MNI US Macro Weekly: Poor Payrolls Trumps Patient Powell

Aug-01 2025 19:31By: Chris Harrison and 1 more...

Federal ReserveUS

Hidden PDF

Executive Summary

- The second half of the week has seen some significant moves in markets from first a patient Fed Chair Powell not giving a nod to a September rate cut before a weak payrolls report with huge downward revisions materially altered recent trends.

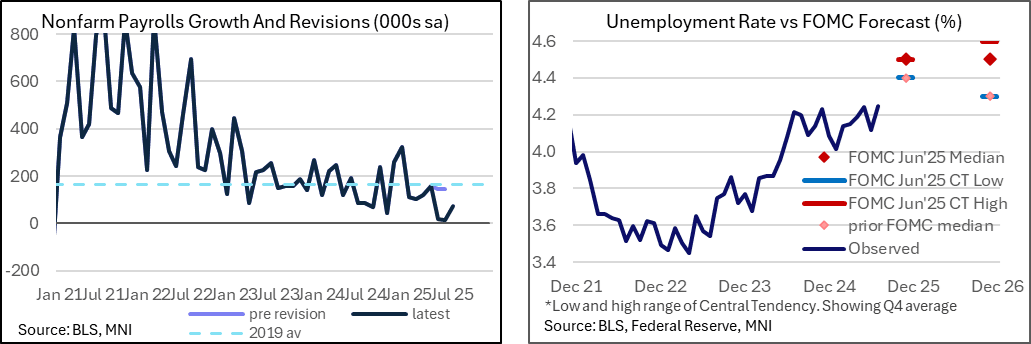

- Nonfarm payrolls growth underwhelmed at 73k in July but the major headline was the -258k two-month downward revision, of which -139k came from the private sector and -119k from the public sector. Outside of April 2020, that’s the largest two-month downward revision in at least forty-five years.

- We caution though that whilst jobs growth has soured sharply, it’s doing so along with a significant slowing in labor supply under immigration curbs.

- As such, the unemployment rate may have technically ticked up to a new cycle high of 4.248% (above 4.244% in May) but it continues to roughly plateau in the 4.0-4.25% range seen since last July. The median FOMC forecast from the June SEP had the unemployment rate increasing to an average 4.5% in 4Q25 as part of forecast with two rate cuts in 2025 so further deterioration would be expected.

- A note on the latest initial jobless claims data, which are back at 2019 averages, a period when the unemployment rate averaged 3.7%.

- The weak report prompted an extraordinary response from President Trump, directing his team to fire BLS Commissioner Erika McEntarfer. It’s a broadening out of criticism beyond the Fed’s Powell and its Board.

- Speaking after payrolls, Atlanta Fed’s Bostic (in a non-voting role this year) said he hasn’t changed his view that there should be just one rate cut this year.

- Elsewhere in a major week for data, core PCE inflation exceeded latest Fed tracking in June at 2.8% Y/Y, whilst away from any tariff impact, market-based services inflation printed 3.3% Y/Y. Various inflation metrics showed a continued stabilization at above 2% target rates.

- The Q2 GDP advance release meanwhile beat analyst expectations with 3.0% annualized although it was close to Atlanta Fed GDPNow expectations. PDFP moderated further to 1.2% annualized for its weakest since 4Q22 although could have been worse.

- As a precursor to next week’s ISM Services report, the Manufacturing counterpart was weak across the board in July. Prices paid pulled back from recent highs, new orders chalked up a sixth consecutive month firmly in contraction territory and the employment index fell to its lowest since mid-2020.

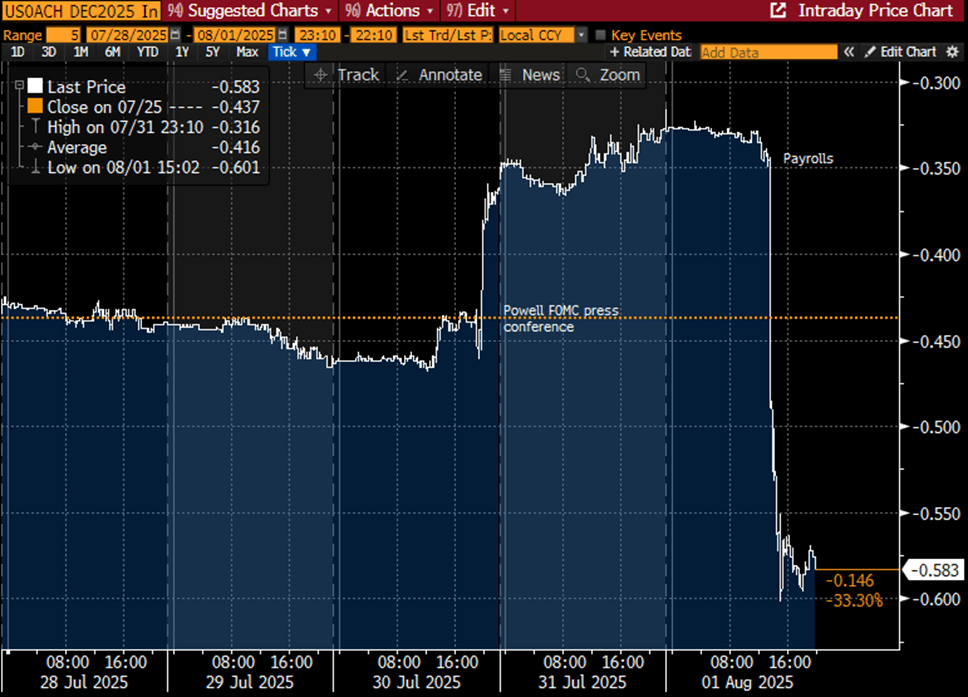

- Yields have tumbled after the weak payrolls report. A September cut is mostly priced now vs 50/50 before the release, with a cumulative 59bp by year-end and five cuts in total from current levels.