh cycle high above 1.14, continuing to narrow the gap with the 2022 highs located at 1.1491. With risk reward for AUDNZD longs perhaps diminishing, AUDCAD (shown below) might be a better candidate to take advantage of additional AUD strength. Recent highs at 0.9227 are initial resistance, closely coinciding with trendline resistance, drawn from the 2021 highs. A breach would signal scope for a move to 0.9377, last year’s highs.

- Bullock highlighted stronger wealth effects from rising housing and asset prices, which could lift consumption and support growth. However, the RBA could still lower rates if the labour market loosens further and supply-demand imbalances ease, she said, with decisions dependent on forecasts and forward-looking indicators.

- Bullock welcomed the publication of full monthly CPI data set to launch in November, but reiterated the Bank's preference for quarterly results, noting the new series would require a transition period as seasonal patterns are established.

Source: Bloomberg Finance L.P. / MNI

FOREX: Yen Recovery Extends, GBPJPY Testing Below 50-day EMA

- Rising odds of a US government shutdown following the remarks from VP Vance have continued to weigh on the US dollar to start the week. USDJPY has been hardest hit, extending the week’s pull lower to around 1.3% at typing as spot consolidates back below 148.00.

- The move down appears technically corrective and initial support to watch lies at 147.59, the 50-day EMA. Stronger pivot support has been defined at 145.49, the Sep 17 low.

- We did highlight GBPJPY as a potentially vulnerable candidate to further yen demand, and the significance of the 50-day EMA. The cross is currently attempting to break below the average, which intersects at 198.98, and the next downside target would be 195.04, the August low.

- While the US shutdown and potential implications for US data releases remains the focus, it is worth highlighting that overnight the BOJ released the summary of opinions. The disclosures gave no clear signal of an October move, with most members aside from Naoki Tamura and Hajime Takata – who dissented and proposed a hike – seeing little urgency.

- Still, some members cited diminishing external risks and rising domestic pressures as reasons to shift. "Given this, the Bank may return to its monetary policy stance to raise the policy interest rate, and adjust the level of real interest rates that are currently low compared with overseas economies.”

FOREX: Gov Shutdown Still in Flux, AUD Rallies on Hesitant RBA

- The countdown to what will likely be the furthest reaching government shutdown in over 10 years continues, with betting markets looking toward a very high likelihood of a formal government shutdown starting from October 1st. Resultantly, haven currencies are bid and spot gold is key beneficiary, although the outlook for the USD is more complex.

- The USD Index remains pinned to the 50-dma of 98.043 - a level that's helped define price action since the beginning of August. The inability of the USD to build on last week's post-GDP rally will concern those looking for a firmer near-term bounce in the USD, with the Fed's views on a possible second rate cut in October a likely factor here.

- AUD trades well, with the cautious RBA decision overnight providing an additional Aussie tailwind. Governor Michele Bullock declined to say whether the RBA retains an easing bias after the Board held the cash rate at 3.6%, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive. Overall, the AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Initial firm resistance to watch is 0.6628 (Sep 24 high). A stronger reversal higher would refocus attention on 0.6707, the Sep 17 and post-Fed high.

- Data due today includes preliminary German CPI data. Regional numbers out already today suggest an uptick in inflation for this month, inline with the consensus view for today's +0.2% M/M, +2.3% Y/Y expectation.

- Today's MNI Chicago PMI, consumer confidence and JOLTS data may represent some of the last US data releases of the week, with a possible government shutdown likely curtailing the release of nonfarm payrolls due this Friday, as well as the CPI print due on October 15th.

- Central bank speak is far busier relative to the data schedule, with ECB's Rehn, Cipollone, & Nagel, Fed's Jefferson, Collins & Goolsbee and BoE's Lombardelli, Mann & Breeden all set to speak.

OPTIONS: Expiries for Sep30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-05(E2.4bln), $1.1695-00(E1.8bln), $1.1725(E528mln), $1.1775(E715mln), $1.1800(E1.8bln), $1.1825-30(E850mln), $1.1850(E878mln)

- USD/JPY: Y148.00($827mln), Y149.00-15($755mln)

- AUD/USD: $0.6595-00(A$1.3bln)

- NZD/USD: $0.5785(N$1.0bln)

INR: Rupee Slips to Fresh Record Low on Eve of RBI Rate Decision

USD/INR has edged marginally higher to a fresh all-time high, prompting intervention from the RBI to support the rupee – Reuters note, citing traders, that the central bank sold dollars to limit intraday volatility and prevent the currency’s record low from triggering a broader impact.

- Little substantive progress on reaching a trade deal with the US has been an ongoing headwind for the rupee, while a recent hike in US H-1B visa fees has compounded pessimism towards local assets.

- The visa fee issue could weigh on revenues in India’s technology sector and trigger renewed equity outflows, with foreign investors having already withdrawn more than $2bln from Indian stocks over the past six sessions. The Nifty 50 has fallen over 3% from the September highs.

- Weakness across Indian assets comes just ahead of the RBI’s October meeting tomorrow (05:30BST/10:00IST). While a majority of surveyed analysts (24 of 39 surveyed by Bloomberg) expect the central bank to keep the repo rate on hold at 5.50%, 15 expect a 25bp reduction, citing India’s worsening growth prospects.

- The rupee’s slump to a record low and Governor Sanjay Malhotra’s cautious approach to rate cuts raises the bar for easing, and we are of the view that the RBI will hold tomorrow and instead look ahead to the December meeting for its next rates adjustment. See our full preview here.

EQUITIES: Bull Cycle in E-Mini S&P Intact, Key Resistance at 6756.75

- Eurostoxx 50 futures maintain a bullish theme. Yesterday’s gains resulted in a breach of key resistance and the bull trigger at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend and paves the way for a climb towards 5564.82, a Fibonacci projection. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Initial firm support lies at 5442.85, the 20-day EMA.

- A bull cycle in S&P E-Minis remains intact. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, the contract has recently pierced initial support at the 20-day EMA, currently at 6647.54. A clear breach of this average would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6526.11.

COMMODITIES: Gold Hits Fresh Record High Just Shy of $3900

- WTI futures have pulled back from their recent gains. The contract has recently breached $65.43, the Sep 2 high and this has potentially improved the S/T condition for bulls. However, the next key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. For bears, a reversal lower would refocus attention on key support at $60.85, the Aug 13 low. A break of this level would reinstate the downtrend.

- The trend condition in Gold is unchanged and a bull cycle remains in play. The yellow metal has started the week on a bullish note, trading to a fresh cycle high, confirming a resumption of the primary uptrend. Note that MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on $3909.4, a Fibonacci projection. On the downside, support to watch lies at $3646.3, the 20-day EMA. A pullback would be considered corrective.

| Date | GMT/Local | Impact | Country | Event |

| 30/09/2025 | 1100/1300 | ECB Cipollone In Panel At Sibos | ||

| 30/09/2025 | 1150/1250 | BOE Lombardelli Panel On MonPol, Bank of Finland | ||

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1250/1450 | ECB Lagarde Keynote at MonPol Conference, Bank of Finland | ||

| 30/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 30/09/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/1500 | ECB Elderson In Panel On Climate Action | ||

| 30/09/2025 | 1300/0900 | Boston Fed's Susan Collins | ||

| 30/09/2025 | 1325/1425 | BOE Mann Fireside Chat At FT | ||

| 30/09/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/09/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 30/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 30/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 30/09/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 30/09/2025 | 1530/1630 | BOE Breeden Speech At Cardiff University | ||

| 30/09/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 30/09/2025 | 1600/1200 | ** | USDA GrainStock - NASS | |

| 01/10/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 30/09/2025 | 2310/1910 | Dallas Fed's Lorie Logan | ||

| 01/10/2025 | 2350/0850 | *** | Tankan | |

| 01/10/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/10/2025 | 0630/0830 | ** | Retail Sales | |

| 01/10/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0730/0930 | ECB Elderson Keynote at ECB Climate Conference | ||

| 01/10/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0755/0955 | ECB de Guindos Interview & Panel at Politico Summit | ||

| 01/10/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/10/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/10/2025 | 0900/1100 | *** | EZ HICP Flash | |

| 01/10/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 01/10/2025 | 0955/1055 | BOE Mann In Bloomberg Interview | ||

| 01/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 01/10/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/10/2025 | 1215/0815 | *** | ADP Employment Report | |

| 01/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) | |

| 01/10/2025 | 1400/1000 | *** | ISM Manufacturing Index | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1400/1000 | * | Construction Spending | |

| 01/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 01/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 01/10/2025 | 1730/1330 | BOC Summary of Deliberations | ||

| 01/10/2025 | 1805/1405 | BOC Sr Deputy Rogers speaks at competition panel |