MNI US MARKETS ANALYSIS - Equities Slip into NY Crossover

Highlights:

- Equities slip lower headed into NY crossover, with earnings in focus

- GBP/USD touches a new multi-year high in Asia-Pac trade

- JOLTS job openings, advance US trade balance make up data schedule

US TSYS: Modestly Lower Ahead of Bessent Briefing and Data

- Treasuries are mildly lower on the day after a late open for cash with a Japan holiday despite recent downward pressure in equity futures.

- The net move lower after yesterday’s sizeable bull steepening has been aided by the WSJ reporting after the close yesterday that Trump is expected to soften the impact of auto tariffs.

- Bessent at 0830ET in a White House briefing with Leavitt today drew some short-lived optimism on trade deal progress yesterday, and will be watched today.

- Data will also be important, including trade, JOLTS and consumer confidence, along with earnings (including Booking, Snap, Starbucks, Visa after the close) and Trump headlines.

- Cash yields are 1-2bp higher across the curve, consolidating yesterday’s bull steepening with 2s10s for example at 52bps.

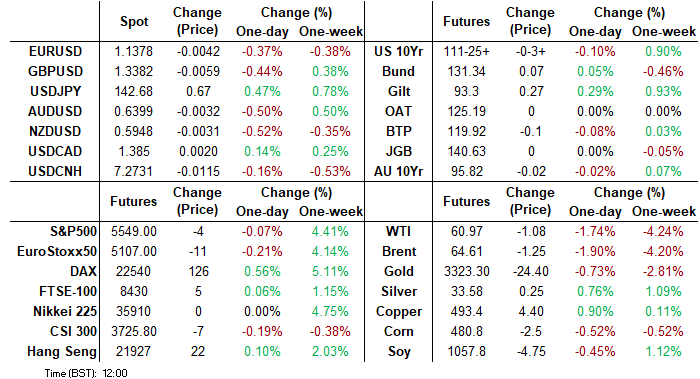

- TYM5 trades at 111-25+ (-04+) on particularly low volumes of 215k although the Japan holiday will have impacted at the margin.

- It has pulled back off yesterday’s high of 111-31 having cleared resistance at 111-25 (50% retrace of Apr 7-11 bear leg). This undermines a recent bearish theme, opening the round 112-00 before 112-12 (61.8% retrace of Apr 7-11 bear leg).

- Data: Advance goods trade balance Mar (0830ET), Wholesale/retail inventories Mar P/Mar (0830ET), FHFA/S&P CoreLogic House prices Feb (0900ET), JOLTS Mar (1000ET), Conf. Board consumer survey Apr (1000ET), Dallas Fed services Apr (1030ET)

- Bill issuance: US Tsy $70B 6W bill auction (1130ET)

- In case missed yesterday, Treasury's latest borrowing estimates were slightly higher than MNI's estimates, at $514B for the Apr-Jun quarter and $554B for the Jul-Sep quarter (MNI had pencilled in $500B for each quarter). There may have been some disappointment given Treasury did not lower the quarter-end TGA cash targets, which had been expected by some, but the current quarter's borrowing requirements are - excluding the effect of TGA cash rebuild - actually $53B lower than estimated at the last refunding in February. It could tilt the balance on Wednesday’s full QRA to no change in guidance on nominal coupon sizes being unchanged for “at least the next several quarters”, a positive development for Treasuries.

STIR: Slight Rise In Fed Rate Path After Lowest Terminal Since Tariff Pause

- Fed funds implied rates are 0-1.5bp higher today for 2025 meetings, aided by the WSJ reporting after the close yesterday that Trump is expected to soften the impact of auto tariffs.

- It modestly pares yesterday’s rally with help from some further recovery in equity futures.

- Cumulative cuts from 4.33% effective: 2.5bp May, 17bp Jun, 37.5bp Jul, 57.5bp Sep and 91.5bp Dec.

- In SOFR futures, the terminal yield remains in the U6 (3.06%), with the contract currently leading the day’s losses at -4.5. At 96.940, it’s off yesterday’s high of 96.990 after clearance of 96.97 (Apr 21 high) saw highs since levels prior to the 90-day tariff pause announcement on Apr 9.

- Today sees advance trade data for March at 0830ET, with Bessent set to speak at the same time, before JOLTS and the Conference Board consumer survey at 1000ET.

- There are also multiple earnings releases still to come today plus potential for Trump headlines in reaction to the WSJ report on autos yesterday plus Politico today reporting Amazon as being set to display the impact of Trump tariffs on each product.

US TSY FUTURES: Long Setting Bias On Monday

OI data points to a mix of net long setting (TU, FV, UXY & WN) and short cover (TY & US) during Monday’s rally in Tsy futures, with the former comfortably more prominent.

| 28-Apr-25 | 25-Apr-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,076,047 | 4,075,582 | +465 | +17,299 |

FV | 6,828,511 | 6,784,496 | +44,015 | +1,901,945 |

TY | 4,866,086 | 4,868,495 | -2,409 | -154,383 |

UXY | 2,272,806 | 2,255,470 | +17,336 | +1,540,673 |

US | 1,789,792 | 1,801,330 | -11,538 | -1,488,056 |

WN | 1,889,549 | 1,879,763 | +9,786 | +1,874,410 |

|

| Total | +57,655 | +3,691,889 |

STIR: Long Setting Dominated On SOFR Futures Strip On Monday

OI data suggests that net long setting dominated in SOFR futures on Monday, with only modest net short cover in SFRU7 interrupting the wider trend.

| 28-Apr-25 | 25-Apr-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,102,505 | 1,098,307 | +4,198 | Whites | +76,927 |

SFRM5 | 1,270,249 | 1,251,091 | +19,158 | Reds | +45,334 |

SFRU5 | 990,585 | 964,456 | +26,129 | Greens | -59 |

SFRZ5 | 1,104,926 | 1,077,484 | +27,442 | Blues | +20,091 |

SFRH6 | 725,138 | 714,499 | +10,639 |

|

|

SFRM6 | 703,937 | 692,150 | +11,787 |

|

|

SFRU6 | 692,438 | 680,183 | +12,255 |

|

|

SFRZ6 | 844,507 | 833,854 | +10,653 |

|

|

SFRH7 | 614,938 | 611,814 | +3,124 |

|

|

SFRM7 | 532,413 | 530,213 | +2,200 |

|

|

SFRU7 | 355,449 | 362,095 | -6,646 |

|

|

SFRZ7 | 382,695 | 381,432 | +1,263 |

|

|

SFRH8 | 270,878 | 265,029 | +5,849 |

|

|

SFRM8 | 185,924 | 181,366 | +4,558 |

|

|

SFRU8 | 147,204 | 139,725 | +7,479 |

|

|

SFRZ8 | 163,813 | 161,608 | +2,205 |

|

|

EUROZONE DATA: Credit Growth Firms Again Although Impulse Stabilising

- Private sector lending growth continued its steady acceleration in March, rising two tenths to 2.6% Y/Y or three tenths to 2.0% Y/Y when adjusting for sales & securitisations (highest since Jun 2023)

- Adjusting for sales & securitisations, lending growth to both non-financial corporates (NFCs) and households accelerated two tenths to 2.3% Y/Y (highest since Jul 2023) and 1.7% Y/Y (highest since Jun 2023) respectively.

- Spain leads lending growth to households (2.6% Y/Y) with France lagging (0.7% Y/Y), although France leads NFC growth (3.1% Y/Y) whilst Italy is the only country still contracting (-0.9% Y/Y but from -4.0% Y/Y as recently as July).

- The Eurozone credit impulse metric of 3mth flows vs 3mths a year ago has broadly plateaued so far in 2025, at around 2% GDP after a large swing from the -5 to -6% GDP seen in mid-2023 when credit growth started to slow abruptly - see top right chart.

- On this relative impulse basis, Spain leads (3.4% GDP), followed by Italy (2.5%), France (1.2%) and Germany (0.6%).

- Separately, Eurozone M3 money supply surprisingly eased to 3.6% Y/Y (cons 4.0) from a downward revised 3.9% (initial 4.0) for its softest since Dec. For rough context, it averaged 5.0% Y/Y through 2019.

FOREX: Greenback Firmer as Trump Team Look to Shift Focus to Taxes

- The greenback is firmer, reversing a small part of the minor losses posted into the Monday close. Flow remains a key driver for currency markets here, with price action yesterday consistent with flow drivers marked by month-end value date on Monday. Most corporate and rebalancing flow models point to USD buying for the end of April, which may be showing through in the price action so far Tuesday, given the minimal headline flow.

- Trump's schedule is pretty contained Tuesday, keeping focus on any reports concerning the progress of trade deals - as cabinet members continue to talk up the prospects of deals with Asian nations - and in particular India - which could be the first agreements to cross the line and avoid a return of sky-high tariffs.

- Treasury Secretary Bessent - seen as the most market-friendly member of Trump's cabinet met yesterday with several senior members of Trump's economic team to make the passage of tax legislation a top priority for the party. The meeting set July 4th as a key date going forward, the date by which the team look to achieve the tax overhaul and reset the public's view that this administration has a poor grasp on the economy.

- The USD is firmer against all others in G10, but CAD also trades well following the election results that show Carney's Liberals extending their time in office. EUR/CAD is holding below the 1.5800 handle, keeping the shallow bounce theme and raising the importance of 1.5668 support ahead.

- Event risk picks up Tuesday with the publication of April economic confidence data from the Eurozone and the advance trade balance release, JOLTS job openings for March and the latest consumer confidence data from the US. Central bank speak is still contained as the Fed remain inside their pre-meeting media blackout period. ECB's Villeroy and BoE's Ramsden are set to speak, however.

OPTIONS: Expiries for Apr29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1325(E792mln), $1.1470-75(E701mln)

- USD/JPY: Y141.00($735mln), Y144.00($2.6bln), Y147.00($2.1bln)

- AUD/USD: $0.6600-15(A$1.1bln)

- USD/CAD: C$1.3805-20($710mln), C$1.3925($572mln), C$1.3970($633mln)

- USD/CNY: Cny7.4000($699mln)

EQUITIES: Eurostoxx 50 Futures Maintain a Positive Tone

- Eurostoxx 50 futures maintain a positive tone and are holding on to their recent gains. The contract has cleared the 20-day EMA and pierced the 50-day EMA, at 5101.76. A clear break of this average would strengthen the current bull cycle and signal scope for a continuation of the corrective uptrend. This would open 5165.00 next, the Apr 3 high. Support to watch lies at 4812.00, the Apr 16 low. Clearance of this level would highlight a reversal.

- The corrective bull cycle in S&P E-Minis that started on Apr 7, remains in play. The contract has breached a number of important short-term resistance points. Price has cleared the 20-day EMA and pierced 5528.75, the Apr 10 high. The next key resistance is 5619.66, the 50-day EMA. A clear breach of this EMA would strengthen a bull theme. Initial key support lies at 5127.25, the Apr 21 low. A break would be bearish.

COMMODITIES: Medium-Term Bearish Theme in WTI Futures Remains Intact

- A medium-term bearish theme in WTI futures remains intact and the recovery that started on Apr 9 appears corrective. The move higher has allowed an oversold trend condition to unwind. Recent weakness resulted in the breach of a number of important support levels, reinforcing a bearish threat. A clear resumption of the bear cycle would open $53.72, a Fibonacci projection. Resistance to watch is $65.59, the 50-day EMA.

- Gold continues to trade below its recent highs. The trend needle points north and the latest move down appears corrective. The retracement has allowed an overbought condition to unwind. Moving average studies are unchanged, they remain in a bull-mode position highlighting a dominant uptrend. The next objective is $3547.9, a Fibonacci projection. Initial firm support to watch lies at 3231.3, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 29/04/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 29/04/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 29/04/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/04/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/04/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 29/04/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 29/04/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 29/04/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 30/04/2025 | - | Bank of Japan Meeting | ||

| 30/04/2025 | 2350/0850 | * | Retail Sales (p) | |

| 30/04/2025 | 2350/0850 | ** | Industrial Production | |

| 30/04/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 30/04/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 30/04/2025 | 0130/1130 | *** | CPI inflation | |

| 30/04/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 30/04/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 30/04/2025 | 0530/0730 | *** | GDP (p) | |

| 30/04/2025 | 0530/0730 | ** | Consumer Spending | |

| 30/04/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/04/2025 | 0600/0800 | ** | Retail Sales | |

| 30/04/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 30/04/2025 | 0645/0845 | *** | HICP (p) | |

| 30/04/2025 | 0645/0845 | ** | PPI | |

| 30/04/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/04/2025 | 0755/0955 | ** | Unemployment | |

| 30/04/2025 | 0800/1000 | *** | GDP (p) | |

| 30/04/2025 | 0800/1000 | *** | GDP (p) | |

| 30/04/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/04/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/04/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/04/2025 | 0900/1100 | *** | HICP (p) | |

| 30/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 30/04/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP Q/Q | |

| 30/04/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP Y/Y | |

| 30/04/2025 | 1000/1200 | ** | PPI | |

| 30/04/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/04/2025 | 1200/1400 | *** | HICP (p) | |

| 30/04/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/04/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/04/2025 | 1230/0830 | *** | GDP | |

| 30/04/2025 | 1230/0830 | *** | Employment Cost Index | |

| 30/04/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/04/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/04/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/04/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 30/04/2025 | 1400/1000 | *** | Personal Income and Consumption | |

| 30/04/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 30/04/2025 | 1530/1630 | BOE Lombardelli At New Economics Teacher Training Launch | ||

| 30/04/2025 | 1730/1330 | BOC Meeting Minutes |