MNI US MARKETS ANALYSIS - DXY Fades as Trump Delay Buys Time

Highlights:

- USD Index fades as Trump's Iran decision delay buys time for de-escalation

- Markets return from Juneteenth break to steady yields, Fed pricing

- Canadian retail sales, Philly Fed the schedule highlight

US TSYS: Open Gains Reversed, Geopol Remains In Focus With Thin Docket Ahead

- Treasuries have more than reversed gains seen on the Asia open after the Juneteenth holiday which saw cash closed and futures close early.

- The intraday moves better reflect a firmer risk environment following the White House reporting yesterday (after the early close for rates and equity futures) that Trump will make a decision on whether to strike Iran within two weeks rather than anything more imminent.

- Cash yields are 0.5-2bp higher from Wednesday’s close, with increases led by the long end.

- Curves steepen slightly but are within ranges, with 2s10s at 46.9bp (+1.4bp) and 5s30s at 91.1bp (+1.1bp).

- TYU5 trades at session lows of 110-21+ (-04) from Wednesday’s settle on sluggish volumes at ~250k. It’s close to yesterday’s low of 110-21 in thin holiday trading prior to at the time risk-off moves on geopolitical tensions.

- Support is seen at 110-10+ (Jun 16 low) before 109-28 (Jun 6/11 lows) but resistance at 111-13 (Jun 13 high) before a key 111-14+ (Jun 5 high & 61.8% retrace of May 1-22 downleg) is still watched.

- Today sees a light docket, with data led by the Philadelphia Fed manufacturing survey for a second look at June activity after the Empire survey surprised lower on Monday.

- Data: Philly Fed mfg Jun (0830ET), Conference Board Leading index May (1000ET)

- Fedspeak: None currently scheduled on the first day with the FOMC blackout lifted

- Trump attends national security meeting at 1100ET - closed press (per Roll Call)

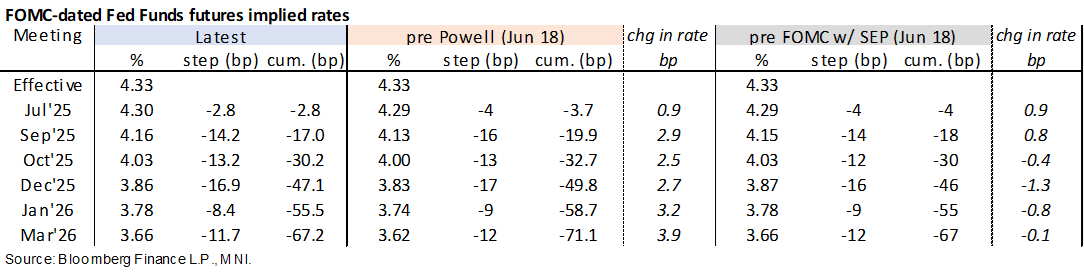

STIR: Fed Rate Path Within Narrow Weekly Range

- SOFR futures have reversed gains seen in yesterday’s holiday-thinned trading, with moves primarily stemming from the White House reporting after the early close yesterday that Trump will make a decision on whether to strike Iran within two weeks rather than anything more imminent.

- SOFR futures are unchanged to 1 tick lower from Wednesday’s full close out to 2027 contracts.

- The terminal yield of 3.29% (SFRZ6) continues to eye a little more than 100bp of cuts ahead.

- As for the near-term path, Fed Funds implied rates are very close to pre-FOMC levels. A next cut is priced for October (30bp cumulative) along with 47bp for year-end (very close to the somewhat surprising 50bp indicated by the median dot in Wednesday's SEP).

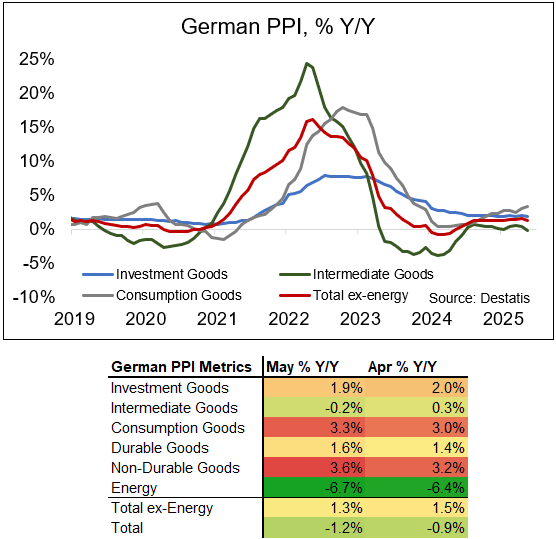

GERMAN DATA: Limited Signs Of Chinese Trade Diversion Deflationary Impact in PPI

German PPI fell to -1.2% Y/Y in May, inline with consensus expectations and a lower rate compared to April's -0.9% Y/Y.

- Consistent with German CPI in May, energy deflation saw relatively little change in May, at -6.7% Y/Y (vs -6.4% prior).

- That leaves ex-energy PPI also lower vs April, at 1.3% Y/Y - broadly in line with yearly rates seen ever since August 2024.

- Looking at the non-energy categories, intermediate goods arguably are in the focus currently following potential Chinese trade diversion into the EU, and the category indeed saw its lowest yearly rate since June 2024 at -0.2%. On a 3m/3m basis, intermediate goods PPI was unchanged at -0.6% in May, however.

- Eurozone trade data indicated that at least up until April, China trade diversion was only notable in pharmaceuticals - a detailed look at that data indicates this is unlikely to be troubling from a disinflation angle.

- The ECB has been listing such potential re-routing of excess supply as a downside risk to inflation since US tariff policies first emerged although its magnitude appears a point of contention on the Governing Council.

- Recall that ECB's Schnabel reiterated on June 12 in a slide deck that "trade diversion from China to the EU is expected to be limited". Previously, speaking on June 7 she said "I would argue that this effect is actually quantitatively quite small."

- See also our note from earlier this month on "No Clear Signs Of Chinese Trade Diversion Into EU In May" looking at Chinese data.

SECURITY: Iran FM Araghchi Dials Down Expectations Ahead Of Geneva Talks

Iran’s Foreign Minister Abbas Araghchi has tempered expectations of a breakthrough at diplomatic talks with European counterparts in Geneva today, saying Iran is “not prepared for talks with anyone while Israeli attacks continue,” per Iranian state television.

- Araghchi said, "after our resistance against Israel, I think countries will distance themselves from this 'aggression.' There is no room for negotiations with the US until the Israeli aggression stops."

- UK Foreign Minister David Lammy said after a White House meeting with US Secretary of State Marco Rubio and President Donald Trump’s Middle East Envoy, Steve Witkoff, yesterday: “A window now exists within the next two weeks to achieve a diplomatic solution,” referring Trump's delay on joining Israeli strikes.

- Laurence Norman at WSJ notes the talks could offer “an off ramp" but Washington “may ignore what happens here,” or “Iran may stick to all its old positions and red lines.”

- The involvement of European signatories to the 2015 JCPoA offers a new angle, as Europe was sidelined from five rounds of talks this year. The Europeans have authority over so-called 'snapback' sanctions on Iran, described by Iran Wire as “one of the most powerful diplomatic tools ever planned in international relations,” which provides leverage over Tehran.

- Reuters notes that Trump's two-week pause, “may not be a firm deadline," as Trump has "commonly used 'two weeks' as a time frame for making decisions and allowed other economic and diplomatic deadlines to slide.”

- The International Crisis Group writes in valuable analysis: "The diplomatic path is very narrow – but until the US decides whether to go to war itself, it is not entirely closed."

SECURITY: Kremlin Expects To Agree On Next Round Of Ukraine Talks, Next Week

Kremlin spokesperson Dmitri Peskov has spoken on conflicts in the Middle East and Ukraine. Peskov declined to predict a meeting between Russian President Vladimir Putin and US President Donald Trump happening this year, noting “complex work” is needed before a meeting could take place, per Reuters.

- Peskov said the Kremlin hopes to agree on a new date soon to resume talks with US on removing “irritants” in relations. Peskov noted that “dialogue with Ukraine continues,” and the Kremlin expects to “agree next week” on a date for the next round of talks.

- On Israel-Iran, Peskov said Putin offered his services as mediator, but it is “hard to say if his offer will be taken up,” adding that “so far we see Israeli desire to continue military action” but “there is always hope, and potential for diplomatic efforts”.

- PBS reports that Moscow shared a proposal with Iran, Israel, and US, “that could allow Tehran to pursue a peaceful atomic program while assuaging Israeli security concerns.”

- Putin said: “...we are simply talking about how we see a possible way out of the situation. But the decision, of course, is up to the political leadership of all these countries, primarily Iran and Israel.”

- On Wednesday, Trump appeared to reject the offer of mediation, saying he told Putin in a call: “I said, ‘Do me a favor, mediate your own... let’s mediate Russia first...’”

- While Russia and Iran have a “strategic partnership” treaty, there have been no signs yet that Moscow has offered Tehran military assistance. Russia, a signatory to the 2015 Iran nuclear deal, has worked with the US in the past on curbing Iran’s nuclear programme.

EMERGING MARKETS: Trade Disruptions Seen In May, Thai, Mex Trade Talks With US

- Latest trade data appear to be showing some early signs of the impact of ongoing global trade tensions. In China, exports of rare earth magnets slumped further last month, with shipments to the US particularly weak, while in Malaysia exports unexpectedly declined in May, with all major categories down on the prior month. The latter followed strong growth in April however, ahead of the tariffs, so may be a correction at this point.

- In India, by contrast, which is well positioned to benefit from US-China tensions, local companies remain in talks with Apple over the manufacture of equipment to make iPhones in the country. This comes amid delays in sourcing the equipment from China.

- Meanwhile, Thai customs exports were surprisingly strong in May, likely due to the frontloading of shipments ahead of reciprocal tariffs on July 8. The country, which has one of the largest export shares to the US in the region, will present its trade proposals to the US today, with hopes of reducing the tariff rate to 10% from the proposed 36%.

- Also today, Mexico’s Economy Minister Ebrard will visit the US to discuss trade issues. Earlier this week, President Sheinbaum said she had spoken with President Trump and proposed a broad agreement on security, immigration and trade.

- Amid progress on these issues and a relatively constructive dialogue between the two countries in recent weeks, MXN has outperformed most peers, rallying almost 10% from its April lows against the dollar to 10-month highs. The trend condition in USDMXN remains bearish, and potential is still seen for an extension towards 18.7774, the 50.0% retracement of the Apr 9 ‘24 - Feb 3 bull leg.

EUROPE ISSUANCE UPDATE:

UK Programmatic Gilt Tender Announcement

- The DMO has announced that it will offer up to GBP1bln of the 4.25% Dec-46 Gilt (ISIN: GB00B128DP45) via the tender on Thursday 26 June.

- The 4.25% Dec-46 Gilt was originally issued in 2006 as a 40-year gilt and hasn't been reopened since August 2019 (when it was last sold via tender).

- The gilt if anything looks a little cheap on RV terms compared to those trading around it based on yesterday's closing prices.

- And the BOE still holds GBP7.6bln of the GBP25.7bln outstanding with only GBP460mln sold back to the market in APF sales operations so far.

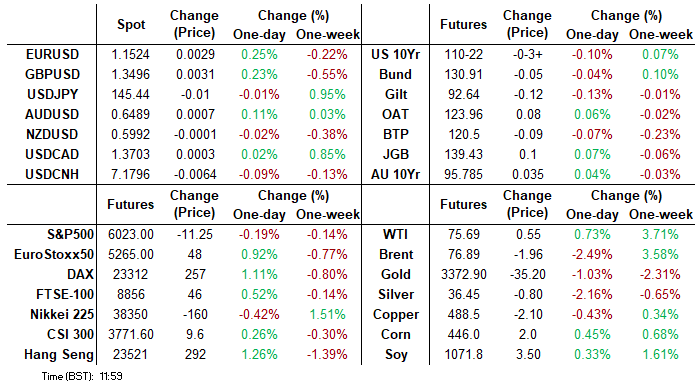

FOREX: USD Drifts on Trump Delay, Prevents USD Index Test of Resistance

- The two-week delay for Trump's decision on whether to intervene in Iran has granted some reprieve for oil markets, with Brent crude off ~2% at typing, despite continued reports of conflict and exchanges of fire between Iran and Israel. This has worked against the USD Index, which dips through yesterday's low and prevents - for now - any test of the downtrending 50-dma, today at 99.479.

- EUR has been favoured, putting the single currency higher against all others in G10, however momentum has been lacking across the European morning. This lack of momentum leaves EURUSD just 25 pips lower on the week, a very positive sign for market participants looking for further appreciation in H2. Moving average studies continue to display a dominant uptrend, with corrective dips remaining well supported. Scope is seen for a climb towards 1.1696, a Fibonacci projection, while initial firm support moves up to 1.1436, the 20-day EMA.

- GBP trades well, holding just below the 1.35 level despite a very poor set of retail sales numbers for May, with the details showing broad-based slowdowns in consumption across all categories - adding to the growing evidence that the UK consumer is curtailing purchases in the face of inflation and tax pressures. For now, support at the 50-day EMA, at 1.3357, remains intact. Key trend signals remain bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend.

- Canadian retail sales data and the Philly Fed Business Outlook for June are the data highlights Friday. There are no key central bank speakers due, despite the Fed existing their media blackout after Wednesday's rate decision.

FOREX: EURUSD Dips Remaining Supported, Flash PMIs Due Monday

- Despite the week being characterised by a fragile risk backdrop associated with the middle east conflict, G10 currency markets have traded in a subdued fashion. The renewed optimism for the greenback has lacked impetus, and yesterday’s fleeting attempt above the 20-day EMA and the downtrend from the February highs for the DXY is evidence of this.

- This lack of momentum leaves EURUSD just 25 pips lower on the week, a very positive sign for market participants looking for further appreciation in H2. Moving average studies continue to display a dominant uptrend, with corrective dips remaining well supported. Scope is seen for a climb towards 1.1696, a Fibonacci projection, while initial firm support moves up to 1.1436, the 20-day EMA.

- Goldman Sachs still expect the pair to rise to 1.20 by year-end and now expect it to rise to 1.25 over the next 12 months. In similar vein, HSBC strategists now see the EURUSD at 1.20 in Q4 2025, whereas Commerzbank expect 1.20 to be reached by September next year.

- Immediate focus turns to Monday’s flash PMIs, highlighted by French and German releases before the Eurozone measure. RBC expect an improvement in the euro area composite PMI to 50.6 in June from 50.2 in May. Although, their model suggests there are risks to the upside due to the strong improvement in the Sentix survey, higher copper prices and more optimism about the outlook in the PMIs last month.

EQUITIES: Eurostoxx 50 Futures Recover Moderately From Thursday's Lows

Eurostoxx 50 futures maintain a softer tone and the contract traded lower yesterday. Recent weakness has resulted in a breach of the 50-day EMA, at 5293.56. Price has also traded through 5255.00, the May 23 low. A clear break of both support points signals a S/T top and highlights scope for a deeper retracement. Sights are on 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance is 5333.37, the 20-day EMA. The trend condition in S&P E-Minis remains bullish. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6006.73, the 20-day EMA. A clear breach of this average would suggest potential for a deeper retracement and expose the 50-day EMA, at 5902.27. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

- Japan's NIKKEI closed lower by 85.11 pts or -0.22% at 38403.23 and the TOPIX ended 20.82 pts lower or -0.75% at 2771.26.

- Elsewhere, in China the SHANGHAI closed lower by 2.212 pts or -0.07% at 3359.896 and the HANG SENG ended 292.74 pts higher or +1.26% at 23530.48.

- Across Europe, Germany's DAX trades higher by 154.44 pts or +0.67% at 23212.6, FTSE 100 higher by 29.26 pts or +0.33% at 8820.99, CAC 40 up 36.74 pts or +0.49% at 7590.19 and Euro Stoxx 50 up 35.54 pts or +0.68% at 5232.57.

- Dow Jones mini down 106 pts or -0.25% at 42082, S&P 500 mini down 19.75 pts or -0.33% at 5961.75, NASDAQ mini down 68.25 pts or -0.31% at 21652.

COMMODITIES: Bull Cycle in WTI Futures Remains Intact

A bull cycle in WTI futures remains intact and the contract is trading closer to its recent high. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted at $67.11, the Jun 13 low. A breach of this level would signal scope for a deeper retracement. A bullish theme in Gold remains intact and this week’s pullback is considered corrective. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3279.3, the 50-day EMA.

- WTI Crude up $0.52 or +0.69% at $75.66

- Natural Gas up $0.09 or +2.33% at $4.081

- Gold spot down $20.92 or -0.62% at $3349.84

- Copper down $6.7 or -1.37% at $483.45

- Silver down $0.44 or -1.2% at $35.9913

- Platinum down $11.39 or -0.87% at $1292.04

| Date | GMT/Local | Impact | Country | Event |

| 20/06/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 20/06/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/06/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 20/06/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 20/06/2025 | 1230/0830 | ** | Retail Trade | |

| 20/06/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/06/2025 | 1530/1630 | BOE to announce Q3 APF sales schedule | ||

| 20/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 20/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |