MNI US MARKETS ANALYSIS - Fed Rate Path Edges Higher

Oct-20 11:08By: Edward Hardy

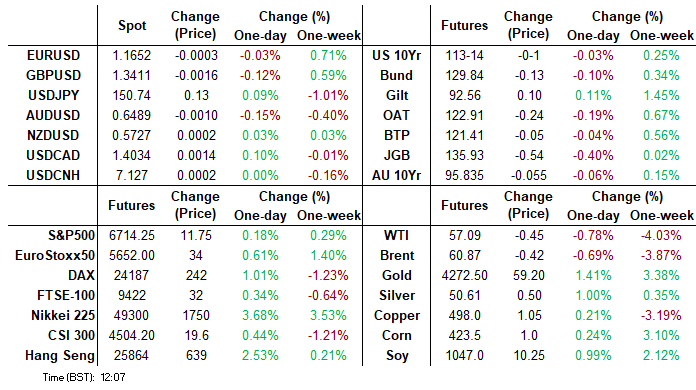

US

Highlights:

- Fed rate path creeps higher as Trump affirms optimism on US-China relations

- LDP, Ishin seal coalition deal, paving way for Takaichi premiership

- No data, FOMC inside media blackout leaves focus on geopolitics

US TSYS: Mild Pullback Doesn’t Alter Bullish TY Outlook

- Treasuries are mildly lower across the curve, slowly extending Friday’s more pronounced paring of regional bank risk-off that had started on Thursday.

- They marginally outperform EGBs where France leads losses after S&P’s unscheduled downgrade on Friday.

- President Trump over the weekend expressed optimism around US-China trade talks but with clear focus points on rare earths, fentanyl and soybeans before those talks.

- The session is likely to be driven by headlines/flows, with no data scheduled and the Fed in blackout. One area of attention will be Trump comments when meeting with the Australia Prime Minister late this morning.

- Cash yields are 0.2-1.2bp higher across the curve, within Thu-Fri ranges.

- TYZ5 trades at 113-12+ (-02+) off an earlier low of 113-10+, on thin cumulative volumes of 230k.

- The outlook remains bullish. It has pulled away from last week’s high of 114-02 (Oct 14 high) after clearing notable resistance levels, with next key resistance now seen at 114-10 (Apr 7 continuation). Support is seen at 113-00 (20-day EMA).

- No data scheduled and Fed now in media blackout

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump in bilateral meeting with Australia PM (1115ET) before bilateral lunch (1145ET)

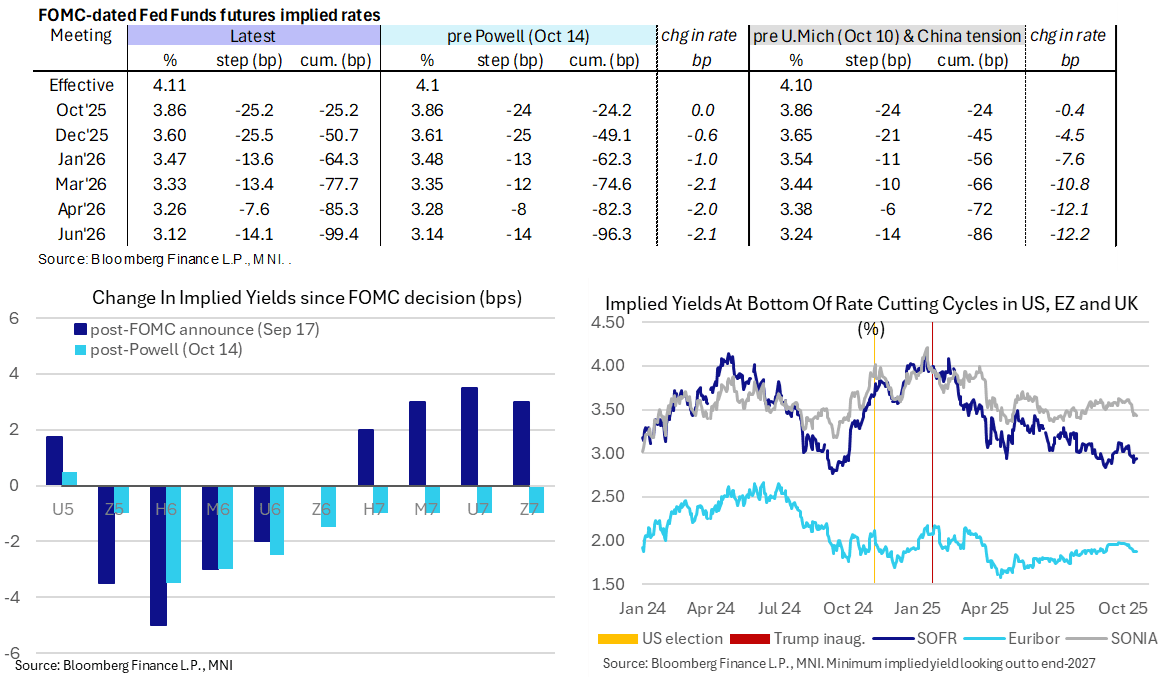

STIR: Fed Rate Path Mildly Higher On Cautious Optimism

- Fed Funds implied rates are modestly higher from Friday’s close, mirroring equity futures in cautious optimism on US-China trade talks ahead of a Trump-Xi meeting at the end of this week.

- They’re back to fully pricing 2x25bp cuts in the two meetings left this year having hit ~20% odds of a 50bp cut at the Dec meeting early Friday morning on US regional bank concerns.

- Cumulative cuts from an assumed 4.11% effective: 25bp Oct, 50.5bp Dec, 64.5bp Jan, 77.5bp Mar, 85.5bp Apr and 99.5bp Jun.

- SOFR futures are broadly 1-1.5 ticks lower on the day.

- The SOFR implied terminal yield of 2.945% (SFRZ6) is 1.5bp higher as it continues to slowly pull away from Thursday’s 2.89% close at what was the lowest in a month. Cycle lows are seen at 2.77% from Sep 2024.

- The FOMC is now in media blackout ahead of the Oct 29 FOMC decision.

- The ongoing US government shutdown further restricts data this week, leaving Friday’s CPI report for September the clear headline (with the BLS making an exception for the release on social security payment grounds).

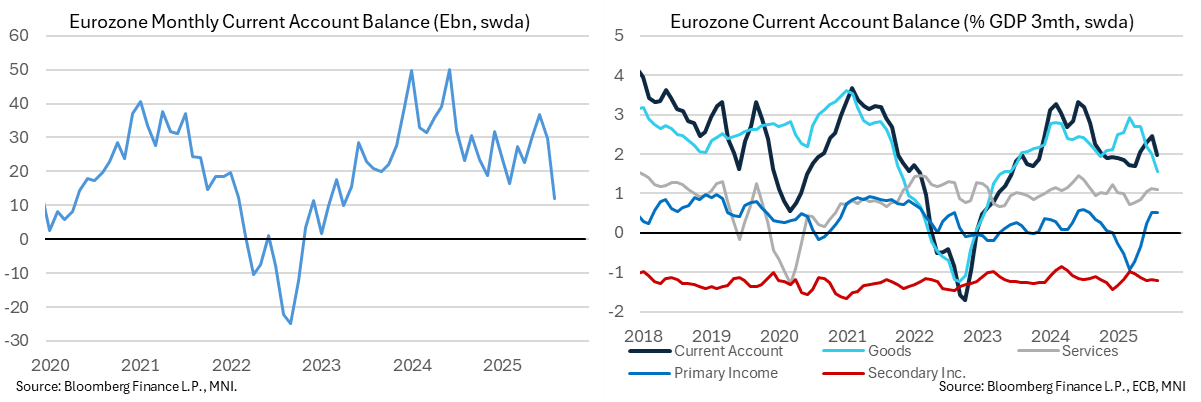

EUROZONE DATA: Smallest Current Account Surplus Since Apr 2023 [1/2]

- The current account surplus fell to E11.9bn (swda) in August for its smallest since Apr 2023, down from E29.8bn in July.

- The merchandise trade data had pointed to a narrowing, and indeed the goods surplus shifted from E24.6bn to E15.0bn (also smallest since Apr 2023), but the narrowing was further boosted by the primary income balance shifting from a surplus of E8.3bn to a deficit of E1.2bn.

- Primary income had masked a smaller goods surplus earlier in the summer, with a surplus worth E13.2bn in June (highest since Jun 2024 and before that mid-2022) and E8.3bn in July after large deficits in Jan and Feb.

- The non-seasonally adjusted details show that those large primary income deficits earlier in the year came on greater direct investment outflows (potentially ahead of US tariff policies) before the June/July surpluses were boosted by larger portfolio investment income credits.

- More broadly, the current account surplus narrowed to 2.0% GDP on a three-month rolling basis in August from 2.5% GDP in July, at what had been its highest since Aug 2024.

- The goods surplus stood at 1.6% GDP (smallest since mid-2023), the services surplus was unchanged at 1.1% GDP, the primary income surplus was unchanged at 0.5% GDP (largest since Aug 2024 but seemingly likely to shrink ahead) and the secondary income deficit was unchanged at 1.2% GDP.

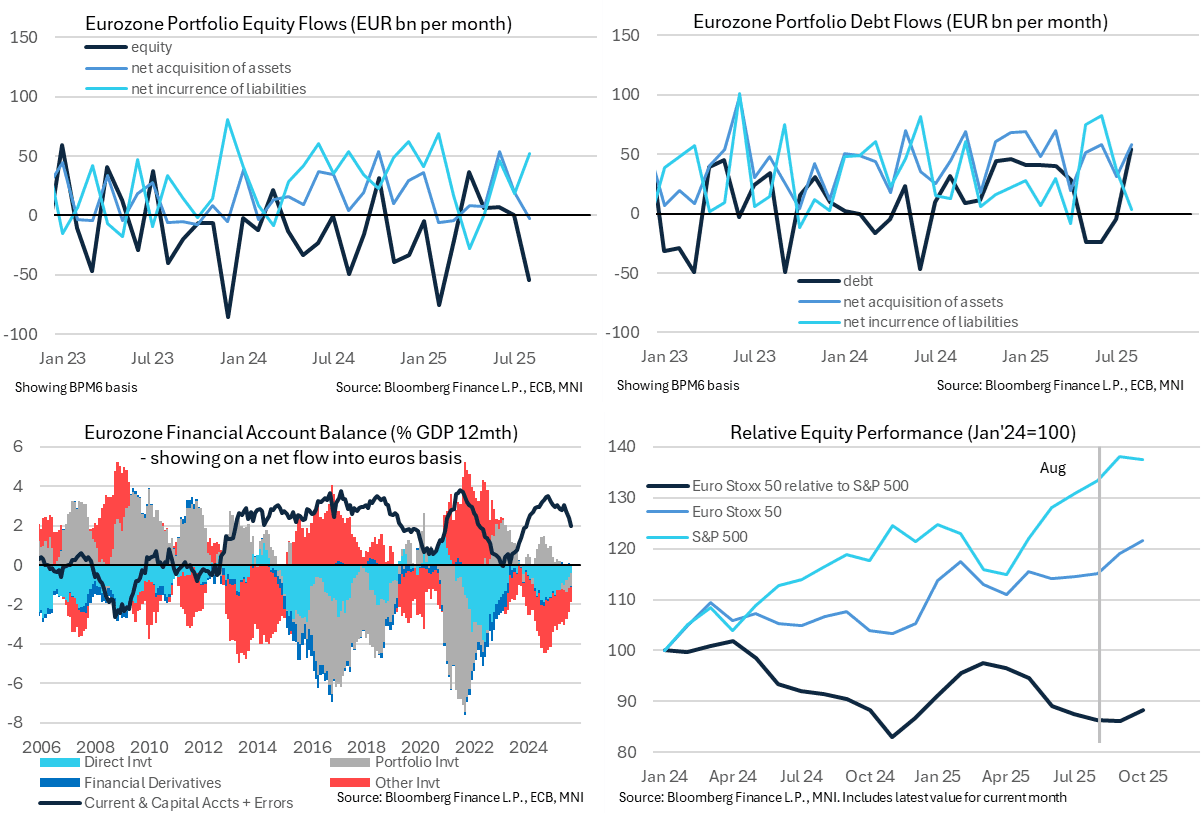

EUROZONE DATA: Foreign Appetite For EZ Debt Dwindled In August [2/2]

- On the financial account side, there were some large swings in portfolio net flows in August, including for equity flows after three mild months. The following figures are all on a non-seasonally adjusted basis:

- Debt net outflows jumped to E55bn in August - the largest since Dec 2022 – to reverse three months of inflows summing to E52bn. (Note that we write from a currency perspective as opposed to the charts below which stick to the BPM6 basis)

- This switch to debt outflows came as net acquisition of assets bounced back to E58bn whilst the net incurrence of liabilities narrowed to a small E3.5bn.

- On the latter, prior months had seen far larger foreign appetite for Eurozone liabilities, including E75bn in May and E82bn in June. August can be a small month for foreign net flows into Eurozone debt liabilities but the E3.5bn still compares with E13bn in Aug 2024, E14bn in Aug 2023 and E25bn in Aug 2022.

- Equity saw large inflows meanwhile, with E55bn in Aug the largest since E75bn in Feb and before that Dec 2023. Domestic investors shied away from overseas investments (a net pullback of E2.5bn in further backtracking from a E53.5bn net investment in June) whilst foreign investors saw increases appetite for Eurozone equity with the E52bn the highest since Feb.

EUROPE ISSUANCE UPDATE

Estonia syndication: Mandate

- "The REPUBLIC OF ESTONIA has mandated Erste Group, J.P. Morgan and Societe Generale for a potential EUR500m (WNG) RegS only tap of their outstanding 3.250% EUR 1bn bond due in January 2034 (ISIN: XS2740429076). The transaction is expected to be launched in the near future, subject to market conditions. The issuer is available for 1-on-1 calls upon request." From market source

- Following our policy team's interview with their Treasury earlier: https://www.mnimarkets.com/articles/mni-interview-estonia-likely-to-favour-longer-maturities-1760952192051

Slovakia auction results

- E115mln of the 3.00% Nov-31 SlovGB. Avg yield 2.8405% (bid-to-cover 1.69x).

- E191mln of the 3.75% Feb-35 SlovGB. Avg yield 3.2964% (bid-to-cover 3.13x).

- E93mln of the 0.375% Apr-36 SlovGB. Avg yield 3.4279% (bid-to-cover 2.91x).

- E100mln of the 2.00% Oct-47 SlovGB. Avg yield 4.1247% (bid-to-cover 3.30x).

EU-bond auction results

- E2.259bln of the 2.625% Jul-28 EU-bond. Avg yield 2.128% (bid-to-cover 1.15x).

- E1.798bln of the 2.75% Feb-33 Green EU-bond. Avg yield 2.68% (bid-to-cover 1.15x).

- E1.335bln of the 3.75% Oct-45 EU-bond. Avg yield 3.709% (bid-to-cover 1.25x).

FOREX: USDJPY Has Volatile Session, NZD Firmer Post Q3 CPI

- The USD index holds close to Friday’s closing levels, having traded within a tight 18 pip range to start the week. China third quarter GDP slowed to 4.7% Y/y, however the print came in marginally above expectations, prompting minimal impact on broader risk sentiment and the greenback. President Trump expressed optimism around US-China trade talks (albeit with clear focus points), keeping major equity benchmarks in the green Monday.

- Despite the limited price adjustments across G10 FX, the Japanese yen has had a volatile session overnight. Developments regarding Japan's LDP and Ishin parties forming a coalition, which should pave the way for Takaichi to become the new PM, initially boosted USDJPY to 151.20, extending its bounce from the Friday lows to 1.22%.

- Howver, the pair has traded notably lower since since, weighed by hawkish remarks from BoJ board member Takata, BOJ headlines on revising the economic growth forecast up and pressure off the highs for major equity benchmarks. Short-term USDJPY support at the 20-day EMA was pierced last week, and further weakness would signal scope for a deeper retracement towards 50-day EMA, at 148.86. Markets will remain attentive to the gap to the October 03 close, located at 147.47.

- Elsewhere, New Zealand Q3 CPI came in at 1.0% Q/q, one tenth above market expectations. While the data overall was close to RBNZ expectations as well, NZD does stand 0.25% higher on the session, while AUDNZD is comfortably off session highs to trade closer to 1.13. For NZDUSD, bearish conditions remain firmly intact, with the pair remaining within 1% of cycle lows at 0.5683, 6-month lows for the pair.

- Looking ahead, the ECB's Nagel and Vujcic speak later today after Canada's Q3 BoC business survey print. Tomorrow, UK fiscal data will be published ahead of Canada CPI.

OPTIONS: Expiries for Oct20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1515(E1.0bln), $1.1540-50(E1.2bln), $1.1640-55(E1.3bln), $1.1710-30(E1.4bln),$1.1790-00(E1.0bln)

- USD/JPY: Y150.00-05($2.0bln), Y150.25($600mln), Y154.80($2.0bln)

- EUR/JPY: Y178.00(E530mln)

- AUD/USD: $0.6670(A$589mln)

- USD/CAD: C$1.4000($718mln)

EQUITIES: Recent Weakness in E-Mini S&P Appears Corrective For Now

- The trend direction in Eurostoxx 50 futures remains up and the latest pullback appears to have been a correction. The contract remains above key support at 5498.73, the 50-day EMA. A clear break of the 50-day average is required to highlight a stronger reversal. On the upside, the bull trigger is unchanged at 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- Recent weakness in S&P E-Minis appears corrective - for now. Price has pierced support at the 50-day EMA, currently at 6615.80, but this support area remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Moving average studies continue to remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

COMMODITIES: Next Support for WTI Futures at $54.89, the May 5 Low

- A bearish theme in WTI futures remains intact and the move down last week reinforces current condition. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. Sights are on $54.89 next, the May 5 low, where a break would open $54.10, the Apr 9 low and a key support. Initial firm resistance is seen at $61.93, the 50-day EMA. Key resistance has been defined at $66.42, the Sep 26 high.

- A bull cycle in Gold remains intact and last week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4400.00 handle next, and $4404.9, a Fibonacci projection point. Note that the trend is in overbought territory. A move down - a correction - and would allow the overbought set-up to unwind. Support to watch lies at $3986.3, 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 20/10/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/10/2025 | 1400/1600 | ECB Schnabel Panel at Macroeconomics and Finance Conference | ||

| 20/10/2025 | 1430/1030 | ** | BOC Business Outlook Survey | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 21/10/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/10/2025 | 0700/0900 | ECB Lane at Macroeconomics and Finance Conference | ||

| 21/10/2025 | 0900/1100 | * | government debt | |

| 21/10/2025 | 0900/1100 | * | government deficit | |

| 21/10/2025 | 0900/1000 | BOE Saporta Fireside Chat at Islamic Development Bank | ||

| 21/10/2025 | 1030/1130 | BOE Bailey & Breeden on Private Markets at Financial Services Regulation Committee | ||

| 21/10/2025 | 1100/1300 | ECB Lagarde Keynote at Norges Bank Climate Conference | ||

| 21/10/2025 | 1230/0830 | *** | CPI | |

| 21/10/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 21/10/2025 | 1915/2015 | BOE Mann Fireside Chat at Lazard |