MNI US MARKETS ANALYSIS - Bonds Bounce on Renewed Haven Flow

Highlights:

- Bonds bounce as markets see greater risk of broad trade disruption

- US 10y yield edges toward 4.00% as a result, with the USD bid

- Soft UK jobs data prompts markets to re-price 2026 easing plans

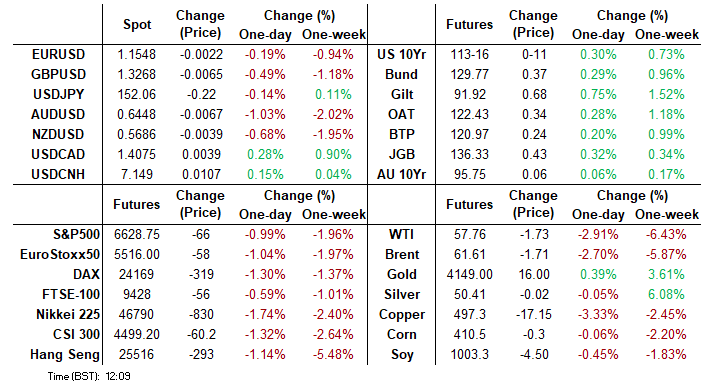

US TSYS: 10Y Yields Probe 4.00% In Broad Haven Demand

- Treasuries trade firmer across the curve in further reaction to US-China trade tensions which continued overnight.

- Headlines confirmed that China were ratcheting higher their controls on rare earth exports. On a related note from the WSJ: “People close to the Trump administration say the U.S. side likely will demand that China rescind, not merely delay or water down the rare-earth export rule”.

- Cash trading has resumed after yesterday’s Columbus Day holiday although futures saw a full session.

- Today sees early focus on earnings before Powell’s economic update headlines the session, whilst markets will firmly be on headline watch for US-China trade prospects. Note also the holiday-compressed bill issuance calendar.

- A solid earnings schedule is being digested, with recent results from Blackrock, JPMorgan, Wells Fargo leading financials plus Johnson & Johnson. GS (expected 0730ET) and Citi (expected 0800ET) are still to come.

- Cash yields are 2-4bp lower, with 3s leading declines and 20s lagging.

- 10Y yields currently at 4.003% (-2.9bp) have seen support at 4.00%, briefly hitting 3.9976% having last been sub 4% briefly on Sep 17 and Sep 11. 10Y yields were last more materially sub-4% in early April under reciprocal tariff deliberations.

- TYZ5 trades at 113-16 (+11) on strong cumulative volumes of 550k.

- An earlier high of 113-17+ sits as the latest initial resistance level, building on Friday’s clearance of 113-00 as it increasingly looks to the bull trigger at 113-29 (Sep 11 high). Support meanwhile is seen at 112-15 (50-day EMA).

- Data: NFIB for Sept already published, Weekly Redbook retail sales (0855ET)

- Fedspeak: Bowman (0845ET), Powell (1220ET), Waller (1525ET), Collins (2030ET), Goolsbee (time unknown)

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET), $95B 6W bill auction (1300ET)

- Politics: Trump in bilateral lunch with Argentina President (1315ET), Trump in Charlie Kirk ceremony (1600ET)

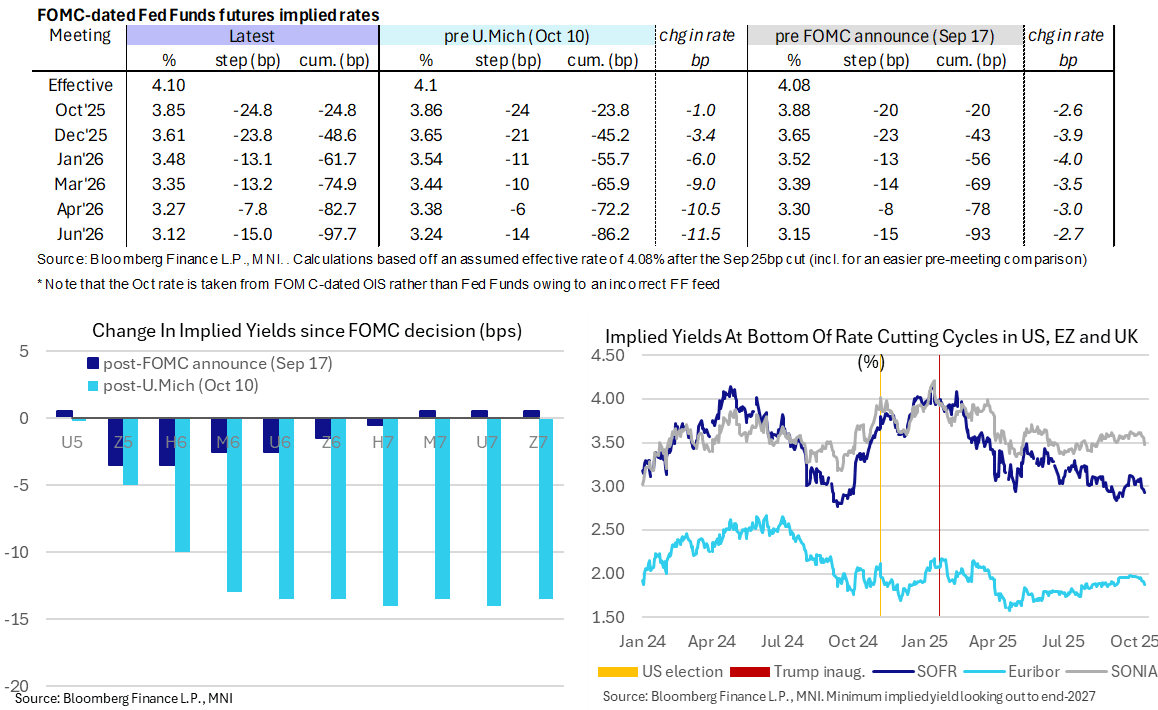

STIR: Terminal Fed Rates Extend Recent Decline, Powell Eyed

- Fed Funds implied rates range from unchanged on the day to 2.5bp lower out in mid-2026 in a continuation of US-China trade tensions.

- Cumulative cuts from an assumed 4.10% effective: 25bp Oct, 48.5bp Dec, 61.5bp Jan, 75bp Mar, 82.5bp Apr and 97.5bp Jun.

- SOFR futures range from near unchanged to up to +4.5 ticks when looking out to end 2027.

- It sees the implied terminal yield now down to 2.925% (SFRH7, -4bp), implying ~120bp of cuts ahead depending on fixed rate assumptions.

- Looking at daily closes, this terminal yield recently bottomed at 2.84% on Sep 8 vs cycle lows of 2.77% in Sep 2024 ahead of the then start of the FOMC’s easing cycle.

- Powell’s remarks on the economic outlook and monetary policy at 1220ET should headline today’s economic calendar – more to follow on this shortly.

FED: Powell To Lead Fedspeak In First Address Since Sept FOMC Presser

Today sees a return of heavier Fedspeak, all with voting roles this year (three permanent and two on rotation). The most focus will clearly be on Fed Chair Powell’s update at 1220ET in the last week before the media blackout begins this weekend ahead of the Oct 28-29 FOMC meeting.

- These will be Powell’s first notable remarks since the Sep 17 FOMC press conference (MNI Review, here), where a lack of clarity on delivering future cuts shown in the accompanying SEP prompted a hawkish reversal of an initially dovish reaction to the rate decision and SEP.

- Powell best summed up the decision to cut rates last month as “a risk management cut”. He said that the Committee’s diverse opinions on the rate path ahead – as encapsulated by a wide dispersion in the Dot Plot and a continued split on year-end 2025 rates – reflected difficult choices that would have to be addressed on a “meeting-by-meeting” basis: “it's not a bad economy or anything like that. We've seen much more challenging economic times but from a policy standpoint… it's challenging to know what to do…there are no risk-free paths now. It's not incredibly obvious what to do, so we have to keep our eye on inflation. At the same time, we cannot ignore and must keep our eye on maximum employment.”

- Powell said that while a move “toward the direction of neutral” was warranted, when asked, he wouldn’t commit to saying that an exit from restrictive policy was warranted. He said that “Over the course of this year, we’ve kept our policy at a restrictive level, and people have different views, but a clearly restrictive level, I would say so… [earlier in the year] the risks which were clearly tilted toward inflation, I would say they’re moving toward equality. Maybe they’re not quite at equality. We don’t need to know that. But we do know that they’ve moved meaningfully toward greater equality - the risks between the two goals. And that suggests that we should be moving in the direction of neutral. And that’s what we did today.”

- We’ll watch his comments on labor market risks. Last month’s remarks somewhat echoed last year’s August “pivot” ahead of easing, saying “we see that the labor market is softening and we don’t need it to soften anymore, don’t want it to.” But it was much less emphatic than in August 2024 when he presaged a 50bp cut the following month with: “We do not seek or welcome further cooling in labor market conditions…We will do everything we can to support a strong labor market as we make further progress toward price stability."

- The FOMC minutes from the meeting made it clear that members are looking at broad measures of labor market balance even more closely than would otherwise be the case. Markets will no doubt be attuned to Powell’s latest take here, likely influenced by liaison survey evidence (the Beige Book is publicly released tomorrow) and other private indicators amidst a lack of government data. The ADP employment report was of course notably weak at -32k in Sept after -3k in Aug.

Today’s schedule:

- 0845ET – VC Supervision Bowman (voter, dove) in moderated discussion at IIF (no text)

- 1220ET – Chair Powell (voter) on economic outlook and mon pol at NABE (text + Q&A)

- 1525ET – Gov. Waller (voter, dove) on payments panel at IIF (no text)

- 1530ET – Boston Fed’s Collins (’25) at Greater Boston Chamber of Commerce (text + Q&A)

- Time unknown - Chicago Fed's Goolsbee ('25) in morning podcast appearance "You Might Be Right"

US DATA: Small Businesses See Stronger Price Pressures In Sept After A Soft Aug

The NFIB small business survey saw a small decline in business confidence in September, with supply chain and inflation issues taking more prominence again after a dovish August report. Of note, the share expecting to increase prices over the next three months ticked back close to recent highs seen in June, more clearly consistent with above target inflation.

- The NFIB small business optimism index surprisingly fell 2pts in September to 98.8 (cons 100.6) after 100.8 in August, its first decline in three months for its lowest since June.

- From the overview (link): “While most owners evaluate their own business as currently healthy, they are having to manage rising inflationary pressures, slower sales expectations, and ongoing labor market challenges. Although uncertainty is high, small business owners remain resilient as they seek to better understand how policy changes will impact their operations.”

- “Supply chain and inflation issues stood out as a key problem in the report.” Indeed, price metrics bounced in this latest September survey after a dovish backdrop to August’s report.

- Specifically, the net share raising average selling prices compared to three months ago bounced back 3pts to 24% after the 21% reported in August was the lowest since Oct 2024. It averaged 23% in 2024 or ~12% pre-pandemic.

- The net share expecting to increase prices over the next three months meanwhile increased 5pts to 31%, close to June’s recent high of 32% after the 26% in August was its joint lowest since Sep 2024. This series averaged 28% in 2024 and 22% pre-pandemic, although it does of course remain far below some sustained readings in the 50s in 2021/22.

- “In September, 64% of small business owners reported that supply chain disruptions were affecting their business to some degree, up 10 points from August.”

- The already released jobs figures (link) had noted that “a seasonally adjusted 32% of all small business owners reported job openings they could not fill in September, unchanged from August. The last time unfiled job openings fell below 32% was in July 2020. […] A seasonally adjusted net 16% of owners plan to create new jobs in the next three months, up 1 point from August and the fourth consecutive monthly increase. Hiring plans are at their highest level since January.”

EUROPE ISSUANCE UPDATE

Gilt syndication: Allocations

- GBP9bln (above the GBP4.0-8.5bln MNI expected - although we had noted the top half of that range was likely) of the new 5.25% Jan-41 gilt. Spread set at 4.375% Jan-40 Gilt + 8.0bps (guidance was +8/8.5bps), books closed in excess of GBP128bln.

ESM syndication: Allocations

- E1bln WNG tap (We had pencilled in a E1.0-1.5bln range for this week's ESM transaction, but leant towards a E1.25bln size rather than the E1bln WNG announced) of the 2.75% Feb-35 ESM bond. Spread set at MS + 31bps (guidance was MS +34bps area), books in excess of E18.5bln (exc. JLM interest).

Netherlands auction results

- E2.125bln of the 0% Jul-31 DSL. Avg yield 2.376%.

Italy auction results

- E1.25bln of the 2.80% Dec-28 BTP. Avg yield 2.23% (bid-to-cover 1.78x).

- E2bln of the 2.35% Jan-29 BTP. Avg yield 2.36% (bid-to-cover 1.68x).

- E3.5bln of the 3.25% Nov-32 BTP. Avg yield 3.05% (bid-to-cover 1.54x).

- E1.75bln of the 3.85% Oct-40 BTP. Avg yield 3.87% (bid-to-cover 1.70x).

Germany auction results

- E5.5bln (E4.25bln allotted) of the 2.00% Dec-27 Schatz. Avg yield 1.91% (bid-to-offer 1.07x; bid-to-cover 1.39x).

SOFR: Net Long Setting Dominated In Front End Of SOFR Futures Strip On Monday

OI data points to net long setting dominating through the reds as SOFR futures ticked higher on Monday (only broken by net short cover in SFRZ5), reacting to the increase in Sino-U.S. trade tension.

- A more balanced mix of net long setting and short cover was then seen further out the strip.

| 13-Oct-25 | 10-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,429,965 | 1,421,986 | +7,979 | Whites | +46,490 |

SFRZ5 | 1,505,430 | 1,509,984 | -4,554 | Reds | +50,439 |

SFRH6 | 1,196,091 | 1,157,568 | +38,523 | Greens | +3,342 |

SFRM6 | 1,028,376 | 1,023,834 | +4,542 | Blues | -2,091 |

SFRU6 | 1,037,469 | 1,009,868 | +27,601 |

|

|

SFRZ6 | 1,046,188 | 1,045,109 | +1,079 |

|

|

SFRH7 | 811,353 | 793,456 | +17,897 |

|

|

SFRM7 | 780,578 | 776,716 | +3,862 |

|

|

SFRU7 | 676,469 | 677,721 | -1,252 |

|

|

SFRZ7 | 747,999 | 747,938 | +61 |

|

|

SFRH8 | 434,055 | 432,157 | +1,898 |

|

|

SFRM8 | 377,274 | 374,639 | +2,635 |

|

|

SFRU8 | 300,757 | 301,434 | -677 |

|

|

SFRZ8 | 331,518 | 333,395 | -1,877 |

|

|

SFRH9 | 193,294 | 194,209 | -915 |

|

|

SFRM9 | 172,931 | 171,553 | +1,378 |

|

|

US TSY FUTURES: Modest Positioning Adjustments On Monday

OI data points to a mix of net long setting (TU & TY), short cover (FV), short setting (UXY &S US) and long cover (WN) as Tsy futures twist steepened in holiday-thinned trade on Monday.

- There was no real movement in net curve-wide DV01.

| 13-Oct-25 | 10-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,613,433 | 4,584,997 | +28,436 | +1,110,898 |

FV | 6,718,630 | 6,740,383 | -21,753 | -953,158 |

TY | 5,395,260 | 5,392,735 | +2,525 | +171,686 |

UXY | 2,452,629 | 2,451,380 | +1,249 | +113,904 |

US | 1,924,764 | 1,920,026 | +4,738 | +616,103 |

WN | 2,059,001 | 2,063,485 | -4,484 | -860,178 |

|

| Total | +10,711 | +199,254 |

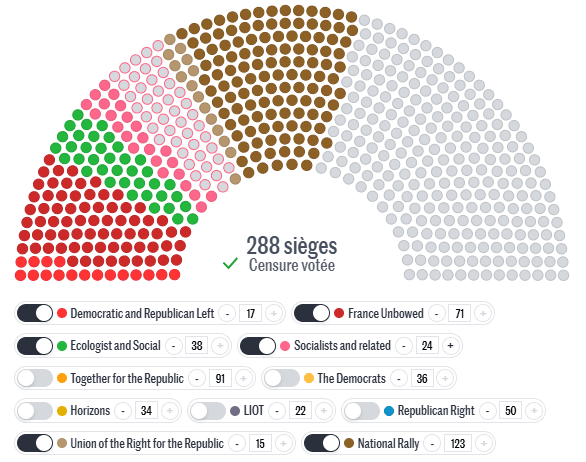

FRANCE: Censure Motions Against PM Go Before Parl't On 16 Oct; PS Stance Crucial

AFP reports that according to its parliamentary sources, censure motions against PM Sebastien Lecornu's second gov't, put forward by the far-left La France Insoumise ('France Unbowed', LFI) and far-right Rassemblement National ('National Rally', RN), are due to go before the National Assembly on Thursday, 16 October. It is viewed as unlikely that either of these censure motions reaches the required 288 votes to oust Lecornu.

- In recent censure motions, those put forward by the RN have generally failed to win support from other parties. The LFI motion could win the backing of the RN and its allies. However, even if the LFI motion can get the backing of the RN and its allies, as well as the Communist bloc and the Ecologists, this would amount to 264 deputies, short of the majority threshold.

- The actions of the centre-left Socialist Party (PS) will prove crucial. The PS has initially indicated that it will not back either the RN or LFI motion, condemning both to defeat. However, the PS' National Office holds a meeting at 13:00CET (07:00ET, 12:00BST), ahead of Lecornu's general policy statement due ~15:00CET (09:00ET, 14:00BST). The PS is set to decide on whether to present its own censure motion against Lecornu, and this could seal the PM's fate. A PS motion would likely go before the National Assembly on the evening of 16 Oct alongside the RN and LFI motions.

- A PS-led censure motion would almost certainly result in the swift removal of the second Lecornu gov't. Additionally, if just 24 of the 69 PS and PS-aligned deputies vote for the LFI censure motion, it would cross the majority threshold (see chart below).

Chart 1. Hypothetical Censure Motion to Remove Lecornu II Gov't

Source: Le Monde

JAPAN: Diet To Elect New PM 21 Oct; Intense Negotiations On PM Candidate Ongoing

The chairpersons of the House of Councillors' Diet Affairs Committees from the governing Liberal Democratic Party (LDP) and main opposition Constitutional Democratic Party (CDP) met earlier today and agreed on the convening of an extraordinary session of the National Diet on 21 October (likely to elect a new PM).

- Negotiations between parties are ongoing, with the LDP looking to secure the backing from the opposition to ensure the election of new party president Sanae Takaichi as PM. However, given the LDP lacks a majority in either chamber, the liberal CDP, libertarian-federalist Japan Innovation Party (Ishin), populist conservative Democratic Party for the People (DPFP), and centrist social conservative Komeito could unite to put their own candidate in the PM's office.

- LDP officials have met with counterparts from Ishin and the DPFP today in an effort to dissuade them from backing an alternative PM. Also today, the secretaries-general of the CDP, Ishin and DPFP meet to discuss their own prospects of putting forward a candidate to lead a coalition gov't.

- Ahead of the SG's meeting, DPFP leader Yurichiro Tamaki outlined his demands if his party, Ishina and the CDP are to form a gov't, saying "...it is essential that we agree on basic policies, and especially when it comes to security policy, [...]...If the three parties come together, they will be able to nominate the prime minister, but this will mean the birth of a new minority ruling party, so it will be difficult to run the government without continuing to gain the cooperation of the other parties and factions."

FOREX: Higher China Trade Tensions Help Pressure Risk; AUD Slides to New Lows

- Headlines confirming that China were ratcheting higher their controls on exports of rare earths provided a further dose of risk-off Tuesday, with markets clearly growing more concerned that global trade tensions will begin to hinder the global economy outside of just the US and China. Resultantly, AUD is in reverse, with AUDUSD making light work of Friday's lows to print the lowest level since mid-August. This narrows the gap with key support layered between the 0.6415 August 22 low and the 200-dma of 0.6423. Reports that Trump is looking to de-escalate the tensions have failed to help prop up markets.

- Infitting with the higher trade tensions, the USD is bid. The USD Index is yet to rally north of last week's highs, however further weakness in EURUSD would make this an inevitability. 99.563 is the level to watch, through which the dollar is at a new multi-month high.

- Similarly, USDCNH is bid - rate is through the 50-dma of 7.1452, but it's 7.1535 that marks the more salient level. It's worth noting last week's high in USDCNY & USDCNH came the session before the higher-than-expected CNY fix - which helped the course correction back down toward 7.12 in USDCNY.

- Renewed trade pressures have tipped EURUSD and GBPUSD to new pullback lows. GBP was already trading weaker on the back of a slower pace of change for private sector wages - helped reignite outside speculation that the BoE could look to cut rates again this year.

- Focus for the rest of today turns to the beginning of US earnings season, with Blackrock, Citigroup, Goldman Sachs, J&J, JPMorgan and Wells Fargo all due today.

OPTIONS: Expiries for Oct14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E537mln), $1.1500(E848mln), $1.1600(E663mln), $1.1650(E636mln)

- USD/JPY: Y151.50($691mln), Y152.00($751mln)

- AUD/USD: $0.6500(A$1.0bln), $0.6580-00(A$1.2bln)

- USD/CAD: C$1.4000-10($598mln)

COMMODITIES: Strong Start to the Week for Gold Reinforces Bullish Conditions

- A bearish theme in WTI futures remains intact. Last Friday’s move down confirmed a resumption of the bear leg - support at $60.40, the Oct 2 low, has been breached. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, initial key resistance is at $66.42, the Sep 29 high. Clearance of this level would highlight a reversal.

- A bull cycle in Gold remains intact and this week’s very strong start to the week reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4200.00 handle, and $4239.7, a Fibonacci projection point. Note that the trend is in overbought territory. A move down would be considered corrective and would allow the overbought set-up to unwind. Support lies at $3862.6, 20-day EMA.

EQUITIES: Recent Pullback for Eurostoxx 50 Futures Considered Corrective For Now

- The trend condition in Eurostoxx 50 futures is unchanged, the direction is up and the latest pullback is - for now - considered corrective. The key support zone to monitor is 5552.07 - 5478.12, the area between the 20- and 50-day EMAs. A clear break of the 50-day average would highlight a stronger reversal. On the upside, the bull trigger has been defined at 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend.

- A sharp sell-off in S&P E-Minis on Friday appears corrective - for now. The contract has found support below the 50-day EMA, currently at 6602.32, and last Friday’s low of 6940.25 has been defined as a key short-term support. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Sep 9 high. A breach of this hurdle would confirm a resumption of the uptrend.

| Date | GMT/Local | Impact | Country | Event |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 14/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/10/2025 | 1610/1210 | BOC Sr Deputy Rogers fireside talk in Vancouver | ||

| 14/10/2025 | 1620/1220 | Fed Chair Jerome Powell | ||

| 14/10/2025 | 1700/1800 | BOE Bailey Fireside Chat at Institute of International Finance | ||

| 14/10/2025 | 1925/1525 | Fed Governor Christopher Waller | ||

| 14/10/2025 | 1930/1530 | Boston Fed's Susan Collins | ||

| 15/10/2025 | 0130/0930 | *** | CPI | |

| 15/10/2025 | 0130/0930 | *** | Producer Price Index | |

| 15/10/2025 | 0430/1330 | ** | Industrial Production | |

| 15/10/2025 | 0600/0800 | *** | Final Inflation Report | |

| 15/10/2025 | 0600/0800 | *** | Final Inflation Report | |

| 15/10/2025 | 0645/0845 | *** | HICP (f) | |

| 15/10/2025 | 0700/0900 | *** | HICP (f) | |

| 15/10/2025 | 0740/0940 | ECB de Guindos at Single Resolution Mechanism Conference | ||

| 15/10/2025 | 0800/0900 | BOE Ramsden in Panel at Resolution Mechanism Conference | ||

| 15/10/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 15/10/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 15/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 15/10/2025 | - | *** | Money Supply | |

| 15/10/2025 | - | *** | New Loans | |

| 15/10/2025 | - | *** | Social Financing | |

| 15/10/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/10/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/10/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/10/2025 | 1330/0930 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1545/1645 | BOE Breeden in Panel on Financial Regulation | ||

| 15/10/2025 | 1610/1210 | Atlanta Fed's Raphael Bostic | ||

| 15/10/2025 | 1630/1230 | Fed Governor Stephen Miran | ||

| 15/10/2025 | 1700/1300 | Fed Governor Christopher Waller | ||

| 15/10/2025 | 1735/1335 | Kansas City Fed's Jeff Schmid | ||

| 15/10/2025 | 1800/1400 | Fed Beige Book | ||

| 15/10/2025 | 1800/2000 | ECB de Guindos at Alantra Anniversary Event | ||

| 15/10/2025 | 1800/1900 | BOE Breeden in Panel at Fintech Foundation |