MNI US MARKETS ANALYSIS - Data Picks Up, Labor Mkt in Focus

Highlights:

- Data picks up, with a particular focus on the labor market: weekly claims, Revelio, Chicago Fed and Challenger all due

- Chinese authorities begin to counter CNY strength; more could come

- USD weaker across the board, USDJPY weight stems from building BoJ expectations

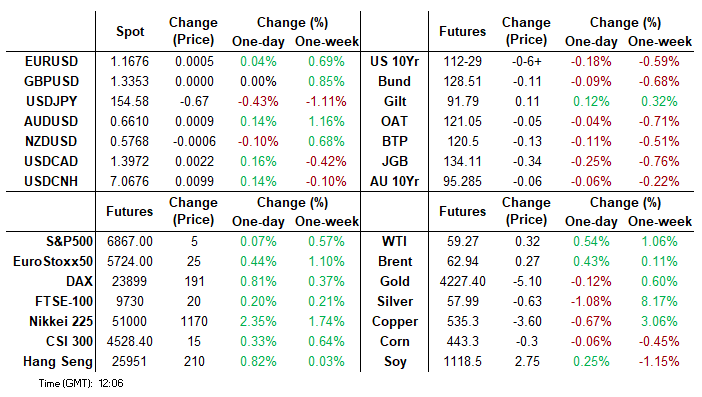

US TSYS: Modest Belly-Led Losses Ahead Of Labor-Focused Docket

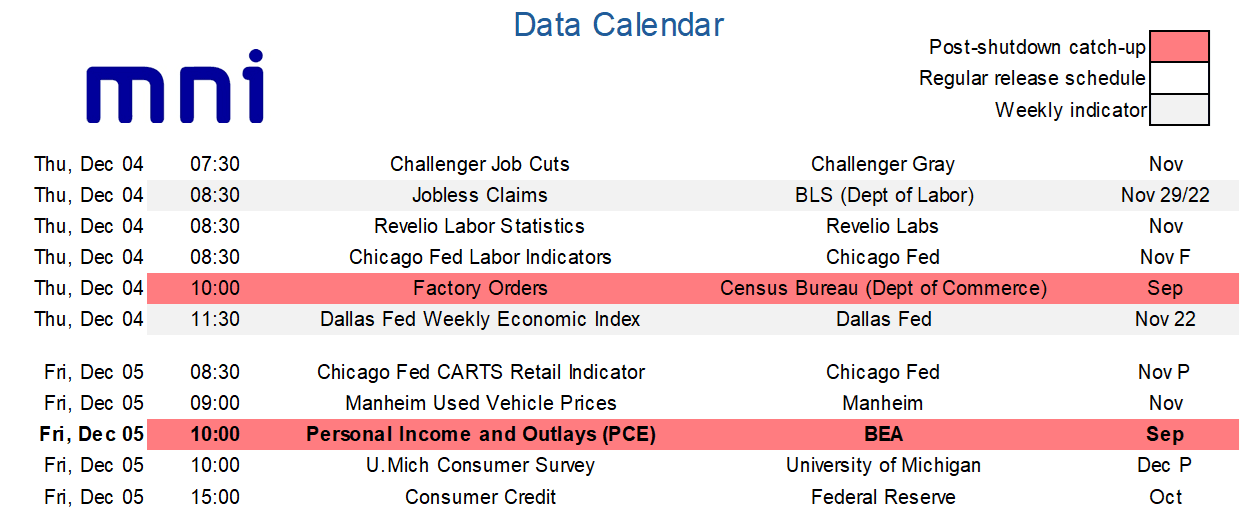

Treasuries have seen modest belly-led losses overnight in spillover from latest JGB weakness on gaining BOJ hike traction. It’s ahead of multiple labor releases that provide useful updates before next week’s FOMC meeting (Challenger job cuts, weekly claims, Revelio labor statistics and latest Chicago Fed u/e rate tracking) plus the shutdown-delayed factory orders report for September.

- Cash yields are 0.5-2.5bp higher on the day, with increases led by the belly.

- The flattening sees 5s30s at 108bps after yesterday’s 111bp marked its steepest since the first half of September.

- TYH6 trades at 112-28+ (-07) on modest volumes of 255k, towards the lower end of the week’s range after continuing to give back intraday gains prior to a somewhat solid ISM services report.

- The technical backdrop points to a bearish tone with support at 112-22 (Dec 2 low) before 112-10+ (Nov 20 low) and a key 112-07 (Nov 5 low). Resistance meanwhile is seen at 113-11 (Dec 1 high) and 113-22+ (Nov 25 high).

- Data: Challenger report Nov (0730ET), Weekly jobless claims (0830ET), Revelio labor statistics Nov (0830ET), Chicago Fed labor indicators (0830ET), Factory orders Sep (1000ET), Dallas Fed weekly economic index (1130ET)

- Fedspeak: Bowman on bank supervision (1230ET) – in FOMC blackout

- Bill issuance: US Tsy $90B 4W, $80B 8W bill auctions (1130ET)

- Politics: Trump in a trilateral greeting with Rwanda and DR Congo presidents (1120ET) before signing ceremony (1210ET)

- Bloomberg reports (link) that “Donald Trump’s aides and allies are discussing the possibility of making Treasury Secretary Scott Bessent the top White House economic adviser — in addition to his current job — should the president pick Kevin Hassett as the next chair of the Federal Reserve, according to people familiar with the matter.”

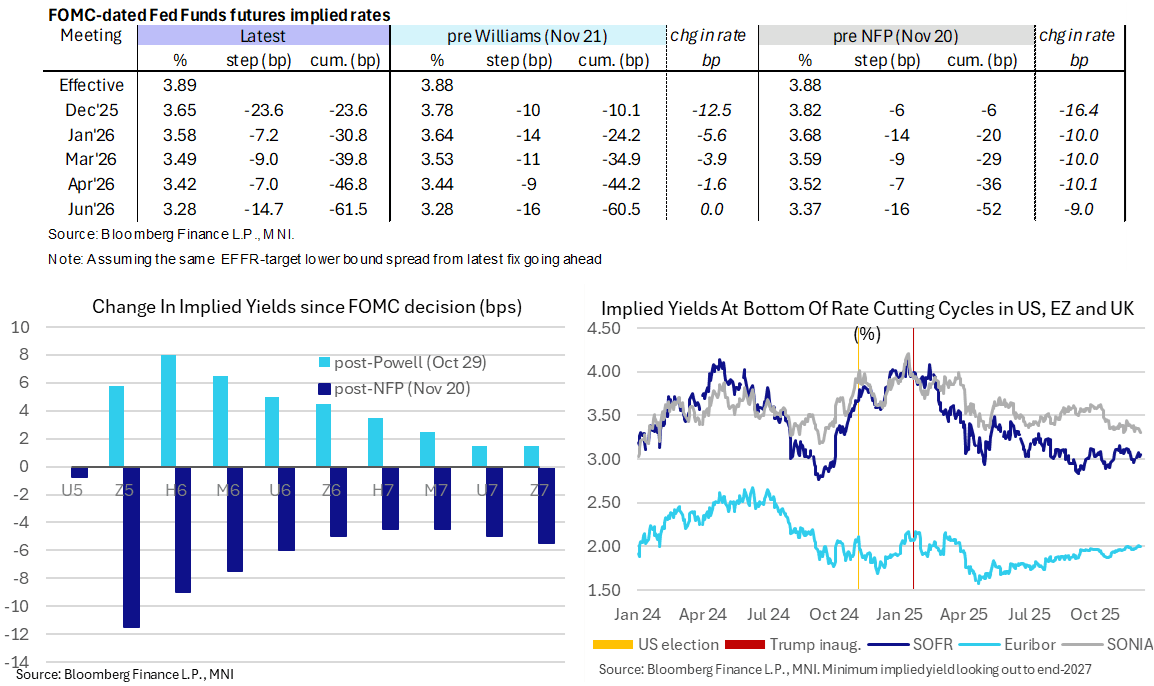

STIR: Fed Rate Path Slightly Firmer Ahead Of Multiple Labor Releases

- Fed Funds implied rates are 0.5-1bp higher overnight for 1H26 FOMC meetings ahead of multiple labor releases plus a recently rescheduled factory orders report for September.

- Cumulative cuts from 3.89% effective: 23.5bp Dec, 31bp Jan, 40bp Mar, 47bp Apr and 61.5bp Jun.

- (Note, the 75th percentile has in the previous two quoted days held an uptick to 3.90% so we wouldn’t be surprised to see another tick higher here).

- SOFR futures are up to 2.5 ticks lower looking out to end-2027 contracts, with the terminal implied yield of 3.055% (H7) holding above the sustained ~3% levels last week in response to a dovish Williams on Nov 21.

- NEC’s Hassett still enjoys a commanding lead in betting markets for next Fed Chair at 72% on Polymarket, although is down from 85% yesterday on various media reports of Wall Street pushback.

- This from yesterday on Fed personnel considerations (Bloomberg link): Treasury Secretary Scott Bessent will push for a new rule that candidates for regional Federal Reserve presidents must have lived in that district for at least three years. Three current Fed presidents don’t meet his criteria. “I am going to start advocating going forward, not retroactively, that regional Fed presidents must have lived in their district for at least three years”.

- VC Supervision Bowman (voter) speaks on bank supervision and regulation (1230ET) – the ongoing blackout ahead of next week’s FOMC decision means she can’t touch on the economic outlook or mon pol.

US LABOR MARKET: It’s Not Only Claims Today, Watch Out For Revelio And More

Weekly jobless claims will continue to be an important update for tracking labor conditions, with initial claims at very low levels but continuing claims having pushed higher in recent weeks. However, when it comes to labor updates, we also flag Challenger job cuts (0730ET) and Revelio Labs' labor statistics (0830ET) for November in particular, rounded out by the final Chicago Fed u/e rate estimate for November (also 0830ET).

- The October Challenger report showed a sharp increase in layoffs to its highest for an October since 2003 along with tepid hiring plans over Sep-Oct combined. Focus should be on the layoff announcements whilst we only watch November hiring plans to see if there were any later than usual plans ahead of the holidays.

- The Revelio nonfarm payrolls estimate drew a dovish market reaction last month when it pointed to nonfarm payrolls growth of -9k in October after a downward revised 33k (initially 60k) in September. It was the first negative M/M reading for the Revelio series since May. ADP yesterday reported a -32k drop for private employment in November after a 47k increase in Oct, with today’s Revelio report offering a sense check.

- The Chicago Fed will release its final estimate for the unemployment rate in November, after its advance estimate published Nov 24 pointed to 4.44% in Nov after an upward revised 4.46% in Oct. Accordingly, it has been implying little additional change in the unemployment rate since the 4.44% in the BLS payrolls report for September (which in turn prompted that Oct estimate of 4.46% to have been revised up 4.36% previously). The next BLS u/e rate we’ll get is the November print on Dec 16 – there won’t be an official October figure as the household survey wasn’t able to be conducted.

SOFR: Mix Of Net Long Setting & Short Cover In Futures On Wednesday

OI data points to net short cover dominating in the whites on Wednesday, even with a fairly large round of net long setting in SFRH6 noted.

- Positioning was more mixed further out the strip, with a better balance between the two seen in the reds, before net long setting came to the fore in the greens and blues.

- SOFR futures settled higher on Wednesday after ADP employment data came in on the soft side, while ongoing speculation surrounding Kevin Hassett becoming the next Fed Chair continues to promote dovish flow.

- As noted in our recent bullet, there are plenty of labor market indicators due for release today (weekly jobless claims, Challenger Job cuts, Revelio nonfarm payrolls estimate & Chicago Fed data).

| 03-Dec-25 | 02-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,317,795 | 1,347,680 | -29,885 | Whites | -62,329 |

SFRZ5 | 1,596,375 | 1,649,548 | -53,173 | Reds | -1,801 |

SFRH6 | 1,364,377 | 1,342,322 | +22,055 | Greens | +6,363 |

SFRM6 | 1,146,339 | 1,147,665 | -1,326 | Blues | +8,762 |

SFRU6 | 1,075,438 | 1,068,152 | +7,286 |

|

|

SFRZ6 | 1,111,785 | 1,126,321 | -14,536 |

|

|

SFRH7 | 845,085 | 841,045 | +4,040 |

|

|

SFRM7 | 778,570 | 777,161 | +1,409 |

|

|

SFRU7 | 831,967 | 831,138 | +829 |

|

|

SFRZ7 | 843,575 | 836,677 | +6,898 |

|

|

SFRH8 | 433,446 | 427,868 | +5,578 |

|

|

SFRM8 | 410,370 | 417,312 | -6,942 |

|

|

SFRU8 | 378,511 | 371,330 | +7,181 |

|

|

SFRZ8 | 321,363 | 320,429 | +934 |

|

|

SFRH9 | 195,364 | 195,784 | -420 |

|

|

SFRM9 | 206,839 | 205,772 | +1,067 |

|

|

UK DATA: Construction PMI falls, details terrible; Budget uncertainty the driver

UK construction PMI data was pretty awful, falling 5 points below consensus to 39.4, but new orders falling off ahead of the Budget can explain much of the move. It might therefore see a bit of a rebound next month but the details are not great.

From the press release:

- "Many construction companies commented on weak client confidence, alongside delayed spending decisions linked to uncertainty ahead of the Budget."

- "Total new business decreased at a rapid pace in November. Around 44% of the survey panel reported a fall in new orders, while only 17% signalled an increase. Aside from the pandemic, the resulting seasonally adjusted New Orders Index pointed to the fastest downturn in new work since early-2009."

- "Employment numbers across the construction sector decreased for the eleventh consecutive month in November, reflecting a lack of new work to replace completed projects and elevated wage pressures. The latest fall in staffing levels was the steepest since August 2020."

- "Looking ahead, the proportion of construction companies expecting an upturn in business activity in the next 12 months (31%) narrowly exceeded those forecasting a decline (25%). The resulting Future Activity Index signalled the lowest degree of optimism since December 2022. Some firms commented on hopes of a rebound in general market conditions and support from lower borrowing costs. However, this was offset by signs of cutbacks to clients' investment spending plans and concerns about long-term domestic economic prospects.

FOREX: USD Index Weakness Persists, Extends Weekly Decline to 0.65%

- Broad dollar declines are persisting this week, prompting the USD index to print fresh pullback lows at 98.80. This extends the week’s decline to around 0.65%, and the two-week selloff now stands around 1.6%. Greenback weakness continues to be a reflection of a more dovish profile for the Fed under potential Kevin Hassett leadership and an associated more optimistic risk backdrop.

- The DXY posted a significant technical close on Wednesday, with the first daily close below the 50-day exponential moving average since early October. This impulse has generated several bullish signals across the rest of the G10 basket, and continues to bolster the optimistic sentiment for EM FX.

- The JPY is outperforming on the session, amid headlines suggesting key members of PM Takaichi’s government wouldn’t try to stop the BOJ if it decides to raise interest rates in December, a stance that makes a move more likely. The move lower for USDJPY remains shy of Monday's low at 154.67, the immediate support. Below here, the 50-day EMA at 153.34 is a more meaningful chart point.

- AUDUSD has also bridged the gap to 0.6618 resistance amid household spending providing another piece of data signalling robust domestic demand in Australia. The cautious RBA and firm risk backdrop is underpinning renewed AUD optimism.

- Elsewhere, Swedish Nov flash CPIF ex-energy inflation came in slightly below expectations, but should not change the near-term Riksbank outlook. USDSEK hovers within close range of a cluster of lows from October around 9.34. GBPUSD has also spent the session consolidating its impressive 1% rally yesterday, as pre-budget positioning was further squeezed.

- US weekly claims and September factory orders are on the calendar today alongside the Canadian Ivey PMI.

FOREX: Chinese Intervention Works Against USDCNY Losses, Raises Cost of Long CNY

"CHINA STATE-OWNED BANKS SEEN BUYING DOLLARS - SOURCES" - Reuters

CHINA STATE-OWNED BANKS TWEAK TRADING STYLE TO BLUNT YUAN GAINS - SOURCES

- Report writes that "China's major state-owned banks bought dollars in the onshore spot market this week and held on to them in an unusually strong effort to rein in yuan strength, according to people with knowledge of the matter."

- "But unlike their usual trading strategy, the lenders did not appear to recycle the dollars into the swap market, market sources said, noting the move was likely aimed at tightening dollar liquidity and so raising the cost of long yuan bets."

The noteworthy part of that Reuters source piece: "the lenders did not appear to recycle the dollars into the swap market, market sources said"

- The net result of this is tighter local dollar liquidity - and more acute negative carry for any USD/CNY shorts.

- CNY swaps were heavily used in recent years on the other side of the trade: during the later years of the Biden admin Chinese exporters would use swaps to hold USD exposure while USDCNY rose, but allow them to settle supplier and tax payments in the local currency - which raised the supply of USD with state banks, which could then be sold in spot markets to contain USDCNY strength.

- As such, this week's behaviour can be seen as a more concerted effort to slow the decline in USDCNY (on top of recent strong fixings) as it not only raises the USDCNY spot price, but disincentivises exporters from accumulating CNY as a hedge to lock in margins.

OPTIONS: Expiries for Dec04 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E4.1bln), $1.1600(E2.2bln), $1.1650(E2.3bln), $1.1675(E1.6bln), $1.1700(E708mln)

- USD/JPY: Y153.00($1.2bln), Y154.00($900mln), Y155.50-70($1.6bln)

- GBP/USD: $1.3030-50(Gbp2.1bln)

- AUD/NZD: N$1.1365(A$600mln)

EQUITIES: E-Mini S&P Continues to Trade Close to Its Recent Highs

- Recent gains in Eurostoxx 50 futures undermine a recent bearish theme and the contract continues to appreciate. Price has recently cleared the 20- and 50-day EMAs, signalling scope for a stronger recovery. Sights are on 5742.40 next, the 76.4% retracement of the Nov 13 - 21 bear leg. A break would open 5825.00, the Nov 13 high and a key resistance. First support lies at 5612.78, the 50-day EMA.

- A bullish theme in S&P E-Minis is intact and the contract is trading at its recent highs. Price also remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight scope for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low.

COMMODITIES: Short-Term Gains for WTI Still Considered Technically Corrective

- Short-term gains in WTI futures are considered corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend condition in Gold is unchanged and remains bullish. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4016.8. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 04/12/2025 | 1245/1245 | BOE Mann Panel at European and Global Issues Conference | ||

| 04/12/2025 | 1300/1400 | ECB Cipollone Chairs Panel on Fiscal Policy | ||

| 04/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 04/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 04/12/2025 | 1500/1000 | * | Ivey PMI | |

| 04/12/2025 | 1500/1600 | ECB Lane at Fiscal Policy Conference | ||

| 04/12/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/12/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/12/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 04/12/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 04/12/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 04/12/2025 | 1730/1230 | Fed Vice Chair Michelle Bowman | ||

| 04/12/2025 | 1800/1900 | ECB de Guindos Speech at Business Innovation Awards | ||

| 05/12/2025 | 2330/0830 | ** | Household spending | |

| 05/12/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/12/2025 | 0730/0730 | DMO to publish issuance calendar for FQ4 | ||

| 05/12/2025 | 0745/0845 | * | Industrial Production | |

| 05/12/2025 | 0745/0845 | * | Foreign Trade | |

| 05/12/2025 | 0800/0900 | ** | Industrial Production | |

| 05/12/2025 | 0900/1000 | * | Retail Sales | |

| 05/12/2025 | 1000/1100 | *** | EZ GDP 3rd (Regular) | |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey | |

| 05/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 05/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 05/12/2025 | 1500/1000 | *** | Personal Income and Consumption | |

| 05/12/2025 | 1510/1610 | ECB Lane in Panel at CEPR Paris Symposium | ||

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 2000/1500 | * | Consumer Credit |