MNI US MARKETS ANALYSIS - ADP Watched Closely for NFP Clues

Highlights:

- ADP watched closely for NFP clues

- Europe happy to buy USD off lows, GBP/USD shows back below 1.3700

- ECB Sintra conference continues, with more members mentioning FX

US TSYS: Lower Ahead Of More Labor Data In Payrolls Build-Up

- Treasuries are lower across the curve, bear steepening as curves partly reverse yesterday’s bear flattening that was extended by a strong JOLTS report.

- Treasuries outperform EGBs but modestly underperform Gilts amidst fiscal concerns.

- Today sees labor market data in early focus with Challenger job cuts and ADP employment, the latter on a clear moderating trend in recent months, as a warm-up for tomorrow’s payrolls report (MNI Preview here).

- Cash yields are 1.2-4.7bp higher across the curve, with increases led by 30s.

- 5s30s has lifted to 95.5bps off a low of 93bps having pulled off last week's fresh ytd high of 103.3bps.

- TYU5 trades at 111-22 (-05+) on moderate cumulative volumes of 345k, having lifted a touch off session lows of 111-20+.

- A bull cycle remains in play although there was a sizeable reversal off yesterday’s high of 112-12+, which now forms initial resistance before 112-15+ (61.8% of Apr 7-11 sell-off). To the downside, firmer support is seen at 111-07+ (20-day EMA).

- Data: MBA mortgage applications (0700ET), Challenger job cuts Jun (0730ET), ADP employment Jun (0815ET)

- Fedspeak: Nothing scheduled

- Bill issuance: US Tsy $65B 17W bill auctions (1130ET)

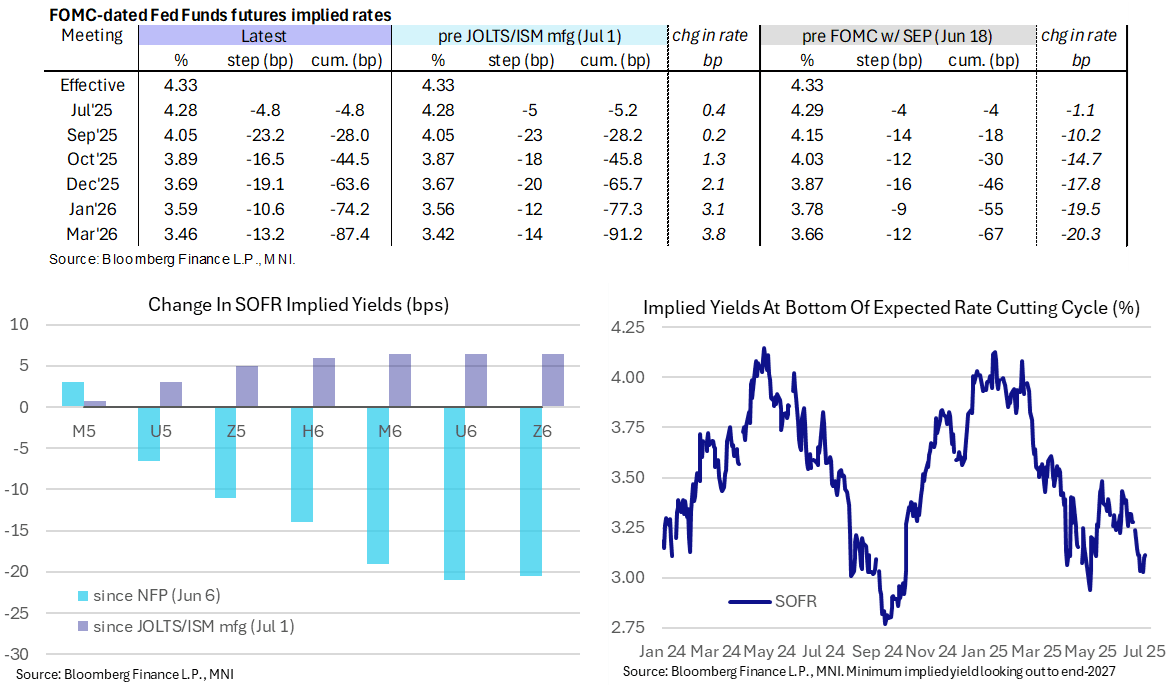

STIR: US Rates Consolidate JOLTS-Driven Shift Off Dovish Lows

- Fed Funds implied rates are up to 1bp higher on the day for 2025 meetings, at the top end of yesterday’s range after a strong JOLTS report helped extend a rates sell-off.

- President Trump has threatened Japan with tariffs of up to 35%, doubting whether the US will make a deal with Japan before the July 8 deadline.

- Cumulative cuts from 4.33% effective: 5bp Jul, 28bp Sep, 44.5bp Oct, 63.5bp Dec, 74bp Jan and 87bp Mar.

- The SOFR implied terminal yield of 3.115% (SFRZ6) is 1.5bp higher after yesterday’s 7bp lift off levels that had started to near lows since before the Presidential election in November.

- That’s a little under fully pricing 125bp of cuts from here by end-2026 compared to the 100bp of cuts envisaged by the median FOMC dot for end-2027 (including 75bp of cuts by end-2026).

- There’s no Fedspeak scheduled today, whilst data is mostly labor market focused with Challenger Job cuts (1230ET) and ADP employment (1315ET) for June.

US TSY FUTURES: Short Setting Most Prominent On Tuesday

OI data points to net short setting in FV through US futures on Tuesday.

- Modest net long cover was seen in TU futures, while it is hard to make any real inference when it comes to WN positioning, with the price of that contract unchanged on the day come settlement.

- Net short setting provided the dominant positioning impulse on the curve.

| 01-Jul-25 | 30-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,309,721 | 4,312,653 | -2,932 | -112,934 |

FV | 7,118,263 | 7,115,835 | +2,428 | +105,581 |

TY | 5,057,110 | 5,040,148 | +16,962 | +1,129,292 |

UXY | 2,444,155 | 2,429,002 | +15,153 | +1,334,227 |

US | 1,807,751 | 1,795,646 | +12,105 | +1,530,824 |

WN | 1,942,612 | 1,934,339 | +8,273 | +1,514,894 |

|

| Total | +51,989 | +5,501,885 |

SOFR: Mix Of Short Setting & Long Cover Seen In SOFR Futures On Tuesday

OI data points to a mix of net short setting and long cover through the SOFR blues on Tuesday, with JOLTS data and another firm reading for the prices paid component within the ISM manufacturing survey driving a hawkish repricing in the short end.

- The most meaningful adjustments came via net short setting in 3 of the 4 white contracts.

| 01-Jul-25 | 30-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,323,659 | 1,299,447 | +24,212 | Whites | +50,316 |

SFRU5 | 1,137,980 | 1,123,994 | +13,986 | Reds | -10,377 |

SFRZ5 | 1,266,096 | 1,273,285 | -7,189 | Greens | +7,569 |

SFRH6 | 982,151 | 962,844 | +19,307 | Blues | -6,023 |

SFRM6 | 870,329 | 861,826 | +8,503 |

|

|

SFRU6 | 829,539 | 832,446 | -2,907 |

|

|

SFRZ6 | 940,377 | 956,058 | -15,681 |

|

|

SFRH7 | 706,290 | 706,582 | -292 |

|

|

SFRM7 | 649,700 | 647,534 | +2,166 |

|

|

SFRU7 | 455,723 | 454,869 | +854 |

|

|

SFRZ7 | 409,837 | 410,377 | -540 |

|

|

SFRH8 | 310,797 | 305,708 | +5,089 |

|

|

SFRM8 | 230,270 | 233,200 | -2,930 |

|

|

SFRU8 | 204,922 | 205,032 | -110 |

|

|

SFRZ8 | 185,378 | 188,924 | -3,546 |

|

|

SFRH9 | 138,709 | 138,146 | +563 |

|

|

MNI Eurozone Inflation Insight – June 2025

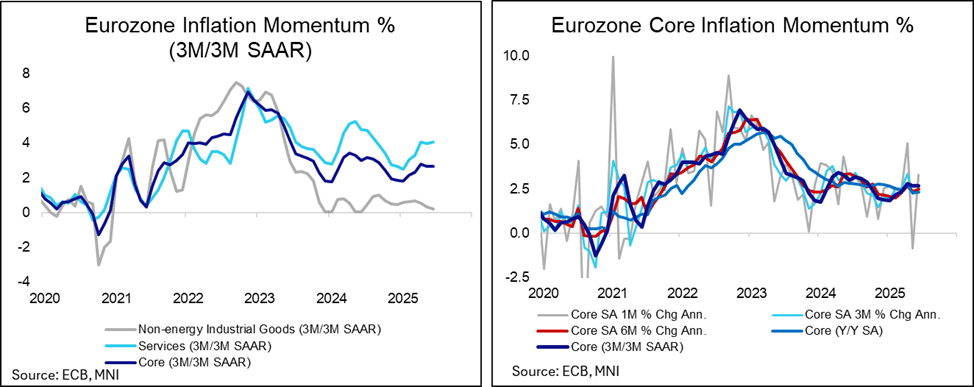

- Eurozone June flash headline HICP printed in line with expectations on Tuesday, at 2.0% Y/Y, slightly firmer than May’s 1.9%, while the core measure also confirmed consensus at an unchanged 2.3% Y/Y. The headline acceleration came as firmer energy inflation outweighed a marginal food/alcohol/tobacco slowdown.

- Particularly watched services HICP meanwhile was ever so slightly firmer than in May this time, providing a cleaner view on underlying pressures as easter and seasonality effects were not of major concern. The data for the category suggests some stickiness remains.

- Near-term ECB market-implied expectations currently stand around 50:50 implied odds for another 25bp cut by the September meeting. Any further repricing will likely hinge on any unexpected developments in the trade negotiations.

EUROPE ISSUANCE UPDATE:

Italy buyback results

The MEF has bought back E5bln of the following BTP/CCTeus:

- E1.25bln of the 3.80% Apr-26 BTP at 101.334.

- E1.00bln of the 1.60% Jun-26 BTP at 99.696.

- E0.89bln of the 3.10% Aug-26 BTP Short Term at 101.188.

- E0.62bln of the 1.25% Dec-26 BTP at 99.074.

- E1.24bln of the 0.50% Apr-26 CCTeu at 100.437.

UK auction results

- Solid 4.375% Mar-28 Gilt auction, as we had expected in our preview given recent performance for this line.

- The 0.1bp yield tail was the lowest this line has seen across seven auctions since November 2024 (prior average including the launch: 0.4bps, excluding the launch: 0.3bps).

- The 3.46x bid-to-cover ratio was also the second highest on record for this line (the April re-opening attracted 3.48x), notable given the step-up in size to GBP5bln.

- The lowest accepted price of 101.324 was above the 101.311 pre-auction mid. The secondary price of the Gilt reached a low of 101.291 just after the bidding deadline, but has since moved back up to 101.324.

- GBP5bln of the 4.375% Mar-28 Gilt. Avg yield 3.847% (bid-to-cover 3.46x, tail 0.1bp).

German auction results

- E6bln (E4.557bln allotted) of the new on-the-run 2.60% Aug-35 Bund. Avg yield 2.63% (bid-to-offer 1.24x; bid-to-cover 1.63x).

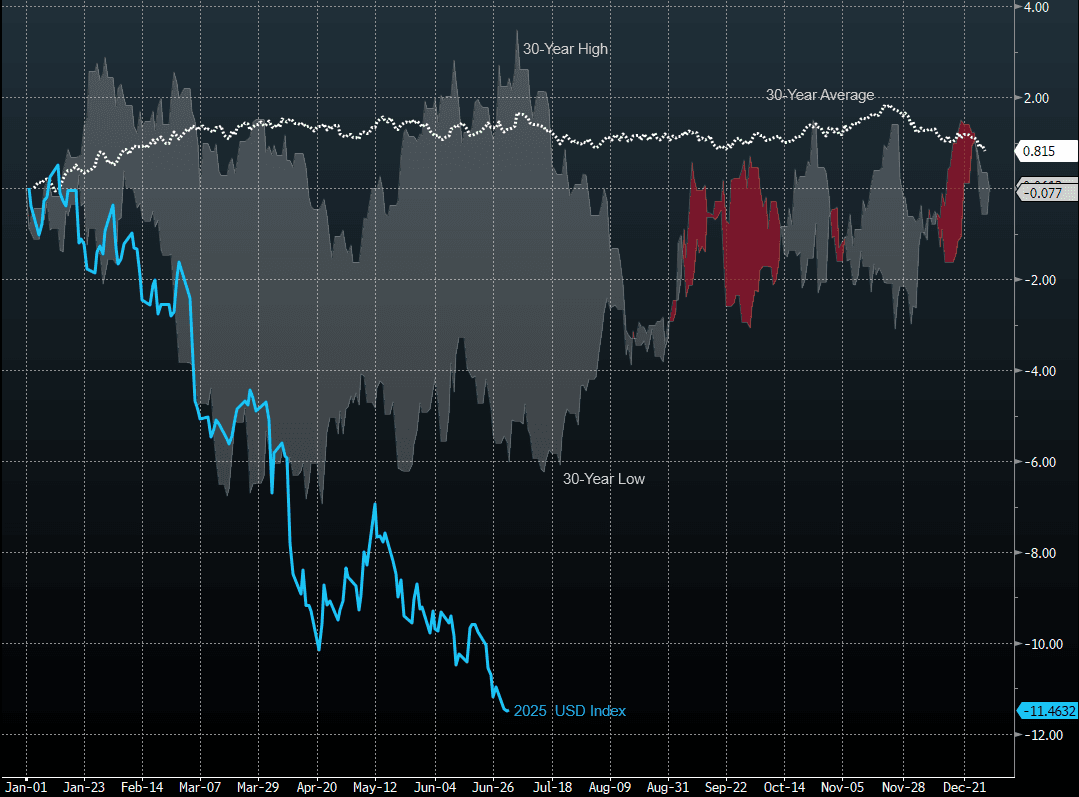

FOREX: Seasonality Sends Mixed messages, Shows July No Quiet Month for FX

- The USD Index has made a somewhat soft start to July, infitting with historical seasonal performance. Over the past 30 years, the USD Index has declined by an average of 0.25% in July, however never before has the dollar posted such a poor H1 return (-11%) - which leaves little historic precedent, or trend to follow through H2 (see below). While July is often a quieter month for financial markets - it's mid-table for the magnitude of returns, with August, September, June and March typically more muted.

- Historically, Scandinavian currencies outperform through July, with SEK and NOK posting average returns of +0.51% and +0.43% respectively, with JPY also a historic outperformer (+0.45%). In contrast, CAD and NZD trade most poorly through July, returning -0.21% and -0.06% respectively.

- On seasonality alone, this makes short CAD/SEK a viable candidate - and one of the best performing technical strategies of the past 12 months (all-in reversing 50-day EMA strategy: long on close above EMA, short on close below EMA) currently signals a winning short position to target congested support layered between 6.8042 - 6.8744.

Figure 1: USD Index YTD negative performance exceeds any other in past 30 years

Source: Blooomberg Finance L.P. / MNI

FOREX: AUDUSD Medium-Term Trend Bolstered This Week [1/2]

- Despite a softer-than-expected retail sales print in May, AUD weakness on Wednesday is more reflective of broader G10 declines as the dollar trades on a more stable footing. Two key factors have helped stabilise the greenback: the reversal higher for US yields from dovish extremes and an important technical support holding for the DXY, a trendline drawn across the 2011 and 2021 lows.

- Despite this, AUDUSD is broadly consolidating at more elevated levels following Monday’s break back above 0.6550 and subsequent extension to fresh recovery highs. Price action bolsters the medium-term bullish trend set-up, and sights remain on key resistance at 0.6688, the US election related highs.

- The RBA is more sanguine about the risk of a global slowdown than it was in May when it cut the cash rate by 25 basis points to 3.85%, with any trade-related impacts likely to take time to materialise domestically and as China shows resilience, MNI understands. The board will meet on July 8 – all surveyed analysts so far expect a 25bp cut to 3.60%.

FOREX: EURAUD Finds Congestion at 1.80, Notable Narrow Range for AUDJPY [2/2]

- The primary driver for the dollar will be Thursday’s US employment report, potentially placing an emphasis on AUD crosses to more cleanly reflect sentiment ahead of the data.

- It’s worth highlighting that the EURAUD rally has stalled in recent sessions, finding congestion ahead of the psychological 1.80 mark. Ongoing resilience for equities and the first murmurings from the ECB on the strength of the Euro could place the cross at a potential inflection point. Support here is seen at 1.7800, the 20-day EMA. Conversely, a break above 1.80 would signal scope for a more protracted rally targeting the April highs around the 1.85 mark.

- Separately, AUDJPY has been unable to benefit from the recent stocks outperformance, holding an eerily narrow range across the past two weeks. Should US labour market data disappoint, developments for both yields and equities could particularly weigh on AUDJPY. A close back below 94.00 might signal scope for a move back towards pivot support around 92.00.

BOE: Taylor: 5 cuts and neutral rate 2.75-3.00% - lower than other MPC members

Taylor is done talking for now on Bloomberg and the text of his Sintra speech is here (which was due at 11:30BST / 12:30CET).

- In this speech he reiterates the 5 cuts in 2025 that he said in the Bloomberg TV interview (mentioned above): "After some shocks and noise clouded my view of the economy and global developments in the first quarter, my reading of the deteriorating outlook suggested to me that we needed to be on a lower rate path, needing five cuts in 2025 rather than the market-implied quarterly pace of four."

- On the neutral rate Taylor says "I estimate the UK neutral real rate to be about 0.75 to 1 percent, putting the neutral nominal rate at around 2.75 to 3 percent"

- "Getting there, under our baseline scenario without further shocks, would take more time and a continued removal of restrictiveness in 2026 and 2027 as the economy returns to long-run real and nominal equilibrium."

- We note that estimate of 2.75-3.00% for the neutral rate is much lower than said by other MPC members recently.

FOREX: Europe Happy to Buy USD Off Lower Levels

- The greenback is on for a steadier start to the session, climbing off overnight lows as European markets are happy to buy the USD at lower levels. As a result, the USD Index is testing yesterday's highs to recoup ~0.5% off the pullback low. We continue to monitor the pierce of key long-term support at 96.55 - the trendline drawn from the May 2011 low - however, we note the oversold position does raise the possibility that either; a correction unfolds soon, or that the pace of the trend slows down, resulting in more volatile price action going forward.

- In contrast with Tuesday trade, JPY is the poorest performer in G10 as spot gravitates back toward the 50-dma. Nonetheless, the bear threat in USDJPY remains intact and Tuesday's sell-off reinforces this theme. The Jun 23 shooting star candle formation highlighted a reversal of the recent recovery and this signal remains in play.

- Meanwhile, GBP is softer off the new cycle high from Tuesday. GBP/USD has shown back below 1.37, with some selling pressure emanating from the failure of UK PM Starmer to press ahead with Welfare Reform in the House of Commons late yesterday. The UK Government continues to lose support among the voting public, and remains under pressure from their party MPs - extending a near-term phase of political uncertainty. EUR/GBP prints 0.8599 ahead of the NY crossover, the highest spot price since late April.

- ADP Employment Change data will be carefully watched later today. Market consensus looks for job gains of +98k over the month - and comes in the context of Powell's insistence that the FOMC are monitoring data very closely ahead of the July meeting, at which he refused to rule out policy action. The Whisper number for this Thursday's (brought forward by one day due to US market holidays on Friday) NFP headline has been trending lower, and now sits below consensus of 110k, meaning any positive surprise in ADP today could shift market perceptions.

- The ECB's Sintra policy conference continues. De Guindos, Cipollone and Lane are all set to speak, as well as BoE's Taylor - all before Lagarde makes the formal closing remarks of the conference at 1515BST/1015ET. The President has no public engagements set for Wednesday, but markets will be on watch for any further unscheduled comments on the incoming tariff regime. The President reaffirmed a 9th July deadline for a higher tariff set after April's delay - and said he is not considering any further rescheduling - placing more pressure on negotiating teams to reach a near-term settlement.

OPTIONS: Expiries for Jul02 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.0bln), $1.1650(E1.4bln), $1.1675(E1.2bln), $1.1700(E2.1bln), $1.1725-30(E1.1bln), $1.1775(E1.0bln), $1.1785-00(E3.0bln), $1.1900(E1.1bln);

- USD/JPY: Y143.00($555mln), Y143.99-00($648mln), Y144.75($699mln)

- USD/CAD: C$1.3800($1.2bln)

EQUITIES: Eurostoxx 50 Futures Holding Onto Bulk of Recent Gains

- Trend signals in Eurostoxx 50 futures remain bearish, however, the recovery from the Jun 23 low appears to be a reversal and the contract is holding on to the bulk of its most recent gains. Price has traded through the 20- and 50-day EMAs. A clear break of both averages would strengthen a reversal theme. This would open 5486.00, the May 20 high and bull trigger. On the downside, a breach of 5194.00, the Jun 23 low, would reinstate a bearish theme.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract has continued to appreciate, this week. Short-term resistance and a bull trigger at 6128.75, the Jun 11 high, has recently been breached. The clear break confirms a resumption of the uptrend that started Apr 7. The 6200.00 handle has been cleared too, this opens 6277.50, the Feb 21 high and bull trigger. Key support is at the 50-day EMA - at 5975.80.

COMMODITIES: WTI Futures Maintaining a Relatively Softer Tone

- WTI futures maintain a softer tone following the reversal from the Jun 23 high. Support to watch is at the 50-day EMA, at $64.64. It has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. On the upside, initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- Gold traded lower last Friday resulting in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low. A clear break of both support points would signal scope for a deeper correction - this would expose $3245.5, the May 29 low. The metal has recovered from Monday’s low and for now, this highlights a possible false trendline break. Stronger gains would refocus attention $3451.3, Jun 16 high. The bear trigger is $3248.7, the Jun 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 02/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 02/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 02/07/2025 | 1415/1615 | ECB Lagarde Gives Closing Sintra Remarks | ||

| 02/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 03/07/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 03/07/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 03/07/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 03/07/2025 | 0130/1130 | ** | Trade Balance | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 03/07/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 03/07/2025 | 0630/0830 | *** | CPI | |

| 03/07/2025 | 0700/0300 | * | Turkey CPI | |

| 03/07/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 03/07/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 03/07/2025 | 0830/0930 | Decision Maker Panel data | ||

| 03/07/2025 | 0830/0930 | BOE Credit Conditions Survey | ||

| 03/07/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 03/07/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 03/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 03/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 03/07/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 03/07/2025 | 1230/0830 | *** | Employment Report | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1230/0830 | ** | Trade Balance | |

| 03/07/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 03/07/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 03/07/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 03/07/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/07/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/07/2025 | 1400/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 03/07/2025 | 1400/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 03/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 03/07/2025 | 1500/1100 | Atlanta Fed's Raphael Bostic | ||

| 03/07/2025 | 1530/1130 | * | US Treasury Auction Result for Cash Management Bill | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 03/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |