MNI US MARKETS ANALYSIS - EUR/USD Sinks Sharply on EU-US Deal

Highlights:

- EUR/USD sinks fast as EU-US strike trade deal targeting 15% on EU exports

- France still eyes use of Anti-coercion instrument - sees situation as not satisfactory or sustainable

- Treasuries pare initial gains ahead of frantic week for central banks and data

US TSYS: Gains Pared, Double Issuance And Borrowing Estimates In Focus

- Treasuries have pared gains as US desks filter in, after a mixed overnight session digesting the weekend US-EU trade deal that includes 15% tariffs on most EU goods. US-China talks in Stockholm meanwhile continue through Tuesday.

- Today sees Treasury announcements in focus, with double 2Y and 5Y issuance before Treasury’s borrowing estimates at 1500ET ahead of Wednesday’s full QRA.

- Cash yields are 0-0.5bp lower on the day.

- TYU5 trades at 110-31 (-00+) having eased off London highs of 111-03, with subdued cumulative volumes of 265k.

- Resistance remains at 111-14+ (Jul 22) whilst support is monitored, seen at 110-19+ (Jul 24 low) after which lies 110-08+ (Jul 14/16 low).

- Data: Dallas Fed mfg Jul (1030ET)

- Treasury borrowing estimates (1500ET): It should show a substantial increase in Treasury’s estimate for marketable borrowing in the current quarter (Jul-Sep). We have pencilled in a $950B-$1T borrowing need in the quarter (on a financing need of $500-550B), up from the May refunding round’s $554B estimate. MNI preview: https://media.marketnews.com/MNI_US_Deep_Dive_Issuance_2025_07_Refunding_e2af296ce5.pdf

- Coupon issuance: US Tsy $69B 2Y Note - 91282CNP2 (1130ET), US Tsy $70B 5Y Note - 91282CNN7 (1300ET)

- Bill issuance: $73B 26W bill auctions (1130ET), $82B 13W bill auctions (1300ET)

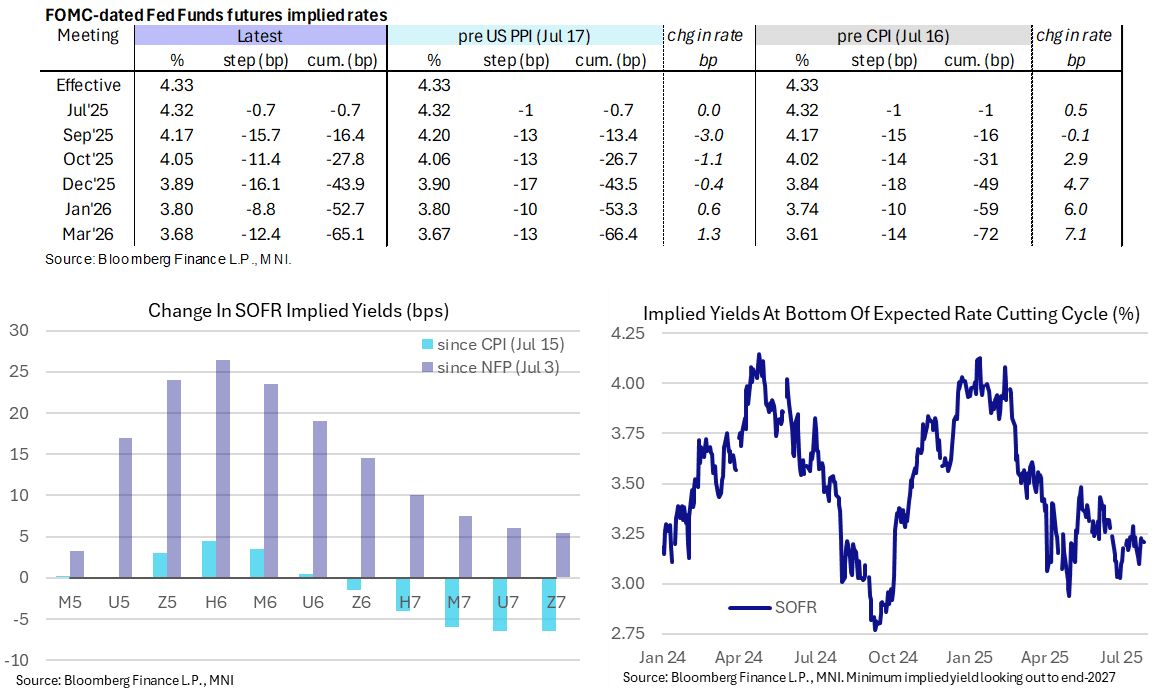

STIR: No Material Impact On Fed Rates From US-EU Trade Deal

- Fed Funds implied rates opened a touch firmer but are back to unchanged from Friday’s close for 2025 meetings, with no notable reaction from weekend announcements of a US-EU trade deal with 15% tariffs on EU goods.

- The deal had already been touted in the media, even if White House adviser Navarro had suggested to take those earlier reports with a "grain of salt".

- US-China relations with US Tsy Sec Bessent and China Vice Premier He Lifeng leading discussions in Stockholm through Tuesday this week.

- Cumulative cuts from 4.33% effective: 0.5bp for Wed, 16.5bp Sept, 28bp Oct, 44bp Dec, 52.5bp Jan and 65bp Mar.

- The 44bp of cuts to year-end is off last week’s high of 42bp, a level that was last sustainably higher in February.

- The SOFR implied terminal yield of 3.21% (SFRH7) is 1bp lower on the day, within a 3.1-3.3% range seen through July.

- MNI Fed Preview for Wednesday’s decision (with analyst version to follow later today as always): https://media.marketnews.com/Fed_Prev_Jul_2025_6823c76c5b.pdf

SOFR: Long Setting Most Prominent In Futures On Friday

OI data points to net long setting dominating in the white, red and green SOFR futures packs on Friday, with only one round of modest net long cover (SFM5) and a single round of net short cover (SFRH7) interrupting the theme across the front 10 contracts.

- Net short cover was most prominent in the blues.

| 25-Jul-25 | 24-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,270,601 | 1,275,532 | -4,931 | Whites | +50,498 |

SFRU5 | 1,313,500 | 1,291,672 | +21,828 | Reds | +9,813 |

SFRZ5 | 1,325,058 | 1,313,615 | +11,443 | Greens | +4,083 |

SFRH6 | 1,046,060 | 1,023,902 | +22,158 | Blues | -3,478 |

SFRM6 | 868,492 | 860,789 | +7,703 |

|

|

SFRU6 | 828,586 | 825,523 | +3,063 |

|

|

SFRZ6 | 916,954 | 915,946 | +1,008 |

|

|

SFRH7 | 720,970 | 722,931 | -1,961 |

|

|

SFRM7 | 702,287 | 698,354 | +3,933 |

|

|

SFRU7 | 520,185 | 517,905 | +2,280 |

|

|

SFRZ7 | 448,454 | 449,803 | -1,349 |

|

|

SFRH8 | 330,064 | 330,845 | -781 |

|

|

SFRM8 | 224,457 | 224,081 | +376 |

|

|

SFRU8 | 202,744 | 200,770 | +1,974 |

|

|

SFRZ8 | 199,182 | 203,102 | -3,920 |

|

|

SFRH9 | 142,499 | 144,407 | -1,908 |

|

|

US TSY FUTURES: Mix Of Modest Long Setting & Short Cover Seen Friday

OI data points to a mix of modest net long setting and short cover on Friday, as Tsy futures ticked higher. There was a very slight bias towards net long setting in curve-wide terms.

| 25-Jul-25 | 24-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,381,444 | 4,373,738 | +7,706 | +285,589 |

FV | 6,973,976 | 6,968,599 | +5,377 | +229,401 |

TY | 4,799,535 | 4,811,091 | -11,556 | -757,469 |

UXY | 2,408,979 | 2,412,874 | -3,895 | -337,726 |

US | 1,773,047 | 1,767,731 | +5,316 | +731,811 |

WN | 1,930,331 | 1,928,505 | +1,826 | +325,720 |

|

| Total | +4,774 | +477,326 |

EUROPE ISSUANCE UPDATE:

Belgium auction results

- E1.065bln of the 2.60% Oct-30 OLO. Avg yield 2.57% (bid-to-cover 2.03x).

- E1.208bln of the 3.10% Jun-35 OLO. Avg yield 3.185% (bid-to-cover 2.19x).

- E735mln of the 3.50% Jun-55 OLO. Avg yield 4.061% (bid-to-cover 2.14x).

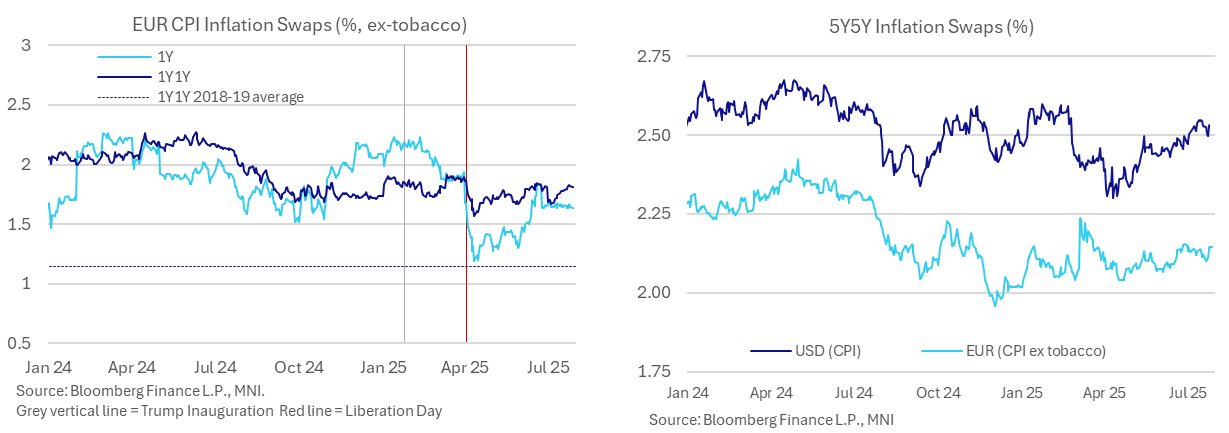

EUROPEAN INFLATION: Expectations Not Swayed By Two-Sided Trade Deal Impacts

- As discussed, there has been little reaction in European front rates to weekend news on the US-EU trade deal with a 15% tariff on EU goods, having already been rumoured last week.

- There is still just 4bp of cuts priced for the Sept ECB, having adjusted from 10bp prior to Thursday’s ECB press conference and subsequent sources pieces pointing to a high bar to a cut next meeting. This had been ~ 12.5bp before headlines earlier in the week on the trade deal nearing.

- Recall Lagarde from the Q&A: "But one thing I will add to that is that the sooner this trade uncertainty is resolved – I think we use the word “resolved swiftly” – so the sooner it is resolved, the less uncertainty we will have to deal with, and that would be welcomed by any economic actors, including ourselves.”

- From a near-term domestic inflation angle, the deal has clearly reduced the prospects of EU retaliation, for which there had been growing support for more penal approaches. Nevertheless, details on the deal more broadly are sparse.

- For now, 1Y inflation swaps are just 0.5bp lower than Friday’s close, at 1.638% a little further off last week’s 1.668% but having broadly kept an unusually narrow range of 1.64-1.69% in July to date.

- 1Y1Y inflation swaps meanwhile at 1.81% are holding their trend climb seen over the month, close to recent highs having average close to 1.9% in the two weeks ahead of early April “Liberation Day” tariff announcements. Whilst still below 2%, as they have been since July 2024, they remain far higher than the tepid 1.1% averaged in 2018/19 pre-pandemic.

- Much further out, 5Y5Y inflation expectations at 2.144% are towards the high end of ranges over the past couple months but with little change over the weekend. This remains comfortably between the ~2.05% seen prior to EU and German fiscal announcements in early March after which they briefly surged to 2.22%.

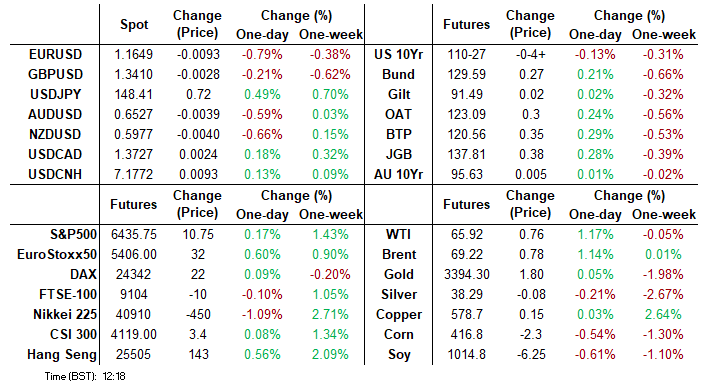

FOREX: A strong early performance for the Dollar

- The Dollar was mostly mixed against G10s going into the European session and just ahead of the EU Cash Govie Open, but as Europe came in, the Dollar saw a Broader base bid, after Desks took in the Overnight Tariff news in their stride.

- The US and the EU agreed a 15% Tariff deal, Europe also agreed to cut its Car Import duty to 2.5% as part of the deal.

- Multiple Desks are still somewhat perplexed at the strength of the Dollar in early trade, and aside from the Trade news, new headlines or drivers have so far been limited.

- Instead some Market participants also speculate that the Fed will stick to its Hawkish stance at Wednesday's Meeting when unchanged Rate is expected from the FOMC, for some of the bid into the Dollar.

- G10 Pairs/Crosses have seen some decent early ranges, the EURUSD sees over a 100 pips range, with the EUR mostly under some small pressure following the fade off the highs in European Equities.

- The Kiwi is the worst early performer within G10 against the Greenback, and the initial support will be seen at 0.5939 in NZDUSD, last Week's low.

- Looking ahead, there are no Tier 1 Data for the session, but the US-EU trade deal details continue to trickle down.

OPTIONS: Expiries for Jul25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E679mln), $1.1740-50(E1.7bln), $1.1800(E2.1bln)

- USD/JPY: Y145.00($1.2bln), Y146.00($841mln), Y147.75-85($600mln)

- EUR/GBP: Gbp0.8725-50(E892mln)

- AUD/USD: $0.6450($552mln)

- USD/CAD: C$1.3700-20($1.2bln)

EQUITIES: E-Mini S&P Starts the Week on a Bullish Note, at Fresh Cycle Highs

- The trend condition in Eurostoxx 50 futures remains bullish and short-term weakness for now, appears corrective. Support at 5281.00, the Jul 1 / 4 low, remains intact. A clear break of this level would strengthen a bearish threat. For bulls, a resumption of gains would refocus attention on key resistance and the bull trigger at 5486.00, the May 20 high. It has recently been pierced, a clear breach of it would resume the bull cycle and open 5500.00.

- S&P E-Minis have traded to fresh cycle high today as the contract begins the week on a bullish note. The climb confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Note that moving average studies are in a bull-mode position highlighting a clear dominant uptrend. Sights are on 6477.31, a Fibonacci projection. Key support is at the 50-day EMA, at 6153.14. Support at the 20-day EMA is at 6302.01.

COMMODITIES: Bearish Theme in WTI Futures Remains Intact, Despite Latest Gains

- A bearish theme in WTI futures remains intact and the shallow recovery since Jun 24 still appears corrective. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower. Support to watch is the 50-day EMA, at $64.77. The average has been pierced, a clear break of it would expose $58.17, the May 30 low. On the upside, initial resistance to watch is $69.41, the 50.0% retracement of the Jun 23 - 24 high-low range.

- Gold has pulled back from its Jul 23 high. Short-term weakness is considered corrective and a bull cycle that started Jun 30 remains intact. Resistance at $3395.1, the Jun 23 high, has recently been cleared. A continuation higher would open $3451.3, the Jun 16 high. Note that moving average studies are in a bull-mode position highlighting a dominant uptrend. An initial firm support to watch is 3282.8, the Jul 9 low.

| Date | GMT/Local | Impact | Country | Event |

| 28/07/2025 | 1400/1000 | ** | housing vacancies | |

| 28/07/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 28/07/2025 | 1530/1130 | * | US Treasury Auction Result for 2 Year Note | |

| 28/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 28/07/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/07/2025 | 1700/1300 | * | US Treasury Auction Result for 13 Week Bill | |

| 28/07/2025 | - | FOMC Meeting | ||

| 29/07/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 29/07/2025 | 0600/0800 | Flash Quarterly GDP Indicator | ||

| 29/07/2025 | 0700/0900 | *** | GDP (p) | |

| 29/07/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 29/07/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 29/07/2025 | 0830/0930 | ** | BOE M4 | |

| 29/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 29/07/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 29/07/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 29/07/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 29/07/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 29/07/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 29/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/07/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note |