MNI US Inflation Insight: Core Relief Overshadowed By Energy

Apr-10 19:57By: Tim Cooper and 1 more...

Inflation+ 1

Download Full Report Here

March CPI undershot expectations on core measures, though the energy price shock due to the conflict in the Middle East came through clearly in a soaring headline inflation reading and more subtly across some energy-sensitive categories. Core CPI printed 0.196% M/M (vs consensus 0.27%) and 2.60% Y/Y (vs 2.7%), while headline CPI surged 0.865% M/M and 3.26% Y/Y

- Underlying momentum was mixed, with recent core trends easing but still elevated. Three‑month core CPI slowed to about 2.9% annualized, while the six‑month pace came in at ~2.3%, partly biased lower by government shutdown distortions earlier in the year.

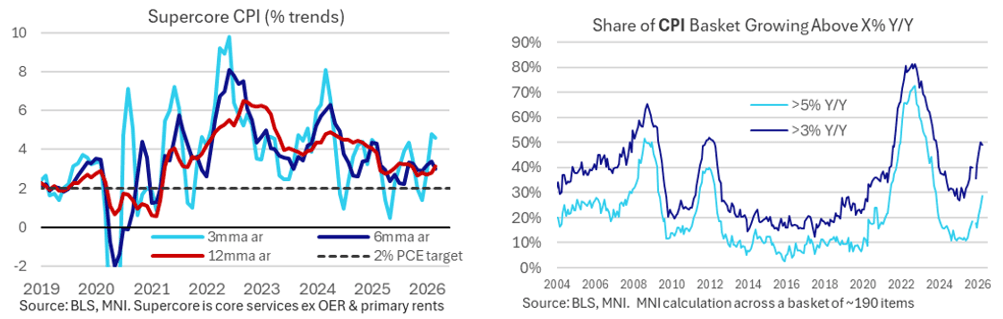

- Supercore inflation cooled meaningfully but remains a key area of concern: it slowed to 0.18% from 0.35%, down sharply from prior months, yet its three month annualized rate remains elevated around 4½%+.

- Housing inflation continued to moderate, supporting the Fed’s longer‑term disinflation narrative.

- Core goods inflation softened again despite tariff‑related pressures earlier in the year. Core goods rose only ~0.1% M/M, dragged down by another decline in used car prices, while median core goods inflation posted a second consecutive soft reading following January’s tariff‑related surge.

- Inflation breadth widened, mainly due to energy, but longer‑term dispersion signals are improving. About half of the CPI basket is now rising at 3%+ Y/Y, though some measures (Cleveland Fed median, trimmed mean) continued to trend lower on a Y/Y basis, offering a glimmer of gradual longer‑term disinflation.

- CPI details had mixed implications for core PCE, with downside and upside risks offsetting. Analysts trimmed March core PCE estimates slightly (median ~0.22% M/M), though volatile categories such as legal services and strong PCE‑weighted core goods remain key forecast risks pending PPI data.

- Beyond the immediate knee-jerk reaction, pricing reverted to trade roughly around pre-data levels. In the half-hour following the release, FOMC-dated OIS effectively showed no change over the next 3 meetings and a cumulative 9bp of cuts through year-end.