MNI US MARKETS ANALYSIS - Global Bonds See Support Pre-Data

Highlights:

- Global bonds see support, helping pressure US, UK, German 10y yields to 2026 lows

- ISM services data due, eyed for reflection of Monday's weakness in manufacturing

- AUD upside demand persists despite more tempered inflation outlook

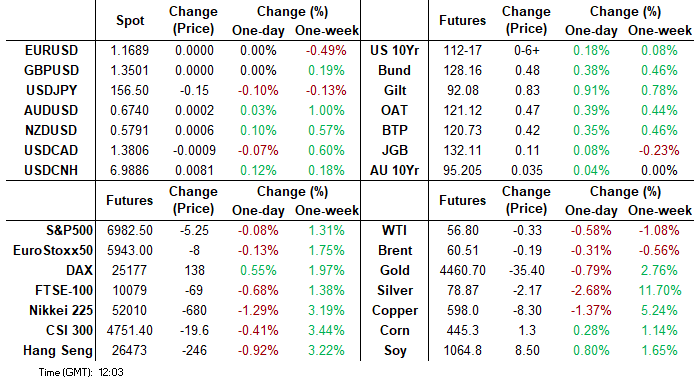

US TSYS: TYH6 Close To Resistance With ADP, ISM Services and JOLTS Ahead

Treasuries have firmed overnight, mainly in London hours, in a further reversal off yesterday’s lows with assistance from soft European data. The WSJ reported that Secretary of State Rubio told lawmakers that recent administration threats against Greenland didn’t signal an imminent invasion and that the goal is to buy the island from Denmark.

- Cash yields are 0.5-4.2bp lower on the day, with declines led by the long-end.

- 30Y yields trade at 4.823% for a sizeable pullback after briefly testing the 4.88% level three times yesterday.

- TYH6 trades close to session and week highs of 112-18 (+07) on reasonable cumulative volumes of 325k.

- It comes close to resistance at 112-19+ (50-day EMA) after which lies 112-25+ (Dec 30/31 high) as it shifts away from support at 112-01+ (Dec 23 low) and 111-29 (Dec 10 low, bear trigger).

- Data: MBA mortgage applications (0700ET), Monthly ADP Dec (0815ET), Chicago Fed CARTS (0830ET), ISM services Dec (1000ET), JOLTS Nov (1000ET), Factory orders Oct (1000ET),

- Fedspeak: Bowman on banking supervision (1610ET, text + Q&A)

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Press briefing by WH Press Sec Leavitt and other cabinet officials (1100ET), Trump signs Executive Orders (1430ET)

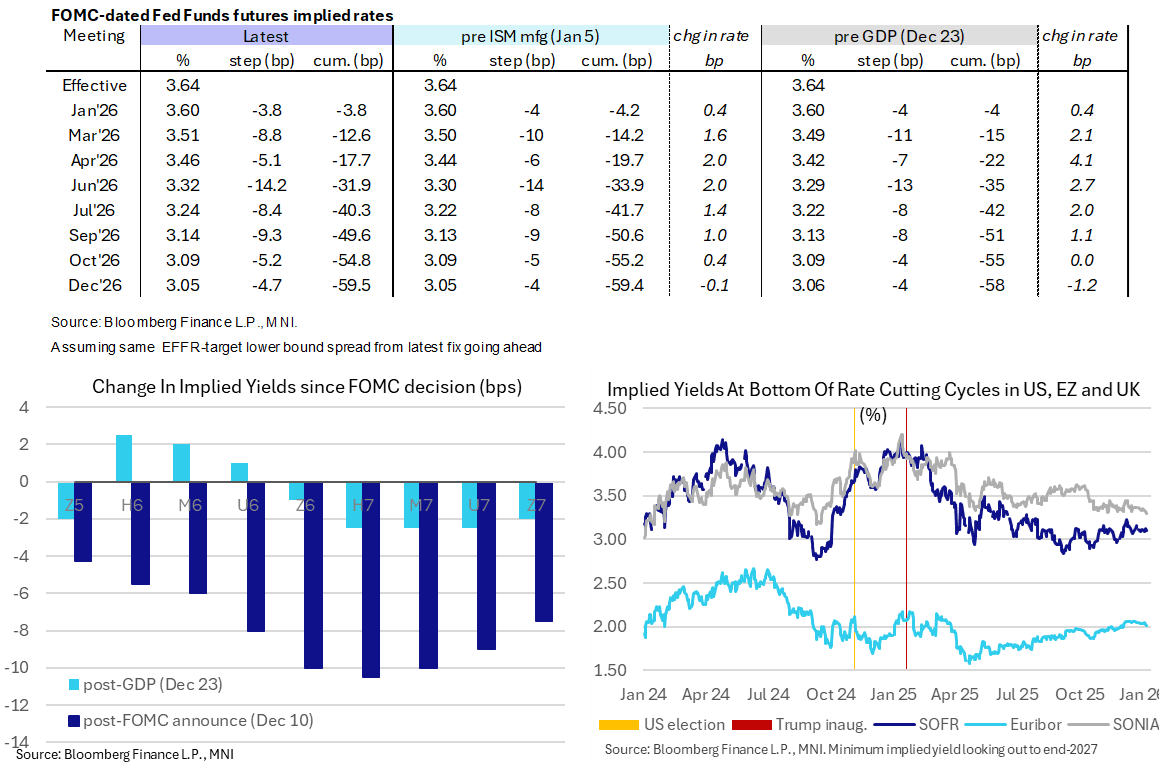

STIR: Holding Two Fed 2026 Cuts From June Ahead Of Important US Data

- Fed Funds implied rates are 0.5bp higher on the day for the late January FOMC meeting but 0.5-1bp lower for 2H26 meetings as they follow European rates after inflation data.

- It holds yesterday’s trimming of rate cut expectations for the remaining meetings under Fed Chair Powell (cumulative 17.5bp Apr) despite downward revisions for the S&P Global US services PMI.

- Cumulative cuts from 3.64% effective: 4bp Jan, 12.5bp Mar, 17.5bp Apr, 32.5bp Jun, 49.5bp Sep and 59.5bp Dec.

- SOFR futures are up to 2.5 ticks firmer looking out to end-2027 contracts vs 4.5 ticks for Euribor, with the SOFR terminal implied yield of 3.10% (H7) holding recent ranges.

- Today’s calendar focus is on data with monthly ADP at 0815ET before ISM Services, JOLTS and factory orders all at 1000ET.

- The Fedspeak schedule is light, with VC Supervision Bowman (voter) on banking supervision and regulation (1610ET, text + Q&A).

US TSY FUTURES: Mix Of Net Short Setting & Long Cover Seen On Tuesday

OI data points to a mix of net short setting (FV, TY & US) & long cover (TU, UXY & WN) as Tsy futures ticked lower on Tuesday, with the former being more prominent (~$2.4mln DV01 net short exposure added across the curve).

| 06-Jan-26 | 05-Jan-26 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,567,602 | 4,569,157 | -1,555 | -60,066 |

| FV | 6,734,954 | 6,731,990 | +2,964 | +129,764 |

| TY | 5,530,984 | 5,513,165 | +17,819 | +1,190,234 |

| UXY | 2,573,023 | 2,577,499 | -4,476 | -403,756 |

| US | 1,868,745 | 1,856,740 | +12,005 | +1,668,639 |

| WN | 2,092,516 | 2,093,420 | -904 | -163,634 |

| Total | +25,853 | +2,361,181 |

SOFR: Bias Towards Net Short Setting In Futures On Tuesday

OI data points to net short setting dominating (in pack terms) through the greens as most SOFR futures ticked lower on Tuesday.

- We can't provide any real inference when it comes to the blues, where prices were unchanged on the day come settlement.

| 06-Jan-26 | 05-Jan-26 | Daily OI Change |

| Daily OI Change In Packs |

SFRZ5 | 1,475,063 | 1,495,953 | -20,890 | Whites | +18,281 |

SFRH6 | 1,298,566 | 1,287,972 | +10,594 | Reds | +22,281 |

SFRM6 | 1,172,386 | 1,150,433 | +21,953 | Greens | +30,722 |

SFRU6 | 1,220,630 | 1,214,006 | +6,624 | Blues | -3,272 |

SFRZ6 | 1,194,582 | 1,169,316 | +25,266 |

|

|

SFRH7 | 866,124 | 863,396 | +2,728 |

|

|

SFRM7 | 758,450 | 759,212 | -762 |

|

|

SFRU7 | 792,979 | 797,930 | -4,951 |

|

|

SFRZ7 | 864,386 | 853,582 | +10,804 |

|

|

SFRH8 | 469,970 | 471,759 | -1,789 |

|

|

SFRM8 | 420,456 | 404,218 | +16,238 |

|

|

SFRU8 | 368,702 | 363,233 | +5,469 |

|

|

SFRZ8 | 348,133 | 348,698 | -565 |

|

|

SFRH9 | 215,390 | 217,749 | -2,359 |

|

|

SFRM9 | 216,336 | 215,124 | +1,212 |

|

|

SFRU9 | 169,479 | 171,039 | -1,560 |

|

|

SECURITY: Risks Abound As US Tracks Russian-Flagged Tanker In North Atlantic

A standoff could be developing in the North Atlantic, with at least one Russian naval vessel having been dispatched to guard an empty oil tanker that may be a target for US military interception, according to NYT and WSJ reports. The tanker was formerly known as the Bella 1. Having failed to dock in Venezuela to load oil, it evaded the US blockade of sanctioned vessels and steamed into the Atlantic in December, with its crew repelling US attempts to seize it. Reports suggest the tanker's crew changed the vessel's designation to 'Marinera' and painted a Russian flag on its hull in an effort to claim Moscow's protection.

- Newsweek reports the ship is currently between Iceland and the UK, traversing part of the GIUK gap, a key two-channel naval chokepoint in the North Atlantic.

- The UK Defence Journal reports, "The movement comes as evidence mounts that the United States is preparing a maritime interdiction operation to prevent the tanker reaching a safe haven [...] As Marinera progresses northward, open-source observers have identified a corresponding increase in Western intelligence, surveillance and reconnaissance activity across the North Atlantic.[...] the pattern and timing of these movements closely match known requirements for a compliant or non-compliant maritime boarding operation."

- The seizure of the Skipper tanker off the coast of Venezuela in December passed off relatively smoothly (albeit as an early indicator of US intentions towards Venezuela). However, a potential boarding operation in the North Atlantic on a nominally Russian-flagged tanker, with the reported close proximity of Russian naval vessel/vessels, presents a much higher risk of conflict escalation.

DENMARK: White House Raises Stakes In Greenland Bid w/'Military Option' Comments

The prospect of Greenland coming under the control of the US appears increasingly feasible amid statements from Washington, D.C., both bellicose and negotiatory in nature. Speaking on 6 January, White House Press Secretary Karoline Leavitt said that President Donald Trump views securing Greenland as "vital to deter our adversaries in the Arctic region," and that the administration is "discussing a range of options to pursue this important foreign policy goal, and of course, utilising the US military is always an option at the commander in chief's disposal."

- However, the WSJ reports that during the course of a briefing to senior members of Congress on 5 Jan, Secretary of State Marco Rubio indicated "recent administration threats against Greenland didn’t signal an imminent invasion and that the goal is to buy the island from Denmark", with the apparent aim of scaring Copenhagen and Nuuk into a peaceful handover.

- Kuno Fencker, a member of the pro-independence Naleraq party in the Greenlandic parliament posts on social media, "I am almost certain now, and the rumours are now that the US is coming up with a Compact of Free Association offer, which is much better than the current self-government law."

- COFAs are currently in place between the US and several small Pacific island nations. These deals give the US military free access to operate in the country in question, duty-free trade, while the US would also provide basic social functions. This option would not see Greenland become a state of the US, or even a territory with the same status as Guam or Puerto Rico.

EUROPE ISSUANCE UPDATE

Belgium syndication: Spread set

- EUR benchmark (MNI expects E7-8bln)of the new 10-year Jun-36 OLO. Spread set at MS+54bp (guidance was MS+56 area), Books in excess of E80bln.

Portugal 10-year mandate:

- "The Republic of Portugal has mandated Barclays, BBVA, BNP Paribas, CaixaBI, Citi and HSBC as Joint Lead Managers for a forthcoming 10-year Portuguese Government Bond (PGB) maturing on 13 June 2036. The syndicated transaction is expected to be launched and priced in the near future, subject to market conditions." From market source

- This again is in line with our expectations, we wrote in the MNI EGB Supply Daily: "We expect Portugal to launch a new 10-year Oct-36 OT in the first half of January. We pencil in a E4bln transaction size."

EFSF syndication: RfP sent

- The EFSF has sent a request for proposal on an upcoming transaction, subject to market conditions. This means a transaction tomorrow is likely, and comes fully expected as we’ve noted previously that an EFSF syndication was possible this week or next week.

Gilt auction results

- The bid-to-cover ratio of 3.50x was above December's 3.23x, November's 3.01x and October's 2.83x.

- The 0.2bp tail was in line with December's re-opening. Lowest accepted price of 100.660 was above the 100.645 pre-auction mid.

- The secondary price of the Gilt has climbed to a fresh session high in the minutes after the results were published, but core FI trades higher generally today.

- GBP4.25bln of the 4.125% Mar-31 Gilt. Avg yield 3.980% (bid-to-cover 3.50x, tail 0.2bp).

German auction results

- A technically uncovered 10-year Bund auction for the first time since October.

- Looking at grey price metrics it's also quite soft (but not super bad). Also bear in mind that as this is a launch, it is the largest 10-year Bund auction since July at E6.0bln and some of the smaller auctions in October saw far fewer bids.

- So a disappointing auction, but it's not terrible.

- E6bln (E4.542bln allotted) of the 2.90% Feb-36 Bund. Avg yield 2.83% (bid-to-offer 0.98x; bid-to-cover 1.29x).

FOREX: AUDUSD Extends Bull Wave Despite Cautious Sentiment And CPI

- Sentiment across crude/equity markets has been dented on Wednesday, amid President Trump announcing Venezuela oil shipments as well as growing concerns about US intentions regarding Greenland. This has filtered through to a moderately higher JPY and lower NOK, although aggregate moves have remained very contained.

- Despite the cautious tone, AUDUSD extended its recent bullish wave overnight, reaching a high of 0.6767 with topside levels of 0.6795 and 0.6858 the next chart points of note. This comes in the aftermath of Australian CPI data for November, in which underlying momentum remained elevated despite headline moving in the right direction for the RBA. Demand for AUD upside in options also persists, providing further evidence that markets are looking through any softness in the inflation data.

- For the Euro, the declaration of intent for Ukraine security guarantees signed by French President Macron and UK PM Starmer, as well as Eurozone HICP coming in marginally below consensus didn't move the needle. Commitments from the biggest military spenders in Europe are notable, but will mean little without continued US backing, and more material inflation downside would be needed over the coming months to put any ECB cut discussions back on the table again.

- A strong recovery from Monday’s low print in EURUSD highlights a potential reversal - the price pattern on Jan 5 is a bullish long legged doji candle. It is a bullish reversal pattern and highlights a key short-term support at 1.1659, the Jan 5 low.

- MBA mortgage applications, ADP employment change, ISM Services, JOLTS, and durable goods orders constitute today's heavy data calendar. This comes ahead of Friday's December NFP, in which a material downside would be needed to put even talks about a January FOMC cut on the table again.

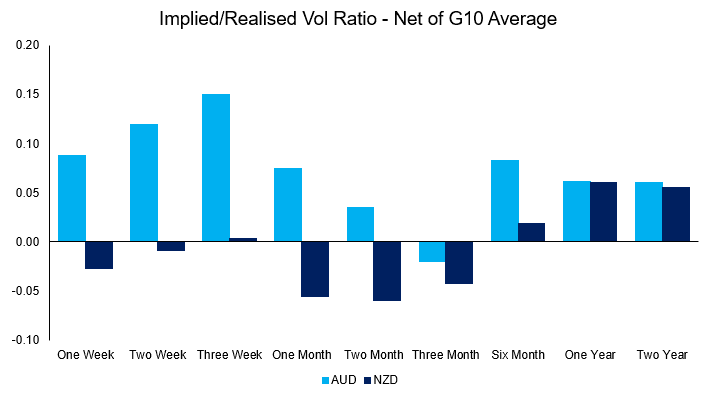

OPTIONS: Strong Start to the Year; AUD Upside Demand Persists

Global FX option markets are starting the year with a bang: over $250bln notional in currency options have traded since the beginning of this week, with yesterday's session the busiest in over three months.

- Better activity persists today, with outsized demand for HKD, JPY, AUD and AUDNZD structures setting markets up for another busy session.

- Mimicking the price action in spot markets, demand for AUD upside persists, providing further evidence that markets are looking through the somewhat softer-than-expected inflation print overnight.

- Over $3 in calls traded for every $1 in puts overnight, with strikes as high as 0.6925 in solid demand. Characterising the theme, strikes consistent with a 0.6800/0.6875 call spread traded on the spot rally, expiring on January 16th - thereby capturing the possible dates within which some speculate Trump could announce the next Fed chair.

- The extension of the AUD spot rally this year continue to lend support to the front-end of the vol curve - so much so that one-week out to two-month vol maturities continue to print a premium over the G10 average, in contrast with NZD:

OPTIONS: Expiries for Jan07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1725(E685mln), $1.1775(E1.4bln)

- USD/JPY: Y156.00($677mln), Y157.00($903mln)

- NZD/USD: $0.5650(N$1.1bln)

- USD/CAD: C$1.3800($1.3bln), C$1.3835($852mln)

EQUITIES: Eurostoxx 50 Futures Remain Close to 6000.00 Handle

- A bull cycle in Eurostoxx 50 futures remains intact and a fresh cycle high this week, reinforces the bull theme and confirms a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on the 6000.00 handle next. On the downside, initial firm support to watch is at 5795.81, the 20-day EMA. A pullback would be considered corrective.

- The trend condition in S&P E-Minis remains bullish. A key near-term support has been defined at 6771.50, the Dec 18 low. Clearance of this level is required to signal scope for a deeper retracement and would also highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. A move through this hurdle would confirm a resumption of the primary uptrend.

COMMODITIES: WTI Futures Reapproaching December's Cycle Lows

- The trend theme in WTI futures is unchanged, it remains bearish and recent gains appear to have been corrective. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would signal scope for a move towards $53.77, a Fibonacci projection. Key short-term resistance is $61.25, the Oct 24 high. First resistance is at $58.41, the 50- day EMA.

- The trend structure in Gold is bullish and a sharp sell-off late December appears corrective - for now. The trend is overbought and a deeper retracement would allow this condition to unwind. First support at $4351.9, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4215.8. For bulls, a resumption of gains would open $4578.3, a Fibonacci projection.

| Date | GMT/Local | Impact | Country | Event |

| 07/01/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 07/01/2026 | 1315/0815 | *** | ADP Employment Report | |

| 07/01/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | ** | Factory New Orders | |

| 07/01/2026 | 1500/1000 | *** | JOLTS jobs opening level | |

| 07/01/2026 | 1500/1000 | *** | JOLTS quits Rate | |

| 07/01/2026 | 1500/1000 | * | Ivey PMI | |

| 07/01/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 07/01/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/01/2026 | 2110/1610 | Fed Vice Chair Michelle Bowman | ||

| 08/01/2026 | 2330/0830 | ** | average wages (p) | |

| 08/01/2026 | 0030/1130 | ** | Trade Balance | |

| 08/01/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 08/01/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 08/01/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 08/01/2026 | 0730/0830 | *** | CPI | |

| 08/01/2026 | 0745/0845 | * | Foreign Trade | |

| 08/01/2026 | 0830/0930 | ECB de Guindos Fireside Chat at Next Spain | ||

| 08/01/2026 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 08/01/2026 | 0930/0930 | BOE Decision Maker Panel data | ||

| 08/01/2026 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 08/01/2026 | 1000/1100 | ** | EZ PPI | |

| 08/01/2026 | 1000/1100 | ** | EZ Unemployment | |

| 08/01/2026 | 1330/0830 | *** | Jobless Claims | |

| 08/01/2026 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 08/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 08/01/2026 | 1330/0830 | ** | Trade Balance | |

| 08/01/2026 | 1330/0830 | ** | Trade Balance | |

| 08/01/2026 | 1330/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 08/01/2026 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/01/2026 | 1500/1000 | ** | Wholesale Trade | |

| 08/01/2026 | 1500/1000 | ** | Wholesale Trade | |

| 08/01/2026 | 1530/1030 | ** | Natural Gas Stocks | |

| 08/01/2026 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/01/2026 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/01/2026 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/01/2026 | 2000/1500 | * | Consumer Credit | |

| 09/01/2026 | 2330/0830 | ** | Household spending |