MNI US MARKETS ANALYSIS - Firm EUR May Reflect Tariff Hopes

Highlights:

- Trumps ups the ante on tariffs, but EUR resilience may suggest optimism of last minute deal

- HKD sees no relief, despite higher front-end HIBOR fixings

- Geopolitics remains in focus with POTUS expected to make 'Major Statement' on Russia

US TSYS: Mildly Lower With Tariff Talk Deliberations And Russia Statement Eyed

- Treasuries trade mildly lower from Friday’s close, keeping to relatively narrow ranges for the session as they consolidate the sell-off seen Thu/Fri last week.

- President Trump has threatened 30% tariffs on EU and Mexico (its largest and second largest source of imports as of 2024 trade) ahead of an Aug 1 deadline. Talks will continue in the interim.

- Trump meets the NATO Secretary General Rutte at 1000ET and has also said a “major statement” on Russia is due.

- Cash yields are 0-1.5bp higher on the day.

- 30Y yields touched 4.9791% earlier (currently 4.965%) for highs since Jun 9 having last sustainably been above 5% in May.

- 5s30s of 99.1bps is elevated but remains below last month’s fresh ytd highs of 103.3bps.

- TYU5 is slightly higher at 110-26 (+03) as it roughly consolidates Friday’s decline to 110-22+, amidst slightly elevated cumulative volumes of 300k.

- Support at 110-21+ (Jul 8 low) and 110-17 (61.8% of May 22 – Jul 1 bull leg) holds for now, with declines undermining a previous bull theme.

- Data: None

- Fedspeak: None

- Bill issuance: US Tsy sell $82bn 13-W and $73bn 26-W bills (1130ET)

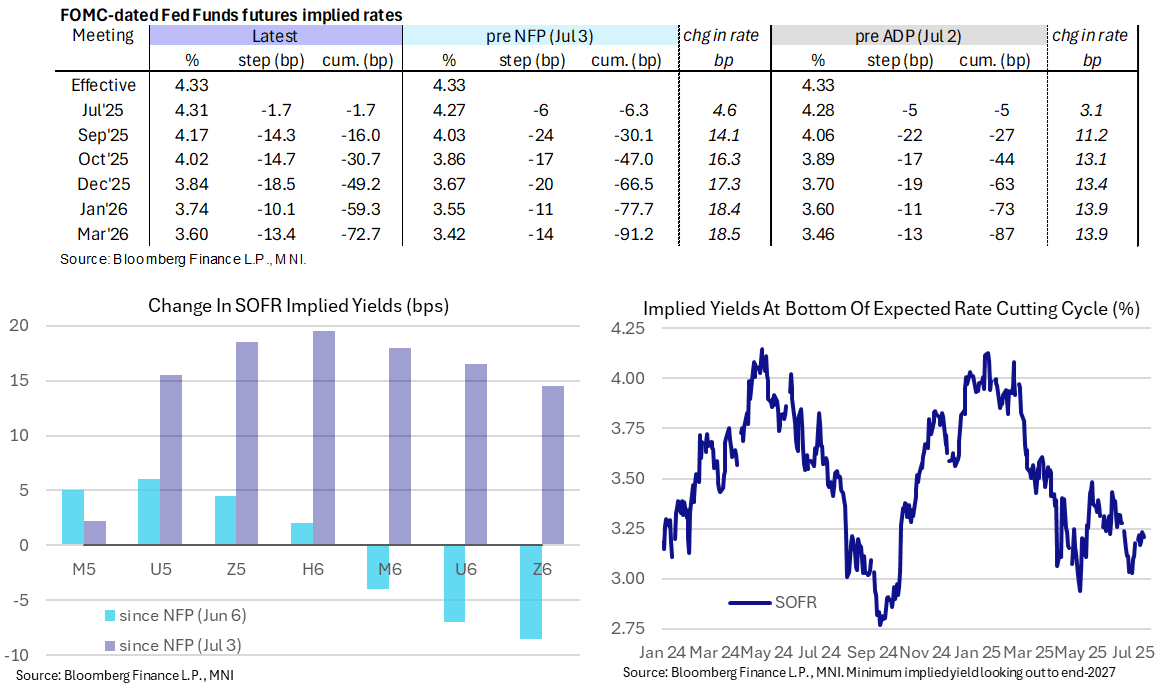

STIR: Least Conviction On Sept FOMC Cut In A Month

- Fed Funds implied rates are up to 1.5bp higher from Friday’s close for near-term meetings after President Trump’s weekend threats of 30% tariffs on the EU (the largest source of US imports) ahead of a Aug 1 deadline.

- Trump talking up an upcoming “Major Statement” on Russia has also supported oil futures.

- Increases in implied rates are quickly limited further out the curve owing to the associated growth concerns, with the Mar 2026 rate just 0.5bp higher for example.

- Cumulative cuts from 4.33% effective: 1.5bp Jul, 16bp Sep, 30.5bp Oct, 49bp Dec, 59bp Jan and 73bp Mar.

- Similarly, SOFR futures trade flat to 3 ticks firmer on the day.

- The SOFR implied terminal yield of 3.21% (SFRZ6, -2.5bp) inches lower after Friday’s close of 3.235% was the highest since Jun 20.

- It's a particularly thin docket today, with no notable data or Fedspeak. US CPI looms large tomorrow - the MNI Preview will be out later today but we currently see unrounded estimates for core CPI with a median of 0.24% or average of 0.26% M/M, suggesting downside risk to broad Bloomberg consensus of 0.3%.

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen Friday

OI data points to net short setting in TU, FV & WN futures on Friday, which outweighed net long cover across TY, UXY & US futures.

- A reminder that futures sold off on feedthrough from hawkish CAD rate repricing that followed local labour market data and as swap spreads tightened (some linked the latter to setup for this week's IG supply).

| 11-Jul-25 | 10-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,361,881 | 4,332,538 | +29,343 | +1,109,329 |

FV | 7,072,259 | 7,039,055 | +33,204 | +1,426,239 |

TY | 4,886,489 | 4,896,647 | -10,158 | -667,329 |

UXY | 2,434,824 | 2,442,227 | -7,403 | -641,537 |

US | 1,816,179 | 1,819,810 | -3,631 | -495,817 |

WN | 1,964,372 | 1,954,444 | +9,928 | +1,786,271 |

|

| Total | +51,283 | +2,517,157 |

SOFR: Mix Of Cover & Short Setting Most Prominent On Friday

OI data points to net cover across the SOFR whites (short cover in SFRM5, long cover elsewhere), before net short setting came to the fore further out the strip.

| 11-Jul-25 | 10-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,295,809 | 1,298,370 | -2,561 | Whites | -38,021 |

SFRU5 | 1,192,070 | 1,218,425 | -26,355 | Reds | +1,806 |

SFRZ5 | 1,315,380 | 1,320,764 | -5,384 | Greens | +13,432 |

SFRH6 | 986,539 | 990,260 | -3,721 | Blues | +16,130 |

SFRM6 | 853,365 | 835,534 | +17,831 |

|

|

SFRU6 | 817,821 | 832,140 | -14,319 |

|

|

SFRZ6 | 880,985 | 892,434 | -11,449 |

|

|

SFRH7 | 725,298 | 715,555 | +9,743 |

|

|

SFRM7 | 668,931 | 671,852 | -2,921 |

|

|

SFRU7 | 473,340 | 474,050 | -710 |

|

|

SFRZ7 | 430,517 | 418,417 | +12,100 |

|

|

SFRH8 | 318,794 | 313,831 | +4,963 |

|

|

SFRM8 | 240,132 | 230,934 | +9,198 |

|

|

SFRU8 | 205,232 | 204,571 | +661 |

|

|

SFRZ8 | 209,350 | 201,403 | +7,947 |

|

|

SFRH9 | 139,452 | 141,128 | -1,676 |

|

|

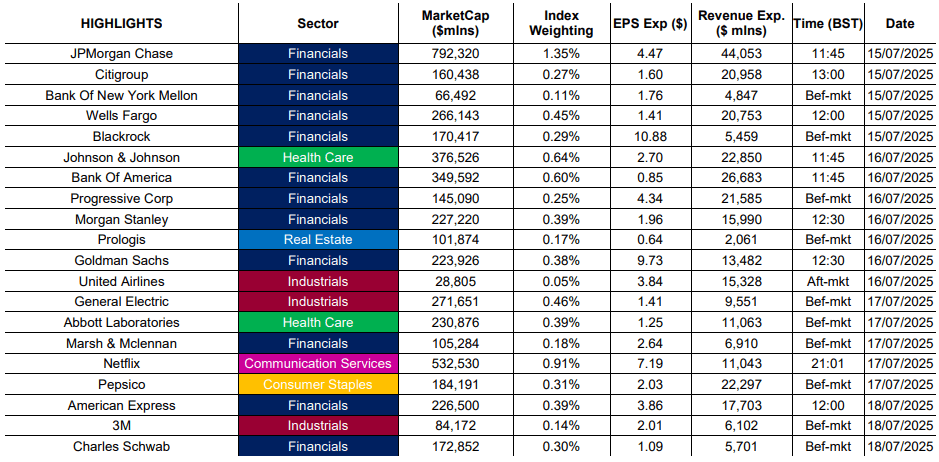

EQUITIES: An Unusually Busy Start to Quarterly Earnings Season

As noted above, quarterly earnings season kicks off in earnest today, and it's an unusually busy start to the quarter. 9.4% of the S&P 500's market cap is set to report, with the usual early focus on big banks and financials. Our full quarterly earnings schedule found here, including EPS, revenue expectations and full timings: https://mni.marketnews.com/44tWRA8

Highlights are:

- TUES: JP Morgan, Citigroup, BNY Mellon, Wells Fargo, Blackrock

- WEDS: Johnson & Johnson, Bank of America, Morgan Stanley, Goldman Sachs

- THURS: General Electric, Netflix, PepsiCo

- FRI: American Express, 3M, Charles Schwab

Tariffs remain a key buzzword in corporate reports. Heavy industry including General Electric, Snap-On and 3M which be watched for possible impacts, Markets will be particularly focused on any signs of frontloading of corporate purchases, the rate at which firms will passthrough costs to the consumer, and the expected impacts of tariffs on the bottom-line for consumer staples.

US-RUSSIA: Trump Expected To Announce UKR Weapons Package, Endorse RU Sanctions

10:00 ET 15:00 BST: President Donald Trump will hold a (closed press) White House meeting with NATO SecGen Mark Rutte, where he is expected to finalise a new plan to arm Ukraine “that is expected to include offensive weapons,” per Axios. Later today, Trump is expected to make a 'major statement' on Russia. No timing has been released.

- Axios reports the plan is likely to include long-range missiles that could reach targets "deep inside Russian territory” a “major shift for Trump, who had until recently [said] he would provide only defensive weapons to avoid [escalation].”

- Politico reported the weapons package "numbers in the hundreds of millions”, and “could come from the fund approved by [Biden] that lets the DOD give weapons from the U.S. military stockpile...”

- Trump's 'major statement' is also likely to include preliminary approval of Senator Lindsay Graham's (R-SC) punitive sanctions/tariffs bill, reworked to provide Trump full discretion over implementation.

- Graham said on X: “.... A turning point is coming.” He told Axios: "Trump is really pis--- at Putin. His announcement tomorrow is going to be very aggressive."

- Senate Majority Leader John Thune (R-SD) indicated the bill will hit the Senate next week. House Speaker Mike Johnson (R-LA) endorsed the bill, putting it on a track to Trump’s desk.

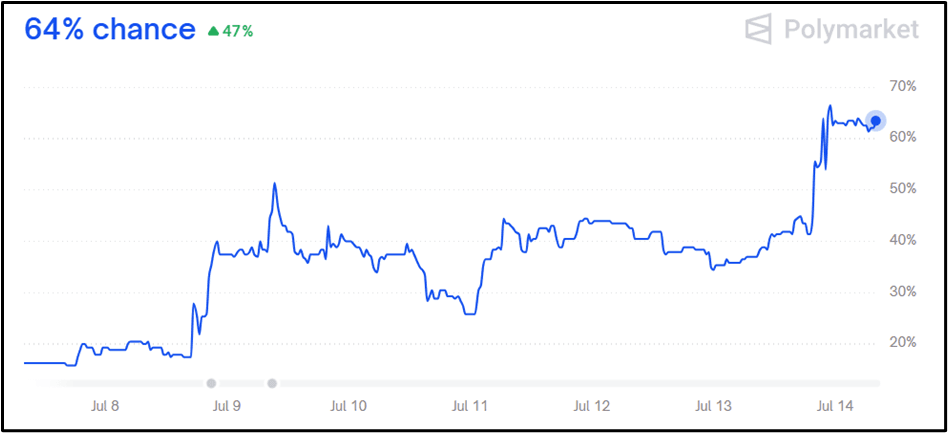

- Polymarket sees a 64% chance Trump increases Russia sanctions before August, a significant spike since last week.

Figure 1: Trump increase sanctions on Russia before August?

Source: Polymarket

HKD: No Relief for Weak-side of HKD Band, Despite Higher HIBOR Fixings

- Front-end HIBOR fixings came in higher again overnight (overnight up to 0.20%, one-month up to 1.1486%, both of which are the highest levels since the move to the weak-side of the band last month), however term rates remain more subdued, with one-year HIBOR still lower than mid-June levels and fixing roughly unchanged at 2.9241% today.

- Despite the nascent signs of recovery in HIBOR, FX swap rates remain under pressure. Both overnight and one-week HKD funding rates have struggled to hold above 0.4% despite the lower aggregate balance and higher HIBOR fix. It's these rates that will need to recover to fully endorse a pull lower in USD/HKD which signals the aggregate balance needs to reach a lower equilibrium from here, despite recent intervention phases.

- With higher HIBOR fixings and a lower aggregate balance, why aren't FX swap rates normalising? HKMA's Yue wrote after the local close on Friday that HKD funding demand was strong across May and June, but this waned late last month, and remains the case in mid-July. He highlighted the passing of the seasonal peak in dividend payments, foreign firms repatriating HKD proceeds from capital markets activities as well as fading half year-end funding demand. He did not reference market rumours that HIBOR was being artificially supressed to help aide the refinancing of New World Development Co.'s loan portfolio.

- This leaves focus on corporate activity in H2. Sizeable demand for securities can help narrow the HKD forward discount, which has proved sensitive in recent years to a pick-up in capital markets. This has been muddied in recent weeks by the much-anticipated confidential IPO filing for Shein Group. Reportedly, Shein filed in Hong Kong last week - but the prospectus is confidential, meaning the company keeps some details of the float private for a longer period. This bucks the usual practice for big Hong Kong floats and may muddy valuation estimates, distort demand for exposure and potentially restrain any impact on local rates relative to a public float of the same size.

FOREX: EUR and MXN Unfazed by Latest Global Tariff Developments

- Despite President Trump threatening to impose 30% tariffs on the EU and Mexico, both the Euro and the Mexican peso have taken the news in their stride as markets remain cautiously optimistic that more lenient deals may be struck before the August 01 deadline. These limited reactions, and the lack of data on Monday keeps the dollar index within close proximity to Friday’s close.

- For EUR specifically, the brief bout of initial weakness did prompt a fresh pullback low at 1.1651 and notably, the 20-day EMA has been pierced. However, the lack of follow through shows that these shallow dips remain corrective, keeping bullish sentiment firmly intact for now. The July 01 high of 1.1829 remains the bull trigger for the pair.

- In similar vein, the USDMXN trend remains bearish, reinforced by fresh cycle lows for the pair last week. Potential is seen for a bearish extension towards 18.4302, the Aug 01 low.

- Elsewhere in G10, the likes of AUD and NZD are both underperforming in G10, however, it’s the Kiwi’s relative weakness that is helping AUDNZD extend its most recent upswing. The cross looks set to extend its winning streak to six consecutive sessions, shifting the upside target to 1.1032, the April 01 high.

- Tuesday’s data calendar is stacked with China activity figures kicking things off. The focus will then swiftly turn to US and Canadian inflation data, final inputs before both the Fed and BOC decisions on July 30. We will also have the beginning of quarterly earnings season with financials the usual early focus.

OPTIONS: Sizeable Strikes in EUR/USD Could Contain Intraday Strength

Larger FX options rolling off at the cut today include some sizeable strikes in EUR/USD that could contain any intraday strength, while EUR/GBP and AUD/USD also see smaller, but very close-to-market interest:

- EUR/USD: $1.1600-05(E1.5bln), $1.1615-25(E1.6bln), $1.1650(E1.2bln), $1.1700(E853mln), $1.1725-40(E2.3bln) $1.1800($1.5bln)

- GBP/USD: $1.3590-05(Gbp565mln)

- EUR/GBP: Gbp0.8650(E581mln), Gbp0.8695-00(E882mln)

- AUD/USD: $0.6560(A$631mln)

- USD/CAD: C$1.3660-75($527mln)

COMMODITIES: Crude Sees Support Ahead of Trump's 'Major Statement' on Russia

The bull cycle in Gold that started Jun 30, remains intact and the yellow metal is holding on to its recent gains. Note that medium-term trend conditions are bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend. WTI futures maintain a bearish tone following the reversal from the Jun 23 high, and recent gains still appear corrective. Support to watch is the 50-day EMA, at $65.39. The average has been pierced, a clear break of it would signal scope for a deeper retracement.

EQUITIES: Stocks Hold Bullish Poise Into Earnings Season

The trend condition in S&P E-Minis remains bullish and short-term weakness is considered corrective. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend that started Apr 7. Eurostoxx 50 futures traded higher last week as the contract extended the recovery that started Jun 23. This exposed key resistance and the bull trigger at 5486.00, the May 20 high. It has been pierced, a clear break of it would confirm a resumption of the medium-term bull cycle.

| Date | GMT/Local | Impact | Country | Event |

| 14/07/2025 | 1230/0830 | ** | Wholesale Trade | |

| 14/07/2025 | 1500/1700 | ECB Cipollone At EU Parliament | ||

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/07/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 15/07/2025 | 0200/1000 | *** | GDP | |

| 15/07/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/07/2025 | 0200/1000 | *** | Retail Sales | |

| 15/07/2025 | 0200/1000 | *** | Industrial Output | |

| 15/07/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 15/07/2025 | 0700/0900 | *** | HICP (f) | |

| 15/07/2025 | 0900/1100 | ** | Industrial Production | |

| 15/07/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/07/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 15/07/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/07/2025 | 1315/0915 | Fed Vice Chair Michelle Bowman | ||

| 15/07/2025 | 1645/1245 | Fed Governor Michael Barr | ||

| 15/07/2025 | 1845/1445 | Boston Fed's Susan Collins | ||

| 15/07/2025 | 2000/2100 | Mansion House: Chancellor Reeves and BOE Bailey | ||

| 15/07/2025 | 2245/1845 | Dallas Fed's Lorie Logan |