MNI US MARKETS ANALYSIS - GBP/USD Still Struggles Above 1.34

Highlights:

- Treasury curve renews steepening bias ahead of Trump appearance at GOP meeting

- GBP/USD still struggles above 1.34; CPI print key

- AUD sinks as RBA signal less concern over inflationary pressure

US TSYS: Renewed Steepening, Trump To Speak At House GOP Meeting At 0900ET

- Treasuries trade twist steeper but have held to reasonably narrow ranges overnight.

- It follows yesterday’s clearance and then reversal back below 4.5% yields for the 10Y and the more notable 5.0% for the 30Y. The earlier sell-off was an extension of Friday’s US downgrade from Moody’s, the last of the major ratings agencies that had been marking the US as Aaa/AAA.

- Amidst a thin docket, any comments from President Trump with remarks at the House GOP Conference Meeting today at 0900ET could be particularly of note. The House is set for a mid-week vote on Trump’s “Big, Beautiful Bill”. It follows his Middle East trip last week and yesterday's call with Putin.

- Cash yields are 2bp lower (2s/3s) to 2.5bp higher (30s). The 10Y trades at 4.459% and 30Y at 4.931%.

- 5s30s has lifted to 87.2bp off yesterday’s low of 83.8bp but remains within ranges having touched 90.4bps yesterday for still within the ytd high of 100bp from May 1.

- TYM5 trades at 110-09 (+ 04+) on reasonable cumulative volumes of 340k.

- Support remains exposed after yesterday’s 109-20 came close to 109-18+ (May 15 low) after which lies a key 109-08 (Apr 11 low). Resistance meanwhile is seen at 110-23+ (20-day EMA).

- Data: Philly Fed non-mfg May (0830ET)

- Fedspeak: Bostic (0900ET), Barkin (0900ET), Collins (0930ET), Musalem (1300ET), Kugler (1700ET), Hammack and Daly (1900ET) – see STIR bullet

- Bill issuance: US Tsy sells $70 Bln 6-Week Bills (1130ET)

STIR: Fed Implied Rates A Touch Lower, Barkin and Musalem Pick Of Fedspeak

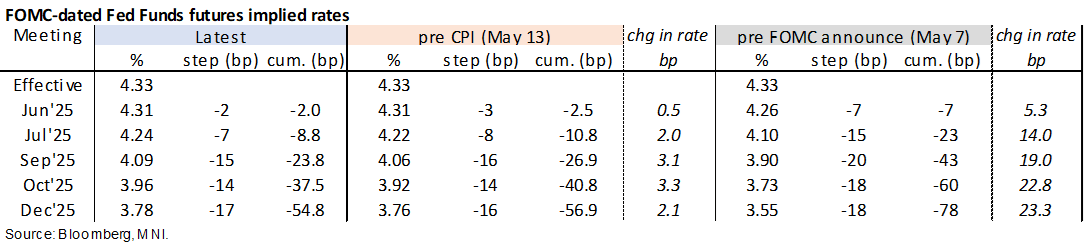

- Fed Funds implied rates are up to 1.5bp lower on the day for 2025 meetings, almost fully pricing a next cut with the September meeting.

- Cumulative cuts from 4.33% effective: 2bp Jun, 9bp Jul, 24bp Sep, 37.5bp Oct and 55bp Dec.

- SOFR implied yields are a little softer further out the curve, with the terminal yield 2.5bp lower at 3.335% (SFRZ6) having struggled to meaningfully shift away from ~100bp of cuts for the cycle.

- Yesterday saw NY Fed’s Williams even more explicit than usual in offering a rough timetable behind rate cut patience, with broader FOMC communications continuing to suggest that a cut before the end of summer is not in the frame.

- Amidst today’s second day with a solid Fedspeak docket, we focus on Barkin and Musalem for updates since the May 12 de-escalation in US-China trade policies and subsequent fiscal plans.

- Musalem, one of the most hawkish members on the FOMC, said May 10 that the Fed must ensure tariffs don’t lead to persistent inflation but it may tolerate higher inflation to lessen the employment cost. He added that trade de-escalation could get the economy back on track.

- Barkin on May 9 noted that consumer spending and business investment is still very solid although it’s not a given that firms can raise prices on tariffs.

- 0900ET – Bostic (non-voter) opening remarks in second day of Atl Fed Financial Markets conference

- 0900ET – Barkin (non-voter) speech at Richmond Fed conference (text only)

- 0930ET – Collins (’25 voter) brief remarks at Fed Listens event – won’t touch on current mon pol or outlook

- 1300ET – Musalem (’25 voter) speaks on the economy and mon pol (text + Q&A)

- 1700ET – Kugler (voter) commencement address (text only)

- 1900ET – Hammack (’26 voter) and Daly (non-voter) in panel discussion with Bostic (Q&A only)

EUROZONE DATA: An Even Larger Current Acct Surplus Plus Equity Profit Taking

- The Eurozone current account surplus increased further to E50.9bn (sa) in March after an upward revised E40.6bn in Feb (initial E34.3bn) and another large E40.3bn in Jan.

- There isn’t a Bloomberg consensus entry but the March increase shouldn’t have come as too much of a surprise considering the already known surge in the goods surplus on a jump in Irish pharmaceutical exports linked to US tariff front-running.

- The three-month current account surplus was worth circa 3.4% GDP (up from 2.2% GDP to Dec 2024). It’s comprised from a 3.1% goods surplus (vs 2.2%), a 1.0% services surplus (vs 1.2%), 0.2% primary income surplus (vs 0.1%) and a secondary income deficit of 0.9% (vs 1.3%).

- These current account and goods surpluses are right at the top end of recent historical ranges albeit with a temporary boost from tariff front-running.

- One of the more interesting areas within the financial account were equity flows.

- Net equity holdings from abroad had increased a strong E53.6bn in Feb after E11.3bn in Jan for the most since Aug 2024 and before that Dec 2023, but this abated in March with net selling worth E8.9bn (the first net sales since Mar 2024).

- This apparent profit-taking chimes with price action at the time, with global equity markets more generally rolling over in March. In the European case, the Eurostoxx 50 fell over the course of the month although to less extent than the US S&P 500. It came with the the realization of early March announcements on both EU and German defence and infrastructure spending after strong gains in Jan and Feb on growing expectations of greater European fiscal stimulus.

- Profit taking was likely bolstered ahead of the touted reciprocal tariff announcements due Apr 2. Indeed, it was seen on the other side of the ledger as well, with the E40.4bn net sale of resident equity holdings abroad the largest net sale since Sep 2022.

EUROPE ISSUANCE UPDATE:

Gilt syndication: Priced

- GBP4.0bln (smaller than MNI expected - that's the average size in the DMO's funding plan with no upsizing) of the new 5.375% Jan-56 gilt. Books closed in excess of GBP74bln pre-rec, spread set at 4.25% Dec-55 gilt (GB00BT7J0241) + 1.75bp (guidance was 1.75bp/2.25bp)

Germany auction results

- E1bln (E996mln allotted) of the 0% Aug-30 Green Bund. Avg yield 2.13% (bid-to-offer 3.75x; bid-to-cover 3.76x).

- E1bln (E921mln allotted) of the 1.80% Aug-53 Green Bund. Avg yield 3.01% (bid-to-offer 1.70x; bid-to-cover 1.85x).

Finland auction results

- E722mln of the 1.50% Sep-32 RFGB. Avg yield 2.702% (bid-to-cover 1.59x).

- E780mln of the 3.00% Sep-35 RFGB. Avg yield 3.011% (bid-to-cover 1.86x).

BONDS: Long-end Gilts Outperform Bunds Despite 30-year Syndi

German and UK yields are biased lower this morning, with the German curve lightly bull steepening and the Gilt curve bull flattening. Those dynamics come despite today’s syndicated launch of the new 5.375% Jan-56 gilt. Books are now closed and final terms have been set for the syndication, with the GBP4bln size smaller than MNI's expectations.

- The 10-year Gilt/Bund spread has tightened 2bps to 205.5bps this morning, but there hasn’t been an overt driver of the UK outperformance.

- The reaction to UK Chief Economist Pill’s opening remarks was relatively contained. Although Pill thinks the MPC started easing too early, he viewed May as the appropriate moment for a skip and seems to still broadly support quarterly cuts going forward.

- In the EGB space, Germany will sell green Bunds at 1030BST while Finland will issue RFGBs at 1100BST.

- Bund futures are +4 ticks at 130.58, off earlier session highs of 130.75. Gilt futures are +30 at 91.80, from a high of 91.91.

- Following a record high merchandise trade surplus ahead of US Liberation Day, the Eurozone seasonally adjusted current account surplus rose to E50.9bln in March (vs an upwardly revised E40.6bln prior). German April PPI was weaker-than-expected, but more interest will be in the flash Eurozone May consumer confidence reading at 1500BST.

- In the UK, focus remains on tomorrow’s April CPI report. MNI’s preview will be released later this morning.

FOREX: AUD Slips as RBA Considered Jumbo Rate Cut

- AUD is slipping against all others in G10 following the RBA rate cut to 3.85%. While the rate cut itself was expected, Bullock's more assertive language on easing ahead has pressured the front-end of the curve. The RBA disclosed that a 'jumbo' rate cut of 50bps was discussed - signaling the bank's approach to inflation is less restrictive than expected. As a result, AUD/USD has retreated away from any test of the 200-dma of 0.6452, reverting to the lower-end of the recent range in the pair.

- An uptick in oil prices has helped support commodity-tied currencies. Comments from Iran's Khamenei talked down the prospects of progress with the US in nuclear negotiations. Khamenei stated he does not believe talks with the US will yield any results - supporting Brent crude to briefly trade back to yesterday's highs. As a result, NOK is outperforming most others in G10.

- Broad EUR and GBP strength that played out across Monday has faded somewhat, however GBP/USD remains well toward the upper-end of the week's range. GBP/USD holds above 1.3350, but is yet to make any material challenge on the weekly high of 1.3404.

- Canadian CPI for April is the data highlight Tuesday, at which markets look for Y/Y CPI to slow to 1.6% from 2.3% previously. The Atlanta Fed's financial markets conference continues, while appearances are also due from Fed's Bostic, Barkin, Collins, Musalem and Kugler. Knot & Cipollone represent the ECB.

GBP/USD Still Struggling Above 1.34 Pre-CPI

The GBP trend condition is undoubtedly positive, with the pick-up in the S/T upside trend for spot evident in the growing premium of the 50-dma over the 200-dma - which now sits at its widest since October last year. This keeps the $1.3400 handle in focus, a level that markets have had difficulty in sustaining a move above on several occasions this year, as well as in 2019, 2020 and 2024. The keeps focus on the bearish tweezer candle formation printed on April 28/29, which could mark a near-term top.

- Overnight GBP vols have ticked higher ahead of the print, and now clear 10 vol points against the USD and 7 points against the EUR - although outright implied remains well below recent tariff-tripped highs. We see EUR/GBP vols as a cleaner read, which post a near 3 point vol premium into the CPI print - the largest pre-UK CPI premium of the year so far.

- As a result, a downside surprise for CPI tomorrow could see a correction lower of decent size, particularly as the market maintains a net long GBP position which, while off the year's best levels, still accounts for a net of 14.0% of open interest.

- 1.3342 undercuts as first support, ahead of the more meaningful 50-day EMA at 1.3126. A move through here would challenge the near-term bullish trend narrative.

OPTIONS: Expiries for May20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1015(E1.1bln), $1.1070-75(E1.8bln), $1.1100-05(E780mln), $1.1195-00(E1.5bln), $1.1245-50(E1.2bln), $1.1300(E1.1bln)

- USD/JPY: Y145.00($795mln), Y145.50($1.0bln), Y146.00($621mln)

- USD/CAD: C$1.3900-15($807mln)

EQUITIES: Eurostoxx 50 Futures Hit New Short-Term Cycle High

- A bullish theme in Eurostoxx 50 futures remains intact and price has traded to a fresh short-term cycle high. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg, and maintains the sequence of higher highs and higher lows. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5190.67, the 50-day EMA. Clearance of this level would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and the contract is holding on to its latest gains. An important resistance at 5837.25, the Mar 25 high and a bull trigger, has been cleared. This strengthens the current bullish theme, and paves the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5693.1, the 50-day EMA.

COMMODITIES: Corrective Cycle in Gold Still in Play, Price Close to Recent Lows

- A downtrend in WTI futures remains intact and recent gains are considered corrective. Key resistance to watch is $62.90, the 50-day EMA. It has recently been pierced, a clear break of it would highlight a stronger reversal. This would open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. Clearance of this support would confirm a resumption of the downtrend.

- A bearish corrective cycle in Gold remains in play and price is trading closer to its recent lows. A key support at $3202.0, the May 1, low has been breached. The break of this level signals scope for a deeper retracement, towards $3085.0, 76.4% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA at $3171.7, has also been breached, strengthening a bearish threat. Initial resistance is $3256.6, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 20/05/2025 | - | ECB's Lagarde and Cipollone at G7 Meeting | ||

| 20/05/2025 | 1230/0830 | *** | CPI | |

| 20/05/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 20/05/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 20/05/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/05/2025 | 1700/1300 | St. Louis Fed's Alberto Musalem | ||

| 20/05/2025 | 2100/1700 | Fed Governor Adriana Kugler | ||

| 20/05/2025 | 2300/1900 | San Francisco Fed's Mary Daly | ||

| 20/05/2025 | 2300/1900 | Atlanta Fed's Raphael Bostic | ||

| 20/05/2025 | 2300/1900 | Cleveland Fed's Beth Hammack | ||

| 21/05/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 21/05/2025 | 0600/0700 | *** | Consumer inflation report | |

| 21/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 21/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 21/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 21/05/2025 | 1600/1800 | ECB's Lane at Monpol Panel Discussion | ||

| 21/05/2025 | 1615/1215 | Richmond Fed's Tom Barkin, Fed Gov. Michelle Bowman | ||

| 21/05/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond |