MNI US MARKETS ANALYSIS - Curve Steeper, USD Softer

Highlights:

- Curve bear steepens, USD sells off on Moody's sovereign downgrade

- Fedspeak thick and fast as Atlanta Fed policy conference kicks off

- European Commission slash growth, inflation forecasts in face of Trump tariffs

- Trump-Putin call set for Monday, Moscow believe they hold the cards

US TSYS: Bear Steeper As Last AAA Shoe Drops

- Treasuries have firmly bear steepened, primarily in continued reaction to the Moody’s downgrade late Friday but also with heavy supply impacting EGBs.

- Moody’s on Friday downgraded the US from Aaa to Aa1, the last of the major rating agencies to downgrade from AAA. As noted earlier, bank’s risk-weighted capital asset calculations shouldn’t be materially impacted following changes in prior episodes. It does however help build on long-end angst seen in particular since early April.

- The House Budget Committee approved President Trump’s tax and spending package late Sunday night after an agreement to speed up cuts to Medicaid health coverage appeased four Republicans who subsequently abstained from the vote.

- Cash yields are 0.7-7.9bp higher since Friday’s close, with increases led by 30s.

- 30Y yields have seen highs of 5.0269% (currently 5.0227) for highs since Nov 2023, in clearance of the 5% handle that had proved solid resistance in the interim.

- 5s30s is 3.8bp higher at 89.3bps, still shy of the multi-year high of 100bps on May 1.

- 2s10s has seen a more pronounced steepening on the day and intra-session however, currently +5.9bps at 54.2bps for highs since May 6.

- TYM5 trades at 109-24 (-18+) having earlier hit 109-22+, on elevated cumulative volumes of 540k.

- It has stopped short of probing support at 109-18+ (May 15 low), after which lies a key 109-08 (Apr 11 low), with US desks filtering in, having on Friday bottomed out at 109-31 in the initial reaction in late US trading.

- Data: Conference Board Leading Index Apr (1000ET)

- Fedspeak: Bostic (0830ET), Jefferson (0845ET), Williams (0845ET), Logan (1315ET), Kashkari (1330ET), Bostic (1445ET) – see our Fedspeak bullet 0604ET.

- Bill issuance: US Tsy $76B 13W & $68B 26W bill auctions

US TSYS: Bear Steepening Extends As 30s Hover Round 5%; Does Downgrade Matter?

UST bear steepening has extended this morning, as markets digest Moody’s US ratings downgrade late Friday. While the move may not have been expected, Moody’s were previously the last of the three major agencies to still assign the top rating (Aaa) to US debt.

- US 5s30s is 5bps higher at 90bps, still shy of the multi-year high of 100bps on May 1.

- 30-year yields are up 5bps, hovering around the 5% handle once again. This level has provided solid resistance since Q4 2023, and was most recently respected last Thursday.

- As noted above, early moves in USD FX suggest the deterioration in US credit worthiness was partially priced in through the recent tax bill headlines and tariff volatility. Meanwhile, Tsy Secretary Bessent played down the ratings action over the weekend, noting Moody’s – and ratings agencies more generally – were a “lagging indicator” of US fiscal health.

- Over the weekend, FT Alphaville weighed in on whether the downgrade matters from a technical perspective. They wrote that “banks’ risk-weighted capital asset calculations look unlikely to be impacted by the rating change. This is because regulators don’t tend to differentiate between Aaa and Aa1 when setting capital risk-weights”.

- Additionally, they cited Barclays research that noted: “For collateral purposes, a downgrade to Aa1 is also unlikely to have an effect. For instance, DTCC and CME refer to the asset class as US Treasuries and the haircut is a function of the maturity and security type (TIPS/FRNs) but not the ratings. At LCH, a downgrade to Aa1 is unlikely to lead to a change. For instance, USTs and Gilts have similar haircuts, even as the latter are rated lower”….”Legislation since the financial crisis has reduced the use of explicit ratings guidelines in investment mandates”.

STIR: Next Fed Cut Eyed In Sept or Oct Despite Trump Pleas

- Fed Funds implied rates are up to 2bp lower from Friday’s close for 2025 meetings as lower equity and and crude oil futures weigh (S&P 500 -1.3%, WTI -1.1%).

- They’re still close to recent hawkish extremes though, with a next Fed cut only fully priced for October (but still close with Sept).

- Cumulative cuts from 4.33% effective: 2bp Jun, 9.5bp Jul, 22.5bp Sep, 35bp Oct and 52bp Dec.

- SOFR implied yields are increasingly higher further out the curve though, amidst Treasury market steepening following Moody’s downgrading the US from Aaa to Aa1 on Friday,.

- The terminal yield of 3.40% (SFRZ6) is 3bp higher on the day, back close to levels seen just prior to Apr 2 Liberation Day announcements. It pushed as high as 3.485% last week (for pricing at close) but struggled to hold onto the move. SFRZ7 meanwhile is 5.5bp higher.

- President Trump offered his latest criticism of the Fed’s Powell on Saturday. His May 17 Truth Social post: “THE CONSENSUS OF ALMOST EVERYBODY IS THAT, “THE FED SHOULD CUT RATES SOONER, RATHER THAN LATER.” Too Late Powell, a man legendary for being Too Late, will probably blow it again - But who knows???”

- Today’s docket is led by Fedspeak – see our 0604ET bullet on why we think main focus there should be on ’26 voters Kashkari and Logan.

US TSY FUTURES: CFTC CoT Points To Sizable Fund & A Manager Cover In FV

The latest CFTC CoT report revealed a bias towards cover of existing positions for both asset managers and leveraged funds, with a particular focus on trimming exposure in FV futures.

- Note that leveraged funds did still manage to add a cumulative ~$6mn DV01 equivalent of net shorts across TY, US & WN.

- Asset managers remain net long across the curve, while leveraged funds are net short across all contracts.

- Wider non-commercial positioning saw a mix of net short setting and cover, with the cohort remaining net short across the curve (see table below).

STIR: Mix Of Positioning Swings On SOFR Strip On Friday

OI data points to a mix of net short setting, long cover and long setting dominating as the SOFR futures strip twist flattened on Friday.

- Net short setting was seen in the very front end, before net long cover was noted in SFRZ5 through M6.

- Net long setting then dominated beyond SFRU6.

| 16-May-25 | 15-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,058,780 | 1,032,945 | +25,835 | Whites | +63,591 |

SFRM5 | 1,249,244 | 1,213,288 | +35,956 | Reds | +14,077 |

SFRU5 | 1,090,328 | 1,084,372 | +5,956 | Greens | +46,427 |

SFRZ5 | 1,123,485 | 1,127,641 | -4,156 | Blues | +4,539 |

SFRH6 | 779,118 | 783,855 | -4,737 |

|

|

SFRM6 | 737,016 | 757,676 | -20,660 |

|

|

SFRU6 | 745,767 | 745,326 | +441 |

|

|

SFRZ6 | 899,687 | 860,654 | +39,033 |

|

|

SFRH7 | 706,550 | 686,078 | +20,472 |

|

|

SFRM7 | 603,490 | 584,829 | +18,661 |

|

|

SFRU7 | 378,708 | 376,289 | +2,419 |

|

|

SFRZ7 | 402,562 | 397,687 | +4,875 |

|

|

SFRH8 | 265,697 | 263,003 | +2,694 |

|

|

SFRM8 | 189,836 | 187,909 | +1,927 |

|

|

SFRU8 | 150,891 | 151,507 | -616 |

|

|

SFRZ8 | 164,753 | 164,219 | +534 |

|

|

GILTS: Sell Off & Steepening Extends

Gilts remain under pressure as Tsys soften in the wake of the U.S. sovereign rating downgrade from Moody’s late on Friday.

- Futures are through next support and the bear trigger (90.96) and have pierced Fibonacci support (90.92), with bears now eying the April 11 low (90.47). lows of 90.86 so far.

- Yields are 3-9bp higher, curve steeper.

- 10-Year yields register the highest level of the month 4.726%, with the next upside level of note at the April high (4.800%).

- 30-Year yields also hit the highest level of the month (5.492%), with the April 11 high (5.546%) presenting the next area of upside interest.

- 10s spread vs. Bunds 1bp wider at 206.5bp, set for the highest close since April 22.

- GBP STIRs move in a hawkish direction given the sell off further out the curve.

- SONIA futures little changed to -7.5.

- BoE-dated OIS little changed to 1.5bp more hawkish across ’25 meetings showing ~41bp of cuts through year-end.

- Wednesday’s CPI data headlines the UK calendar this week. We have written a little on that in our global week ahead/late Friday bullets, expect more in our full preview.

MACRO OUTLOOK: EC Downgrades Euro Area Growth, Inflation Outlook

Our Policy Team on the EC Forecast Update:

- The European Commission has significantly downgraded its Euro Area's growth and inflation outlook due to the weaker global trade environment as well as the continuing uncertainty surrounding US tariff policy.

- The EC revised EA growth for the year down to 0.9% for this year and to 1.4% for next year from the 1.3% and 1.6% forecast in the autumn. Inflation was also revised down to 2.1% and 1.7% in 2025 and 2026 from the 2.4% and 2.0% estimates made in the autumn forecast.

- Based its forecasts on certain assumptions around US tariff policy, specifically a 10% US tariff on EU exports, as had been the case until April 9, along with a 25% tariff on cars and steel and exemptions for pharma products and microprocessors. Brussels add that while the negotiated US-China tariff deal turned out lower than it had assumed, it was still big enough to cause a "big hit" to US-China trade.

EUROZONE DATA: Q1 Negotiated Wages Seen Around 2.5-2.7% Y/Y On Friday

Although Thursday's May flash PMIs headline this week's Eurozone data calendar, there will also be interest in the ECB’s Q1 negotiated wages print on Friday. There isn’t a solid consensus for the data, but the ECB’s forward looking wage tracker alongside some sell-side estimates we have seen suggest a reading around 2.5-2.7% Y/Y. This should be viewed as consistent with existing ECB projections, and have limited impact on rate cut pricing.

- Q4 ‘24 negotiated wages were 4.13% Y/Y, down from 5.43% in Q3. This indicator can be volatile quarter-to-quarter, as it includes one-off payments in wage agreements.

- The ECB’s forward looking wage tracker, which is publicly released the Wednesday after each monetary policy decision, currently tracks wages with unsmoothed one-off payments at 2.51% Y/Y.

- The smoother ex-one-off payments tracker is currently at 4.43% Y/Y for Q1.

- The March Eurozone Indeed wage tracker was 2.67% Y/Y (vs 2.86% in February).

- The ECB projects Q1 compensation per employee growth at 3.8% Y/Y (vs 4.09% in Q4). This data will be released on June 6 alongside the final Q1 national accounts, the day after the ECB’s June decision.

- Summarising a few recent sell side views on negotiated wage growth:

- Morgan Stanley: “In January and February, euro area negotiated wages were running around 3.1%Y. As per preliminary data from Destatis, the year-on-year growth rate of German negotiated wages in March could be very low, maybe even negative, because of base effects from very large one-off payments in the same month last year (mostly in the public sector). If confirmed (we will have German March data from Bundesbank on Thursday), this would push down the quarterly reading for the euro area to, we think, 2.7%Y in 1Q25”.

- Nomura: “We forecast euro area negotiated wage growth to slow to 2.6% y-o-y in Q1 2025”…”Our euro area aggregate forecast is based on 65% of country-level data that are already available and our expectations for the remaining data. The main elements not yet published are German data for March 2025 and French data for the entirety of Q1 2025”.

FOREX: EUR Main Beneficiary From US-Triggered Risk Off

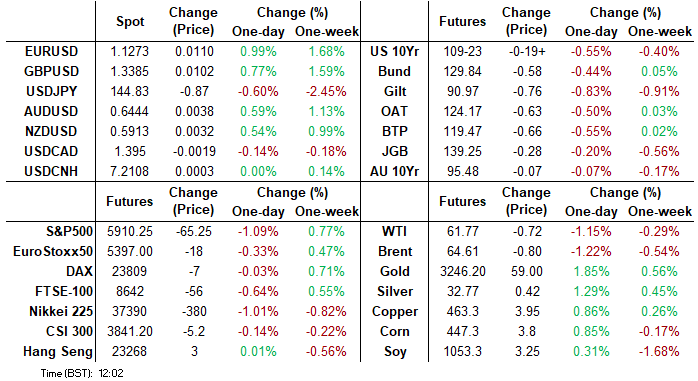

Today's EUR/USD rally extends the post-Moody's downgrade move to almost 125 pips, with a new daily high of 1.1274 clearing the May 14 high and marking a clean break of the downtrendline resistance drawn off the May 6th high on the 15min candle chart - a bullish signal.

- USD weakness is accompanying the higher, steeper US yield curve - supporting the view that today's USD move is based on lower US credit worthiness and may complicate the reaction function to risk-off in the near-future. EUR has been the main beneficiary, with early JPY strength fading into NY hours.

- Moody's actions make fiscal news this week more market-relevant, even as the Treasury see the ratings themselves as "lagging indicators" and could strengthen the hand of fiscally conservative lawmakers who argue against unfunded spending pledges in Trump's Big Beautiful Tax Bill. This may have played a part in Republican hardliners winning accelerated cuts to Medicaid in weekend negotiations.

- The downgrade adds additional weight to the importance of the debt ceiling - Bessent noted that the US would exhaust borrowing authorities by August if the ceiling isn't raised or suspended by then - far from the base case, but still a concern for markets.

FOREX: CHF, JPY Fail to Benefit as Global Bonds Backtrack

- Both JPY and CHF underperform against EUR, GBP and Scandi FX, failing to benefit from equity weakness and the risk-off tone following the Moody's US downgrade. - However, CHF and JPY's relative underperformance is consistent with higher yields and steeper curves across bond markets, and further questions around US credit worthiness could keep the pressure on low-yielding currencies.

- Moves are most apparent against the Euro, with EURJPY at 163.27 after clearing its 20-day EMA. Initial resistance is clustered at a set of highs just above 164.00 ahead of the key 165.21 level, the May 13 high and bull trigger.

- EURCHF continues to trade within recent ranges, and just below resistance at 0.9447, the highs seen on April 25. A break of that level would open up a set of highs slightly above the 0.95 handle.

COMMODITIES: WTI Future Downtrend Intact Despite Recent Test of Key Resistance

- A downtrend in WTI futures remains intact and recent gains are considered corrective. Key resistance to watch is $62.93, the 50-day EMA. It has recently been pierced, a clear break of it would highlight a stronger reversal. This would open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. Clearance of this support would confirm a resumption of the downtrend.

- A corrective cycle in Gold remains in play and the metal traded lower last week. A key support at $3202.0, the May 1, low has been breached. The break of this level signals scope for a deeper retracement, towards $3085.0, 76.4% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA at $3169.4, has also been breached, strengthening a bearish threat. Initial resistance is $3259.5, the 20-day EMA.

EQUITIES: Bullish Theme in Eurostoxx Futures Intact With Price at Recent Highs

- A bullish theme in Eurostoxx 50 futures remains intact and price is trading at its recent highs. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5181.06, the 50-day EMA. Clearance of this level would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and last week’s appreciation reinforces current conditions. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5681.27, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 19/05/2025 | 1245/0845 | New York Fed's John Williams | ||

| 19/05/2025 | 1245/0845 | Fed Vice Chair Philip Jefferson | ||

| 19/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 19/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 19/05/2025 | 1715/1315 | Dallas Fed's Lorie Logan | ||

| 19/05/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 20/05/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 20/05/2025 | 0600/0800 | ** | PPI | |

| 20/05/2025 | 0800/1000 | ** | EZ Current Account | |

| 20/05/2025 | 0800/0900 | BOE's Pill At Barclays Briefing | ||

| 20/05/2025 | 0900/1100 | ** | Construction Production | |

| 20/05/2025 | 1000/1200 | ECB's Cipollone pre-rec video at Sustainability Festival | ||

| 20/05/2025 | - | ECB's Lagarde and Cipollone at G7 Meeting | ||

| 20/05/2025 | 1230/0830 | *** | CPI | |

| 20/05/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 20/05/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 20/05/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/05/2025 | 2100/1700 | Fed Governor Adriana Kugler |