MNI US MARKETS ANALYSIS - AUD Firms on Solid Election Result

Highlights:

- AUD gains on back of solid election results, ends consolidation phase

- Light markets as UK public holiday clips volumes

- Trump hints trade deals could come before Friday

US TSYS: Spring Holidays Dampens Volumes, Focus on Midweek FOMC

- Treasuries are running mixed on very light overnight volumes (TYM5 <190k) with multiple Spring holidays around the globe: Japan, China, HK, South Korea, as well as the UK, EU is open however.

- Focus on Wednesday's FOMC rate annc at 1400ET. The FOMC is expected to extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement.

- Monday data (prior, est): S&P Global US Services PMI final (51.4, 51.2), Composite (51.2, 51.2) at 0945ET; ISM Services Index (50.8, 50.3), Prices Paid (60.9, 61.4), New Orders (50.4, 50.0) & Employment (46.2, 46.0) at 1000ET.

- US Treasury auctions: $76B 13W & $68B 26W bill auctions at 1130ET followed by $58B 3Y Note auction (91282CND9) at 1300ET.

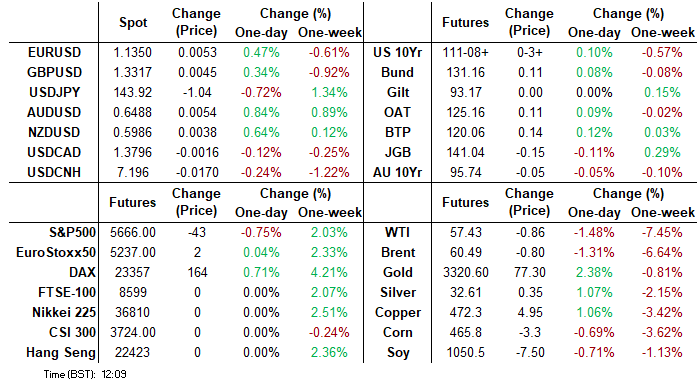

- Tsy Jun'25 10Y contract trades +3.5 at 111-08.5 (yld 4.3121, +.0038), lower half of narrow overnight range (111-06 low, 111-13.5 high). Curves twist steeper with Bonds lagging mildly firmer 2s-10s: 2s10s +2.636 at 50.868, 5s30s +2.664 at 89.544.

- Cross asset roundup: Bbg US$ index lower (-4.32 at 1220.19), Crude weaker (WTI -.70 at 57.59), Gold surges to 3313.22 (+72.73).

FED: MNI Fed Preview-May 2025: When In Doubt, Wait It Out

We've published our preview of the May FOMC meeting - Download Full Report Here

- The FOMC will extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement.

- It has been an eventful six weeks since the prior decision which included escalation and subsequent partial backtracking in US tariff policy, and the impact of uncertainty on economic sentiment (if not yet the “hard” data).

- As the FOMC awaits clarity in both government policy and the data on the degree to which one if not both dual mandate targets will be missed, most participants will continue to support a holding pattern until there is a clearer signal to act.

- A cut doesn’t look a likely prospect until July at least. Barring some unexpected developments, we would think that the median Committee member is only looking to cut later in the year, perhaps not before September.

- At the press conference, Chair Powell is likely to warn about the risks to both sides of the dual mandate, while saying something along the lines of "For the time being, we are well positioned to wait for greater clarity before considering any adjustments to our policy stance. We continue to analyze the incoming data, the evolving outlook, and the balance of risks."

- We don’t anticipate any meaningful changes in the Statement, though any signal that the Fed is looking seriously at “soft” survey data to assess the outlook could be significant.

LOOK AHEAD: Monday Data Calendar: S&P Services/Comp PMIs, ISM Services, 3Y Note

- US Data/Speaker Calendar (prior, estimate)

- 5-May 0945 S&P Global US Services PMI final (51.4, 51.2), Comp (51.2, 51.2)

- 5-May 1000 ISM Services Index (50.8, 50.3), ISM Prices Paid (60.9, 61.4)

- 5-May 1000 ISM Services New Orders (50.4, 50.0), Employ (46.2, 46.0)

- 5-May 1130 US Tsy $76B 13W & $68B 26W bill auctions

- 5-May 1300 US Tsy $58B 3Y Note auction (91282CND9)

SWITZERLAND DATA: CPI Details Point Towards Travel-Related Svcs; Overall Soft

Looking at the details of the April Swiss CPI print indicates that while the overall decline does appear broad-based, volatile travel-related services did have a particularly negative impact this time.

- While some of that might have the potential to reverse next time, the print remains soft - markets now price about a 1/4 chance of an outsized 50bp cut to -0.25% at the next SNB meeting in June, and EURCHF has seen some strength following the release, printing 0.9362 at typing. Initial resistance for the cross should stand at 0.9438, the April 28 high.

- Contribution to headline of travel-related services (airfares, hotels, package holidays, rental cars) was 0.145pp lower this time than in March - explaining the overall services contribution drop in full (see table).

- That appears a little surprising as in the Eurozone, national-level data released last week indicated that travel-related items were particularly firm in April this time amid the so-called Easter Effect - we might have expected some correlation there. One notable caveat here is that the Swiss M/M HICP print (which is being produced using standardized European methodology) was 0.7% - much higher than the 0.0% M/M CPI (which is the one the SNB focuses on).

FOREX: Greenback Edges Lower in Partial Reversal of Friday Rally

- The greenback is modestly softer against all others in G10, as markets partially retrace the phase of USD strength posted into the Friday close. EUR/USD is back above the $1.13 handle, which is helping support EUR/GBP above 0.8500. Trade deals and negotiations remain a key focus this week, as reports circulate deals could be announced by Friday. Japan, India and South Korea are seen among the nations with the most advanced negotiations.

- Meanwhile, after an extended period of consolidation, AUD/USD is gaining following the surprisingly strong showing for Anthony Albanese in the weekend's general elections. The price action puts the rate above the 200-dma and a close above would be the first since November last year. 0.6550 is the next key level here, marking the 61.8% retracement of the downleg posted off the late September low.

- JPY is among the strongest currencies in G10, benefiting from the modest pullback for US equity futures as well as firmer regional APAC currencies. The run higher in TWD has seen the central bank respond with a press conference today which, while not disclosing any new measures, saw the central bank talk down speculation that Taiwan would settle for a firmer currency at the request of the US.

- US ISM services data is the scheduled highlight Monday, with central bank speak quiet as the Fed remain inside their pre-meeting media blackout.

OPTIONS: Expiries for May05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1073(E2.4bln), $1.1100($1.5bln), $1.1120-25(E1.1bln), $1.1190-00(E2.0bln), $1.1285-00(E3.0bln), $1.1400(E636mln)

- GBP/USD: $1.3100-20(Gbp529mln)

- EUR/GBP: Gbp0.8525(E740mln)

- AUD/USD: $0.6500(A$509mln), $0.6550-60(A$1.0bln), $0.6635-45(A$1.1bln)

- USD/CAD: C$1.3865-70($2.6bln)

EQUITIES: Friday Rally Strengthens S/T Bull Cycle for Stocks

- The latest recovery in the e-mini S&P reinforces current bullish conditions.The contract has traded through the 50-day EMA, at 5620.87. A continuation of the bull phase would expose 5837.25 next, the Mar 25 high and a bull trigger.

- Eurostoxx 50 futures maintain a positive tone and Friday’s rally strengthens the current bull cycle. The contract has cleared both the 20- and 50-day EMAs, and attention is on 5263.01, a Fibonacci retracement point.

COMMODITIES: M/T Bearish WTI Trend Continues

- A medium-term bearish trend in WTI futures remains intact and last week’s sell-off reinforces this theme. The move down signals the end of the correction between Apr 9 - 23. Gold is trading closer to its recent lows and a corrective cycle remains in play for now.

- The yellow metal has breached the 20-day EMA. A continuation lower would highlight a deeper retracement and open the 50-day EMA, at 3115.11.

| Date | GMT/Local | Impact | Country | Event |

| 05/05/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/05/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 05/05/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 05/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 05/05/2025 | 1700/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 06/05/2025 | 0130/1130 | * | Building Approvals | |

| 06/05/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 06/05/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 06/05/2025 | 0545/0745 | ** | Unemployment | |

| 06/05/2025 | 0645/0845 | * | Industrial Production | |

| 06/05/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 06/05/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 06/05/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 06/05/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 06/05/2025 | 0900/1100 | ** | PPI | |

| 06/05/2025 | - | FOMC Meeting | ||

| 06/05/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 06/05/2025 | 1230/0830 | ** | Trade Balance | |

| 06/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 06/05/2025 | 1400/1000 | * | Ivey PMI | |

| 06/05/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result |