MNI US Macro Weekly: War And PCE

Apr-10 20:26By: Tim Cooper and 1 more...

US+ 1

Download Full Report Here

Executive Summary

- While a ceasefire in the Middle East war was announced this week, the implications of the related energy and supply chain shocks are just beginning to show in the data.

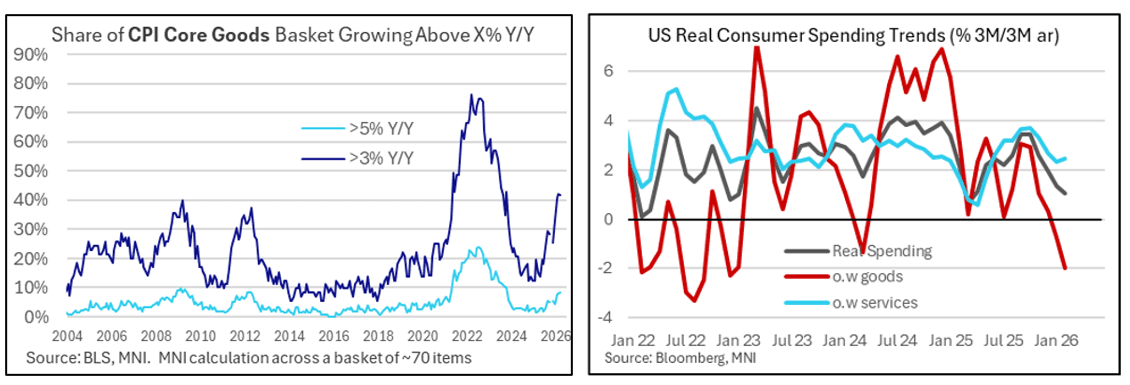

- In the week’s key release, March CPI undershot expectations on core (0.20% M/M vs 0.27% consensus) but headline surged on energy, printing 0.87% M/M. At best, any disinflation narrative coming into the year remains extremely fragile, with energy leaving inflation dispersion metrics elevated.

- Implications for core PCE are mixed, with risks on both sides. Analysts trimmed March core PCE estimates modestly (median now ~0.22% M/M) following the CPI release, though questions over some PCE‑specific categories—particularly legal services—remain a key downside risk pending next week’s PPI. Core PCE inflation remains stubbornly firm near 3.0% Y/Y, with recent run rates closer to 4% annualized.

- Inflation has been taking a bite out of consumption, with latest data showing nominal resilience but less impressive volumes. February PCE showed solid nominal spending, but real consumption growth slowed, with goods volumes flat to negative and services carrying growth almost alone. Overall, real consumption momentum is decelerating despite tax refunds offering something of a tailwind.

- Against this backdrop, Q1 growth tracking remains subdued, but with an unusual mix of drivers: the Atlanta Fed GDPNow estimate of ~1.3% Q/Q SAAR, sees business equipment investment contributing more to growth than consumption. The Dallas Fed WEI corroborates a 1.3–1.5% Q1 growth signal, pointing to modest domestic demand momentum overall.

- And labor market indicators remain consistent with “low hire, low fire.” Weekly ADP showed improving job growth, and continuing claims continued to trend lower, suggesting labor market resilience. However, survey data show rising worker pessimism and muted hiring.

- With markets focused on the degree of concern over energy pressures spilling into broader inflation, it was noteworthy that the latest FOMC minutes suggested more participants in March saw potential for the next move being a hike (compared with January's meeting).

- That said, while Fed rate pricing swung with ceasefire headlines, they ended little changed. Markets briefly priced a more dovish Fed following the US‑Iran ceasefire announcement, but much of that move reversed as the truce appeared tenuous. By week’s end, pricing implied only 5–6bp of cuts through end‑2026.

- While attention this weekend will firmly be on peace talks in Pakistan, the week ahead is headlined by March PPI, crucial for refining core PCE expectations. Other items of note include import/export prices, and several Fed speaker appearances ahead of the pre-meeting blackout period starting next weekend.

Trending Top

May-22 16:54