MNI US MARKETS ANALYSIS - Breakthrough Unlikely in France & US

Highlights:

- Government shutdown enters 7th day, Fedspeak in focus

- Lecornu re-enters negotiations, but near-term breakthrough in France unlikely

- Heavy supply docket weighs on core bonds

US TSYS: Hovering Around Yesterday’s Lows Ahead Of A Multi-Pronged Session

- Treasuries are mildly lower across the curve, broadly back close to yesterday’s lows although with 10s earlier nudging through them.

- Volumes are light ahead of a session that sees focus on government shutdown prospects (which continues to curtail some data releases), a Trump-Carney meeting, 3Y supply and Fedspeak.

- NYT: “President Trump briefly dangled the possibility of a negotiation with Democrats, only to pull back several hours later — insisting that Democrats must end the standoff first before he would be willing to make a deal on health care.”

- Cash yields are 1-1.4bp higher across the curve.

- TYZ5 trades at 112-11 (-01) at yesterday’s low, having earlier probed it with 112-10+, amidst thin overnight volumes of 175k.

- Those thin volumes have seen a lack of conviction to materially push below support at 112-12 (50-day EMA) after which lies 112-01 (50% of Jul 15 – Sep 11 upleg).

- Data: Redbook retail sales (0855ET), NY Fed consumer survey Sep (1100ET), Consumer credit Aug (1500ET) – trade report delayed by government shutdown.

- Fedspeak: Bostic (1000ET), Bowman (1005ET), Miran (1030ET), Kashkari (1130ET), Miran (1605ET) – see FED bullet.

- Coupon issuance: US Tsy $58B 3Y Note auction - 91282CPC9 (1300ET). Last month’s 3Y auction was solid, stopping through by 0.7bp and with the bid-to-cover rising from 2.53x to 2.73x.

- Bill issuance: US Tsy $90B 6W bill auction (1130ET)

- Politics: Trump-Carney bilateral meeting at White House (1145ET) before bilateral lunch (1215ET)

FED: Two-Week Updates From Four FOMC Members

Today’s Fedspeak might see greater focus considering the continued shutdown-thinned data calendar. We hear from four separate speakers, who have all appeared since the Sep 16-17 FOMC meeting but not for the past two weeks.

- 1000ET – Bostic (non-voter, hawk) at Fisk University (audience Q&A only). He reiterated on Sep 22 that he pencilled in only one rate cut for 2025 before adding on Sep 23 that the Fed definitely needs to be concerned about inflation with more inflation to come. He’d be open to using a range for the inflation target.

- 1005ET – VC Supervision Bowman (voter, dove) welcoming remarks at Community Banking conference (text only). She said Sep 26 that it’s time to act decisively and proactively to protect jobs but that she prefers a gradual approach to rate changes. She prefers the smallest possible balance sheet.

- 1030ET – Gov. Miran (voter, outright dove) in fireside chat at MFA Policy Outlook (moderated Q&A only). He was the September dot looking for 150bp of cuts to 2.75-3.0% by end-2025 and with appropriate rates in “the mid-2 percent area”. He laid out his rationale in a speech on Sep 22, heavily focused on his estimates of the neutral rate: https://www.federalreserve.gov/newsevents/speech/miran20250922a.htm

- 1130ET – Kashkari (’26 voter) in conversation on AI and the economy. Speaking a few days after the Sept FOMC decision, he said on Sep 19 that two more rate cuts this year are appropriate and that he’s more confident that tariffs will have a one-time effect on inflation. He is confident that underlying inflation will head down.

- 1605ET – Gov. Miran (voter) at Deutsche Bank macro conference (moderated Q&A only)

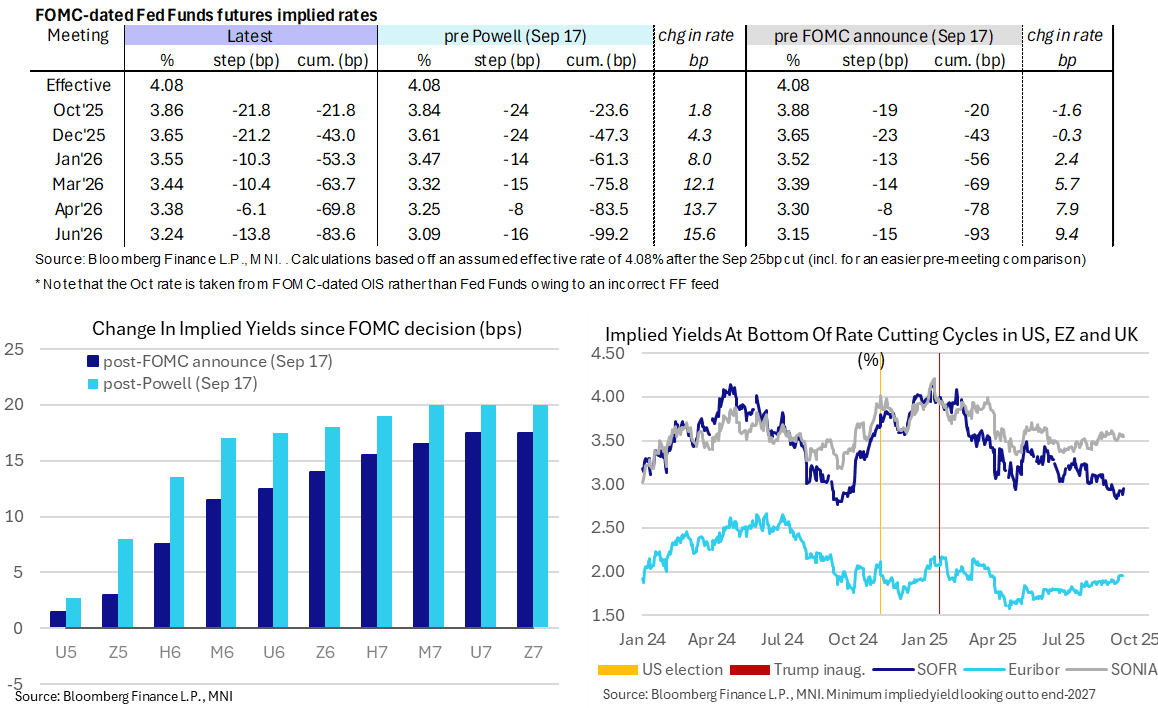

STIR: Fed Rates Little Changed

- Fed Funds implied rates are broadly 1bp higher on the day, with the mild increase coming in London hours rather than in response to typically hawkish comments from Schmid late yesterday (policy in right place, only sightly restrictive).

- Cumulative cuts from 4.08% effective: 22bp Oct, 43bp Dec, 53.5bp Jan, 64bp Mar, 70bp Apr and 83.5bp Jun.

- SOFR futures mild losses are led by the M6 (-0.01) and otherwise little changed at -0.005.

- The SOFR implied terminal yield at 3.085% (~100bp of cuts from current levels) is seen in the Z6 and H7 contracts, having ticked into the Z6 yesterday for the first time since mid-July.

- It remains off recent highs of 3.11/3.12% seen in late September (looking at closes).

US TSY FUTURES: Offsetting Short Setting & Long Cover Seen On Monday

OI data points to a mix of net short setting (TU, FV & US) and long cover (TY, UXY & WN) as Tsy futures ticked lower on Monday, although the two were near enough perfectly offsetting in DV01 terms.

- The net long cover in TY futures provided the most meaningful DV01 swing on the day (~$3.0mln).

| 06-Oct-25 | 03-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,590,941 | 4,576,722 | +14,219 | +559,052 |

FV | 6,714,559 | 6,689,272 | +25,287 | +1,104,069 |

TY | 5,429,931 | 5,475,093 | -45,162 | -3,042,257 |

UXY | 2,462,211 | 2,464,467 | -2,256 | -203,017 |

US | 1,886,981 | 1,871,029 | +15,952 | +2,247,022 |

WN | 2,052,180 | 2,055,193 | -3,013 | -556,292 |

|

| Total | +5,027 | +108,577 |

SOFR: Net Short Setting Dominated In Futures On Monday

OI data suggests that net short setting dominated through the blues as SOFR futures ticked lower on Monday, with only a couple of limited rounds of net long cover seen.

| 06-Oct-25 | 03-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,419,164 | 1,413,218 | +5,946 | Whites | +49,941 |

SFRZ5 | 1,489,327 | 1,478,236 | +11,091 | Reds | +39,345 |

SFRH6 | 1,183,700 | 1,157,361 | +26,339 | Greens | +23,873 |

SFRM6 | 1,031,799 | 1,025,234 | +6,565 | Blues | +10,374 |

SFRU6 | 990,023 | 985,701 | +4,322 |

|

|

SFRZ6 | 1,023,362 | 1,008,718 | +14,644 |

|

|

SFRH7 | 796,745 | 785,221 | +11,524 |

|

|

SFRM7 | 793,166 | 784,311 | +8,855 |

|

|

SFRU7 | 682,142 | 679,226 | +2,916 |

|

|

SFRZ7 | 744,518 | 729,508 | +15,010 |

|

|

SFRH8 | 429,083 | 422,857 | +6,226 |

|

|

SFRM8 | 356,843 | 357,122 | -279 |

|

|

SFRU8 | 299,198 | 289,697 | +9,501 |

|

|

SFRZ8 | 317,465 | 315,874 | +1,591 |

|

|

SFRH9 | 190,094 | 188,187 | +1,907 |

|

|

SFRM9 | 166,503 | 169,128 | -2,625 |

|

|

EUROPE ISSUANCE UPDATE

EU dual-tranche syndication: Final terms

- E5bln - in line with initial guidance (MNI expected E4-5bln) of the 2.75% Dec-32 EU-bond. Spread set at MS + 34bps (guidance was MS + 36bps area), Books in excess of E81bln (inc E7bln JLM interest)

- E6bln - up from initial E5bln guidance (MNI expects E5-6bln) of the New 15-year Dec-2040 EU-bond. Spread set at MS + 75bps (guidance was MS + 77bps area, Books in excess of E78bln (inc E6.75bln JLM interest).

Austria auction results

- E575mln (E500mln allotted) of the 2.95% Feb-35 RAGB. Avg yield 2.997% (bid-to-cover 3.01x; bid-to-issue 2.62x).

- E575mln (E500mln allotted) of the 3.15% Oct-53 RAGB. Avg yield 3.742% (bid-to-cover 2.85x; bid-to-issue 2.47x).

Germany auction results

- E4.5bln (E3.405bln allotted) of the 2.20% Oct-30 Bobl. Avg yield 2.31% (bid-to-offer 0.84x; bid-to-cover 1.11x).

11:57:22 Pressed enter too early

11:59:42 EU dual-tranche syndication: Final terms - E5bln - in line with initial guidance (MNI expected E4-5bln) of the 2.75% Dec-32 EU-bond. Spread set at MS + 34bps (guidance was MS + 36bps area), Books in excess of E81bln (inc E7bln JLM interest)

- E6bln - up from initial E5bln guidance (MNI expects E5-6bln) of the New 15-year Dec-2040 EU-bond. Spread set at MS + 75bps (guidance was MS + 77bps area, Books in excess of E78bln (inc E6.75bln JLM interest).

UK auction results

- Decent demand at the long 2-year 0.125% Jan-28 gilt tender - but a small size of GBP1.25bln so no real wider market implications likely.

- GBP1.25bln of the 0.125% Jan-28 Gilt. Avg yield 3.783% (bid-to-cover 3.84x, tail 0.4bp).

Austria auction results

- That the prices achieved at the Austrian RAGB auction are both notably above the secondary market prices going into the end of the bidding window.

- For the 10-year 2.95% Feb-35 RAGB the lowest accepted price of 99.600 was higher than the secondary market priced we have seen all day (Bloomberg data quotes 99.447 today).

- RAGBs rallied in response.

- E575mln (E500mln allotted) of the 2.95% Feb-35 RAGB. Avg yield 2.997% (bid-to-cover 3.01x; bid-to-issue 2.62x).

- E575mln (E500mln allotted) of the 3.15% Oct-53 RAGB. Avg yield 3.742% (bid-to-cover 2.85x; bid-to-issue 2.47x).

Germany auction results

- The 1.11x bid-to-cover achieved at today's auction of the 2.20% Oct-30 Bobl was the joint lowest at a Bobl auction since July 2021 (1.11x was also reached in July 2022). Bid-to-offer also very weak at 0.84x.

- Demand metrics were similarly weak for other parts of the German curve recently but this has been the first time this has filtered through to the extent seen today to the Bobl segment.

- The low price achieved at the auction (99.48) was above the secondary market mid-price right before the cutoff (99.467), at least.

- No discernible price impact of the weak results on the line, this is not untypical for German auctions.

- E4.5bln (E3.405bln allotted) of the 2.20% Oct-30 Bobl. Avg yield 2.31% (bid-to-offer 0.84x; bid-to-cover 1.11x).

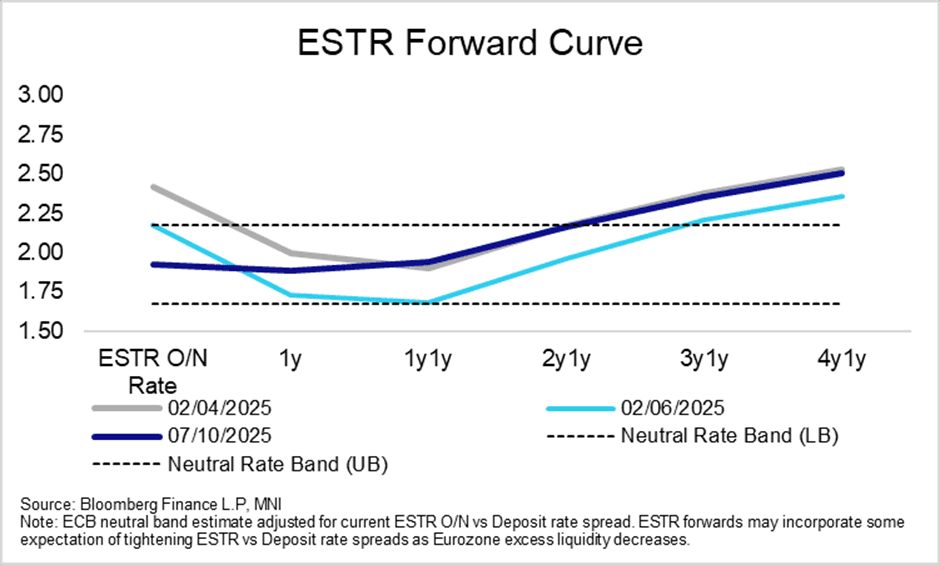

STIR: Front-end EUR Rates Vol Still Compressed, Near-term Hikes Not On The Radar

Compressed EUR front-end rates volatility remains a theme, with recent data/political developments not enough to tempt ECB officials from deviating from the well-signalled “good place” stance. President Lagarde yesterday re-iterated the data dependent approach. The immediate fallout from French (ex-) PM Lecornu’s resignation yesterday sparked a fleeting ~2.5 tick rally in the likes of ERU6, but these moves quickly faded.

- It’s notable that the ESTR forward curve from the 1y1y point onwards is currently very similar to the April 2 close (i.e. just before Trump’s Liberation Day announcement). Markets have fully unwound the early April uptick in trade policy uncertainty, with focus now on the direct (rather than indirect) impacts of tariffs and the implementation of German fiscal stimulus.

- We think markets are justified in pricing in some implied probability of hikes over the coming years to account for increased fiscal stimulus, but believe that the risk of another cut still comfortably outweighs the risk of a hike (Chief Economist Lane explicitly said as much yesterday). It’s also historically been rare for the ECB to be hiking at the same time as a Fed cutting cycle, though the idiosyncratic nature of proposed German stimulus measures may caution too much reliance on past trends.

- ECB-dated OIS continue to price ~10bps of easing through the middle of next year.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Oct-25 | 1.926 | 0.1 |

| Dec-25 | 1.905 | -2.0 |

| Feb-26 | 1.892 | -3.3 |

| Mar-26 | 1.849 | -7.6 |

| Apr-26 | 1.842 | -8.3 |

| Jun-26 | 1.827 | -9.8 |

| Jul-26 | 1.828 | -9.7 |

| Sep-26 | 1.839 | -8.6 |

| Source: MNI/Bloomberg Finance L.P. | ||

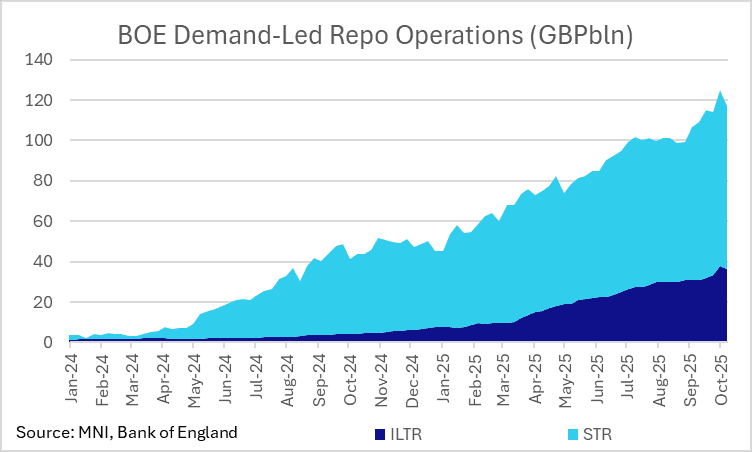

BOE: ILTR Usage Falls for First Time Since 3 June

- For the first time since 3 June, take up of the BOE's ILTR facility will be lower than the volume maturing from 6-months ago.

- Today's takeup will be GBP1.41bln lower than the amount due to roll off this week.

- It does, however, follow last week's strong take up of GBP5.085bln - the highest since the week the first Covid lockdown was announced.

- This follows last week's smaller STR usage which saw the biggest weekly fall (GBP6.565bln) in the facility's usage since 24 April - albeit this was unwinding a similar increase the prior week.

- This puts the total in the BOE's repo operations at GBP117.0bln, down from last week's GBP125.0bln - but still higher than the prior week's GBP113.9bln.

- The BOE likely won't be concerned, as week-to-week movements in response to different funding conditions are to be expected from these operations - and the flexible nature of these operations and high frequency (weekly) is designed to help market functioning.

FOREX: EURJPY Pressed Higher Despite Ongoing French Woes

- The initial fade in the JPY on Monday stalled as advisor Honda talked up governmental support for a December BoJ rate hike, however the currency is on the back foot again early Tuesday, helping usher in new weekly highs for USDJPY at 150.83. The move narrows the gap with key resistance and the bull trigger in the pair at 150.92, clearance above which puts prices at the best level since late March. Takaichi's victory in the LDP leadership race remains the primary driver here, with local press focusing on her negotiations with junior coalition partners - who oppose her more conservative political views.

- EURJPY's rally to new alltime highs this week is largely holding, with Tuesday seeing a 176.35 print, however ongoing fiscal and political concerns in France will be containing the strength. Implied EUR vols are steadying and appear to have halted their multi-month downtrend in the front-end. Calls for early Presidential and legislative elections in France to clear the political logjam have been rising - an unlikely occurrence in the very near-term, but a growing possibility given the government's inability to proceed with an acceptable budget.

- NZD is the poorest performing currency on the day, with AUD not far behind. Price action comes ahead of the RBNZ rate decision on Wednesday, at which markets are split between expecting a 25bps rate cut, or something more sizeable. Consumer confidence data in Australia also deteriorated, dragging AUDUSD toward the weekly lows of 0.6582.

- The ongoing US government shutdown keeps data further delayed, meaning today's trade balance data for August is unlikely to be released (and may have spillover impacts on the Canadian trade balance statistics, which are cross-referenced against the US numbers). As such, the speaker schedule is likely to be of more market importance: Fed's Bostic, Bowman, Miran & Kashkari are all set to appear and may shed some insight into the Fed's views on the shutdown ahead of the Minutes release tomorrow. ECB's Nagel & Lagarde are also on the calendar.

OPTIONS: Expiries for Oct07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650-65(E2.2bln), $1.1695-10(E869mln), $1.1750(E1.3bln), $1.1820(E2.3bln)

- USD/JPY: Y149.25($667mln), Y149.75($811mln), Y150.00($747mln), Y150.60($525mln), Y151.00($776mln)

- AUD/USD: $0.6675-90(A$630mln)

EQUITIES: Bullish Theme in E-Mini S&P Intact, Sights on $6812.29 Proj. Level

- Eurostoxx 50 futures remain in a bull-mode condition. Last week’s gains resulted in a breach of key resistance at 5525.00, the Aug 22 high. The break confirms a resumption of the uptrend. The impulsive climb opens the 5700.00 handle next, with potential for a test of 5727.18 further out, a Fibonacci projection. Moving average studies are in a bull-mode position too, highlighting a dominant uptrend. Initial firm support is 5525.00, Aug 22 high.

- A bull cycle in S&P E-Minis remains intact. The contract traded to a fresh cycle high last week to confirm a resumption of the uptrend and maintain the positive price sequence of higher highs and higher lows. Sights are on 6812.29, a Fibonacci projection. Initial support to watch is at the 20-day EMA, at 6694.17. It has recently been pierced, a clear break of it would signal scope for a deeper pullback, potentially towards the 50-day EMA, at 6575.48.

COMMODITIES: Fresh Cycle Highs in Gold Reinforces Current Conditions

- WTI futures remain in a bear-mode condition and gains are considered corrective. Last week’s sell-off resulted in a move through key support and the bear trigger at $60.85, the Aug 13 low. Clearance of this level strengthens a bearish theme and paves the way for an extension towards $57.50, the May 30 low. Initial firm resistance has been defined at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal.

- A bull cycle in Gold remains in play and Monday’s fresh cycle high, reinforces current conditions. This maintains the price sequence of higher highs and higher lows. Furthermore, momentum studies highlight a condition known as momentum drag - where momentum studies remain in overbought territory and move sideways - a bullish signal. Sights are on $3987.3 next, a Fibonacci projection. Support to watch lies at $3753.2, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 07/10/2025 | 1400/1000 | * | Ivey PMI | |

| 07/10/2025 | 1405/1005 | Fed's Miki Bowman | ||

| 07/10/2025 | 1430/1030 | Fed Governor Stephen Miran | ||

| 07/10/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/10/2025 | 1530/1130 | Minneapolis Fed's Neel Kashkari | ||

| 07/10/2025 | 1610/1810 | ECB Lagarde Speech at Business France Event | ||

| 07/10/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 07/10/2025 | 1900/1500 | * | Consumer Credit | |

| 07/10/2025 | 2005/1605 | Fed Governor Stephen Miran | ||

| 08/10/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 08/10/2025 | 2330/0830 | ** | average wages (p) | |

| 08/10/2025 | 2350/0850 | Balance of Payments | ||

| 08/10/2025 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 08/10/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/10/2025 | 0600/0800 | ** | Industrial Production | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr | ||

| 08/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 08/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 08/10/2025 | 1500/1600 | BOE Pill Speech at University of Birmingham | ||

| 08/10/2025 | 1600/1800 | ECB Lagarde Video Message at Werner Report Event | ||

| 08/10/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 08/10/2025 | 1800/1400 | FOMC Minutes | ||

| 08/10/2025 | 1915/1515 | Minneapolis Fed's Neel Kashkari | ||

| 08/10/2025 | 2145/1745 | Fed Governor Michael Barr |