MNI US Macro Weekly: Still Bracing For Impact

Jun-06 19:23By: Tim Cooper and 1 more...

Federal Reserve+ 1

Download Full Report Here

EXECUTIVE SUMMARY

- The past week delivered another mixed set of data that maintained the theme of underlying economic momentum likely weakening over the course of Q2, but not to a dramatic extent.

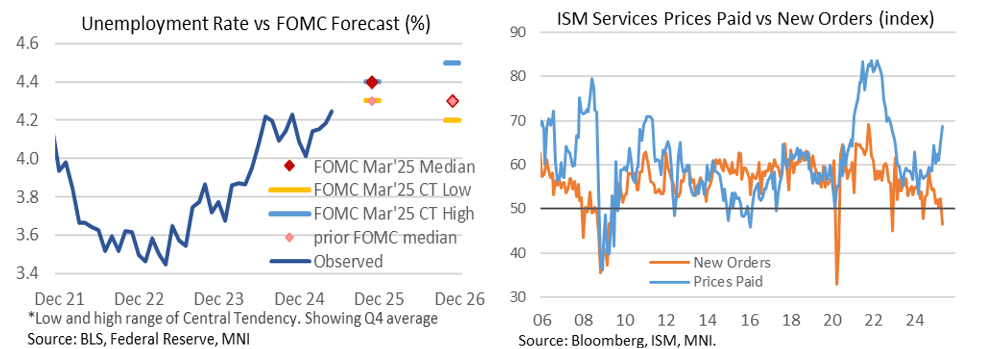

- The key release was the May Employment Report, which saw nonfarm payrolls growth modestly beat expectations. And despite downward revisions to prior months and another uptick in the unrounded unemployment rate, MNI (and markets) saw the report vindicating further patience on cuts from the Fed.

- Both the ISM Services and Manufacturing surveys disappointed, leaning toward the stagflationary side. Retail sales were mixed, with the weekly Redbook showing solid results while auto sales were poor. Furthermore, factory orders and construction spending implied a weaker outlook for those sectors.

- Confounding the signal was a collapse in the trade deficit in April as tariff front-running reversed, while the Atlanta Fed's GDPNow estimate for Q2 briefly exceeded 4%. Note the composition of that GDP estimate though: net exports will definitely be a strong upside contributor, and personal consumption will pick up from Q1, but investment (both fixed and inventories) appears to be pulling back.

- Fed officials continued to call for patience on the rate path. While an easing bias ostensibly remains, we couldn’t help but notice hints from officials like Philly Fed's Harker that the 'direction of travel' for policy is also a consideration amid significant uncertainty.

- While the data so far have been ambiguous, FOMC members appeared to agree that the full impact of tariffs was yet to be seen, particularly on the inflation front. The latest Beige Book likewise noted that while prices had picked up at a moderate pace since the April edition, there were “widespread reports of contacts expecting costs and prices to rise at a faster rate going forward.”

- There’s one last major release before the June FOMC: next week’s US macro calendar is headlined by CPI Wednesday, with the Fed currently not expected to cut rates again until October.

- The Bloomberg survey sees core CPI at 0.3% M/M after 0.24% M/M in April. That didn’t translate into core PCE inflation last month, at 0.12% M/M, although some tentatively look for that to switch this month in part on strength in portfolio management and investment advice prices after April’s weakness.