MACRO ANALYSIS: MNI US Macro Weekly: War And PCE

We've just published our US Macro Weekly - Download Full Report Here: https://media.marketnews.com/U...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Trump Remarks In Kentucky Underway Shortly

US President Donald Trump is shortly due to deliver remarks on the economy at an order fulfilment centre in Kentucky. LIVESTREAM While the speech has been billed as focusing on 'affordability,' Trump is likely to speak broadly on a range of issues, including the Iran war.

- Politico noted this morning that the Trump administration had been hoping for good monthly inflation numbers to bolster his economic agenda, "Unfortunately, they’ll also be well out of date — and here’s the inflation stat people really care about: Gasoline in the Cincinnati area was $2.64 a gallon on average this time last year, per the AAA. A week ago it was $2.97. Today it’s $3.43.”

- Republican pollster Tony Fabrizio told White House officials last month that Trump’s prescription drug initiative, TrumpRx, is likely to be a vote-winner in November, so expect Trump’s remarks to tout the programme.

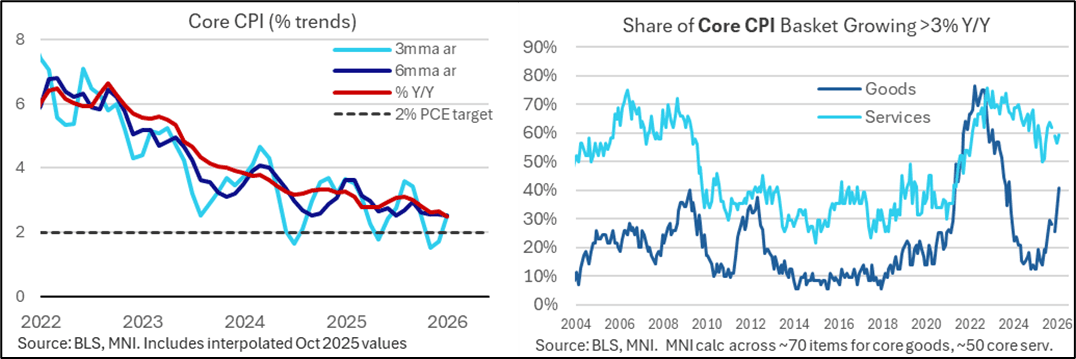

US INFLATION: MNI US Inflation Insight: Mind The PCE Gap

We've published our latest US inflation Insight - Download Full Report Here

- February’s CPI aggregates came in broadly in line with expectations, though the underlying details will have appeared less encouraging from the Fed’s perspective.

- Unrounded core CPI printed at 0.216% M/M (vs MNI median 0.24%) and headline at 0.267% M/M (vs 0.27%).

- Core Y/Y of 2.46% remained at a rounded 2.5% as per consensus, while rounded headline CPI held at 2.4% Y/Y (2.41% vs 2.4% median), the lowest since May.

- The details mattered though: analysts lifted Feb core PCE estimates to ~0.39% M/M (range 0.31–0.45) vs closer to 0.25% pre-CPI, citing in part stronger core goods components with heavier PCE weights.

- Core goods inflation printed a slightly below-expected 0.08% M/M with large category swings; ex‑used vehicles inflation cooled, while median core goods inflation fell sharply after January’s tariff‑related jump.

- Supercore CPI (ex-housing core services) cooled to 0.35% M/M (from 0.59%) but was still slightly hotter than expectations. The PCE translation from key categories were more punchy than the overall CPI data.

- The three‑month core CPI run rate rose to 3.0% annualized while the six‑month pace eased to 2.3%, suggesting mixed underlying momentum.

- Inflation breadth widened by MNI’s estimates: 50% of the CPI basket rose 3%+ Y/Y, and core goods breadth reached 42%, the highest since Oct 2023. That said, regional Fed estimates of stickiness and dispersion showed continued disinflation over a longer-term horizon.

- Key to FOMC doves’ overall disinflation narrative is housing CPI which moderated again, with OER at 0.22% M/M and primary rents at 0.13% M/M; softness was concentrated in the South region.

- Food prices reaccelerated, with food-at-home at 0.44% M/M and food-away-from-home at 0.32% M/M (a positive driver of core PCE); energy saw modest recovery ahead of the March shock.

- Due to government shutdown-related delays we still don’t have the January PCE release, which comes Friday March 13. February’s PCE drops on April 9, well after the Fed’s next decision on March 18.

- Of course even the latter would be considered somewhat stale given the significant inflationary impulse implied by spiking energy prices amid the Middle East conflict.

- Market rate expectations moved slightly hawkish on the day, with cumulative 2026 cuts repriced from 36bp to 32bp in the hours after the CPI release, and the next cut now seen in October rather than September pre-release.

EURJPY TECHS: Key Support Remains Intact

- RES 4: 186.87 High Jan 23 and a key M/T resistance

- RES 3: 186.36 High Feb 9

- RES 2: 185.05 76.4% retracement of the Feb 9 - 12 bear leg

- RES 1: 184.77 High Feb 25 and a short-term bull trigger

- PRICE: 183.84 @ 17:06 GMT Mar 11

- SUP 1: 182.90/03 Bull channel from Feb 28 ‘25 low / Low Mar 03

- SUP 2: 180.81 Low Feb 12

- SUP 3: 180.10 Low Dec 5 ‘25

- SUP 4: 179.30 23.6% of the Feb 28 ‘25 - Jan 23 bull cycle

EURJPY has recovered further from recent lows. Key support at 182.90, the base of a bull channel drawn from the Feb 28 ‘25 low, remains intact. A clear channel breakout is required to signal a stronger reversal and would open another key support at 181.81, the Feb 12 low. For bulls, initial resistance to monitor is unchanged at 184.77, the Feb 25 high. Clearance of this hurdle would highlight the resumption of a fresh bull wave inside the channel.