MNI US Macro Weekly: War Shock Meets Weak Jobs Data

Mar-06 21:12By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

Executive Summary

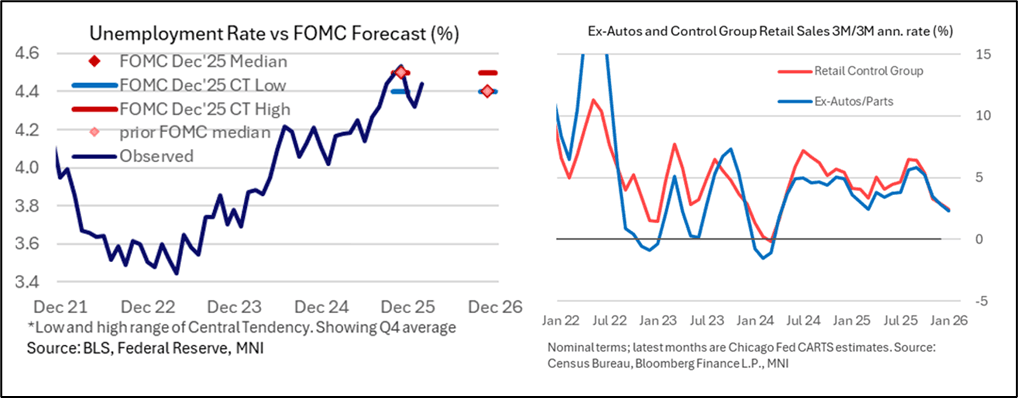

- In the key release of a tumultuous week that was overshadowed by geopolitical developments, both the establishment and household surveys disappointed in the February Employment report with a 92k NFP drop, an unemployment rate rise to 4.44%, and large lower revisions.

- But survey quirks and one‑offs complicate interpretation and it comes after a relatively solid January report. As such it doesn't appear to have greatly impacted FOMC participants' overall views on the rate outlook as we head into the pre-March FOMC blackout period.

- Indeed it sounds as though all of the FOMC participants will have to weigh the surprisingly soft report alongside the potential macro implications of the conflict in the Middle East before coming up with a synthesis and forming March SEP projection updates.

- Soaring energy prices and broader market uncertainty over the war in the Middle East started over the weekend saw rate cut pricing evaporate. Cumulative pricing at one point suggested that a rate cut would have to wait until after the September FOMC, having last Friday pointed to about a 50/50 chance of a second 25bp cut by that point (after July).

- End-2026 pricing briefly touched ~32.5bp of cuts in the hour prior to the release of the February employment report, a 28bp repricing vs prior to the US-Iran conflict. The unexpected drop in payrolls and uptick in the unemployment rate was enough to bring a September rate cut to fully priced (29bp), even if a cut as soon as July remained slightly elusive.

- Otherwise, data were mixed. Import prices remained firm, with ex‑petroleum import prices posting their strongest four‑month stretch since 2024 amid tariff effects and fading China concessions.

- Growth indicators softened, with GDPNow falling to 2.1% on weaker expected consumption. Business surveys diverged: ISM Manufacturing held gains but saw a sharp jump in Prices Paid, while ISM Services surprised strongly with broad‑based strength and cooling prices; S&P PMIs pointed to ~1.5% Q/Q growth.

- Retail sales and consumption signals were mixed, with headline and category breadth softening despite a modest Control Group gain.

- The week ahead features key inflation releases, with February CPI (Wed) and January PCE (Fri) central to shaping expectations before the March 17–18 FOMC meeting and new SEP; additional data in the week to come include GDP revisions, JOLTS, durable goods, and housing indicators.