MNI US MARKETS ANALYSIS: Dollar Stabilises Ahead Of Fed

Highlights

- Treasuries bull flatten, equities falter

- USD stabilises

- Fed & BoC decision headline later

FED: MNI Fed Preview-September 2025: Analyst Outlook

We've published our updated Fed preview, with analyst expectations - Download Full Report Here

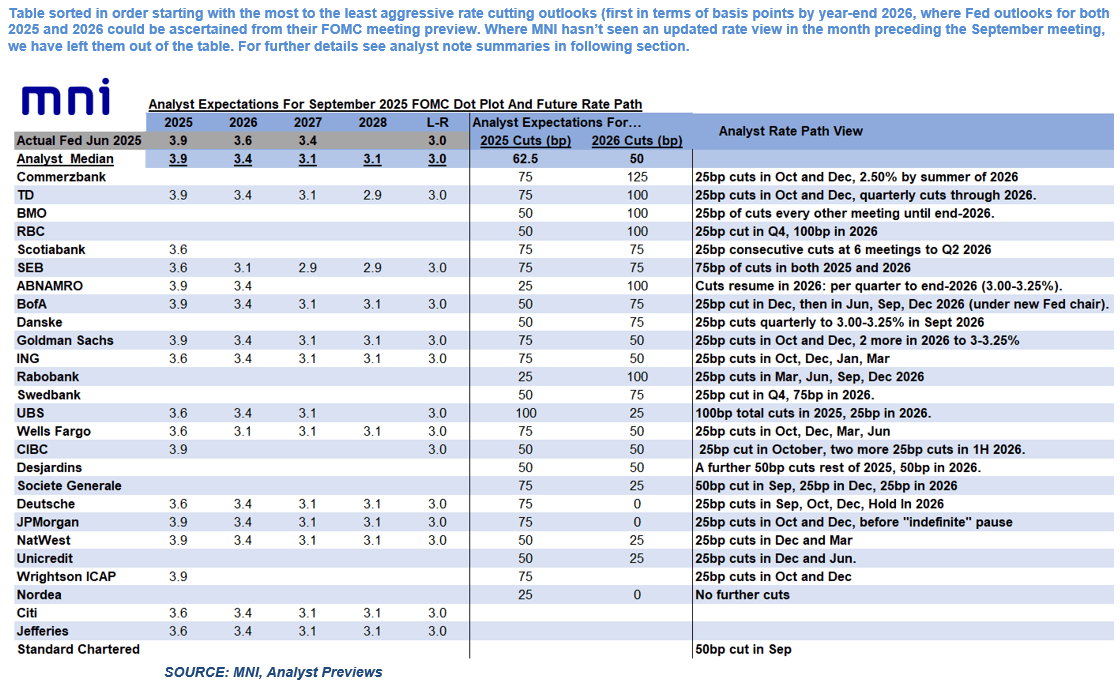

September 2025 FOMC Analyst Views: 2 Or 3 Cuts This Year

All but 2 analysts expect a 25bp cut at the September FOMC, based on 32 sell-side previews MNI saw.

- Standard Chartered and Societe Generale expect the FOMC to cut by 50bp.

- Most analysts who expressed an opinion believe that Gov Miran (if confirmed in time for the decision) will dissent in favor of a 50bp or greater cut, with potential for 2 or 3 total dovish dissents (Waller/Bowman).

- Risks of a dissent toward a hold are seen as limited (candidates: Schmid, Goolsbee, Musalem).

- SEP/Dot Plot: Analysts see a slightly lower “dot” profile in the Fed funds medians vs the last edition in June. For 2025 the median is narrowly in favor of a 3.9% (unchanged) end-year median, though many see 3.6%. For 2026 most see 3.4% (down from 3.6% in June), moving to 3.1% by end 2027 (down from 3.4% in June). No analyst sees the longer-run rate changing (3.0%).

- Analysts see the macroeconomic projections remaining relatively unchanged.

- Statement: The statement is widely expected to revise the language around the characterization of the labor market, to reflect the rise in unemployment and slowdown in payrolls growth.

- There are no expectations that the Fed will change the language re the description of inflation, or the 2nd paragraph’s balance of risks. However we saw one expectation that the Fed could alter the forward guidance sentence (Citi: To remove “and timing”).

- Future action: Expectations for total easing in 2025 (including September’s rate cut) ranges from 25bp (ABN Amro, Rabobank, Nordea) to 100bp (UBS). However, the median is 62.5bp, implying a split between 50 and 75bp of easing in 2025 – mirroring expectations of the Dot Plot.

- The median for total cuts by end-2026 is 125bp, ranging from 25bp to 200bp.

BOC: MNI BoC Preview-Sept 2025: Cuts To Resume On Softening Data

The Bank of Canada is expected to cut its benchmark overnight rate by 25bp to 2.50% on Wednesday September 17. This comes after three consecutive holds, amid a period in which activity and labour market data proved more resilient than expected in the face of the US-Canada trade conflict.

- Data since the July meeting have been almost unambiguous in tilting the balance toward a further easing, culminating with softer core CPI trends in August’s inflation report released on the eve of the decision.

- Almost all Canadian analysts expect a 25bp cut to be announced Wednesday.

- A 25bp reduction would bring rates toward the lower end of the BOC’s estimated neutral range.

- With no Monetary Policy Report released at this meeting and thus no new economic projections, there will be initial attention on the decision statement which is expected to remain non-committal on future cuts but retain the overall easing bias. That’s a tone likely to be echoed at the press conference.

- While Governing Council’s message will probably reiterate they are proceeding “carefully” with a meeting-by-meeting approach, the overall meeting communications will leave the door open to another rate cut in October if data continue to develop in a similar direction over the interim period.

- Views on the BOC terminal rate are split between those analysts who see one further cut beyond this week (2.25% terminal), and those who see two more (2.00%, so slightly below what would largely be considered neutral). That matches markets pricing between 1 and 2 cuts by end-2026 in addition to this week’s.

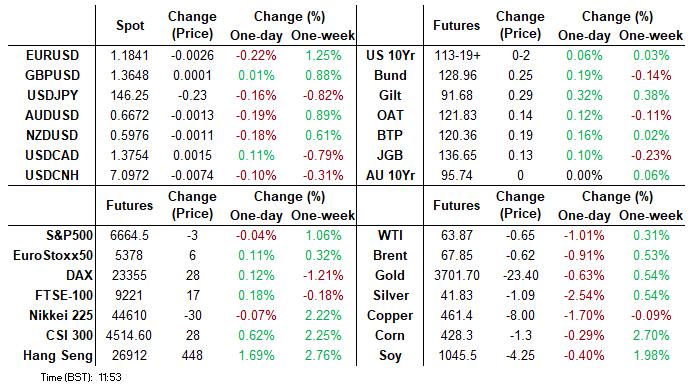

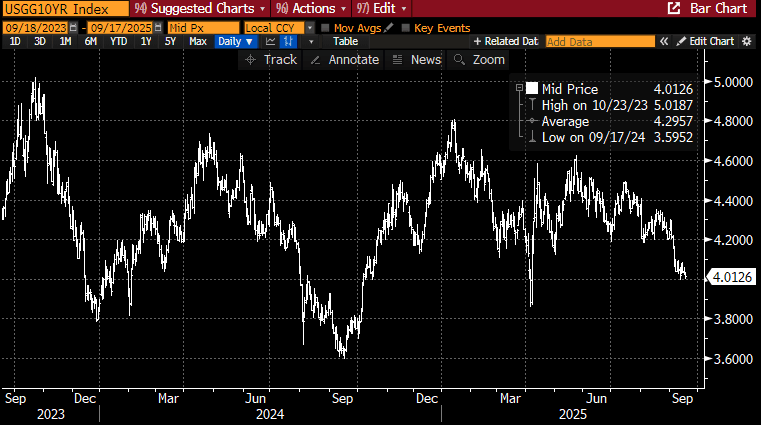

US TSYS: Modestly Bull Flatter With FOMC Later, 10Y Yields Eye Sub-4%

- Treasuries sit modestly bull flatter ahead of today’s FOMC decision and Summary of Economic Projections including a closely watched dot plot.

- Some softness in equity and crude oil futures likely feeds into the day’s rally, aided by the FT reporting that "China tells its tech companies to stop buying all of Nvidia's AI chips".

- EGBs see similarly broadly similar momentum whilst yesterday’s solid UST 20Y auction drew little reaction at the time but won’t be hindering the flattening seen in London hours.

- Cash yields are 0.5-2.5bp lower on the day.

- 10Y yields at 4.013% (-1.5bp) are off an earlier low of 4.0012% that eyed the first sub-4% since brief visits on Sep 11 and early April around reciprocal tariff announcements.

- TYZ5 trades at 113-19 (+02) off an earlier high of 113-21+ on another overnight session with thin volumes at 180k.

- Today’s modest gains mark the latest step back closer to resistance at 113-29 (Sep 11 high), as part of the bull mode condition. Further resistance is seen nearby at the round 114-00 whilst support is seen at 112-28 (20-day EMA).

- Data: Housing starts/building permits Aug/Aug prelim (0830ET)

- Fed: FOMC decision (1400ET), Powell press conference (1430ET)

- Bill issuance: US Tsy to sell $65bn 17-week bills (1130ET)

- Politics: Trump in UK, including Windsor Castle arriving ceremony (0720ET) and state banquet (1530ET)

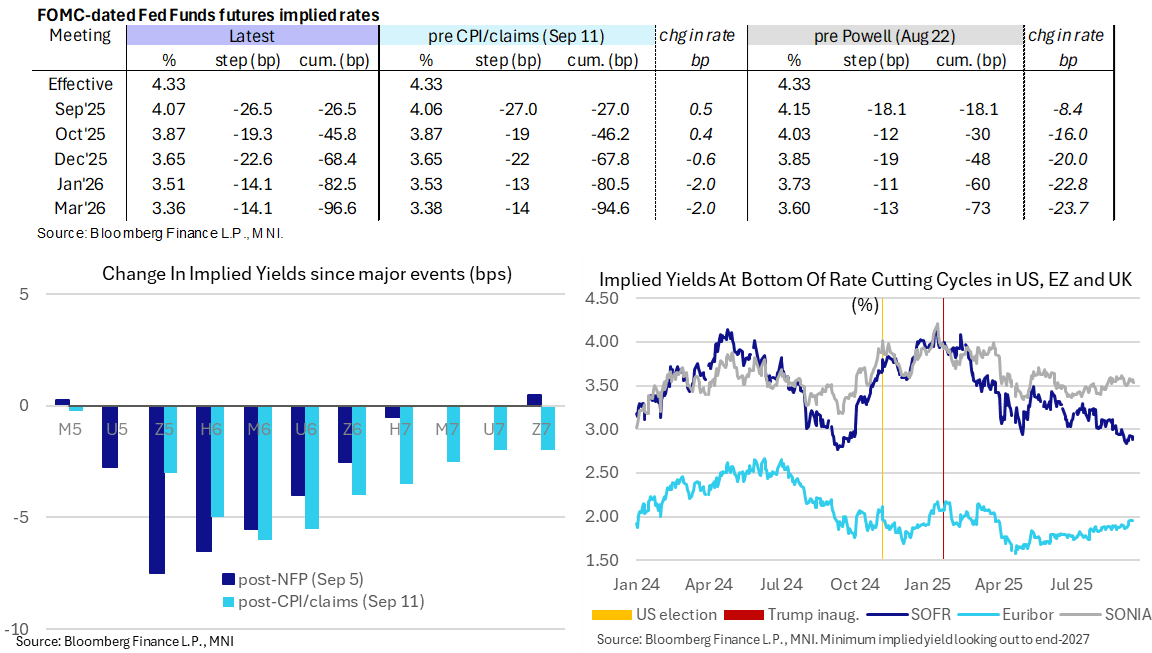

STIR: Fed Cut Pricing For Today Inches Higher But Still <10% Odds Of 50bp Cut

Fed Funds implied rates have dipped 0.5bp for today’s decision in response to aforementioned flow (Ongoing trade in FFV5 with paper paying 95.945 on 7K, taken bid over), but it still points to less than 10% odds of a 50bp cut.

- It holds the broad paring in 50bp cut expectations having increased to ~20% after payrolls earlier in the month.

- Cumulative cuts from 4.33% effective: 26.5bp for today, 46bp Oct, 68.5bp Dec, 82.5bp Jan and 96.5bp Mar.

- SOFR futures are essentially unchanged on the day.

- That includes the implied terminal yield of 2.88% (SFRH7), eyeing 145bp of cuts ahead including fully priced cut. It’s within ranges for the past two weeks, including dovish extremes of ~150bp of cuts after payrolls.

US TSY FUTURES: Net Long Setting Most Prominent On Tuesday

OI data points to net long setting in most Tsy futures as contracts ultimately ticked higher on Tuesday, with short cover in FV futures breaking the theme seen on the wider curve. Just under $5mln of fresh net DV01 equivalent was added across the curve, with the biggest DV01 move coming in TY futures.

| 16-Sep-25 | 15-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,486,838 | 4,459,627 | +27,211 | +944,004 |

FV | 6,756,143 | 6,783,745 | -27,602 | -1,228,769 |

TY | 5,410,199 | 5,376,498 | +33,701 | +2,229,293 |

UXY | 2,373,567 | 2,372,002 | +1,565 | +138,949 |

US | 1,823,266 | 1,809,691 | +13,575 | +1,958,873 |

WN | 2,018,376 | 2,014,249 | +4,127 | +786,901 |

|

| Total | +52,577 | +4,829,251 |

SOFR: Net Long Setting Dominated In Futures On Tuesday

OI data points to net long setting in most SOFR futures on Tuesday, as contracts settled a little higher on the day. Instances of short cover were fairly limited.

| 16-Sep-25 | 15-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,228,379 | 1,226,388 | +1,991 | Whites | +58,172 |

SFRU5 | 1,481,457 | 1,452,391 | +29,066 | Reds | +22,225 |

SFRZ5 | 1,685,350 | 1,679,287 | +6,063 | Greens | +9,140 |

SFRH6 | 1,206,952 | 1,185,900 | +21,052 | Blues | +34,803 |

SFRM6 | 1,011,037 | 1,007,896 | +3,141 |

|

|

SFRU6 | 953,801 | 939,719 | +14,082 |

|

|

SFRZ6 | 1,036,950 | 1,031,325 | +5,625 |

|

|

SFRH7 | 758,116 | 758,739 | -623 |

|

|

SFRM7 | 823,104 | 821,609 | +1,495 |

|

|

SFRU7 | 686,603 | 679,556 | +7,047 |

|

|

SFRZ7 | 703,149 | 694,858 | +8,291 |

|

|

SFRH8 | 444,345 | 452,038 | -7,693 |

|

|

SFRM8 | 365,170 | 368,093 | -2,923 |

|

|

SFRU8 | 281,056 | 263,874 | +17,182 |

|

|

SFRZ8 | 284,826 | 265,019 | +19,807 |

|

|

SFRH9 | 184,107 | 183,370 | +737 |

|

|

EUROPEAN ISSUANCE UPDATE

30-year Bund auction results

- E1bln (E786mln allotted) of the 1.25% Aug-48 Bund. Avg yield 3.18% (bid-to-offer 1.20x; bid-to-cover 1.53x).

- E1.5bln (E1.13bln allotted) of the 2.90% Aug-56 Bund. Avg yield 3.25% (bid-to-offer 1.37x; bid-to-cover 1.82x).

Italy Buyback results

MEF buys back E5bln of the following bonds:

- E1.025bln of the 3.50% Jan-26 BTP

- E695mln of the 4.50% Mar-26 BTP

- E845mln of the 0% Apr-26 BTP

- E835mln of the 0.50% Apr-26 CCTeu

- E1bln of the 1.60% Jun-26 BTP

- E600mln of the 0% Aug-26 BTP

GGB auction result

E250mln of the 3.625% Jun-35 GGB. Avg yield 3.26% (bid-to-cover 3.76x).

FOREX: USD Index Stabilises Just Above Cycle Lows, BOC and Fed Awaited

- Ahead of the keenly awaited September Fed decision, the US dollar trades on a more stable footing, with the dollar index 0.11% higher on the session. However, more broadly the DXY is consolidating its steep losses this week and resides just 35 pips away from the year’s lows, printed on July 01.

- Moderate weakness for equities has prompted some further underperformance for the likes of AUD and NZD, although both are only down around 0.2% on the day at typing. No great surprises within the UK CPI data to alter BOE expectations has kept GBPUSD unchanged on the day.

- Cable trades in a narrow 29 pip range but continues to consolidate its firm break above 1.3595. With both the Fed and Bank of England over the next two sessions, traders will be keeping a close yee on whether topside momentum can continue for the pair. Immediate resistance at 1.3681, the July 4 high, has capped the advance so far. Above here, 1.3789 remains the key resistance for the pair, the July 1 high.

- Overall, EURUSD has also consolidated its impressive move higher to fresh cycle highs on Tuesday, oscillating either side of 1.1850 throughout the morning. Yesterday’s highs of 1.1878 will be the immediate level to watch as we approach the Fed, before more meaningful targets at 1.1923 and 1.2000.

- USDJPY had a significant low print overnight, matching a key support level to the pip at 146.21, the Aug 14 low and a bear trigger. A break of this level would highlight a stronger bearish threat and highlight a range breakout. While spot did subsequently bounce to 146.70, the pair is tracking back below 146.40 as we approach the NY crossover.

- Both the Bank of Canada and FOMC rate decisions highlight the economic calendar on Wednesday, with both expected to cut rates by 25bps. US building permits and housing starts data will cross, with New Zealand GDP kicking off Thursday’s APAC schedule.

FOREX OPTIONS: Expiries For Sep17 NY cut 1000 ET (Source: DTCC)

- EURUSD: 1.1800 (344mln), 1.1850 (1.46bn), 1.1900 (921mln)

- EURGBP: 0.8700 (723mln)

- USDJPY: 146.00 (426mln), 146.85 (881mln), 147.00 (326mln), 147.25 (250mln).

- AUDUSD: 0.6650 (456mln)

- NZDUSD: 0.5900 (830mln)

EQUITIES: EUROSTOXX 50 Pullback Appears Corrective

A bull cycle in S&P E-Minis remains intact and the contract is trading closer to its recent highs. A fresh cycle high yesterday reinforces current bullish conditions. The move higher confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6700.00 handle next and 6712.33, a 1.764 projection of the Aug 20 - 28 - Sep 2 price swing. Initial support to watch is 6569.89, the 20-day EMA.

- EUROSTOXX 50 futures have recently traded through the 20-day EMA - a bullish development for now. The move higher undermines a recent bearish theme and signals potential for a climb towards 5522.0, the Aug 26 high and a bull trigger. On the downside, key support has been defined at 5292.00, the Sep 2 low. Clearance of this level is required to reinstate a bearish theme. For now, yesterday’s move down appears corrective.

COMMODITIES: Gold Bulls Remain In The Driver's Seat

Gold remains in a clear bull cycle and the yellow metal is trading closer to its recent highs. A fresh all-time high, once again this week, confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3705.2, a 1.382 projection of the May 15 - Jun 16 - 30 price swing. Initial firm support lies at $3547.7, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact and the latest recovery is considered corrective. The pullback from the Sep 2 high highlights a possible recent reversal and the end of a corrective phase between Aug 13 - Sep 2. Initial resistance to watch is $66.03, the Sep 2 high. A stronger resumption of weakness would open $57.71, the May 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 17/09/2025 | 1115/1315 | ECB Cipollone Speaks at Netherlands Central Bank Resilience Conference | ||

| 17/09/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 17/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/09/2025 | 1430/1030 | BOC press conference | ||

| 17/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 17/09/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/09/2025 | 2245/1045 | *** | GDP | |

| 18/09/2025 | - | NorgesBank Meeting | ||

| 18/09/2025 | - | Bank of Japan Meeting | ||

| 18/09/2025 | 2350/0850 | * | Machinery orders | |

| 18/09/2025 | 0130/1130 | *** | Labor Force Survey | |

| 18/09/2025 | 0710/0910 | ECB Lagarde Video Message at Women Leadership Summit | ||

| 18/09/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 18/09/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/09/2025 | 0800/1000 | ECB de Guindos at MNI Connect Event | ||

| 18/09/2025 | 0900/1100 | ** | EZ Construction Output | |

| 18/09/2025 | 0945/1145 | ECB Schnabel Chairs Panel at ECB Research Conference | ||

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 18/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/09/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 18/09/2025 | 1915/1515 | BOC speech on payments ecosystem from director Ron Morrow. | ||

| 18/09/2025 | 2000/1600 | ** | TICS |